Study: Tyler Technologies

Preface

Happy Chinese New Year! Here's some reading to kill time… This is a short study, there’s no valuation/financials.

When studying Constellation Software (CSU), we came across Tyler as a competitor in the government VMS niche.

History

Origins & LBO craze

Tyler Technologies was founded in 1966 under the name Saturn Industries. The founder Joseph F. McKinney was a Harvard graduate, early in 1960 he started a business with James “Jimmy” Ling named Electro-Science Investors, a venture capital firm which invested in high-tech companies.

The venture went well and McKinney became a millionaire at 28 years old. However, these were just paper profits and their firm collapsed 3 years later. The company accumulated $800k in debts and seeked refuge in Chapter 11 bankruptcy.

Returning back to his securities business, McKinney would cross path with Jimmy again, and this time Jimmy asked for his help to dispose of three military suppliers from his company. Saturn Industries was created to settle these liabilities.

By the way, an interesting fact: Jimmy gained control of Wilson & Co. in January 1967. Wilson sold meat and produced by-products such as leather for footballs and pharmaceuticals from animal organs. One of the things Wilson produced is basketball skins for NBA:

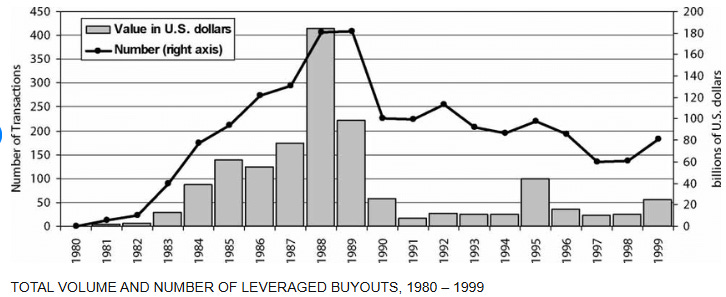

Going forward to the 1980s, McKinney was already 50 years old. This period marked a decade of leverage buyouts (LBO) and high yield junk bonds created by Michael Milken and Drexel.

More than 2,000 LBOs occurred between 1979 and 1989 for a cumulative value of over $250b.

For example, two incredible LBO deals were Gibson Greetings and Sterling Jewelers.

In 1982, a group of investors acquired Gibson Greetings for $80m, with only $1m equity. Just 16 months later, they went for IPO valued at $290m!

In 1985, private equity firm Thomas H. Lee Partners acquired Sterling Jewelers for $28m with just $3m equity. Two years later, they sold the company for $210m. Then 3 years after, in 1990, Sterling Jewelers was purchased by Signet, the world’s largest jewelry retailer.

These LBO deals made alot of money and culminated with KKR’s enormous $31.1b acquisition of RJR Nabisco in 1989, and eventually bankruptcy of Drexel in 1990.

McKinney attended the 1985 Predators’ Ball conference in the Beverly Hilton Hotel Los Angeles. Organized by Drexel, it served as a yearly nexus for companies seeking junk bond funding. He recounted his experience:

“Joe,” argued the director, “the banks wouldn’t do these deals if they didn’t hold water.”

McKinney: “If you evaluate deals based on what the banks will lend on, you’re in trouble.”

Not long after his director tried to get him to buy more assets, McKinney decided it was time to sell.

At that time (1987), Tyler had operations in electronics distribution, specialty coatings, explosives and cast-iron pipe and fittings for the construction industry; just the kind of collection of assets the raiders were looking for.

Since McKinney only owned 5% of his company and didn’t have controlling votes, there was real risk of LBO raiders coming in to flip the company.

McKinney also knew that corporate raiders would pay for less than the intrinsic value of Tyler. So instead of an insiders’ buyout to benefit management and hurt shareholders, he decided to sell off pieces of Tyler.

This was a very unconventional, highly ethical move.

From the third quarter of 1988 to the end of 1991, Tyler shareholders received a total of $21.96 per share of value from:

$0.445 regular cash dividends.

$10 special dividend after the sale of Hall-Mark Electronics (1988).

$4.87 worth of Akzo securities for each share of Tyler from selling Reliance Universal (1989).

$6.64 of ICI securities from selling Atlas Powder (1989).

At the end of 1991, Tyler’s share price traded at a high of $3. Adjusting for the total value of dividends and distributions during this time, the adjusted price would be $24.96 ($3 + $21.96). Compare this to the share price $15.5 in 1988 before all these happened, it was a total return of ~61% over 3 years.

After selling those 3 businesses, Tyler had reduced its debt significantly and had cash to buy new businesses.

So they acquired Forest City Auto Parts in February 1991. Tyler paid $26m, with potential future earnouts of up to $6.6m.

Tyler’s second acquisition came in 1994, acquired Institutional Financing Services (IFS) for $50m, a company that assisted schools in fund raising by arranging for students to sell company-supplied gift items to family and friends.

Next year in 1995, Tyler would sell their last industrial business Tyler Pipe. They had this company for 27 years and sold it to McWane for $85m.

McKinney Resigns

This sale marked a new chapter in Tyler’s corporate life as an industrial conglomerate. McKinney wrote in the 1995 annual report:

With the completion of the sale of Tyler Pipe, it’s time to consider the next phase in Tyler Corporation development. The Company is considering a range of strategic alternatives including acquisitions by Tyler, divestitures of existing operating companies, or merger into a larger company… Deliberations will be directed towards the long-term good of stockholders.

However, things didn’t go well for Tyler. Forest City and IFS never performed well post-acquisition. Forest City had to compete with larger auto parts retailers like AutoZone, while IFS faced its own competitive pressures from school sponsors. Sales declined year after year since 1994 and both businesses reported operating losses in 1996.

With several years of consecutive lousy results, Tyler took a massive goodwill write-off and restructuring charges. The cumulative goodwill write-off was $52.1m and restructuring charges were $9.9m.

After three decades of leading Tyler Corporation, Joseph McKinney announced his retirement on October 7, 1996. Unfortunately, he died just 4 years later at age 69.

So, Bruce Wilkinson came onboard as their second CEO. Shortly after, Louis Waters, a recently retired businessman, invested $3.5m for 10% ownership. Waters became Chairman and convinced Tyler’s directors to sell Forest City and IFS and then pursue acquisitions of vertical market software (VMS) businesses serving local governments.

However, this was pre-internet era and Wilkinson did not see the potential of VMS, he wanted Tyler to go back to its industrial roots. He lost out to Louis Waters and resigned just after 1 year.

Second Corporate Life

Clarence Rundell took the CEO job in 1997 and from 1998 onwards, Tyler would transform into a niche acquirer and operator of government VMS.

After selling IFS for $8.4m and Forest City for $24.5m, they took the money to buy 3 companies in the government VMS space:

Business Resources Corporation

The Software Group

Interactive Computer Designs

Waters’ strategy of providing IT services to public sector proved to be a big success:

Our plan is to consolidate the information industry for local governments. We are looking at smaller counties, municipalities, cities and appraisal districts or police and court systems. They need to computerize their record keeping, dispatch, tax collections, land records, deeds, probation; the possibilities are vast.

Just when they thought everything was bright and cherry, the internet bubble burst and Tyler’s stock nearly got delisted after trading at just $1.18. The whole enterprise value was tiny at $50m.

During 1999 and 2000, Tyler had cash outflows and made losses, they sold Business Resources Corp for $71m and disposed the remaining businesses and assets of their information and property records services segment. Tyler survived by raising common equity worth $9.3m just to meet payroll.

Since then Tyler prospered by acquiring over 45 software companies. John Marr joined Tyler in 1999 through the acquisition of Munis and replaced Rundell in 2004. Marr then transitioned to Executive Chairman in 2018 with current CEO Lynn Moore taking over.

Lynn Moore joined Tyler in 1998 was its first in-house legal counsel. His first tasks were asbestos claims that stayed with Tyler after they sold the old industrial businesses. He went around the insurance companies who didn’t want to pay claims and struck deals with plaintiff lawyers. The insurers became tired of the lawsuits and eventually settled the liabilities of ~$200m when Tyler was just worth $50m.

Fast forward to today, the VMS government market is key to Tyler’s success, they saw revenues increase from $50m in 1998 to $2.1b in 2024, while margins expanded and operating cash flows went from under $1m to $5.2b!

Industry Characteristics

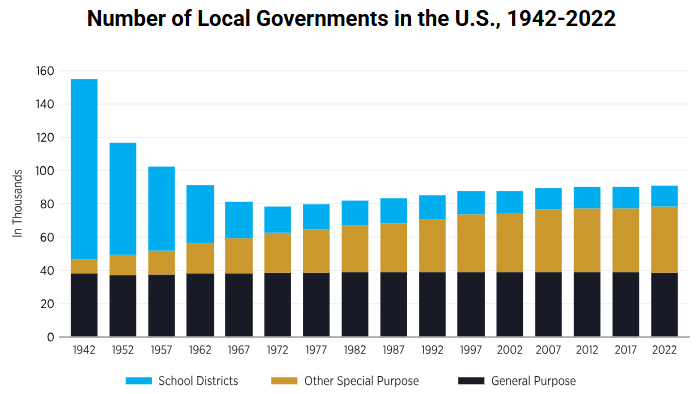

America’s founding was grounded in a preference for limited government. Because of this, governmental power is divided vertically across the federal, state and local levels and horizontally across branches of government and different general and special purpose government entities. The result is a vast patchwork quilt of more than 90,000 different governments.

In 2022, there were a total of 90,837 local governments in the US:

The definition of “government” is:

It is organized.

It has a governmental character.

It is substantially autonomous in the sense that it determines its own budget and is not directly controlled by a parent government.

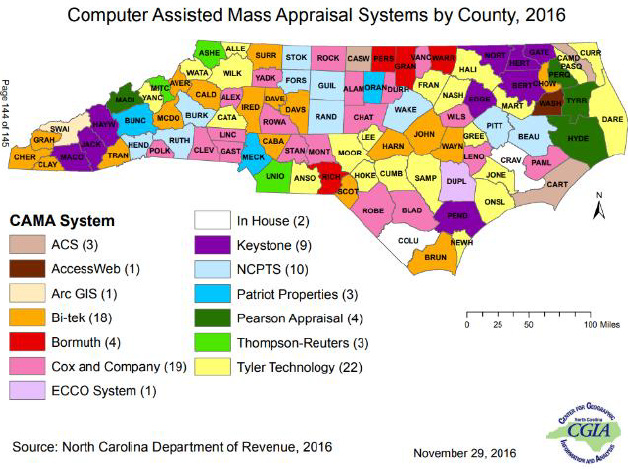

As a result, the market is very fragmented. Take a look at how many VMS players are serving just the North Carolina state:

Tyler operates in the niche government VMS, ranging from justice courts, prisons, K-12 schools, student transportation etc.

Because there are so many differences between the needs of all these government entities based on laws and regulations, Tyler’s success hinges on their long history of knowing and working together with clients. This advantage is why VMS players are hard to replace. They provide specific, tailor-made software solutions to a niche market that is has very sticky customers.

Out of all the fragmented competitors, a significant portion of them are actually ripe for acquisition. Because government entities are slow to change, their systems are decades old, so many software vendors are not competitive anymore. Either they lack the resource, or the software was created in-house. A large number of these players must eventually be replaced and this supplements Tyler’s business runway.

Tyler leads the industry with 11.2% market share in 2024, implying a TAM of $19b.

Sales Process

Selling to local governments is not easy because they tend to use their systems for 30 years without much replacement. However, these systems are also mission critical while costing a fraction of their budgets. Think about a prison management system that is at its end life cycle, when it needs to be replaced it’s a high priority action. Therefore, regardless of the economic cycle, Tyler will still collect recurring revenues.

The evidence is in their gross customer retention rates of 98%. Once a local government becomes a customer, they never leave. For example, St. Louis County has been a client of Tyler’s Appraisal & Tax software since 1980, then in 2012 they moved the permit processing process from in-house to Tyler’s software.

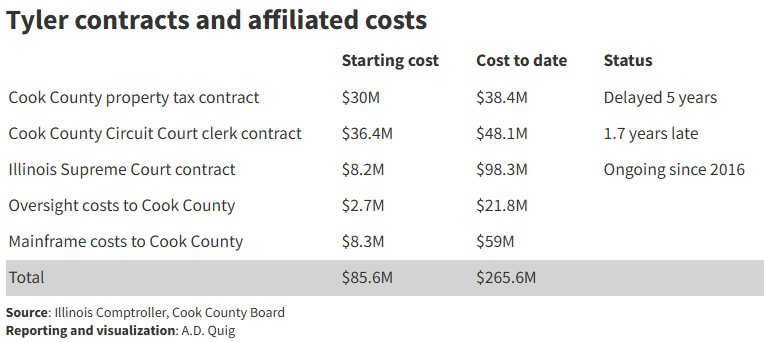

Below are some examples of super old systems that were replaced by Tyler. Not all projects go smoothly, yet these counties have no alternative, it shows how difficult these VMS are to implement and why AI is not going to disrupt this niche:

Cook County 2017: Modernize court and property tax systems. Although the project was delayed and ballooned in cost, the officials have no choice but to continue.

Kenosha 2025: Replaced 40+ years old in-house ERP software. They are already using Tyler’s Enterprise Public Safety solution.

Arizona 2024: Replaced 20+ years old in-house court case management system.

Long Beach 2017: Replaced 25+ years old systems consisting of 17 modules, now integrated into Tyler’s ERP solution.

Clayton County 2018: Replaced 20+ years old ERP system.

Put together, when a local government decides it’s time to upgrade or change its systems, it is because they must.

For example, the city Fredericksburg had used a ERP package from Bright and Associates for 30 years. It ran on AS/400 (IBM computer system first introduced in 1988 and discontinued in 2013). The city made a request for proposal (RFP) in 2016:

There is a waning availability of AS/400 programmers to work on existing applications or develop new products on the AS/400 platform. In addition, many users find the current software deficient in various ways (functionality, usability, accessibility, etc.). Consequently, the current software is either underutilized or fails to provide desired services and results.

Tyler won the contract and was awarded $1.3m with annual maintenance of $130k.

Another interesting aspect: Local governments do not compete against each other like businesses in the private sector.

If a government employee has benefited from a Tyler product, they will likely share their experiences with their peers. Likewise, bad experiences spread fast.

This dynamic favors a company like Tyler that has the resources to invest heavily in its people and products to produce the best customer experience.

In summary, there are 3 important facts about the sales process:

Customer lifetime value is extremely long.

Systems will eventually need to be replaced/improved and existing customers don’t switch providers if they are served well.

VMS is a people business. Technology (code-base, UI/UX) is a small factor in winning customers.

Economies of Scale

The playbook for Tyler is different from CSU.

CSU don’t pursue economies of scale because CSU is in the business of acquiring many small VMS firms across 100+ verticals, they have to decentralize and push capital allocation down to the business unit level. There’s no such thing as corporate level allocated expenses.

However, Tyler focuses only on one vertical market. So they will benefit from spreading cost over many customers.

It's easy to see the difference: Tyler 8–10% organic growth target vs. CSU 2%.

In this case, the scale advantage that Tyler (largest market share) has over smaller competitors is important.

Moore said this in 2016 on the acquisition of ExecuTime:

I mentioned ExecuTime earlier, probably a few of us even remember that acquisition from a number of years ago. Very small, few million dollars in revenue. We bought it at a reasonable price point.

But the reality is when, 5 years later, those revenues start to accelerate and the revenues are several times what they were acquired at and margins start to expand because of the scale, they've improved the competitive position of your other products in those areas, like Munis and Incode.

You could say it almost doesn't matter too much how much you paid for them initially.

We can see the obvious difference in approach:

CSU cares about price because they're focused on IRR.

Tyler wants to buy companies that grow and embed themselves into the customer’s workflow.

Competition

The good thing about catering to local governments is that they are small and not worth the time for large software companies like Microsoft, Oracle, SAP.

But there are companies like Motorola Solutions, Axon, Hexagon, Journal Technologies, CSU etc. who compete directly.

For example, the Daily Journal Corp entered into the justice VMS at the same time as Tyler back in 1999. Today, they have Journal Technologies with more reasonable pricing and better servicing than Tyler.

Competition has also increased over the last decade from private equity (PE).

For example, CentralSquare came in 2018 when two PE firms combined their government VMS. But PE investing in this market does not work well because the time frames are longer and customer budgets are often much smaller.

Local governments want to be sure the companies behind their software are not going to flip ownership in a few years time. Financially, it’s more difficult optimize for operations for decades when PE firms are concerned with debt and eventual exit sale.

Business Model Shift

This is the interesting part. Tyler partnered with AWS in 2019 and started to shift into a SaaS model. This is similar to Adobe which transitioned to SaaS more than 10 years ago.

Why is Tyler so late on this journey?

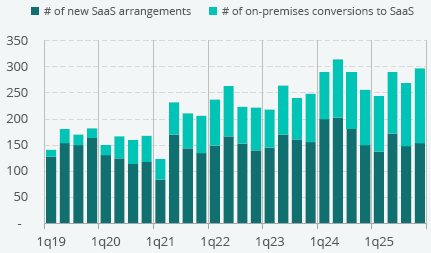

The main reason is that local governments are very slow to change, most of them are still on-premise until they are forced to adopt subscription model. Since 2019, Tyler has converted 2051 on-premise products into SaaS:

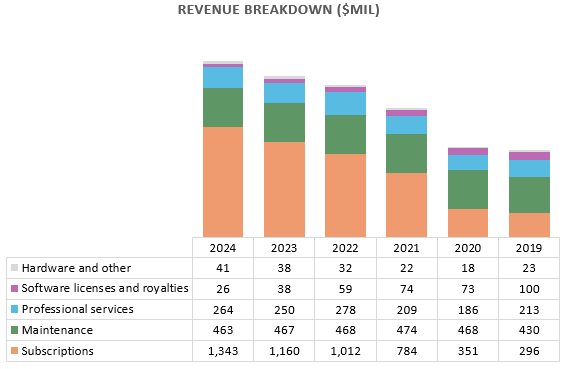

Only recently in 2024, the proportion of subscription-based new contract value was 96%. On the revenues split, subscriptions growth have outpaced everything else:

The benefits of SaaS:

Lower upfront cash outlay for customers.

High efficiency for software updates.

Able to adjust capacity based on usage.

The impact of SaaS transition is long-term positive, but can produce short-term fluctuations. These are just accounting effects and don’t represent the superior economic benefits of SaaS model.

Revenue growth will fall because subscriptions are smaller in quantum. Total lifetime value is still the same.

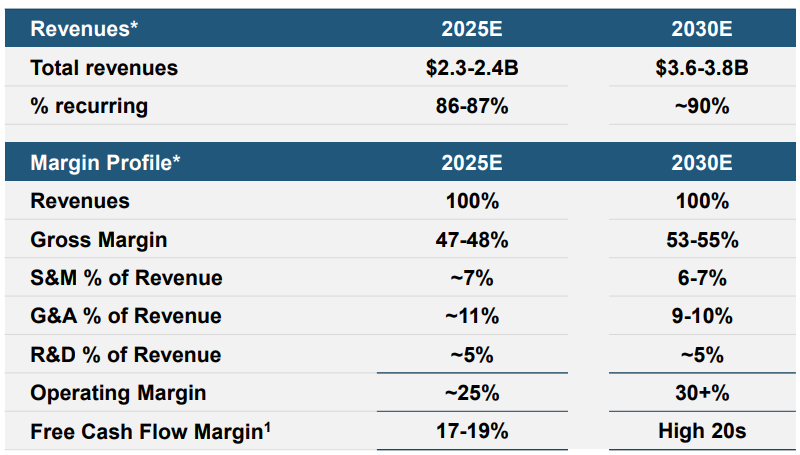

Investments on cloud are expensed off in 1 year instead of capitalized. Tyler’s goal is to transition everything to AWS and sell only SaaS, they aim to achieve low 30% range operating margins over the long run.

Acquisitions

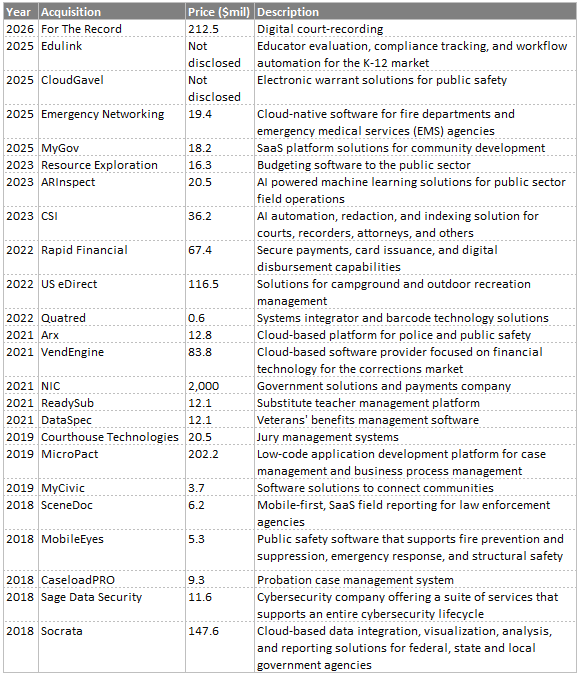

It’s natural for bigger VMS companies to acquire other smaller ones because the market is fragmented. This is a good way to expand the customer base. Tyler is not really a serial acquirer, over the last 25 years, they bought over 45 businesses. And since 2018, they bought 24 businesses:

We think M&A have produced meaningful results.

In 2015, Tyler acquired New World Systems (NWS) for $670m (public safety software). It was Tyler’s largest acquisition at that time. NWS had customer win rates in the 25—30% range. Tyler added record management and mobile capabilities, and integrated NWS with other justice related products. As a result, NWS was able to achieve win rates in the 50% range.

In 2021, Tyler paid $2b for NIC (18x EV/EBITDA). NIC enhanced Tyler’s expansion into software and services at the State level and also added a large transaction-based payments business. As of 2024, Tyler earned revenues of $698m from processing payment transactions, which they estimate is somewhere between 18—30% of the TAM for their current customers. NIC’s State-level agreements gave Tyler better and more opportunities to cross-sell too.

The latest acquisition was For The Record (FTR) which is expected to close in Q1 2026. FTR SaaS solutions offer sophisticated, secure, and accurate digital recordings that solve operational challenges and industry demands in all 50 US states, in an industry facing a declining number of court reporters. FTR has AI-powered tech for speech-to-text and real-time multilingual transcription. This creates synergies with Tyler’s digital record and case file solutions.

Recent Events

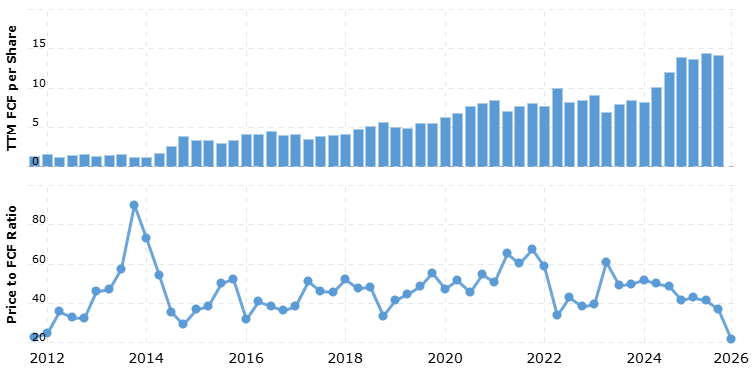

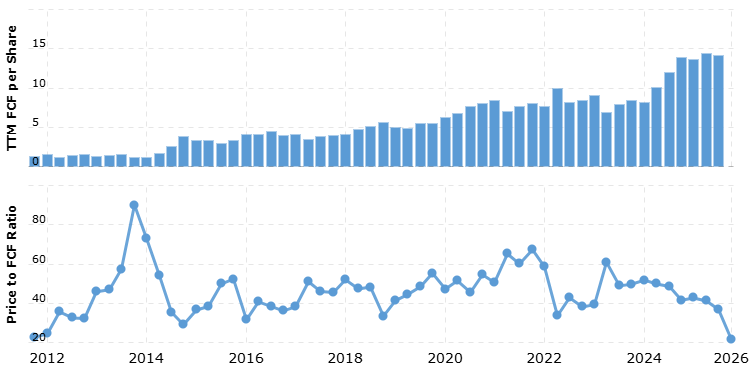

Lately there are concerns about AI disrupting SaaS businesses. As expected of public markets, there was indiscriminate selling of VMS companies like Tyler. The stock fell -36% for the past 5 years, while free cashflows have more than doubled from $211m to $452m (2021—2024, years that involved SaaS transition).

After reading everything above, you don’t need any more explanation why the fears of AI disrupting Tyler’s business are overblown. A better and cheaper product does not guarantee customers will use it. There are many other factors that have nothing to do with technology; relationships, trust, reputation, deep vertical industry knowledge etc.

Government entities want to know there is a company to call when something needs to be fixed. They don’t want to call their own IT people to do work that they paid Tyler for. And they need to know there’s a company they can sue if disaster happens.

Existing solutions are already solving their problems, AI competitors don’t add anything substantial that would incentivize them to replace their systems. Remember that they are reluctant to even change systems that are 30 years old!

With all those advantages in mind, we thought it would be fun to contrast with how the stock is priced now:

Tyler’s stock at $304/share is trading at 21.4x P/FCF multiple, the lowest ever since 2012.

Tyler operates with zero long or short term debt, with cash $745m. It has lease liabilities of $40m, the cash outflow from operating leases is just ~$13m per year.

Tyler’s business model is transitioning well into higher margin SaaS model.

That was a pretty interesting listen. Wasn't even aware that Tyler existed before

Can you provide an analysis of Kelly+Partners?