CPRT: Copart (2)

Preface

Our first article about CPRT is here. It gives a long history and business economics breakdown, maybe a little too long for even the most patient reader.

So here we will summarize the points we want to make on why CPRT is such a wonderful business.

What CPRT does?

What the company does is very simple, but the features of the business and the industry create a complex combination of long-term advantages. CPRT takes damaged vehicles (or salvage title vehicles), usually from insurance companies, and sells them through its online auction house. It generally does not buy vehicles to resell. CPRT makes money by taking a cut from the sales that happen on its website.

Durable Economic Moats

Ownership of Land Assets

CPRT owns large plots of land that were acquired long time ago. Land is an integral piece of asset in the salvage business and it is impossible to purchase land that has operational leverage now. CPRT bought these yards in sub-urban areas in the early stages, and they are strategically situated to minimize cost of transporting salvaged vehicles. See google map for their busiest Yard #36 in Chicago. More than 90% of acreage is wholly owned by CPRT, the remainder is leased.

If a competitor today wants to buy such yards they will face heavy regulatory barriers and rejection from residents, because nobody wants a junkyard in their neighborhood.

The choice to have total ownership instead of leasing also prevents being held hostage by lease renewals.

Relationships with Insurers

CPRT has built close business relationships with insurers who supply the salvage cars. CPRT has a system called ProQuote which leverages their big dataset to provide estimates of used car prices. This benefits insurers because it outsources the work of determining if the cost of repair is more than the average selling price (ASP).

Think about the operational process of an insurer. When they receive an accident report, they want to be able to quickly determine if the car should be a total loss or not. This is a critical business operation and CPRT does this work reliably for them, and insurers would have operating systems built on top of this process. Therefore, it is a very sticky relationship and difficult to disrupt.

Duopoly Market

The other real competitor to CPRT is IAA, meaning the industry features the benefits of a duopoly. CPRT operates much better than IAA, but the duopoly structure exist because it is not good for insurers to be dealing with a monopoly.

So even if IAA was run poorly, the characteristics of this industry are so powerful that it can tolerate some mismanagement. This is an important factor to long-term compounding.

Efficient Operations

CPRT runs an online auction operation that possesses self-reinforcing qualities. Opening the auctions to a large number of buyers increases the ASP, which increases the commissions CPRT extracts. A higher ASP also means a higher likelihood of declaring a total loss, which attracts a higher supply of salvaged cars.

This looping effect creates liquidity between demand and supply, resulting in an efficient price discovery mechanism. The outcome is an attractive value proposition to both parties, and CPRT gets to extract surplus for being the platform operator.

Opportunistic Capital Allocator

When thinking about how to allocate cashflows, CPRT is disciplined and opportunistic.

During the GFC, they took advantage of the low valuation (mid-teens free cashflow multiple) and repurchased significant amounts of shares. Over 2008 to 2009, CPRT spent $272m on shares repurchases, its market cap was between $3b to $4b. Contrast with today’s market cap of $50b, the returns of this move is stellar.

In 2011, CPRT launched a tender offer for shares, and issued their first debt ever for $400m to help fund their largest buyback, shrinking the share count by 20%. Within a two-year period, they repurchased over 25% of the company for a share price that is ~10x lower than it currently trades. This is a CAGR of ~25% on those repurchases!

Since then, CPRT executed a few other large share repurchases, including another tender offer in 2016. They never set an annual share buyback target, but just allow excess cash to accumulate and do repurchases when mispricing occurs.

We admire this quality of intelligent capital allocation.

Conservative Expansion

Organic growth within the US market is limited and CPRT must expand globally. We examine the success of penetrating the Germany market.

In Germany, after an accident, instead of the insurance company taking away the vehicle, the consumer is left with it and the insurer just pays the claim. That means the consumer is stuck trying to sell the damaged vehicle themselves. The consumer usually relies on a variety of salvaged vehicle marketplaces to sell the car, which is also how the insurance company typically assesses the value of the car.

CPRT played the long game in Germany. In 2012, they acquired WOM, Wreck Online Marketing, which gave them their first foothold into the salvaged vehicle value chain. They could use their marketplace to run tests purchasing vehicles directly from consumers and selling them on the online platform to gauge returns. In 2016, they opened their first yard, together with the data from tests on WOM, it allowed them to approach insurers and show how their model is more profitable for the insurer, and also vastly preferred by the consumer (no one wants to deal with a multi-weeklong process of selling a salvaged car after being in an accident). In Q3 2022, CPRT reported that they were selling on consignment basis for the majority of the top 10 carriers in Germany.

Long Term Industry Trends

We will not repeat the charts in our prior article, it would be suffice to say that total loss frequency has dramatically increased over the past decade, from 15% to 21% (it was 4% in the 1980s). Cars on the road are getting older which are much more likely to be considered a total loss because the ASP is often much less than the cost to repair. New cars are also becoming significantly more expensive to repair. The two main reasons for this are a shift from using steel to aluminium and more electronic components.

A counter argument to this is if we subscribe to the idea that accident-free autonomous driving is the end game, resulting in a collapse in accident rates. This idea has been floating around for years but has not materialized as a negative for CPRT, we think that this is a far fetched risk.

Stock Price Too Expensive?

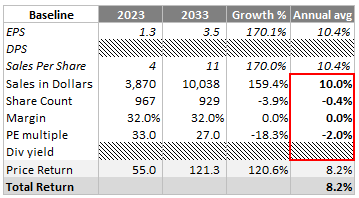

In the prior article we alluded to the need for a margin of safety quoting off a baseline scenario like this:

Currently the price is $52 (market cap $50.3b), we feel the virtues described above are too good to pass. We bought our first tranche at $51b.

Can Competitors Copy CPRT?

Barriers of entry are very high in this industry for the reasons mentioned above. Then what about existing competitors copying CPRT’s playbook? We argue that it is theoretically possible, but practically impossible.

The unique advantages that CPRT has built does not come from a handful of factors. Because if it is true, competitors can indeed easily copy their strategy. Instead, if a competitor wants to get results like CPRT, all factors that make it so defensible must be copied. That means an overhaul of the business model, think about changing these:

Outright land ownership

Building global auction platform

Convincing insurers to switch platforms

Capital allocation discipline

Operating with no debt

To use Willis Johnson’s words, CPRT is like a sewage system between insurers and the salvage market. As long as cars are being manufactured, insurers will continue to insure them, and dismantlers will continue to want salvaged vehicles.

In this sense, CPRT is like an unregulated utility business. We think that it is irresistible not to have an interest in a business that is both understandable and durably wonderful.