MKL: Markel (4)

Update Q2 2024: MKL is Still Good Value

Q2 2024 earnings reported another fine quarter, these are the YTD highlights:

Net earned premiums grew YOY +5%.

Combined ratio at 94.4%, worsening by 1% from last year due to reinsurance.

Net investment income increased to $438m from last year $328m.

Non-insurance segment (Ventures) grew operating income by +7% to $281m (op margin 10.8%).

Acquisition for 98% of Valor Environmental. It’s a company providing erosion control and related services to commercial development sites and homebuilders in US. The $156.4m transaction was paid fully by cash.

Shares repurchase worth $97m in Q2 at average price $1,537. Total YTD cash used for repurchases was $260m, about 1.3% of market cap.

Insurance float grew to $14.8b from $14.3b at year end 2023.

Despite a larger float size, continued profitable underwriting, earnings growth in Ventures, higher fixed income yields… MKL share price fell -4%.

Recall the last valuation we did in Q1 2024:

Since Q1, shareholders’ equity grew from $15b to $15.9b (+$0.9b), while market cap only increased by +$0.7b.

We don’t need to do the math again to appreciate that the economics of MKL has improved, but the market value has not proportionally increased.

Therefore, we purchased a substantial amount at $1,560 per share, raising our allocation to 26%. This is our second largest holding behind Berkshire.

We love the consistency in the business, MKL’s management does not aim for big gains but they do a little better than average over a long period of time.

Economic Moat

The economic moat of MKL can be summarized into 3 factors:

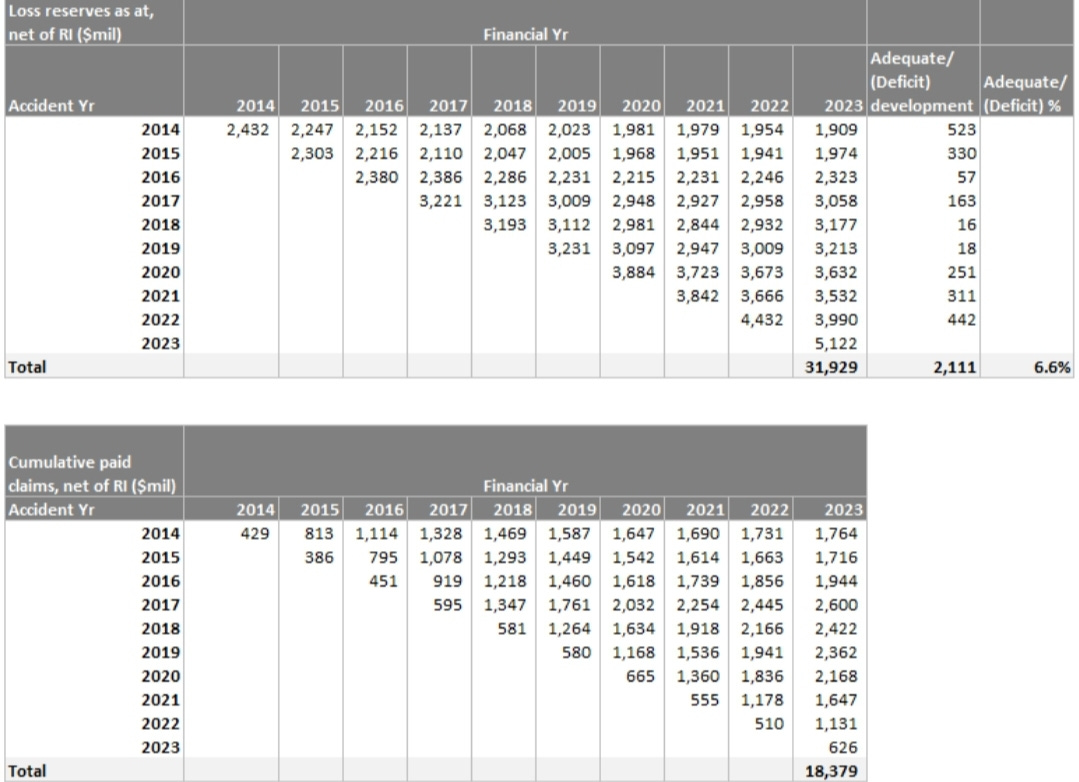

Insurance float increases over time, as long as underwriting remains profitable, this effectively acts as a negative-cost float to reinvest in other businesses. MKL discipline and conservatism results in reserves that are historically more redundant than deficient, shown by the loss development triangle:

Ventures segment (non-insurance businesses) are profitable, as a group they produce ~10% ROE. This builds up retained earnings for MKL to underwrite larger insurance volumes.

The investment segment consists of marketable equities that compound over a long time. Due to conservative reserving and cashflows from Ventures, there is no pressure to touch the investment portfolio. This further increases the equity base and benefits from deferred tax. As a matter of record, MKL’s equities portfolio 20-year CAGR is 10.2%.

Incentives and Ownership Alignment

Management continues to have significant net worth tied to the company, with a meaningful number of their shares purchased out of their own pockets. CEO Tom Gayner owns 50.2k shares with a value of ~$79m, his net worth is estimated ~$92m. Since 2021, he has bought MKL shares in 9 separate trades worth $739k.

Chairman Steven Markel owns 65.6k, and Vice Chairman Anthony Markel owns 15k.

There are 2 people on the board who are wonderful authors and we enjoy their books very much:

Lawrence Cunningham, author of Essays of Warren Buffett: Lessons for Corporate America.

Morgan Housel, author of The Psychology of Money.

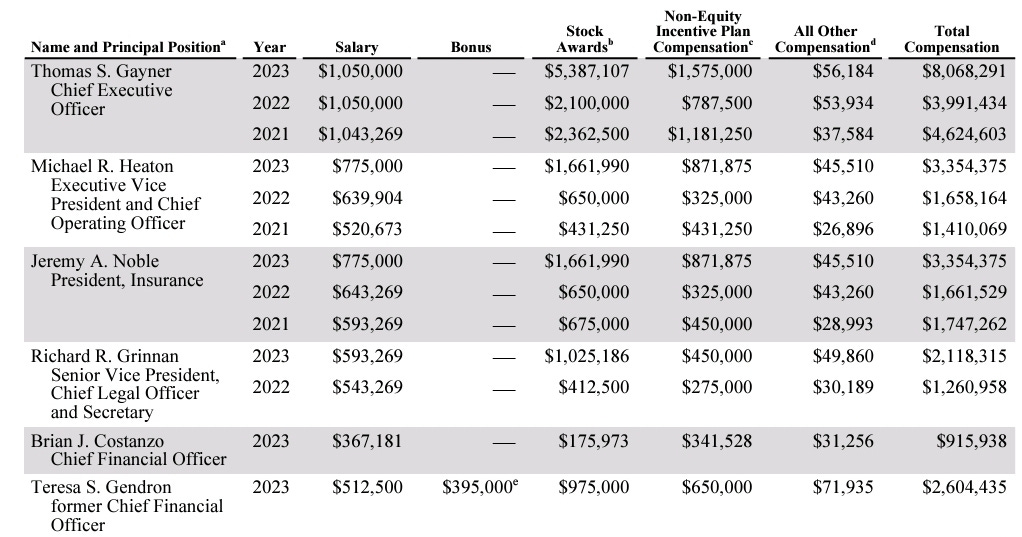

Compensation structure for executives includes cash salaries and SBC:

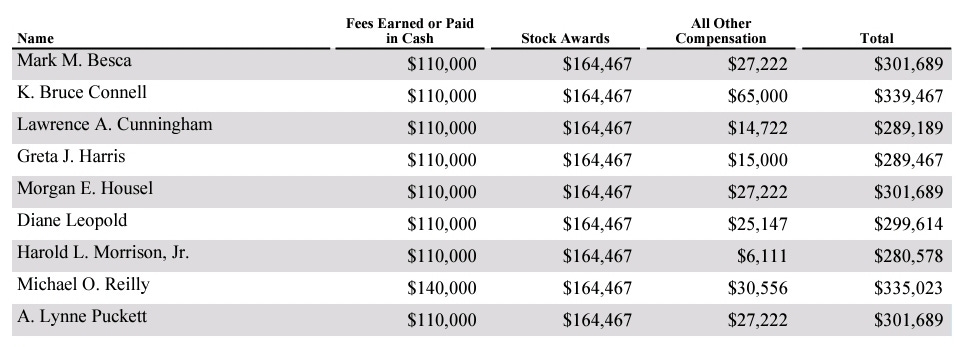

For non employee board of directors, they are paid a fee plus stock awards:

SBC dilution is not significant. Total SBC amount paid in 2023 was $35.8m. Basic common shares outstanding was 13,347k and RSU (restricted stock units) issued was 31k, representing a dilution of only 0.2%. Furthermore, 322k number of shares were repurchased, resulting in a net decrease of share count.

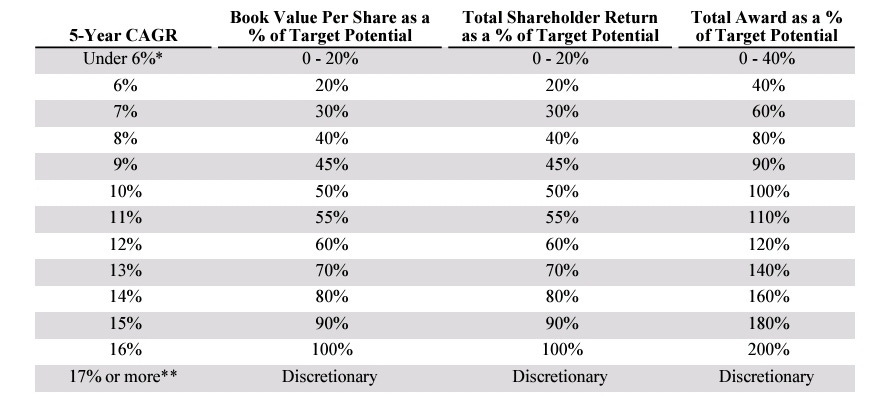

Incentives are paid based on equal weightage of average 5-year growth of book value per share and total returns:

Another Way to Think About Valuation

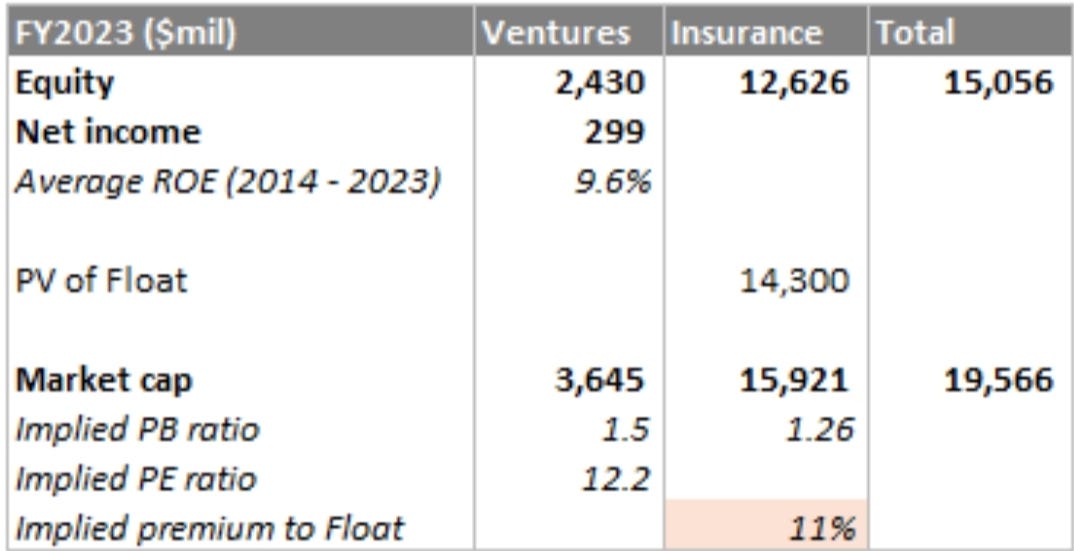

In our previous few articles on MKL, the valuation approach was sum-of-parts. This approach has its merits because the insurance and non-insurance operations run on different economics.

However, we have not properly addressed the question of “what is MKL’s earning power?”

Banks and financial companies usually get superficially valued off price-to-book (PB) ratios. We don’t value anything relative to book value, we are really interested in earning power.

A company does not make money on tangible book equity. It makes money on the funds given and the difference from the cost of those funds and the income it can generate.

In other words, unless MKL gets liquidated, book value is not really relevant. What is relevant is how much value MKL can produce from its equity capital.

So we think about MKL like how we think about most other businesses: using a price relative to earning power, not book value. And one way to think about it is; as long as we are paying a fair price (equal or below intrinsic value), and MKL can grow intrinsic value at x% per year, then we should expect minimum x% shareholder returns over a long period of time.

How to estimate earning power

We start with these per share data as at 2023:

1. Shares outstanding = 13.1m

2. Investment less debt = $22,742m (Investment = $26,522m, Debt = $3,780m)

3. Investment less debt per share = $1,736

4. Equity per share = 15,056/13.1 = $1,149

Now, we assume the investments can yield 5% normalized returns. In 2023, the weighted return was 6.5% (fixed income of 4.5% and 20-year equities CAGR record of 10%)

5. Insurance segment earnings per share (EPS) = 5%*1,736 = $87

Then, we add in non-insurance (Ventures) earnings = $299m.

6. Ventures EPS = 299/13.1= $23

7. Total EPS = $23+$87 = $110

8. ROE = 110/1,149 = 9.5%

This 9.5% estimate assumes that underwriting is breakeven. In actual, MKL is consistently profitable in underwriting, but we will save this for margin of safety.

Price relative to earning power

After we estimated the ROE, we simply have look up the PB ratio is MKL trading at today.

Given, PB ratio = 1.3x

Thus, PE ratio = PB/ROE = 1.3/0.095 = 13.7x (or 7.3% earnings yield)

Will an investor get the 9.5% returns if he pays 1.3x book value?

If MKL can produce 9.5% ROE, then intrinsic value will also compound at 9.5%, assuming all cash is reinvested back into the business.

Therefore, to get at least 9.5% returns, we have to purchase at below intrinsic value. We can phrase this query in another way, “what is a justified PE multiple such that the price is likely below intrinsic value?”

There are no scientific rules to this, but we are sure that buying at 7.3% earnings yield is not excessive for 9.5% ROE.

In summary, putting aside all the wonderful qualitative factors of MKL and simply consider the price today, we are looking a business that sells at:

PB 1.3x;

Earning ROE 9.5%;

Implied PE 13.7x (earnings yield 7.3%).

In today’s market, we think that it is a very attractive price to pay at market cap $19.9b.