CPRT: Copart (11)

Bear Case: Demand Collapses?

We have written many articles about CPRT, refer here for a comprehensive explanation of business economics.

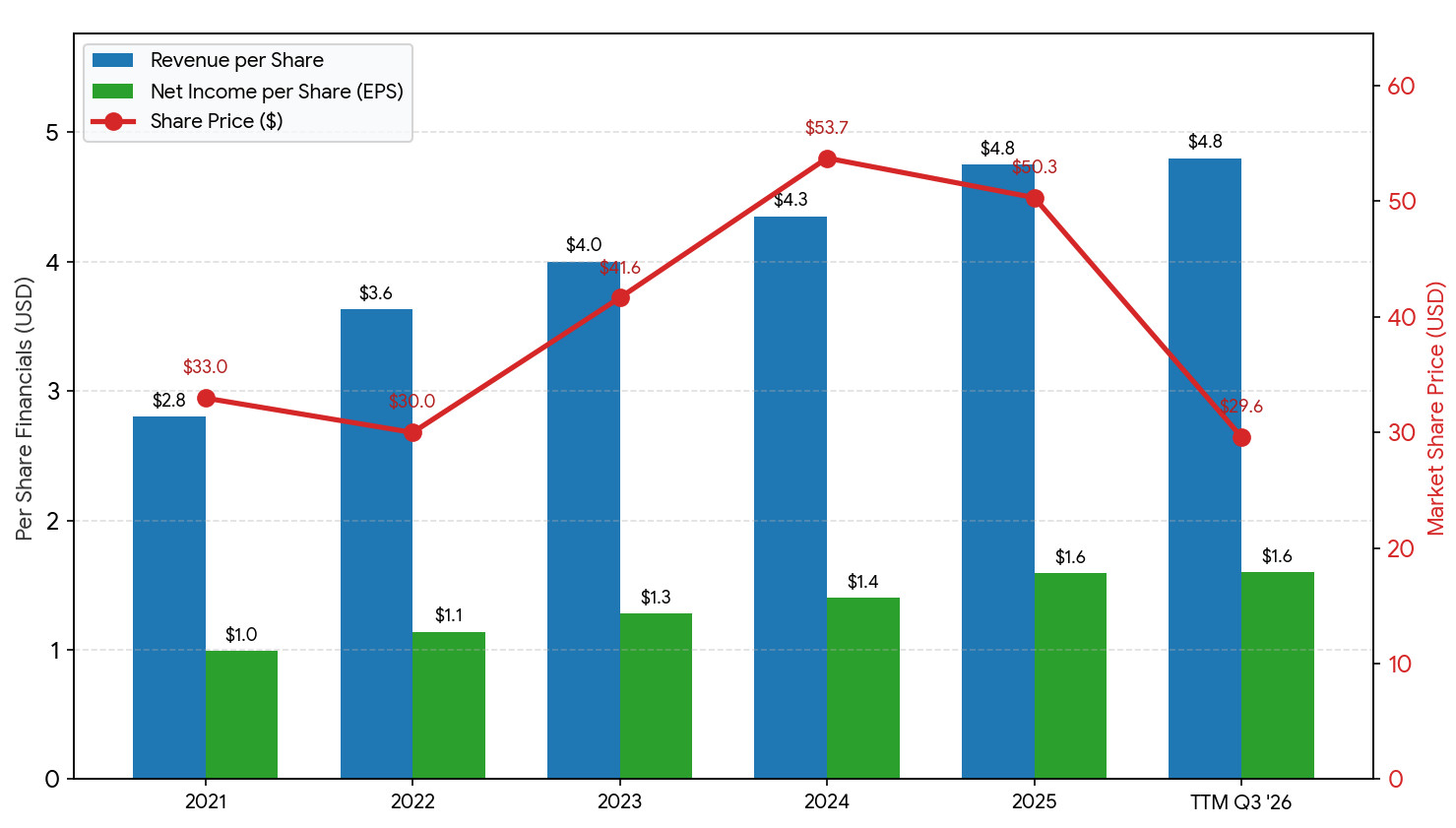

Ever since we have bought the stock at an average price of $41, it has fallen by over -20%. The stock price divergence with their financials is stark, as if suddenly the market thinks that CPRT is structural impaired:

In our Q3 FY2026 update, we have explained the near-term headwinds that CPRT is facing and why these are non-structural issues.

However, there is one structural bear case we want to address here. It attacks the demand side of CPRT’s business:

As cars become more complex and EV penetration increases, repairing cars will become more difficult due to lack of parts and skilled labour.

We might end up with a future where nobody has an incentive to repair salvaged cars leading to low demand.

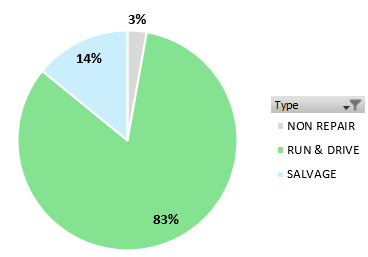

To answer this case, we have to first see what type of auctions is CPRT doing today. We went to its auction page and downloaded 3 sets of data (sample size = 3000).

The dataset can be split into 3 types of salvage vehicles:

Non Repair: Very badly wrecked cars that cannot be repaired, most likely sold for scraps and dismantled for raw materials.

Salvage: Repairable cars, this is what the bear case is attacking.

Run & Drive: Car engines that can start on their own without intervention, supposedly able to buy and drive off (no gaurantees).

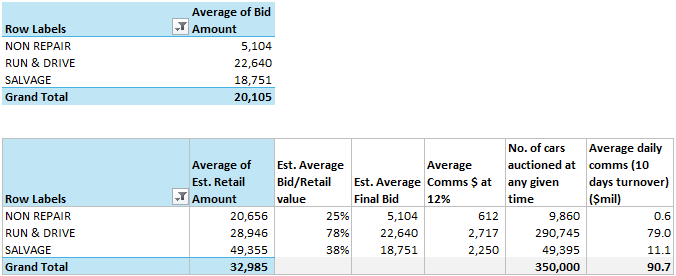

We refined the dataset so that “average bid amount” makes sense:

Excluded bid amounts that are less than 50% of estimated retail price. This removes entries which are very early in the bidding process.

Excluded Purple Wave vehicles as these are not supplied from insured accidents.

Firstly, based on the total bid amount, majority 83% of bids are for Run & Drive types. 14% are repairable (Salvage), while a tiny 3% are Non Repair:

So that’s one piece of good news: Auctions are mostly made up of cars that are “ready to drive”.

Baseline Model

Next, we look at the average bid amount and estimate average daily commissions CPRT receives from buyers. This will serve as our baseline:

As expected, Non Repair has very low bid amount, followed by Salvage. The average bid against retail value also makes sense:

Non Repair are only worth 25% of their retail value.

Salvage are also very low at 38% of retail value.

Run & Drive is high at 78% of retail value. People are willing to bid for decent conditioned cars.

The average commissions are 12% for sales that are above $5,000. All of the categories exceed this amount.

CPRT states on their website that the number of cars auctioned at any given time is ~350,000. Then, we proportionally split it by the share of total bid amount in the above pie chart.

CPRT also says that it takes 7 to 10 days to sell a car after it is put on auction. We assume 10 days turnover:

Average daily comms = 12% * Est. Final Bid * Number of cars/10

Therefore, we estimate CPRT earns daily commissions of ~$91m.

Sense check:

Gross $91m up to full 365 days for each 10-day cohort = $3.3b.

Compare to FY2025 service revenues of $4b, the remainder $0.7b is reasonably made up of insurers and membership fees.

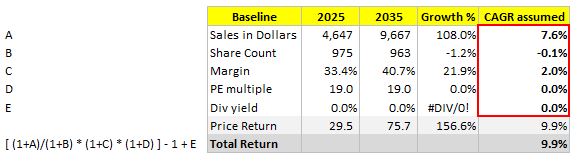

Scenario Model

Now we have a baseline, let’s simulate a scenario after 10 years where 50% of Salvage cars become Non Repair.

Our assumed changes from baseline:

Proportion of Non Repair increase +7% (from 3% to 10%), contributed by Salvage -7%.

Average retail price CAGR at +5.4%.

Average bid amount CAGR at +5% (slightly lower than retail price growth).

Commissions increase from 12% to 14%.

Number of cars auctioned increase from 350k to 400k (CAGR +1.3% represents total loss frequency trend).

Turnover unchanged at 10 days. Assume no operational improvements.

The average daily commissions works out to be $188m (CAGR +7.6% from baseline). This is essentially the sales growth rate we can expect if this scenario plays out.

Note: Vehicle sales segment (15% of revenues) assumed to grow at same +7.6%.

Finally, we can calculate our total return… To keep things simple, let’s assume:

No further economies of scale and overseas transition to agency model: +2% margins improvement come from hiking commission rate from 12% to 14%.

No more shares repurchases. Current 963 million shares outstanding unchanged.

PE ratio 19x unchanged.

Based on these inputs total returns is ~10%.

We think this is a decent return for such a conservative scenario.

There are upsides that we have not considered which require no heroic expectations:

Margins improvement from international expansion as CPRT slowly move from principal to agency model.

Share count reduction. CPRT has zero debt and $5.1b in cash against the current market cap of $27.3b.

Car auction sales turnover can be improved. CPRT is investing in their towing network to reduce friction in the whole process.