PGR: Progressive (3)

Recap

We have written a valuation piece about PGR in May 2024, recommended a buy at market value of $122b, so far the results have been great. In this article, we want to explain more about the auto insurance industry and how we think about forward returns.

For the past 38 years, PGR stock has returned a CAGR of 17% while only having three CEO changes: Peter Lewis (1965-2000), Glenn Renwick (2001-2016), and Tricia Griffith (since 2016).

PGR structurally low costs and the large, fragmented auto insurance market suggest that the company still has a long runway.

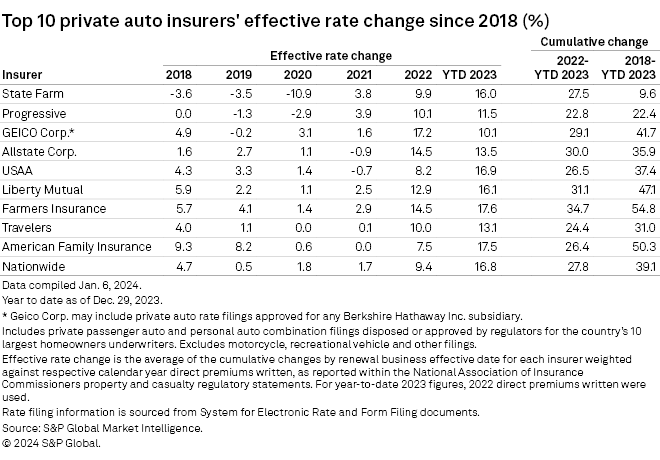

Industry

Auto insurance is required by law, which makes it an attractive, non-cyclical market. Consumers typically purchase auto insurance based on price, brand awareness, and an agent’s advice. Since policies are more or less the same everywhere, price is the biggest differentiator. A low cost structure allows insurers to offer cheaper policies, which turns out to be a major competitive advantage.

The US auto insurance market is mature and growth is only likely to match inflation. However, the market is fragmented, with the largest player, State Farm, having 18% share. PGR (15% share) and GEICO (12% share), the industry’s two low-cost operators, have consistently gained share over the years and are likely to continue doing so.

How Insurers Make Money

Insurance companies make money in two ways: underwriting and investing. Since insurance premiums are paid up front, insurers can invest the premiums until they pay out a claim. If they collect more premiums than they pay out in claims and expenses, they earn underwriting profits.

Because of the fact that insurers can earn investment income, the auto insurance industry as a whole can afford underwriting losses. They rely on investing to turn a profit.

PGR is one of the exceptions. Since 2010, it has averaged a 7.5% underwriting profit margin with no losses. Only GEICO has a similar track record.

The combined ratio measures this underwriting profit margin. It is the sum of loss ratio and expense ratio.

1. Loss ratio = current and future claims / net earned premiums

2. Expense ratio = operating expense / net earned premiums.

PGR aims for a long run average of 96% combined ratio (4% underwriting margin) while growing as fast as possible. Historically, it achieved a better average of 93%.

There is a trade-off between profitability and growth. The higher the combined ratio, the cheaper the policies are to consumers: low prices drive growth. This means that underwriting profits decrease when growth increases.

Insurance is an unusual industry in that rapid growth is usually bad as it suggests the insurer has mis-priced their risk. PGR thinks a 96% combined ratio strikes the right balance between profitability and growth.

Direct Sales Channel

In a commodity business like auto insurance, the operator with the lowest costs usually wins. They can price below their competitors’ breakeven and still earn a profit. PGR has a cost structure that’s lower than all of its competitors except GEICO.

On average, GEICO has lower expense ratio of ~5% but higher loss ratio of ~8%, so GEICO net combined ratio is higher than PGR by ~3%.

An insurance company’s sales channels have the largest effect on expense ratio. GEICO has a low expense ratio because 100% of its business is written directly over the phone and internet. GEICO has no agents to pay a commission or salary.

For example, Allstate has a higher expense ratio because it relies 100% on agents to write its policies. They need salaries, commissions, health care, office space, etc.

PGR runs a mix with 42% of premiums direct and 58% through independent agents. Most insurers pay independent agents 15-20% commission, PGR only pays 10%.

This minimizes costs but can create a conflict of interest for the independent agent. If the agent can sell a different policy that’s only slightly more expensive, they can earn significantly more commissions. As a result, PGR has a lower policy retention rate.

Why Doesn’t Everyone Sell Direct?

It comes down to incentives. Companies with captive agents like Allstate would lose alot of business if they started undercutting their own agents and dealing directly with customers.

PGR was able to introduce a direct offering despite its independent agents because:

1. They already paid below-average commissions, which disincentivized agents from selling their policies unless PGR was their only option.

2. PGR writes a lot of policies to high-risk drivers who have few other options.

3. PGR provides its independent agents with better technology (platform, processes, quotations). Competitors don’t seem to see the need to invest in such technology.

In other words, PGR was able to build a direct sales channel because its independent agents had no choice but to continue doing business with it.

Today, the direct sales channel is highly consolidated, with just three companies carrying more than 75% share. GEICO leads with about 45%, while PGR and USAA have about 20% each. USAA only writes insurance for military members, which limits their potential growth. GEICO is therefore the most important competitor.

Over time, PGR sales mix will continue shifting towards its direct channel. This should cause the expense ratio to converge with GEICO. As the low-cost leaders, these two companies will continue to take market share and should eventually become the #1 and #2 insurers.

Economies of Scale

Scale is another factor affecting expense ratios. Insurers that write more premiums can spread cost across a larger base. In 2023, PGR spent the most on advertising among the major auto insurers (PGR $1.2b, GEICO $838m, State Farm $992m, Allstate $651m).

Although State Farm has written more premiums than PGR and GEICO, it spent less on advertising because it has to pay sales agents.

Matching Price to Risk

In 2008, PGR began using telematics to help price their risk. Drivers can elect to use PGR’s Snapshot device to measure their driving habits in exchange for a discount. Over the years, PGR has collected extensive amounts of driving data, which it uses to segment its customers and price risk more granularly. GEICO was slow to adopt telematics and has consistently reported higher loss ratios compared to PGR. Finally in 2019, GEICO started their own telematics program.

Underwriting Leverage

Most insurers typically write 1 to 1.5x to equity. PGR writes at 2.8x, they are able to do so because of the incredible ability to produce underwriting profits.

However, this is also a big source of risk if PGR makes above 100% combined ratio. A 105% combined ratio at 2.8x leverage will reduce equity by 14% assuming no debt.

Capital Allocation

In 2007, PGR implemented a variable dividend policy. Rather than pay a steady quarterly sum, PGR uses a formula to relate its business performance to its dividend. This is a highly rational policy which we don’t see in corporations.

PGR aims to offset stock-based compensation with stock repurchases. We contend with this policy as repurchases should be done when shares are trading at below intrinsic value.

Since 2005 shares outstanding have shrunk 2.5% per year.

Forward Returns

We want to calculate a baseline rate that PGR can grow intrinsic value.

If PGR earns its target 96% combined ratio and leverages 2.8x to equity, it should earn ~11.2% ROE from underwriting.

Investment portfolio yields ~2.5%.

Expected ROE = 11.2%+2.5% = 13.7%.

Assume PGR continues reinvesting 80% of its FCF at ROE of 13.7%, then intrinsic value will grow at 11% per year.

Add 2.5% for repurchases and average 1.8% dividends. The pre-tax expected total return is ~15%.

Potential upsides:

PGR actually does better than 96% combined ratio.

Moving to direct selling.

Improving retention rate.

Today, PGR trades at trailing PE multiple of 21x. We don’t find this cheap enough to realize the forward returns of 15%.

There is no magic number on what is a “cheap multiple”, but we should be comfortable purchasing at below 16x.