UNP: Union Pacific

Investment Thesis

We state the investment theme upfront: US railroads are a “picks & shovels” play on the future industrials commodities rush.

This article aims to provide an introduction to the economics of freight rails and why decarbonization benefits railroads, we argue that this is an idea that current market participants are not pricing in. We will focus on Union Pacific (UNP) and BNSF (owned by Berkshire).

History

During the years 1870 – 1900, also known as the Gilded Age of America, the country was experiencing rapid economic growth, heavy industrials, factories, and coal mining dominated the landscape. To facilitate all these industrialization, railroads were at the center of it. The first market index was created in 1884 and was originally known as the Dow Jones Railroad Average; it consisted of 11 stocks, including the New York Central and Union Pacific, and two non-rails, Pacific Mail Steamship and Western Union.

One of the famed businessmen who dominated the landscape was a magnate named Cornelius Vanderbilt. He got his start by making a name for himself in the steamship industry, where he earned his affectionate nickname “Commodore”. He then went on to build a railroad empire with the help of another famous businessman, John D. Rockefeller.

Other than being the richest man in America until his death is 1877, Vanderbilt was known for his brutally efficient approach to enterprise. At the time, US labour laws were nowhere near as robust as they are today, and he exploited that in the treatment of their employees. On top of that, antitrust or anti-competitive laws had not been developed yet, which led to coercive business tactics and aggressive acquisition activities. While this was certainly a net negative to society, it also led to Vanderbilt’s railroad empire growing into a force of nature, as its rail lines slowly but surely consumed the American landscape.

One reason for the stock market’s obsession with the railroad industry at the time was because they represented a new technology, effectively making them the “Tech Stocks” of their time. People could travel from the East to West coast in 3 days for the first time, before railroads they took weeks by ship or months by horses. Without laws against stock market manipulation, the market for railroad stocks turned into a place where management siphoned resources at the expense of shareholders, and also functioning as unsanctioned casinos, where speculators like Jesse Livermore earned their infamy.

Unfortunately, all things must eventually come to end, and so it was with the railroad industry as well. After antitrust regulations were developed in the post-Rockefeller era and Henry Ford popularized the automobile, railroads began their downward slide as they were gradually eclipsed by the more personalized mode of transport.

Airlines and trucking were also being deregulated during this period. Airline deregulation, an objective of the Nixon, Ford, and Carter administrations, was achieved with the Airline Deregulation Act of 1978. The legislation called for elimination of regulatory restrictions on domestic routes and services within three years, and complete deregulation of domestic fares within five years.

In July 1980, the Motor Carrier Act was signed into law by President Carter, deregulating trucking. The Motor Carrier Act eliminated most restrictions on entry, commodities carried, routes, and geographic zones.

The Stagger Act of 1980 came to the financial rescue of railroads, effectively reducing regulations on pricing. Mergers, declassification, and the Conrail breakup resulted in industry consolidation in the 1990s. Three events in particular had the largest impact on industry concentration.

1. In 1995, Burlington Northern merged with the Atchison, Topeka and Santa Fe Railway to form the BNSF Railway Company.

2. In 1997, the Union Pacific and the Southern Pacific railroads, the second and third largest railroads, merged and kept the Union Pacific name.

3. In 1998 and 1999, Conrail was broken up into roughly equal parts and absorbed into the CSX and Norfolk Southern systems. Also, in 1998, the Canadian National Railway, which had been privatized in 1995, acquired the Illinois Central Railroad.

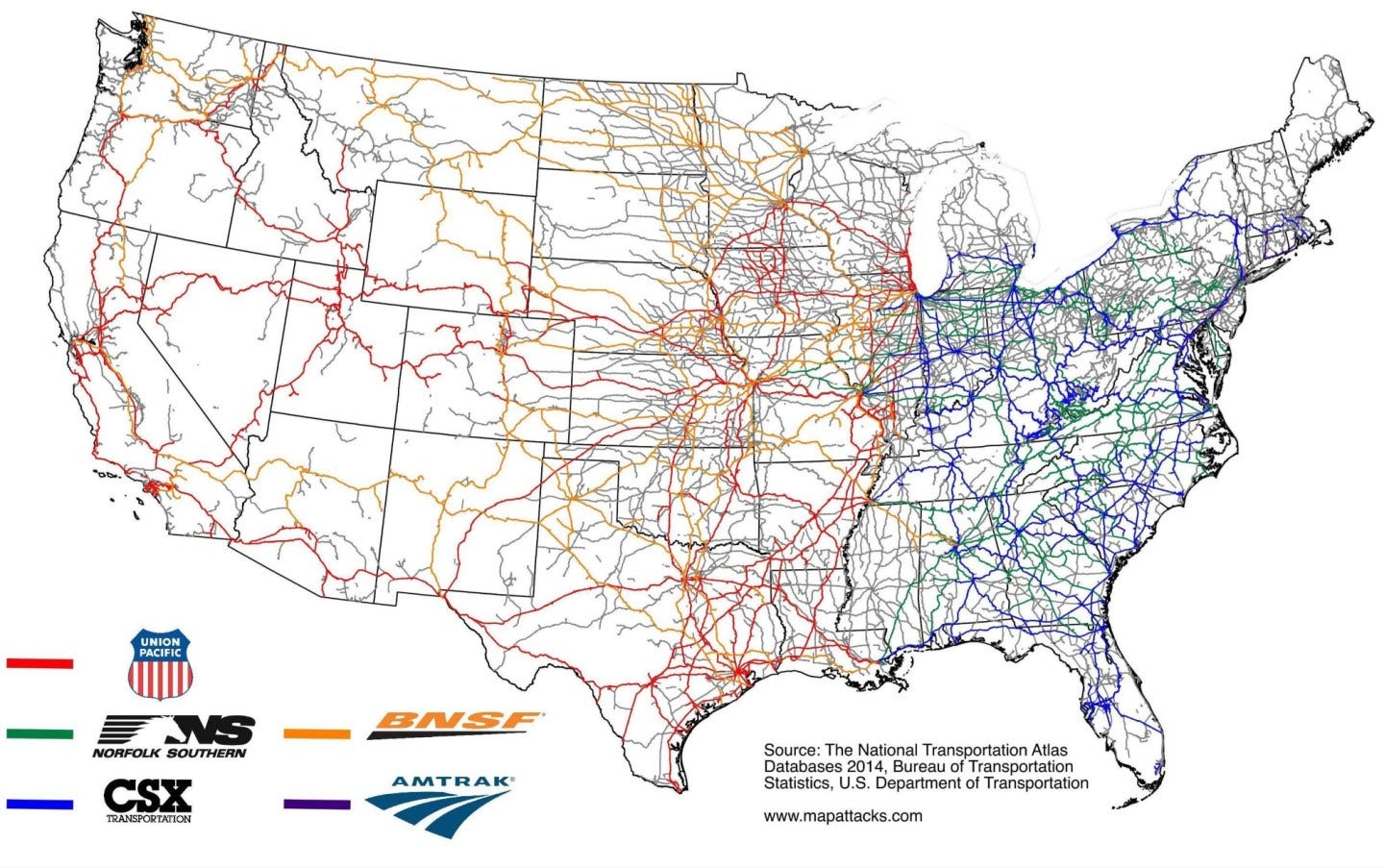

The beauty of being a shareholder of a Class 1 railroad (defined by inflation adjusted 1992 dollars as annual revenues over $250m) is that they are oligopolies. Over the decades, industry consolidation has led to the entire US rail network to just six Class 1 freight railroads, with Amtrak being a Class 1 passenger rail.

Although some of their railways do overlap, the entire rail landscape of North America can basically be split into 3 duopolies:

1. CNI and CP (now the merged CPKC) in the North & South

2. BNSF and UNP in the Midwest

3. CSX and NSC in the East

This means that at worst the competitive landscape is a duopoly, we can see this in the rail map below:

Eventually, Class 1 Railroads resulted in complete market penetration of the US economy. Most of the materials that railroads are best at carrying are very heavy and they need to be affordably shipped in bulk (coal, grain, chemicals etc.). Shipping by rail is significantly cheaper per-ton-mile than by truck for long distances. This means that the main customers of railroads tend to be industrial businesses like manufacturers, refineries, or energy companies whose priority is to ship their raw material inputs at the lowest unit cost. By virtue of their end-products being present in virtually every home, railroads tend to serve as a barometer for the health of the entire US economy.

Decarbonization Efforts are Long Run Tailwinds

Recent events have dramatically changed the growth potential of the railroad sector. The shift in global government policy towards ESG, renewables and electric vehicles (EVs) implies that there will be a huge shortage of commodities over the next generation, both in the US and globally. And with Class 1 Railroads being the cheapest form of transport for bulk commodities, this makes them the beneficiaries of this long term tailwind.

Both US and EU have set an aggressive deadline in 2035 before banning the sales of new ICE (internal combustion engine) automobiles, and 33% renewable energy penetration target within 10 years. Both also have aspirational goals of reducing net greenhouse gas emissions by 50% by 2030 and down to zero by 2050.

To achieve these high goals, the consensus is to do two things:

1. Shift from fossil fuels to renewables

2. Shift from ICE to EV transportation

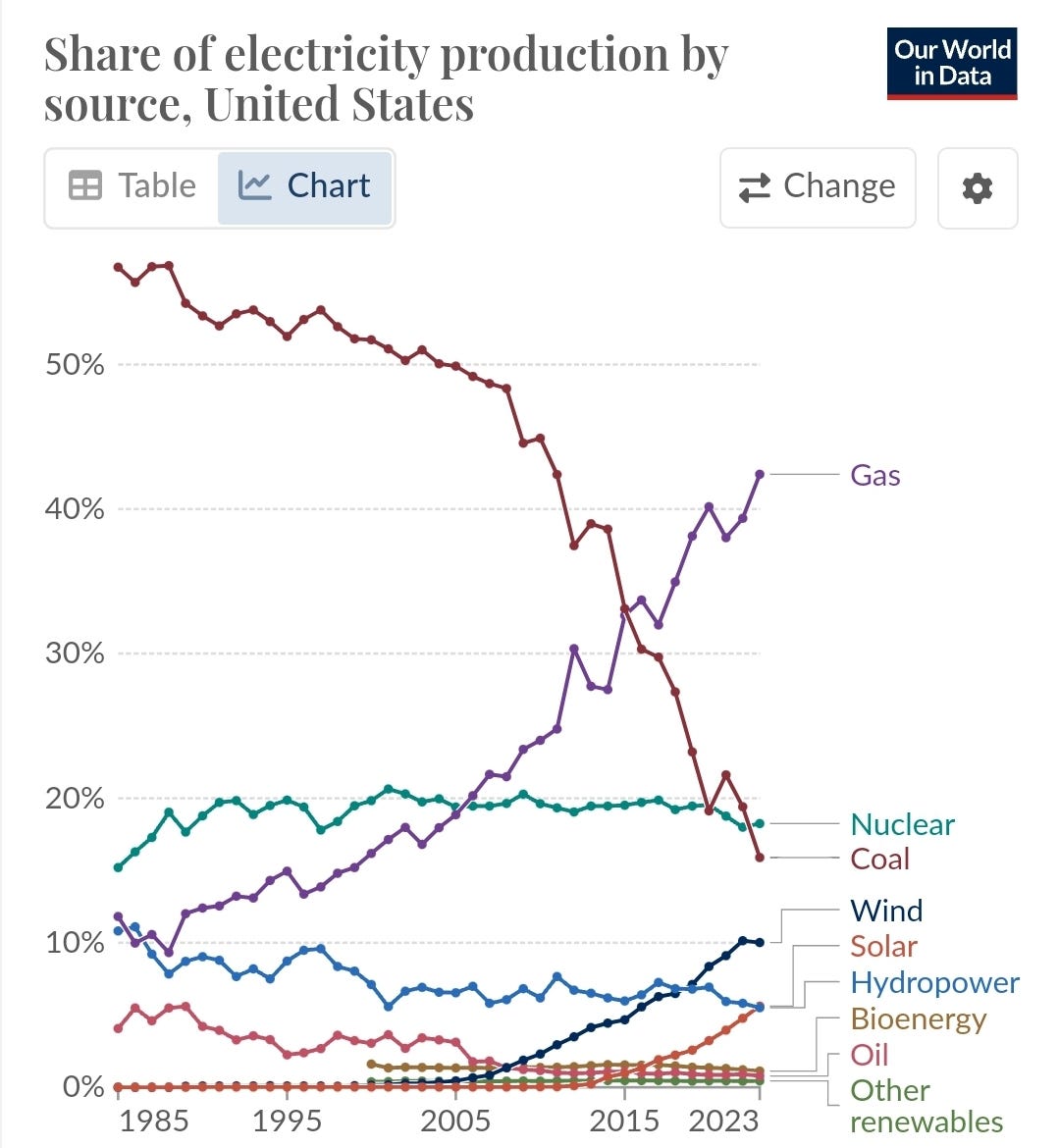

Firstly, to change fossil fuels usage to renewables like solar and wind is a very time consuming proposition. Currently the sources of energy generation come mainly from fossil fuels (coal, gas) of 79%, while renewables (hydro, wind, solar) make up 21%:

The practical implication of such a massive endeavor is to convince Americans to adopt solar panels. The economics of shifting to solar involves large upfront cost to install solar panels, which are equivalent to at least 10 years prepayment of energy bills, for the prospect of future savings which will only enjoyed 10 years later. Clearly, this isn’t an optimal solution for everyone.

Furthermore, solar panels actually require large quantities of commodities to manufacture: copper, aluminium, silicon & zinc. To ramp up renewables, these materials have to be shipped all around the country.

Also it’s going to be highly inflationary, because current productive coal plants are going to be shut down, and additional money is spent on wind/solar plants. Hence, productive capacity is not increased, we are just reducing carbon intensity.

We think that renewables are eventually going to take over, but the time frames are likely longer than expected. As an extra argument, the effects of on-going wars imply that the transition away from fossil fuels will take a long time.

Secondly, the situation for EVs is similar, although the story revolves around copper. Silver is the most conductive metal, and copper is second while costing 99% cheaper. This makes copper ideal for use in both the wiring and batteries of EVs. Nickel will arguably experience an even larger rise in demand, but regardless of which material these are commodities that will likely be shipped by Class 1 railroads.

EV penetration in US is about 7% now, if we expect 35% – 57% by 2030 then the future for copper looks bright.

On the supply side, the top 10 copper mines by production in the world today were all discovered multiple decades ago:

Copper is infinitely recycleable, estimates suggest that since 1950 there has always been, on average, 40 years of copper reserves and over 200 years of resources left. We don’t think there will be a shortage of copper to ship around on railroads.

The result of our arguments above is that we expect commodities to benefit from a large secular uplift that will last decades. Instead of playing the commodities world, we prefer to participate in the businesses that directly benefit from this, which is why we describe US railroads as the “picks & shovels” play on this trend. Coupled with the oligopolistic nature of the railroad industry, we think this is a growth investment thesis hiding in the most unlikely place.

Revenue Trend Reversal?

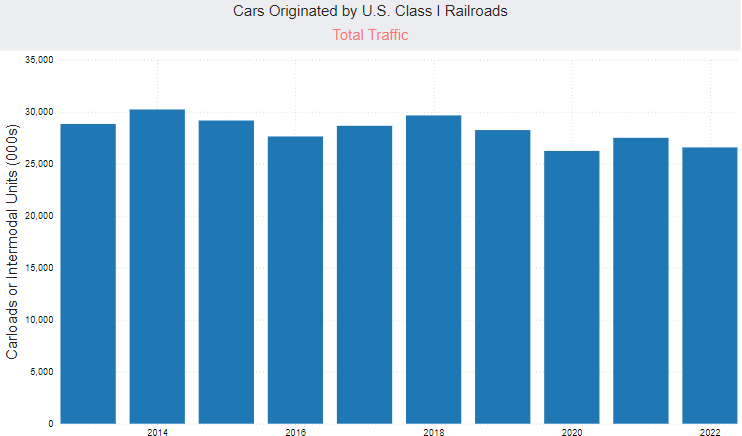

We claim that our thesis is obscure because US railroads have historically dismal growth:

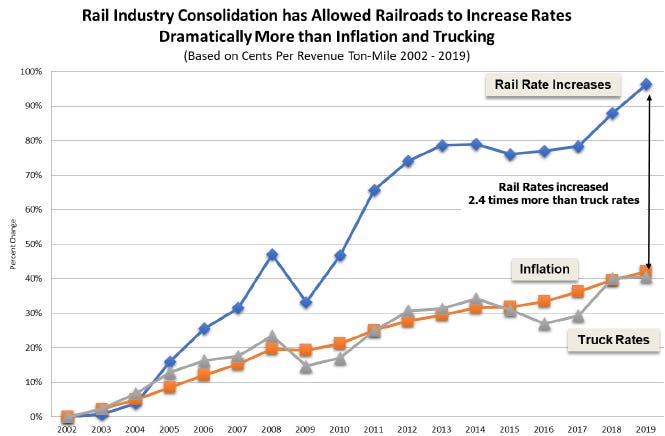

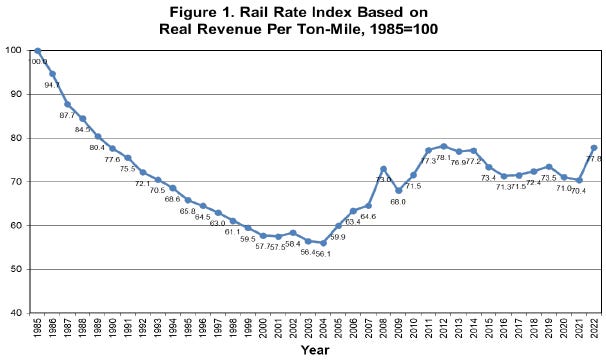

Volumes have been flat for the past decade, meaning that revenues are driven by price increases. Because of the oligopolistic nature, rail prices increased significantly:

This is an interesting trend because prior to 2004, real per unit rates had actually decreased consistently over the past 2 decades, starting from the Staggers Rail Act passed in 1980, which deregulated the industry. That upward reversal after 2004 coincided with Hunter Harrison’s introduction of Precision Scheduled Railroading (PSR):

Given the pricing power of railroads plus our prediction of a long run secular volume growth into the future, we think that the trend of stagnant growth is over.

Precision Scheduled Railroading (PSR)

No primer of railroads is complete without talking about PSR. The implementation of PSR in the railroad industry can be visualized as copying the approach used by the low cost carrier airline industry. Both Hunter Harrison (pioneer of PSR in 1993 and CEO of IC, CNI, CP, CSX) and Herb Kelleher (Southwest Airlines co-founder) were mavericks of their time who were comfortable going against the status quo in their search for ever new ways to cut costs.

To understand why PSR is so efficient, we need to contrast it with how railroads used to run before. Prior to PSR, railroads had 2 ways to optimize costs:

Hold-for-Tonnage

Schedule Adherence

The Hold-for-Tonnage method advocates having longer trains per trip in order to minimize unit shipping costs, since the marginal costs of shipping an extra load tends to justify the marginal revenue generated. This results in operators delaying shipments until the maximum train load has been reached, which increases complexity and costs, and makes rail service inconsistent and unpredictable to customers. Railroads utilizing this method would sometimes even delay a particular shipment to the next day simply because they didn’t want to pay for an extra shift of labour.

The opposite approach is Schedule Adherence which prioritizes trains following a fixed schedule. Naturally, this would mean shorter trains and shipping smaller loads resulting in higher unit costs. However, this method results in higher carload velocity and reduces complexity due to running shorter trains. Obviously, running trains according to schedule also improves customer service.

What PSR does differently is that it aims to combine the best of both worlds: running longer trains according to fixed schedules. In order to effect PSR, Harrison had to uproot the entire status quo of how railroads were traditionally run by removing hump yards to reduce network classification, and insisting on manifest trains rather than unit trains.

We need to explain some railroad terminology here:

Hump yards: They are literally tiny humps used to sort railcars by using gravity as the railcars go one-by-one down the hump they are led to their respectively assigned track. By removing hump yards, operators use flat switching where railcars are pushed by a locomotive to the assigned track, allowing large groups of railcars to be moved at once.

Manifest/unit trains: Unit trains carry one type of cargo while manifest trains carry many different types. Unit trains gained popularity in the 1980s as they could provide better service by dedicating to one customer, but they tend to return empty unless properly assigned which increases operating costs.

Balancing train network: Train yards used to be run as separate entities, while PSR views the entire train network as a single unit, maximizing railcar velocity and ensuring that trains are running on all lines in both directions at all times. This requires planning routes across the network in advance so that inbound and outbound trains are optimized on the supply and demand.

Point-to-point transit: Having as many point-to-point transit as possible reduces time wasted in classification yards. This can result in days of savings, and can only be achieved using manifest trains.

Longer trains, fixed schedules: By employing manifest trains instead of unit trains, different types of cargo from different customers can be attached to the same outbound train, which allows the maximum train length to be reached more quickly. This also facilitates fixed schedule adherence, as trains can still leave the station even if certain customers do not adhere to pre-determined schedules.

Operating Ratio (OR)

OR is the most common metric used to measure the success rate of a railroad’s operations, it is simply:

OR = Operating Expense / Revenue

This is just another way to look at operating margins, and it measures the efficiency of the rail network. Lower OR means higher operating margins.

At the end of the day, consolidating networks, eliminating less efficient lanes, increasing speeds and sizes of trains, and reducing payrolls are all in service of decreasing OR.

A variety of strategies can decrease OR like decreasing labour costs, removing older trains or railcars from the fleet, and implementing newer more efficient equipment and technology. PSR is the most popular and lucrative means of decreasing OR.

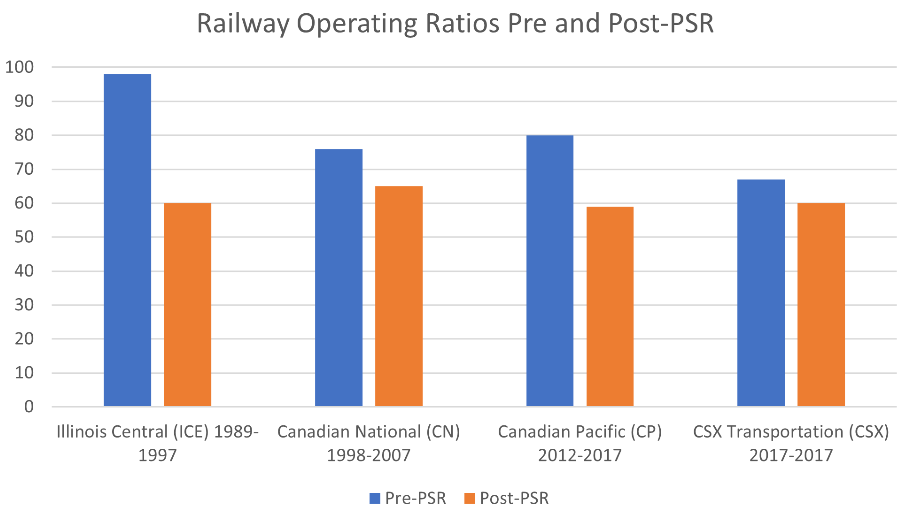

We can see the massive impact Hunter Harrison had on railroads:

Competitive Advantage #1: Irreplaceable Tangible Assets, Duopoly, Pricing Power

Now that we got some basic background of the railroads, let’s examine moats within this industry.

Back in the 1800s, a lot of the land where tracks were built was owned by the federal government. The way that they incentivized companies to build that railroad, was to pay them for the amount of track they built, and also to grant them the land rights on the track that they built.

Rail companies owned basically miles of land on each side of their track. Interestingly over time, a lot of that land became incredibly valuable in the oil and gas market. In the 1990s, Union Pacific Resources Group was one of the biggest oil and gas producers in the US. They sold the business to Anadarko for $4.4b in 2000. But it just goes to show how much value came from the track and land rights.

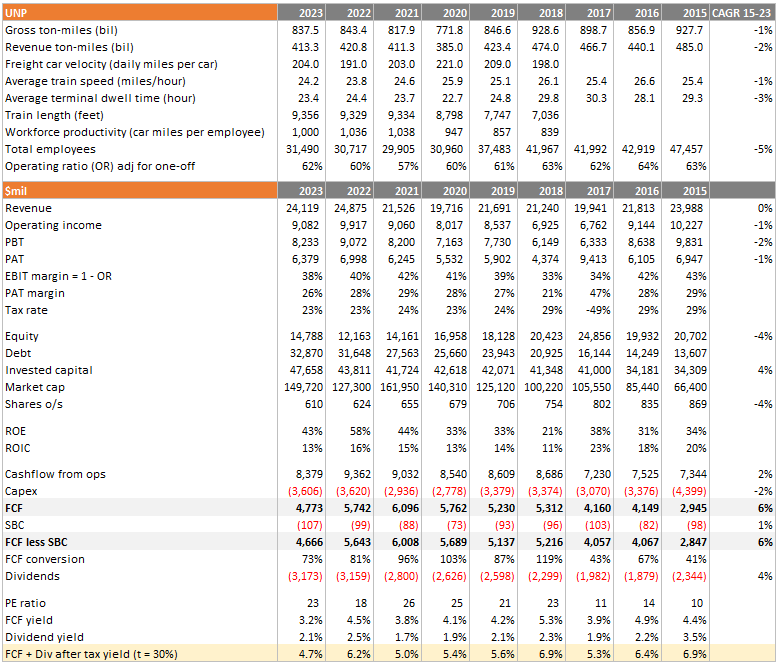

As at 2023, UNP has 32,693 miles of tracks, most of them built 100 years ago (26,110 miles owned, remainder leased). We don’t know what is the cost of 1 mile of track but it’s logical to assume that it is practically impossible build another network of tracks due to regulations around land rights.

UNP operates 7,154 locomotives, these are 40 years useful life assets and they cost several millions of dollars each. For railcars, UNP operates 59,189 units split between owning 56% and leasing the rest.

All these large numbers put together basically give rise to very valuable cash generating long lived real assets that deter new entrants. This results in a permanent duopoly and pricing power shared between BNSF and UNP, which are the top 2 largest railroads by revenue in the US.

Every year, railroads hike prices between 3–4%. Pricing is a function of length, width and weight of the cargo. For intermodal, railroads have lesser pricing power and they are working through intermediaries (eg. JB Hunt, Schneider, Knight Swift) who all have intermodal operations. And those are the companies that interact with the end customers.

Competitive Advantage #2: Volumes Origination, Lower Dwell Time

A high percentage of volumes origination means that the railroad is not handing off cargo to another railroad. This happens at train yards costing money and increases dwell time.

The average industry dwell time (2018 – 2023) is about 27 hours, while UNP dwell time averages 25 hours.

One driver of lesser time wastage is that UNP has a higher proportion of originating volumes, so they dont have to transfer railcars to continue the journey.

Competitive Advantage #3: Rail Network

UNP, as a western rail, covers 2/3 of US land area with long haul lines that don’t intersect. Contrast with the eastern rails covering 1/3 land mass but actually touching 2/3 of the population mass. Therefore, in the east, they have a “spaghetti network” where train tracks intertwine, and that can create challenges. Because tracks that have more stops and starts are more challenging to operate efficiently.

Competitive Advantage #4: High EBIT Margins

UNP produced average EBIT margins of 38% for the past 10 years. This is surprising to know that Microsoft, an asset light business, also had the same average EBIT margins over the same period!

However, we have to remember that in the past before Hunter Harrison implemented PSR, railroads were only earning 10–15% margins. The increased profitability is attributable to railroads running longer trains, using lesser people and fewer stops.

Another reason is in the accounting: depreciation of these long lived assets. The useful life UNP estimates (2023 10K pg. 63) for tracks are 34 to 47 years. Equipment life ranges from 17 to 23 years. Technology life is 12 years. This will create a low free cashflow conversion ratio as depreciation expense is lower than CAPEX.

Risk #1: Volume Mix and Margins

In the past, coal volumes were a huge source of revenue (~30%) and high margins for UNP. However, due to recent decarbonization initiatives, the volumes have reduced. In 2018, coal was 12% of total revenue. Five years later in 2023, it decreased to 8%. Margins on coal remained stable (2018: $2,216m per car, 2023: $2,211m per car).

On the other hand, volumes % of total revenue of metals & energy segment was flat (2018: 22%, 2023: 21%). Margins measured on per car basis improved by 4% (2018: $6.8b, 2023: $7.1b). In terms of number of railcars it was also flat at 1.4m.

Our thesis requires that volumes of industrials increase and that might not materialize. Suppose that we are right, there is still an unknown if the rail network is able to support the extra volumes, if not the railroads will require additional capital investments. This cost factor can possibly offset the gains.

Risk #2: Pricing Regulations

The reason why railroads have been able to escape cyclicality, although their business is tied to industrials and consumer demand, it’s because of the oligopolistic nature. Compared to air freight and trucking where barriers to entry are relatively lower and pricing is competitive.

PSR has enabled railroads to earn high margins but by operating this way it might attract regulators. For example, when CSX went through their change to PSR, there was a lot of disruption. So shippers constantly having issues. Although CSX was producing strong numbers, there was a lot of frustration with shippers, to the point where the STB (Surface Transportation Board) had weekly calls with CSX.

Risk #3: Labour Unions

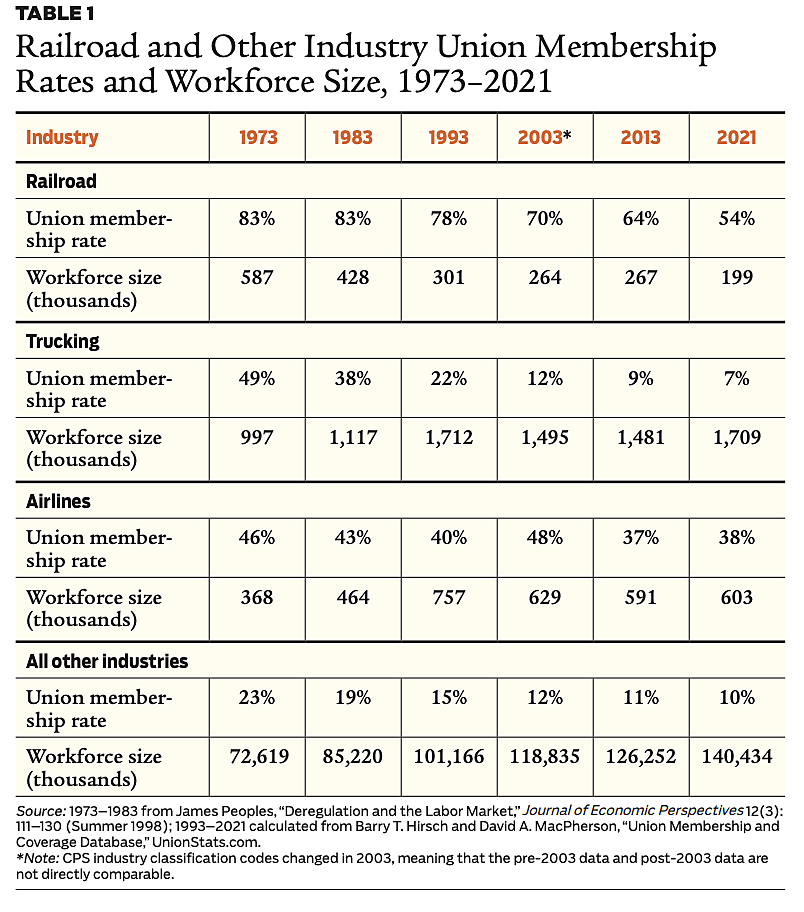

Today, union membership has decreased substantially but is still much higher for railroad employees at 54%, compared to 38% in the airline industry, 7% in trucking, and 10% in other private industries. Meanwhile, the railroad workforce sharply declined from 1973 to 2021, while the workforce in the other industries increased. Within some specific rail occupations, such as locomotive engineers, union membership rates remain even higher, at nearly 80%.

Efficiency usually means employing lesser workers for more output and unions dislike reduced employment. Unions argue that railroads are making record margins but workers are not compensated well enough, on the surface it might look true but the profits are not driven by volumes. One of the most important revenue drivers is coal and volumes have been declining, the offset is from lower fuel cost and tax cuts in 2017.

Labour union friction is inevitable, the latest strike happened in 2022 with unions proposing a contract for immediate 14% wage increase and 24% salary increase over 5 years, plus 1 day of paid leave per year.

Capital Allocation

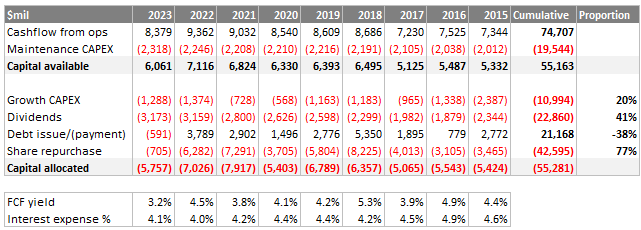

Below shows UNP capital allocation cumulatively since 2015, available capital is returned to shareholders through dividends (41%) and repurchases (77%):

We assumed maintenance CAPEX is equal to depreciation and the remainder goes to finance growth. The deficit was financed by debt. The debt cost and free cashflow (FCF) yield are quite close, this explains why UNP chooses to do share repurchases rather than dividends which are taxed.

Management and Incentives

Incentives structure are rational:

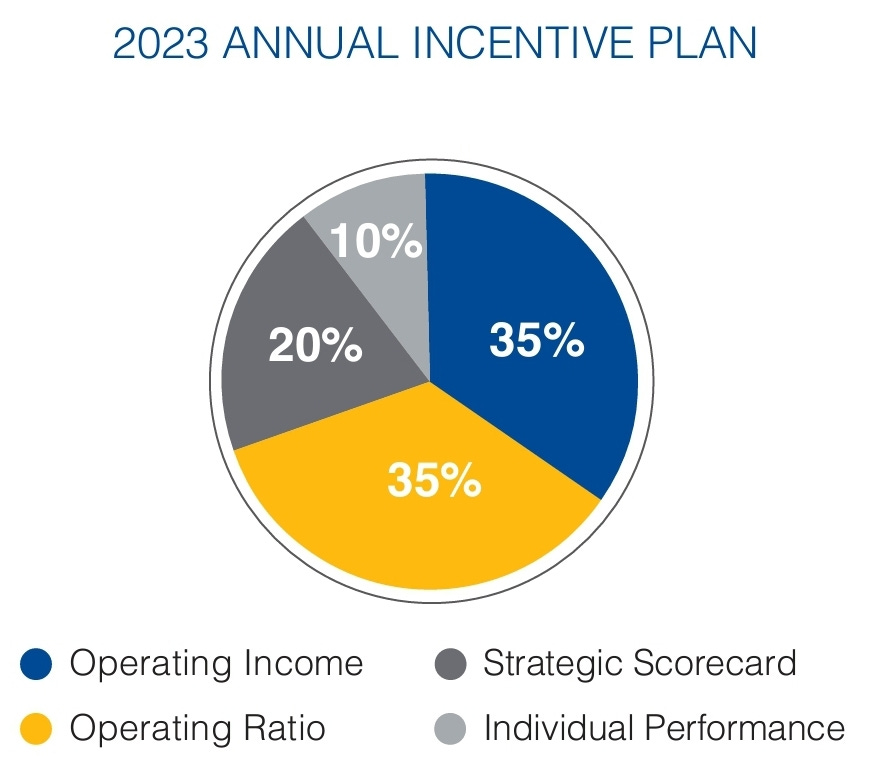

1. Equity incentives for management involves over a 3 year period ROIC growth and operating income growth, 66% and 33% weightage respectively.

2. Annual incentives payout below:

James “Jim” Vena is the recently promoted CEO of UNP in August 2023. Jim worked in railroads all his adult life, beginning his career at Canadian National Railway (CNI) as a labourer in maintenance, then a brakeman, conductor, locomotive engineer, train-master and superintendent. He progressively held roles of increasing responsibility, including senior management positions in Operations, Marketing and Sales. At CNI, Vena was ultimately promoted to Executive Vice President and COO. He ran operations until retirement in 2016 after 40+ years.

Valuation: BNSF first!

Let’s study Berkshire’s purchase of BNSF to get a benchmark at what price did Buffett buy the railroad.

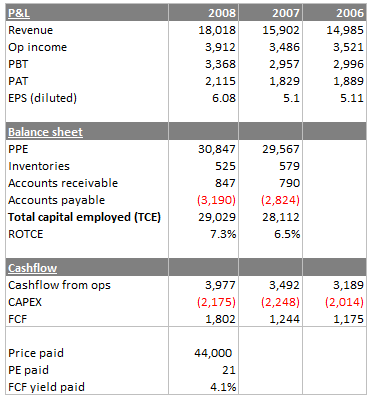

Buffett made his purchase of BNSF in several tranches. In total he paid $44b to fully acquire BNSF:

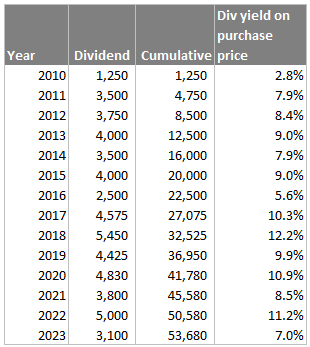

If there’s anything similar to a 100-year bond, it must be a well run railroad. Over the years Berkshire was able to collect dividends and made back the purchase price in 10 years, for context the 10 year Treasuries in 2010 was 3.2%:

BNSF will no doubt continue to generate cashflows and return it back to Berkshire for many decades to come.

So Berkshire paid around 21x PE multiple and 4.1% FCF yield, how does that match up with UNP today? Note: the actual multiple is between 17–21x because Berkshire bought through years 2006 to 2010.

Valuation: UNP

Based on current market cap of $138b, these are the multiples:

Trailing PE = 21.6x

FCF yield = 3.5%

Dividend yield = 2.1%. After 30% with-holding tax = 1.5%

We run a reverse DCF to see what kind of growth profile can justify $138b market cap, and whether the outcome makes sense to our thesis.

FCF less SBC is $4.7b reported in 2023, we need to make some adjustments to normalize the changes in working capital. We apply a historical % of working capital over revenues. The adjusted 2023 FCF less SBC is $4.9b.

Using $4.9b as a starting point, we grow 1.5% annually for 10 years, and set terminal growth of 2.5%.

Discount rate = 7%.

Less debt and lease liabilities and add back cash.

This set of assumptions above solves for today’s market cap. As expected, most of the value is in the terminal value and we are quite confident that UNP can last beyond our investment lifespan.

Conclusion

Market cap of $138b is not extremely cheap, but also not unreasonable given the strengths of the railroad industry. We will look to add positions in tranches.