MKL: Markel (3)

Argument for Undervaluation

We have written 2 prior articles on Markel (MKL) and so we won’t go into the economics of the business here. Readers can look up the blog for MKL related articles.

Since 4 years ago we have taken much interest in MKL as a business and have been accumulating shares at prices ranging from $1,000 to $1,400. At current price of $1,492 we still find some compelling value. This article will examine the reasons.

Book value and Share price growth

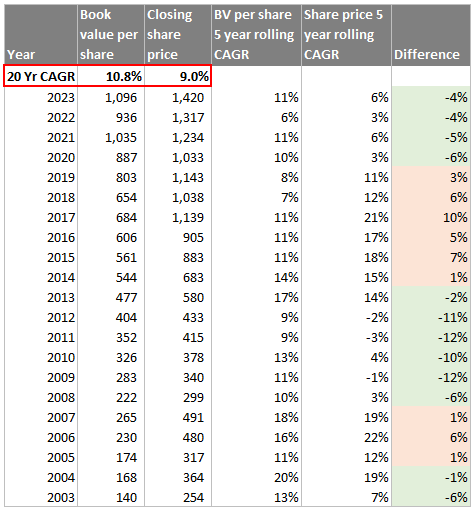

There is an obvious positive correlation between the long run growth in book value per share and price per share. This naturally flows from the logic that over long periods of time, the growth in share price of a company should track closely to the growth in net worth. Below is a table showing the past 20 years for MKL:

As Ben Graham said: “in the short run the market is a voting machine, while in the long run it is a weighing machine”. The 20 year book value per share CAGR of 10.8% tracks closely with the share price CAGR of 9%. However when we examine the 5 year rolling CAGR, the market exhibits characteristics of being a “voting machine”.

In the Difference column, we highlighted in green the years where share price lagged behind book value growth, while in red the share price surpassed book value growth.

As rational investors, we want to take advantage of the market’s mispricing. In MKL annual letters, Tom Gayner points the reader to a method which he uses to determine the company’s intrinsic value. Basically he divides the business up into 2 parts: Ventures and Insurance.

He assigns a reasonable and consistent multiple on Ventures net income. For the Insurance side, he adds up all the investments and cash less debt. There is a condition that the insurance operations continues to underwrite profitably and does not shrink in size. After that, he adds both segments together.

We adopt a slightly different approach to the Insurance segment by comparing the market value to the present value of insurance float (policyholders money that MKL holds but does not own).

Valuation for Ventures Segment

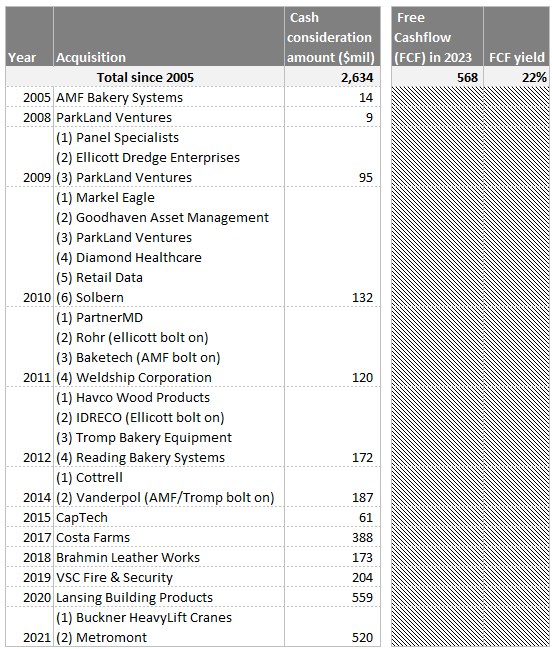

Ventures is a collection of privately owned non-insurance operating businesses. These businesses were acquired for cash, without a single issuance of shares. Therefore, we want to list down the acquisitions MKL made since the start of Ventures in 2005:

The cumulative cash consideration paid for Ventures businesses is about $2,634m. This set of businesses produced free cashflow (operating cashflow less CAPEX) of $568m in 2023.

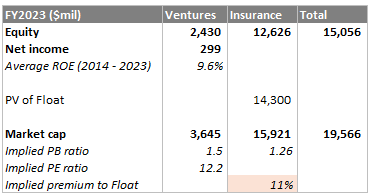

The average ROE from 2014 to 2023 is 9.6%. We do note that 2023 was an exceptionally good year for Ventures, recording ROE at 12%.

The question is then, what is the implied PB ratio we want to pay for Ventures? If we pay 1.5x book, the implied PE is 12.2x. We think this is a fair multiple with reference to ROE and FCF.

Valuation for Insurance Segment

In the previous article we already calculated the PV of insurance float to be $14.3b. This valuation remains unchanged.

Putting both together…

Below is the summary:

First we assume 1.5x PB ratio (implied PE 12.2x) for Ventures to arrive at market cap of $3.6b, then we take today’s market cap of $19.6b and find the remainder for the Insurance segment.

It turns out that we are paying $15.9b for float present value of $14.3b, which translates to implied PB ratio of 1.26x and 11% premium to float.

So is it fair to pay a premium of 26% to book and 11% to float?

There are 2 reasons why we think this is reasonable.

MKL runs a profitable underwriting operations and writes non-standard complex insurance policies which require expertise that is difficult to be competed away. The experience and data MKL accumulated over the decades forms a knowledge-based moat which we think defends the underwriting profits.

MKL most likely will have increased flexibility to allocate more capital to equities as the current portfolio compounds. This will increase the long run investment returns.

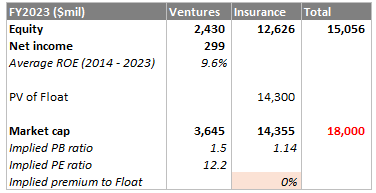

Pay Zero Premium to Float?

Suppose we really want a margin of safety and hence demand no premium to be paid on the float. Then the market cap has to be $18b, this implies a PB of 1.14x. The share price would have to be $1,372 (-8% from today’s price of $1,492).

Conclusion

We are quite comfortable in further building up this position at $1,492 per share. However for readers who wish to initiate a brand new position, we suggest to do it in tranches as there is always possibility that MKL market cap falls nearer to $18b.