CPRT: Copart (1)

History

In the book Junk to Gold, we learnt the fantastic story of Copart and its co-founder Willis Johnson. The history is particularly fascinating, so indulge us with the lengthy story…

Willis Johnson was born in Oklahoma in the 1940s. His family was poor and his eventual success is a rags-to-riches story.

His father worked odd jobs and he spent most of his energy searching for business opportunities in the local paper. One such opportunity landed the Johnson family ownership of an Arkansas dairy farm. Willis learned the value of discipline and the importance of hard work first-hand as he attended to their cows and the farm whenever he wasn’t in school. He recalls waking up at 3:30am to milk the cows, driving into town to hit the creamery by 6:30am before attending school, then returning to the creamery to pick up the empty cans after school and milking the cows again in the evening. However, it wasn’t too long before his dad auctioned off the farm and they returned to California.

Willis’ mom would read the classified ads to his father who was illiterate but possessed a business mind. One of his more notable endeavors was when he bought the assets of a bankrupt construction company and tasked the young Willis and one of his friends with dismantling their equipment and inventory into portable pieces of metal. The plan was to simply sell it for scrap iron and move on, but Willis’ dad realized he could regularly buy cars for $5 and scrap them for $17, so they stayed in the dismantling business. Soon enough, they had to get a farm to store all the junk and get the requisite permit after the city hassled them: they then officially owned a junkyard.

Willis would learn a great deal not just about how to dismantle cars, but also things like what each part could be worth and what to look for in a wrecked car.

This learning was eventually put on pause, as he enlisted to serve in the Vietnam War. His job in the army was to check for ambushes and booby traps. He saw horrendous action: half of his unit was killed. All of the survivors received Purple Hearts, which are awarded for sustaining injury in the line of duty. After leaving Vietnam a year later, he threw his Purple Heart in a drawer and spoke little of it.

After returning home, Willis resumed work at his dad’s junkyard until quarrels with his increasingly drunk father led him to branch out on his own. He started working at Safeway, a supermarket, before eventually finding a junkyard whose owners were set to retire. He convinced them to take a fraction of the $75k asking price as a down payment with interest-only payments in the interim. To save money, Willis and his wife moved into a trailer on the property. It was named Mathew Auto Dismantlers, after the nearby air force base.

Initially, Willis focused on scrap metal. He would find cars that were so beaten up that they had no longer had any value as a car, and then melt them down to sell the raw materials. However, many of the cars he bought still had some working parts, which could be resold to DIY or mechanic shops at a premium to melt value. In order to build out the parts side of the business, he focused on getting less damaged cars.

Willis had a few novel insights: instead of selling parts in their entirety, like an engine, he would break them down into their constituent parts. A competitor would sell an engine for $400, whille Willis sold the parts individually and could get $700 for the dismantled engine.

Additionally, selling parts individually meant he wouldn’t have to guarantee the whole motor worked, especially if it broke soon after a sale. Willis would also clean the parts and paint them when necessary to make them look new. He would then display them in a retail format store with shelves instead of strewn around a yard like competitors did, which further garnered an additional premium for the parts.

The next thing Willis did exhibited his innate business savviness. In order to differentiate himself, he specialized in specific car parts. However, instead of picking the most popular models, he picked items that specifically weren’t “hot-selling” products. He chose to specialize in Chrysler, Dodge, and Plymouth parts. Dismantlers thought he was foolish, but were nevertheless happy to sell him their slow-moving parts, and also refer customers in search of those.

By specializing, he could serve a customer need that competitors had no desire to address. Focusing on items his suppliers didn’t want to carry allowed him to get good pricing, while simultaneously generating customer referrals from these suppliers. Customers were more willing to drive far out to get their Chrysler or Dodge products since he was the only supplier in the region.

As his business grew, he needed more inventory. He started visiting Bob’s Tow Service, also known as BTS Auctions, who would tow total-loss cars on behalf of an insurance company and then auction them off to local dismantlers, car rebuilders, and mechanic shops.

A total-loss car is a vehicle that incurred damage and the insurance company deemed it would be cheaper for them to sell the damaged vehicle and pay the policyholder a settlement instead of trying to repair the vehicle.

Willis would spend $10k a week on total-loss cars to haul back to his yard. With his yard filled with car parts, he spent $110k on a computer, which he later noted cost more than two houses at the time. However, it was more than worth the investment, as it allowed him to keep track of all of his inventory at a time competitors were using paper and file drawers. It taught him which parts of a car to scrap and which he should stock more of across thousands of different parts that varied by make, model, and year.

Showing his entrepreneurial spirit, Willis opened up several related junkyard auto businesses, including:

A minitruck-focused junkyard

Today Radiator, which focused on used radiators

Used auto-parts-focused store

Foreign-car-focused junkyard

U-Pull-It, which operated yards full of damaged cars that customers pulled parts off themselves, making it the cheapest way to buy parts.

He even started a dismantling magazine so he could advertise to more repair shops, insurance companies, and mechanics. Thinking back to his farming days when farmers would store grain together in a co-op, he thought the magazine was a similar concept since there was a “co-op” of parts dealers using the magazine. He decided to call it Copart.

After some time, Willis became BTS Auctions’ largest buyer, and while it was an important source of vehicles for him, the owner wanted to retire and his kids wanted to sell the business. They wanted $1m for the business, even though it had just $100k in equipment and earned $65k pre-tax. However, Willis knew BTS Auctions had basically been on autopilot for years, and that there was enormous growth potential. He had also thought that when a business is family owned, salaries and other family expenses were included in the financials, which he would not have to incur. So he partnered with his friend Peter Kay, each putting up $50k down payment to purchase the company. Since Willis had to use his other businesses as collateral, he got a controlling 51% stake. In 1982, he became the proud owner of his first car auction.

The recession in the mid-70s crippled advertising revenues from his Copart magazine, and since it was already legally incorporated, he decided that rather than pay to set up a new legal structure for BTS, he would use the magazine’s existing one. Copart Auctions was born.

While Willis was focused on all of his different automotive businesses, Peter was in charge of Copart’s day-to-day operations. Soon they opened a second Copart yard in Sacramento. They realized that the shorter the distance each car had to be towed to get to a yard, the cheaper it would be to service that unit, so they kept looking to add locations. Their third yard was opened in Richmond, San Francisco.

Peter, however, was approaching 70 years old, and spending more time with his racehorses over Copart, and it started to show. When a few lapsed bills were overlooked, Willis had enough. He gave Peter an ultimatum: They would each write a number on a piece of paper, and Peter could buy the business at Willis’ number or sell at his own. Peter sold.

Willis now being fully in charge, he started making changes. Sealed bids were changed to live auctions. Guests were allowed to come in so long as they could get a licensed dismantler to take liability over them. And he kept adding yards as opportunities presented themselves.

The biggest business transformation was a change in the incentives and economics of the auction business. Just as cleaning the car parts he sold increased the price he could command, doing the same for his salvaged cars yielded a similar result. He wanted to make the cars look nicer, but knew the insurance companies would be reluctant to spend money on this. He thought: what if there was a way to split the increase in price from making the cars look nicer?

At the time, it might cost about $200 to pick up, store, and auction off a car. Willis wanted to instead incur that cost, plus the cost of cleaning up the car, in exchange for a percentage of the proceeds once the car sold: 20% for old and highly damaged cars and 10% for everything else. The result was that both the insurance companies and Copart generated higher proceeds.

This arrangement, which Willis called the Percentage Incentive Program (PIP) also solved another issue insurance companies had. A fire-damaged car may have fetched only $25 in an auction, but cost that same $200 for Copart to pick up and process. The insurance companies were losing money on each of those units. Under PIP, Copart instead would be the one to lose out on that car by incurring expenses less than their portion of proceeds. The kicker is that Copart would only offer PIP if an insurance company contracted out all of their cars in a region to Copart. So Copart would lose on a fire-damaged vehicle, but make it back on a lightly damaged car. Economics aside, Willis liked how he was now aligned with his customers: they both wanted the highest price for the cars, whereas before, his revenues only increased with volume.

In 1989, he met Jayson “Jay” Adair, a recent high school graduate, and his daughter’s boyfriend. Jay showed a curiosity in the salvage business, partially driven by his amazement that anyone could make money from junkyards. After Jay’s first year of college, he decided it wasn’t a good use of his time and that he wanted to become a businessman. When he told Willis, he was handed a broom. Jay would become Willis son-in-law and eventually CEO taking a symbolic $1 salary since 2013.

Jay started running more of Copart, starting with the titling department, and then moving to customer service. He excelled at work both in the office and out in the yard, but he was worried that Copart could never grow to the size that it would be big enough for him to take on meaningful responsibility and make a lot of money. That all changed in 1991, when IAA (Insurance Auto Auctions), an auto auction competitor, went public. Flipping through the prospectus, Willis thought that if IAA could do it, then so could Copart.

Before going public, Copart had to get larger. So Willis got in touch with a Wall Street investment banker to help raise $10m in a private round. He was able to raise that amount as a convertible that paid 8% interest and would convert into a 26% stake of the company. Willis and Jay then embarked on a growth phase, tripling their footprint to about a dozen yards and generating $1.4m in EBIT on $10m sales.

That was enough that their banker thought they could complete a public offering. They sold 2 million shares at $12 a share, raising over $20m after underwriting fees. Copart (CPRT) was now a listed company valued at over $80m. Willis’ 40% stake made him wealthier than he could have ever dreamt, but he was just getting started.

The proceeds were their ammo, and CPRT was prepared to go to war with IAA. They would try to acquire smaller junkyards, as well as several regional chains, as quickly as they could.

They battled for acquisitions as the industry rapidly consolidated. By 1996, CPRT had 49 locations. Revenues grew to $118m and recorded $18m EBIT. This growth was funded by a near doubling of shares outstanding, as they used their stock as currency to acquire more properties. This included a secondary offering at $19.25 in 1995 that raised an additional $30m.

With many junkyard locations hard to replicate because of permitting requirements, land scarcity, and the public generally against allowing a new junkyard to open up near them, the race was on to acquire properties in as many markets as possible. IAA was buying big and expensive lots in large cities like Chicago for $7–9m, CPRT would opt for smaller suburban yards in for $1.5–2m. CPRT was focused on building a network, because more locations would mean shorter towing distances. This would make operations more efficient, even if it came at the cost of losing some city-center business for the time being.

Interestingly, despite IAA being bigger, CPRT was often winning bids against them because IAA bought companies based on accounting earnings. Willis, on the other hand, knew that a lot of these family-run businesses would use the company as a sort of piggy bank to buy personal cars or pay salaries to family members who didn’t work much (something he learned when he originally bought BTS Auctions). Willis would size up how many cars they sold at auction and what he thought CPRT would make if they owned it. IAA thought more in terms of how an acquisition would look from a pro forma GAAP perspective.

A big difference between CPRT and IAA was what they did after acquiring a property. IAA would more or less leave it alone, thinking it was more urgent to acquire the next property than integrate the one they had just purchased. In contrast, CPRT would train staff members so that each yard would run the same. At one point, they even slowed growth to focus on unifying all of their properties into a single ERP (Enterprise Resource Planning) system. It took two years and cost $3m, but by 1997, they started rolling out their new computer system yard by yard. This made it much easier to manage the increasingly national operation, and keep track of and identify any particular yards that had abnormal inefficiencies.

CPRT readiness to adopt technology and experiment has always set them apart from their competition. In the late 90s, Jay started hearing about “dot-coms”. At first, he thought they could list their cars online to limit the paper they were wasting (it took over 8,000 sheets of paper to circulate the weekly auction list of cars).

But then he realized that they could use the internet to help solve one of their largest pain points: buyers were hiring people to bid on their behalf at the car auctions, paying them $150 every time they won a car. He thought it was silly that people could make $2–3k a day just standing around and raising a paddle. Using the internet, buyers could come the day before and view the cars, then place a bid online for $35 instead of paying a contractor to stand in the live auction. Jay was right: the online platform generated $1m in sales the first quarter it launched.

There was one particular transaction that stood out, and in retrospect, anticipated a multi-decade shift in how cars would be purchased. The auction winner of a car sold in San Diego was a buyer in Connecticut. Cars were always sold locally, maybe occasionally regionally, but this was an instance of someone buying a car across the country without looking at what he’s buying.

Jay called up the buyer, and he said that while he knew what he was buying, it would be helpful if CPRT added pictures online. Jay proceeded to buy 55 cameras and teach the general managers how to take pictures of a car. With photo listings set up two quarters later, that $1m of online sales per quarter grew to $10m, and in year 2000 CRPT recorded revenues of $190m.

At that time, CRPT auctions were still not live, so in the next step forward, CRPT tried to enable real-time bidding. The first iteration of online bidding was born in 2001 and dubbed Virtual Bidding 1 (VB1). It required building out large structures to house the auctions inside with large TVs that showed pictures of the current car. No longer were auctions held out in the open in the yards. The internet system was linked to a row of employees at computers who would monitor online bids and signal to the auctioneer if there was an internet bid. This allowed the internet bidder to be participating in the live auction happening on the floor.

With online auctions, the thing they noticed was not just that buyers from far away markets were participating in the auctions, but that the auction prices were increasing. This meant higher returns for the insurance company and a higher cut for CPRT, since over half of their cars were on the PIP model. “Returns” is industry terminology for the sales proceeds as a % of pre-accident value. If a car is worth $10k pre-accident and Copart sells it for $3k, then the return is 30%.

I literally sat there and watched the vehicles sell and beat the live auction. We even had cars where the live bidder had quit and watched a virtual bidder bid against another virtual bidder for thousands of dollars. A car which has finished at $2,100 live would get a virtual bid for $2,200, then another virtual bidder comes in for higher. Eventually that car would sell for $3,100. So that’s pretty exciting stuff.

Jay Adair, 3Q 2002 earnings call

VB1 was creating operational issues though, and further growth almost assured it would only get worse. The employees who monitored the online bids for more than 1 hour would become tired and error rates would increase. Their largest yards still had yet to incorporate the system for fears it would be too hectic and bids would get lost. Buyers stopped coming to the yards in-person to bid online, which interfered with the live competition component. Taking the middle option of quasi-online and in-person was an optimization of mediocrity. Jay told Willis they would either have to go all in on the internet or abandon the effort.

Willis gathered his managers in a room and wrote the words “what is our job?” on the board. They decided that the company’s job was helping buyers purchase cars easier, so that they could get the most money for the sellers; to get the insurance companies more money. CRPT serves the insurers and the best way to do that is to reduce friction. To achieve this, they must go full online auctions. This is a remarkable decision because their competitor IAA would only go full online when COVID forced them to, 2 decades later!

In 2003, the company went 100% online on their bidding platform. This meant buyers from all over the world could place bids. This increased the sale price of the vehicles by increasing the number of people that can bid on available inventory without being at the yard itself.

VB2 was developed, which introduced preliminary bidding prior to the live online auction. Ten years later in 2013, VB3 launched.

When 9/11 hit, financial markets were spooked and there was a fear that people would be reluctant to travel again for a long time. Planes were flying at just 5% capacity. Willis realized that miles driven would go up as people avoided flying, but he lacked the cash needed to continue their yard acquisition. They had over 70 locations by then, but in order to continue growing, he went back to Wall Street for another secondary offering, this time raising $116m at $29 a share.

CRPT expanded via acquisitions into various new states across the United States, they acquired huge land spaces and never leased. There is a strong case for ownership of land rather than renting and leasing despite the high initial capital outlay. Leasing means there is a risk that landlords can break the contract suddenly causing great disruption to the business. If yards are far from an accident, towing fees would start to eat into the bottom line. Therefore, there is a need for a high density of yards in order to keep towing costs low.

In June 2007, CPRT acquired Universal Salvage, the operator of about 10 salvage yards in the UK and a vehicle remarketer to the insurance and automotive industries. The company also broadened its existing range to farming equipment in the UK in 2011 by acquiring Hewitt International, an auctioneer of agricultural vehicles and equipment based in central England.

During 2008, the company launched CopartDirect (branded as cashcars.com) to sell undamaged cars to the general public, using its VB3 application.

In 2012, the company made several acquisitions in international markets, including Brazil, Canada, Germany, and Dubai, UAE.

Fast forward to today, CPRT and IAA share 80% of the US market, with CRPT slightly ahead. The balance is shared by a number of smaller players. In 2023, CPRT has more than 200 locations globally and recorded revenues of $3.9b, with EBIT of $1.5b, operating with negligible amount of debt of $11m.

Business Model

Insurance companies are the suppliers of damaged cars to CPRT. An insurer determines whether to salvage the car based on this estimate:

(1) Salvage car if PAV – RC < SV

(2) Repair car if PAV – RC > SV

where PAV = pre-accident value, RC = repair cost, SV = salvage value.

So if PAV is $10k, RC is $6k and SV is at least $4k, then the insurer will send the car to CPRT. Otherwise they will repair the car.

CPRT comes in when the insurer decides to write-off the car, settle the claim, and auction the damaged car. It offers vehicle sellers a full range of services, which expedite each stage of the sales process, helping to maximize proceeds and minimize costs:

Salvage value estimation using their database.

Storage, listing, processing, towing services.

Full recycling services for salvaged cars.

There are 3 vehicle processing programs:

Percentage Incentive Program (PIP)

Under PIP, vehicles are sold for a predetermined percentage of the vehicle sales price. Because revenues under PIP are directly linked to the sales price, they have an incentive to actively merchandise those vehicles to maximize the net return. CPRT provides free of charge transportation of the vehicle to their nearest facility.

Consignment Program

Vehicles are sold for a fixed consignment fee. It may include transportation, storage and other incident costs.

Purchase Program

CPRT purchases vehicles from a seller based on a percentage of the vehicles’ estimated PAV, and sells the vehicles for on CRPT own account. Currently, the purchase program is offered primarily in the UK.

In the US, CRPT is overwhelmingly a selling agent and not a principal.

Industry is a Duopoly

CPRT and IAA represent a duopoly structure taking over 80% market share. Both companies have built up scale advantages over 35 years that would be very difficult to replicate.

IAA was acquired by Ritchie Bros Auctioneers (RBA) in 2023 for $7b. It has not performed as well as CPRT. It is much smaller revenues and net income, and the parent RBA operates with significantly more leverage. We believe that RBA is unlikely to have the resources to fight strongly against CPRT.

Insurance companies aim to lower its claim costs by minimizing repair costs on the cars it saves or by maximizing the salvage proceeds for those total-loss cars. In the latter case, the highest proceeds are achieved by creating competition among a large base of potential buyers, who in turn seek a reliable source of supply across a broad range of model. Buyers attract sellers and sellers satisfy buyers in the feedback loop characteristic of market places. Insurers also have an incentive to cut auction transactions costs, but there is perhaps limited scope to do so given the duopoly structure.

Sellers of Salvaged Cars

There are an estimated 292 million cars on the roads in the US. This includes Cars, SUVs, Vans, and other medium and heavy-duty vehicles that are registered with the relevant authorities.

Every year, around 12 million cars end up in salvage auctions. Insurers supply 80%-85% of these with the balance accounted for by banks (due to repossessions), dealers and others.

Main insurers who supply are State Farm and Progressive.

CPRT sells about 60k cars per week, IAA about 35k.

Buyers of Salvaged Cars

Demantlers, dealers, repair shops, individual hobbyists, and parts recyclers make up the demand for salvaged cars. Vehicle dismantlers are the largest group of buyers. They dismantle a salvage vehicle and sell parts individually or sell the entire vehicle to rebuilders, used vehicle dealers, or the general public.

In general, buyers are smaller and more fragmented than sellers. There is one exception: LKQ Corporation (LKQ), a listed company with annual revenues of $13.9b is a major buyer of salvage cars. They sell parts to repair shops. These repairers buy from LKQ to satisfy cost conscious insurers who direct huge repair volumes to the shops. The insurers give a preference to shops using less expensive recycled parts for damaged cars. Insurers account for a large portion of repairs and are an influential force in the repair market.

Fee structure

Most fees come from the buyer side. CPRT imposes a commission based off the average sales price (ASP) of the car. The fee schedule can be found here.

On the seller side, they have not explicitly published what the fees are like, but from what we gathered it’s between 1% to 6.5% of ASP.

Other fees such as storage, towing, titles, processing etc. This is quite standard fee structure in the industry.

In 2023, international sales was 48% of total revenues and we expect the trend to continue increasing.

How Demand Intersects Supply

CPRT business is to match demand with supply with minimal frictional costs, the outcome is fee revenues for CPRT. We break the process down into 2 phases:

Phase 1

In phase 1, which starts 3 days before the live auction, buyers submit the maximum price they are willing to pay for a vehicle and CPRT’s system incrementally bids up to that price on behalf of the buyer, who receives an email if he is topped. So everybody gets an idea of what the highest price for the car somebody will be willing to pay. He may not pay that, but it does create some expectations of what the likely high price is going to be. A lot of price discovery has happened before the auction takes place. Phase 1 is an open bid format similar to eBay.

Phase 2

The winning bid in phase 1 sets the starting price in phase 2, when bidders compete in a real-time virtual auction environment.

Phase 2 allows bidders the opportunity to bid against each other and the high preliminary bidder. When bidding stops, a countdown is initiated. If no bids are received during the countdown, the vehicle sells to the highest bidder.

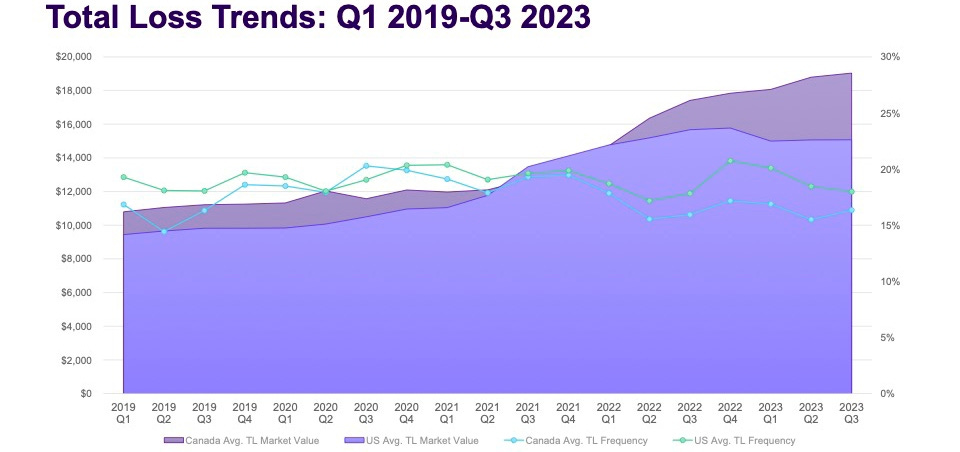

Secular Tailwinds

The tailwinds come from four trends:

Miles driven increasing

Repair costs increasing

Insurers want to retain their policyholders

Average sales price (ASP) increasing

All these factors cause total loss frequency to increase over time, CFO Jeffrey Liaw commented on this the Q4 2022 earnings call:

The history of total loss frequency from 4% in 1980 or so to 20% as of a couple of years ago, has been the product of 2 key factors: vehicle complexity and composition, making cars more expensive to repair along with our auction liquidity and global buyer base has made them more efficient to mark as total loss.

The total loss decision often involves a level of discretion of the insurer. Sometimes an insurer will make a total loss determination to keep a policyholder happy and to retain the business.

This also relates to why CPRT, and the efficient processing of these total-loss vehicles is so important: if an insurance company takes too long to process a claim, it could cause that customer to defect to a competitor.

Repair costs include wages which have been inflating secularly. Supply of skilled workers is constrained, and more electrical parts mean that more man-hours are needed. Also, vehicle parts will only become more expensive as car parts increase in sophistication.

Lastly, higher ASP of cars means that CPRT is able to drive commission revenues without needing to increase volumes. Since there are unit costs involved with volumes, it is beneficial to CPRT that the ASP trend is rising.

Competitive Advantage #1: Land Ownership

CPRT was of the opinion that land in a good location was absolutely key for their business, so not only did they want to control a lot of land, they insisted on owning it. In contrast, IAA preferred to lease. In the short term, this meant that IAA could grow more quickly since instead of tying up capital in the land, they could use it to acquire more lots. For a while, this made IAA look like it had a stronger return on invested capital, while growing at a faster rate (this is before ASC 842 lease accounting standards were adopted, requiring operating leases to show up on the balance sheet).

As time passed, these leases would come up for re-negotiation and IAA was put in a very awkward position. Their entire business would stop functioning without these scarce lots of lands, which were hard to replace since they required special licenses while also being close densely populated areas; and the of course the landowners knew that.

CPRT was correct that land would be in much higher demand in the future. In fact, even once they bought a yard, they would buy land nearby for potential future expansion. Today, CPRT owns more than 90% of their arceage.

Competitive Advantage #2: Reputation

During Hurricane Katrina (2005), which left over 300,000 vehicles in salvage conditions, CPRT built a reputation of going out of their way to work for their customers: they hired almost 300 extra sub-haulers, spent millions buying new equipment when it couldn’t be leased, and they shipped in employees to work extra hours.

CPRT incurred a significant amount of expenses that they never passed on to the consumer. As Jay Adair noted in the 4Q 2005 earnings call:

Our primary purpose right now is getting the cars in as quick as we can, servicing the major carriers. And will we make a profit on this? Probably not.

This word-of-mouth advertisement is probably more effective than paid advertisements.

Competitive Advantage #3: Capital Allocation

CPRT never repurchased shares for almost 25 years as a public company. There are two broad reasons for this:

They were focused on rolling up the industry to become a national player, which they correctly thought was necessary to be competitive in the long-term.

CPRT wanted to build a very conservative balance sheet.

Only after taking care of the business needs, CPRT then started to use excess cashflows for repurchases in 2007. When the GFC came, they positioned themselves to take advantage of the low valuation (mid-teens free cashflow multiple).

In 2011, CPRT launched a tender offer for shares, and issued their first debt ever for $400m to help fund their largest buyback, shrinking the share count by 20%. Within a two-year period, they repurchased over 25% of the company for a share price that is ~10x lower than it currently trades. This is a CAGR of ~25% on those repurchases!

Since then, CPRT executed a few other large share repurchases, including another tender offer in 2016. CPRT would not be able to act so opportunistically unless they had conservatively managed the balance sheet prior. CPRT never sets an annual share buyback target, but rather just let the cash build and act when prices are cheap.

Risk #1: Accident Avoidance Technology

This is a “good for society; bad for Copart” argument, but we don’t think this is a material risk. There is a report by the Insurance Institute for Highway Safety in 2016:

If all vehicles had been equipped with autobrake that worked as well as the systems studied, there would have been at least 700,000 fewer police-reported rear-end crashes in 2013. That number represents 13% of police-reported crashes overall.

If we were to believe this estimation, even with 100% accident prevention system, the effect is only 13% reduction in accidents.

The factual trend is a stable total loss frequency:

Full autonomous driving is likely to take multiple decades to materialize and achieve penetration. Furthermore, new technologies come at higher repair cost, this offsets the decline in accident frequency.

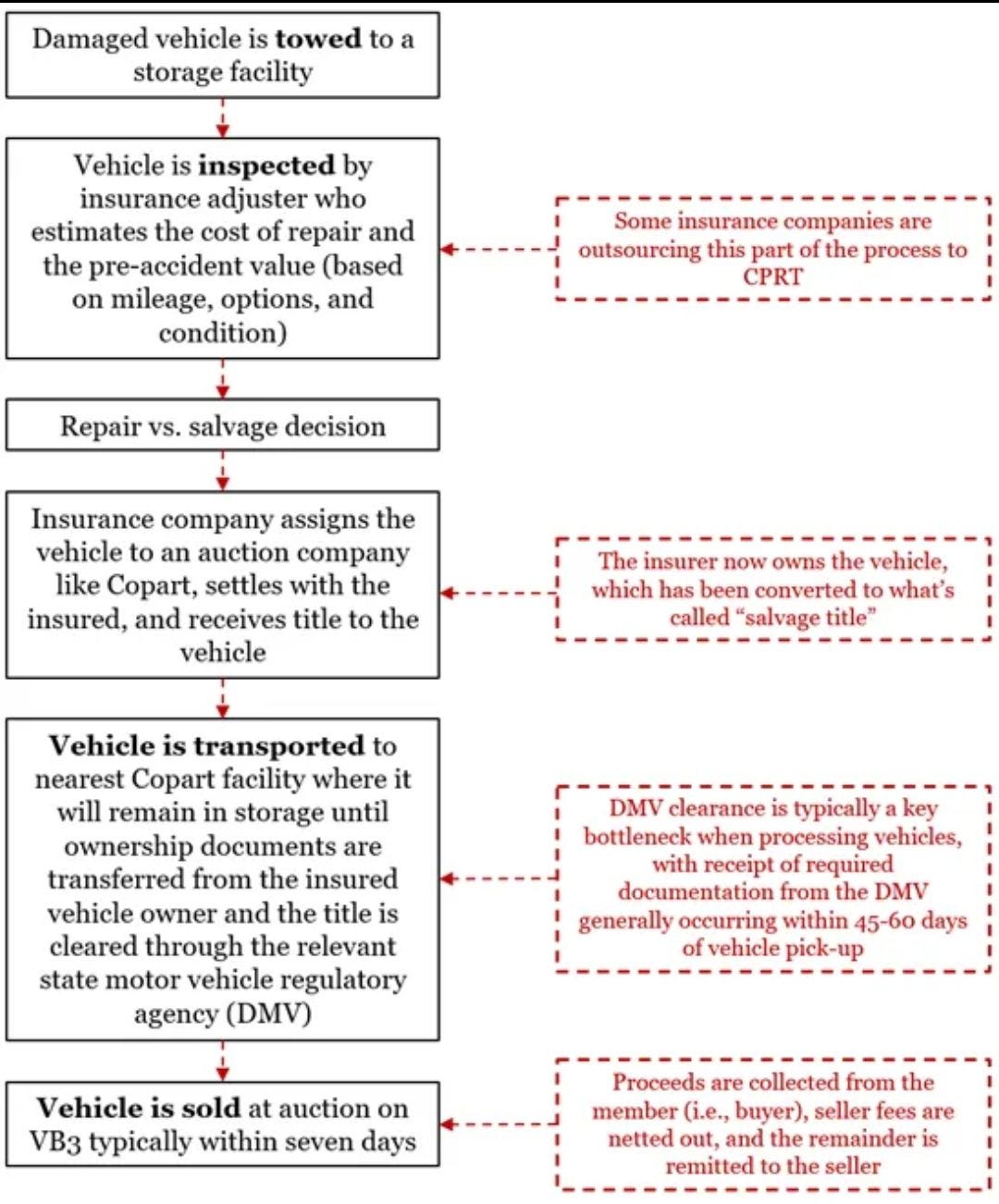

Risk #2: Bottlenecks in Salvage Titles

Above is the flowchart of how the process at CPRT looks like. An obvious bottleneck is the requirement for each state Department of Motor Vehicles (DMV) to process the title of that vehicle. In the US, total-loss vehicles can be sold in most states only after obtaining a salvage title from the DMV. A salvage title is an official indication that a vehicle is damaged and considered a total loss, attaching the salvage designation to a car’s title means that future buyers can do a title check to see that the vehicle was previously written off.

CPRT, in conjunction with the American Property Casualty Insurance Association (APCIA), is pushing for electronic titles and the digital transmission of titles to help speed up the title transfer process. The process is archaic, and it is worth noting that the lack of a nationwide vehicle registration process means that title transfer processes are determined on a state-by-state basis. This makes change more difficult to enact, given that 50 states need to be convinced to make changes to their systems.

Risk #3: Growth Opportunities

Future growth will likely have to come from non-salvaged car businesses (farm machinery, heavy equipment) and international expansion.

In 2015, CPRT made an acquisition outside salvage when it bought National Powersport Auctions (NPA). It is a leading online marketplace for powersports vehicles, such as motorcycles, ATVs, and snowmobiles. NPA has continued to operate as a separate brand under the CPRT umbrella. It has also expanded its operations to include new locations in the United States and Canada.

In 2023, CPRT announced a new strategic investment and partnership with Purple Wave, an online offsite auction company with a specialized focus on the sale of construction, agriculture, and fleet assets.

As mentioned above, the industry is a duopoly, this causes little room for domestic inorganic expansion. CPRT spent a decade building its brand inside Germany with the intention of spreading to the rest of Europe, and now operates in 12 countries (USA, Canada, the UK, Brazil, Ireland, India, Germany, Finland, UAE, Oman, Bahrain, and Spain).

International expansion requires CPRT to adjust for local insurance company regulations and business practices. In order to build trust in the auction system, some cars are purchased by CPRT itself, exposing it to price risk, with the expectation that insurance companies will transition to using CPRT auctions over time.

One of the biggest market CPRT is in Germany. The way the market works there is different from the US. In Germany, when an accident happens, instead of the insurance company taking the damaged car away, they will write a cheque to the policyholder for the difference between PAV (pre-accident value) and SV (salvage value). The policyholder gets to keep the damaged car.

The German insurers will then list the damaged car to get the salvage value. Mechanics, repair shops, and dismantlers will all bid on the damaged car, but the bid is non-binding. Meaning that it is ultimately the policyholder’s decision if they want to sell.

This causes the auction system to fail as the non-binding feature will invite a lot of low-ball bids. As a result, insurers are paying out more claims for the damages than they should if the auction system was functioning properly.

The policyholder is probably not happy even with the higher claims reimbursement, because they have to store and arrange the sales for the salvaged car themselves. It is a laborious process.

However, we can gain confidence from a good record of how CPRT executed overseas expansion in Germany. In 2012, they acquired WOM, Wreck Online Marketing, which gave them their first foothold into the salvaged vehicle value chain. They could use their marketplace to run tests purchasing vehicles directly from consumers and selling them on the Copart Global Platform to gauge returns.

In 2016, after circumventing the myriad of European laws, they opened their first Copart yard. This first yard, together with the data from tests on WOM, allowed CPRT to approach insurers and show how their model not only is more profitable for the insurer, but also vastly preferred by the consumer (no one wants to deal with a multi-weeklong process of selling a salvaged car after being in an accident).

A decade after initial entry, in 2022, CPRT was selling on consignment basis for the majority of the top 10 insurers in Germany.

Risk #4: Total Addressable Market (TAM)

We think the TAM for this industry is more or less fixed. Therefore, it is important to know what’s CPRT market share is, and whether it can win share from IAA.

Even though CPRT is much better than IAA in terms of efficiency metrics, operations and strategy, the insurance companies do not want to be held hostage to just one company. Especially when salvaged cars auctioneers play such a critical role in their value chain.

There are incentives for insurers to keep this duopoly alive in terms of keeping their claims cost down.

In this case, it follows that overseas expansion is required for growth, but this is a slow, costly and challenging process. Land laws are different overseas and it is unlikely that a foreign country will allow full ownership of land by a foreign company. Leasing could be an option, but we know it is less desirable.

CPRT tried to enter the Indian market in 2014, but ultimately it was a failed venture as they found it was too beaucratic and fragmented to get a meaningful return on investment.

Some less developed countries don’t even have insurance for cars, so the CPRT business model won’t work there. It is a long wait for these countries to become more affluent for people to be able to afford insurance and drive adoption. For example, in Brazil, they are waiting for insurance to develop and car ownership to increase.

Therefore, we should not assume that CPRT is able to travel internationally in every country.

Risk #5: IAA Irrational Pricing

There can be situation where IAA decides to cut prices, and somehow CPRT decides they should also do the same if they lose enough buyers.

We argue that there’s nothing to gain by IAA cutting prices because they would just earn less revenues, while CPRT with global operations doesn’t really need to engage in price wars domestically.

Management Ownership and Incentives

Both Willis and Jay have accumulated substantial stakes in the company. Together, they own ~10% of Copart and also have unvested stock.

CEO Jay’s salary is a symbolic $1 and no cash bonus but a generous amount of stock options with different vesting periods (mostly in 5 years cycles). CPRT also discloses that other perks are included as compensation, like the use of the corporate jet for personal use for up to 100 hours a year.

The compensation metrics are total shareholders return and operating income.

This compensation scheme generates a high degree of alignment between shareholders and executives.

Valuation

If you came so far after reading everything above, it’s not a surprise that CPRT is richly valued by the market. CPRT is akin to an utility company without regulations, rewarding shareholders with more than 350x return since going public in 1994 (CAGR 22%).

Future revenue growth will come from a mix of higher ASP and volumes. We are of the opinion that the total addressable market is not going to grow faster than the underlying factors. Also, the duopoly status is not going to swing largely in favor of CPRT for reasons mentioned above.

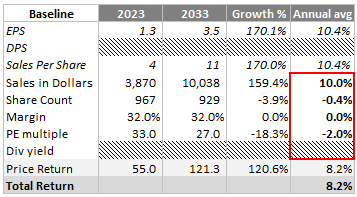

This is our baseline assumptions projecting out 10 years for CAGR of 8.2%:

Sales projected to grow at 10% (last 10 years 14%)

Share count decrease -0.4% (last 10 years -0.9%)

Net margins maintain at 2023 level of 32% (2014: 15%)

PE multiple decrease to 10 year average of 27x

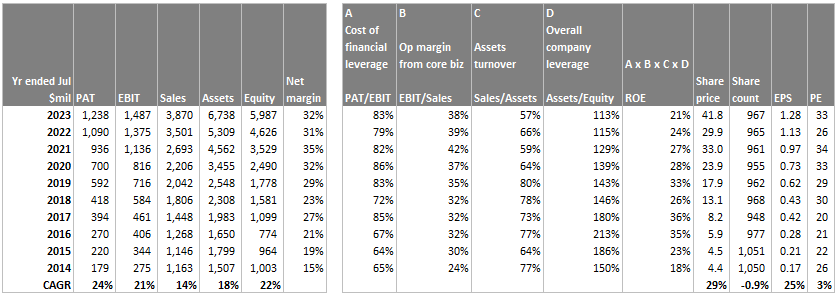

Below is the attribution of ROE:

Interestingly, imagine that the share price in 2014 was double at $8.8, the PE ratio would also double to 52x. Even if we bought CPRT at such multiples, the CAGR over 10 years would have been 19%. This goes to show that if a business can generate high ROE (in CPRT case it was due to expanding margins), it can make sense to buy it at high multiples!

The reverse DCF: to justify CPRT market cap today of $51b, we need free cashflows to grow on average 10% for 10 years and terminal growth of 2.5%, discount rate of 6% (prehaps reflecting our view of the business stability).

Conclusion

We are very impressed with the economics of CPRT and bought our first tranche at today’s market cap of $51b.

We plan to enter in tranches because we still require a margin of safety in valuation, so we hope that the market will provide us with discounts going forward.

This article was copied from my old blog. So the dates dont match.

"We are very impressed with the economics of CPRT and bought our first tranche at today’s market cap of $51b."

I'm wondering where you got the $51b from. At the time of posting this article, Copart's market cap was between $36-37b. Would you mind to elaborate?