Study: Tencent

Five Co-founders

Tencent was founded in 1998 by 5 people. Incorporated in Shenzhen, the 5 co-founders are the current CEO “Pony” Ma Huateng, Tony Zhang Zhidong (CTO, 2014), Daniel Xu Chenye (current Chief Infomation Officer), Charles Chen Yidan (Chief Administrative Officer, 2013), and Jason Zeng Liqing (COO, 2007).

At initiation, Pony Ma invested US$33,000 giving him 47.5% share. Tony Zhang had 20%, Jason Zeng 12.5%, Daniel Xu and Charles Chen had 10% each.

Pony, Tony, Charles, and Daniel attended the same school in Shenzhen and performed very well, particularly in mathematics. All four subsequently began their studies at Shenzhen University. Only Charles studied chemistry while the rest took computer science.

Jason did not study in Shenzhen, but rather took telecommunications at the University of Electrical and Electronic Engineering in Xi’an. After graduating, he worked in sales at the Shenzhen branch of China Telecom.

After the founding of Tencent, the 4 Shenzhen graduates focused on product development, while Jason handled all sales and marketing matters.

Pony Ma Huateng

Pony Ma was born in Shantou in 1971, his family moved to Hainan Island, China’s southernmost province. He grew up in humble circumstances, and his father often struggled to find work. However, the family’s situation improved significantly when his father found a job at the port of Shenzhen and the family moved to the rapidly growing city in the Pearl River Delta in 1984.

At this time, Shenzhen benefited from a political upheaval, as Deng Xiaoping took over after the death of Mao Zedong in 1976. With reform and opening policies, Deng Xiaoping established 4 special economic zones: Zhuhai, Shantou, Xiamen, and Shenzhen, which borders Hong Kong.

The special economic zones are capitalist experimental regions, in which privately owned companies, independent production and investment planning, and foreign direct investment are permitted for the first time. With the momentum of these new opportunities, Shenzhen developed from a fishing village with only 30,000 inhabitants in the 1980s into a metropolis with over 12 million.

During his school years, Pony Ma developed a passion for astronomy and aspired to study this subject in 1989, but Shenzhen University did not offer a suitable program. He achieved a good result on the university entrance test, which would have allowed him to study at a more prestigious university such as Beijing or Shanghai instead of Shenzhen.

At the same time, however, the student protest movement was taking place in the country, and his parents did not want their son to be away from home. Pony Ma then changed his plans and began to study computer science at Shenzhen University instead of astronomy.

During the course of his studies, Pony Ma wrote computer viruses to lock the hard drives of his university computers, but eventually matured into a talented programmer with an obsession for good user interface design and a focus on user-friendliness.

Pony Ma achieved his first commercial success as an intern at Liming Network Systems, a network equipment supplier for the Shanghai and Shenzhen stock exchanges. During his internship, he developed a graphical user interface for stock analysis, which his employer purchased from him for RMB50,000, equivalent to three years’ salary for a college graduate at the time.

In a later interview for a permanent position at China Motion Telecom, Pony Ma scored highly with this very reference project.

Between 1993 and 1998, he worked as a software developer for pager-services that were popular in China in the 1990s. However, a corporate career did not undermine his entrepreneurial spirit, and in his free time, he set up a node on FidoNet (a precursor to today’s internet). Private individuals could send messages on FidoNet via their telephone lines. Among the first users were some of China’s later internet pioneers, including Lei Jun (founder of Xiaomi) and Ding Lei (founder of NetEase). Many contacts on FidoNet took place exclusively virtually, but Lei Jun and Pony Ma met in person for the first time in 1995.

Lei Jun was fascinated by the successful release of the world’s first free email service: Hotmail in 1996. Inspired by this, he founded NetEase in 1997 with an email service for the Chinese market. Pony Ma also took part in the successful IPOs of Yahoo and Netscape in the US.

Five Friends Come Together

In 1998, Pony Ma convinced his friend Tony Zhang to join him. Together, they recruited their former classmates, Daniel Xu and Charles Chen. However, none of the four friends had experience in sales or marketing, so they recruited Jason Zeng.

Pony Ma’s initial product idea aimed to connect the pagers to the internet, allowing text and voice messages to be received. At the same time, mobile phones were becoming increasingly affordable, and major telecommunications companies were no longer interested in further developing pager technology. For this reason, Tencent had to survive for the first 12 months primarily through contract software work.

First Product: OICQ

The dot-com boom was raging. In 1998, AOL acquired the Israeli messaging service ICQ for US$287m. The service did not generate any revenue yet.

During that time, 12 million users used ICQ for an average of 75 minutes a day. Word of mouth alone adds 50,000 new users daily. Tencent thought of developing a copy of ICQ for the Chinese market. The original calculation was that while such a service can never generate revenue or profit, a sale to a major corporation was a possibility.

At this time, in addition to ICQ, three clones already existed in China: CICQ (developed by Taiwanese NetSprite), and PICQ (later acquired by Guangzhou Telecom). On 10 Feb 1999, after only 3 months of development, Tencent released its own ICQ clone, called OICQ.

This service actually gained traction quickly. There were several advantages like storing the social graph of users on its own server instead of on local clients, it had a significantly smaller installation file, and also introduced the possibility of offline messaging. These measures led to a better product-market fit, since unlike in the West, most users in China use messaging services in internet cafes rather than on a home PC.

First Near Bankruptcy

At end of 1999, OICQ had 1 million Chinese users, but generated no revenues. They couldn’t find a way to monetize their service.

Operations were burning cash and with only US$1,000 remaining, Pony Ma attempted to sell the company entirely. He entered into takeover talks with a total of 6 companies, but none of them was willing to pay the asking price of US$400,000 (the highest bid was US$70,000).

Jason Zeng organized a meeting with the Boston-based venture capital (VC) firm IDG Capital, this is the first US company to provide venture capital to Chinese startups on a large scale. During the meeting, when asked how he sees Tencent’s future, Pony Ma replied that it is completely uncertain and that all he knows is that with OICQ, they have a product that people enjoy using. However, he doesn’t have a concrete plan for monetization.

Together, IDG and PCCW acquired a combined 40% stake in Tencent, paying US$2.2m. It was great timing as shortly after the dot-com bubble burst, a later entry with IDG and PCCW would likely have led to bankruptcy for Tencent.

Undaunted by all these business adversities, Tencent’s messaging service OICQ experienced unabated user growth, and they reinvested almost all the venture capital into new servers.

A copyright lawsuit by AOL forced Tencent to change its name from OICQ to QQ.

Second Near Bankruptcy

By end of 2000, QQ had 100 million users but still generated no cash. Having exhausted all of their venture capital, Pony Ma considered to sell his company again.

Enter David Wallerstein who was working for MIH, a subsidiary of Naspers.

Wallerstein was born in America but was fluent in Chinese and regularly spent time in Chinese internet cafes to see which services were popular with young people. He observed QQ’s rapid spread, and Pony Ma demonstrated the trends in daily new registrations (at that time ~500,000 new users per day).

Wallerstein subsequently offered to invest in Tencent at a valuation of US$60m and provide the company with further financing.

PCCW sold its entire 20% stake in this offer, and IDG sold 12.8%, making Naspers the largest owner behind the five co-founders with 32.8%.

Naspers increased its stake pre-IPO to 46.5% and allowed itself to be diluted to 37.5% through the IPO (today it holds 24.3%).

Tencent is currently valued at US$744b, making Wallerstein’s investment the best VC bet in history. This would be the last time Tencent faced financial troubles.

QQ Breakeven

Shortly after, Tencent solved the question of monetizing QQ. They copied a Korean website with customizable avatars (hairstyles, clothing, accessories…). Tencent copied this feature, just as it had previously copied the idea for QQ from ICQ.

Within a few months, 5 million QQ users were using the new avatar feature, paying an average of US$0.50/month. Sales rose to even higher levels when Tencent introduced the monthly “Red Diamond” subscription for US$1/month (this included a red diamond symbol next to the username, exclusive access to certain clothing/ accessories, and discount opportunities).

In June 2001, Tencent broke even for the first time achieving a revenue run rate of US$100m in 2002. In the following years, Tencent also very successfully monetized the sending of QQ messages via SMS to mobile phones in the form of the QQ Mobile product, which required a monthly subscription of US$0.50/month.

Going Public

In 2004, Tencent went public in Hong Kong with huge success. Shares were oversubscribed by 30x and IPO proceeds were US$200m.

Pony Ma commissioned Goldman Sachs to carry out the IPO. It was coordinated by Beijing-born, but US-trained investment banker Lau Chi Ping (Martin Lau). His hard work impressed Pony Ma and he was recruited into Tencent in 2005 as Chief Strategy and Investment Officer. Today, Martin Lau is responsible for Tencent’s investment portfolio.

Western Competition

MSN Messenger

Microsoft was planning to expand the distribution of their MSN Messenger (10% market share in China) with the help of corporate customers. These customers would use MSN in their offices, at that point in time QQ had 77% market share and the threat was real. Tencent decided to take over an email service called Foxmail in China that directly competed with Microsoft’s Hotmail.

Foxmail was developed by a talented programmer named Zhang Xiaolong all by himself. He was then tasked to develop the software as “QQ Mail” for Tencent. However, since he didn’t want to move from Guangzhou to Shenzhen, Tencent opened an R&D center in Guangzhou for him. Xiaolong still works from there today.

Although MSN announced an “anti-QQ alliance” with Yahoo Messenger in 2005 (opening both products to each other), MSN was unable to gain market share from QQ in the years to come.

In 2014, Microsoft finally shut down the MSN service in China. The reasons for this failure were QQ’s wider range of features and more frequent updates. QQ previously offered group chats, very large file transfers, and offline messaging, to which MSN responded only slowly and after consultation with its headquarters in the US.

Founded in 2004, Facebook already had over 100 million MAUs by 2008. The site was not blocked in China until mid-2009.

In 2005, Tencent launched Qzone, its own social network, a copycat of MySpace and Facebook. On Qzone, users can keep diaries, write blogs, and share photos. At the end of 2007, Qzone was monetized for the first time through a membership model for US$1/month. The subscription allows users to play background music on their profile pages and customize their backgrounds.

In 2009, Qzone experienced a major breakthrough thanks to a cooperation agreement with the Chinese game developer Five Minutes. It provided Qzone users with the social farming game: QQ Farm.

QQ Farm exceeded all expectations, and Tencent acquired ~4,000 new servers for this game alone in the second half of 2009. Millions of players spent money on virtual goods such as seeds, fertilizer, animal feed, and tools, generating significant revenue for Tencent.

Rise of Gaming

Tencent’s gaming division currently represents the group’s most important revenue source, accounting for 30% of total in 2024.

In fact, Tencent is the largest game publisher in the world, with Honor of Kings (王者荣耀, HoK) lifetime revenues grossing US$13.9b and PUBG US$9.5b.

However, the rise to the top was marred with failures. The gaming segment started in 2002, when they decided to acquire licenses for the Chinese distribution of the game Turf Battles from the South Korean developer Imazic.

Back then, Turf Battles was considered one of the most advanced MMORPGs, and Tencent offered players a price per hour played or a monthly flat-fee subscription.

Both offers turned into financial disasters for Tencent, as the game’s high computing and networking requirements were far removed from the actual conditions in China. This setback took some time for the team to digest, and it wasn’t until 2004 that a genuine relaunch was made.

For the second attempt, Pony Ma divided the employees into separate teams, each working on different game projects in parallel. He paid bonuses if milestones were reached and immediately restructured teams that weren’t making progress.

Tencent copied Ourgame’s casual games and merged them with QQ, allowing users to see their friends playing and join with one click.

After winning over Ourgame’s market share, Tencent started to copy more complex games from competitors like Nexon, and merging the games into the QQ ecosystem.

The breakthrough years of 2008 to 2009 saw Tencent acquire the rights to operate and market two games from South Korean developers; Crossfire and Dungeon Fighter Online.

These 2 games boosted revenues by +80% in Q2 2009!

In 2011, the acquisition of US developer Riot Games (League of Legends) was another internationally acclaimed coup.

In 2015, Riot Games rejected its Tencent’s request to develop a mobile version of League of Legends for the Chinese market. The prevailing opinion in the West was that AAA games shouldn’t be developed as smartphone versions, as this doesn’t do justice to the gameplay and quality of the franchise. Following Riot Games’ rejection, Tencent commissioned its own studio in Shenzhen (TiMi) to handle the project, and the first screenshots of the game noticeably strained relations:

They were blatantly ripping off our intellectual property.

Riot Games, 2015

Then, in 2015, Tencent released Honor of Kings, and today it also benefits from the fact that foreign developers are not allowed to operate as publishers in China.

HoK is estimated to have generated revenue of $1.9b in 2024, more than the original League of Legends on PCs.

Furthermore, Tencent has vertically integrated almost all stages of the gaming value chain over time, thus gaining a competitive advantage.

The group’s own publishing houses and film production studios can cross-promote for a popular video game. Tencent’s own gaming platform WeGame (similar to Steam) and the consolidated streaming service Huya (67% equity stake, 95% voting rights) serve as important marketing tools.

Copy, Copy, Copy!

After reading through so much of its business history, there is a common theme that surfaces; Tencent is very good at copying ideas and integrating it into their ecosystem.

Look at this poster from 2010 in Chinese magazine Computerworld:

Critics accuse Tencent of abusing its dominant QQ traffic, which would allow even low quality plagiarism to push competitors out of the market. Sina founder Wang Zhidong even publicly calls Ma Huateng the “King of Copying”.

In America, when you bring an idea to market you usually have several months before competition pops up, allowing you to capture significant market share. In China, you can have hundreds of competitors within the first hours of going live. Ideas are not important in China – execution is.

Ma Huateng

This copying strategy is not without failures. Consider these failed attempts despite huge marketing spend:

Ecommerce: Tencent Paipai (拍拍) was a C2C marketplace launched in 2005 to compete with Alibaba’s Taobao. It failed and was sold to JD.com in 2014.

Micro blogging: Weibo (微博) launched in 2010 and shut down in 2020.

Short videos: In 2013, Tencent launched Weishi (微视) App as an 8-second short video sharing community that was among the top five free apps. At that time, the short video was not as popular as it is today. Weishi had experienced a lukewarm development for several years, with no big sales performance. In 2017, Tencent terminated it.

Online group buying: Tencent’s Xiao’e Pinpin (小鹅拼拼) was a social e-commerce group-buying mini-program launched on WeChat in April 2020, designed to compete with platforms like Pinduoduo by offering discounted products when users formed purchasing groups. However, after a period of operation and upgrades, Tencent shut down the platform in February 2022.

WeChat (微信)

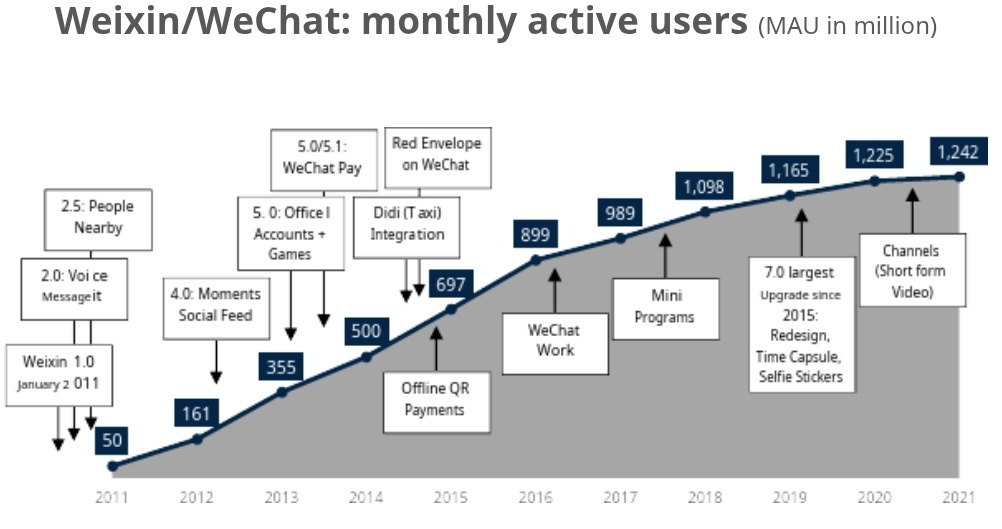

This is the greatest product Tencent owns, with 1.4 billion MAUs, it is ubiquitous in China.

But let’s dial back the clock…

The first generation of the iPhone was released in 2007, followed by the App Store and Google Play Store in 2008. Since 2009, we seen an explosion of apps developed specifically for use on smartphones.

Successful new messaging services for smartphones were introduced in many places, allowing free messages to be sent via the internet instead of SMS. In China, Kik Messenger was launched in 2010 and gained more than 1 million users within just two weeks.

Both Lei Jun (Xiaomi founder) and Zhang Xiaolong (Foxmail founder and QQMail since 2005) took note of this trend and started to race to develop their own program.

Although a QQ team is already working on a messaging app for smartphones, Zhang Xiaolong requested permission to develop his own solution with employees at the Guangzhou location in a long email. Pony Ma approved in a reply that consists of only four words: ⻢上就做 (Do it now!)

Zhang Xiaolong described the process in 2019:

When Kik came out, I realized there was an opportunity – this opportunity did not necessarily just stem from Kik as a product, but it came from me starting to use a smartphone, and from the lack of good communication tools in many PC products and messaging software. My thought was very simple at that time – I wanted to make a communication tool for myself and others to use.

Coincidentally, we had a team developing a mobile version of QQMail, so we assembled a team of ten to start work on WeChat. Including back-end developers, three mobile front-end developers, UI, myself, and a recent graduate on my team, ten people in total.

In two months, we created the first version. This past year has been WeChat’s eighth year, a meaningful milestone. At that time, we had one principle: if a new product can’t grow naturally, we shouldn’t market it ourselves.

See if users would be attracted to WeChat, if they would promote it themselves? If users weren’t willing to do this, whatever marketing we did would be meaningless.

I remember when WeChat version 2.0 was introduced, we saw user growth, not very rapid growth, but it was increasing naturally. At that moment, we knew we could start marketing it.

[…]

First, we didn’t import users and automatically add them as friends within WeChat, instead letting users choose who to invite or send a friend request.

Second, when the product wasn’t yet widely recognized, we let it grow naturally rather than market it. These two things were the right way to do it. Although it took more time, it meant that the product was healthy when it really started to grow.

Lei Jun actually beat Zhang Xiaolong by launching Mi Talk after only 4 weeks of development. Mi Talk was also first to offer voice messaging which was copied from TalkBox.

WeChat then copied the idea and introduced People Nearby dating function. As far as we know, this dating feature is proprietary and not copied. It was much later that China saw dating apps clones.

By end 2011, WeChat had 50 million MAUs. The next year, WeChat copied Facebook News Feeds and launched Moments. By mid-2012, it had exceeded 100 million MAUs.

To reach this milestone, these are how long some platforms took:

QQ 10 years

Twitter 5 years

Facebook, Snapchat 4 years

WeChat 433 days!

From this point on, the network effect is so strong that new competitors entering the market (eg. NetEase and China Telecom with Yixin, Alibaba with Laiwang) can no longer pose a threat to WeChat as the market leader.

Attention Economics

From the day Moments was released, users’ friends have increased more and more. Logically, content on Moments continues to increase as well. However, everyone fails to realize that even as users’ friends and content increased, everyone is still spending the same amount of time on moments: ~30 minutes.

When you have fewer friends, you read slowly and with more focus. When you have more friends, you browse faster.

Actually, users won’t divide their time based on the amount of content. If Tencent insisted on extending visit duration, they have many ways to do it. However, this would only frustrate users, because their social interaction efficiency would decrease.

WeChat never made user in-app time their objective. Instead, they are more concerned with when users communicate, post a picture, read an article, make a payment, or find a Mini Program, that they can do it as quickly and efficiently as possible – this is what makes the best tool.

Within WeChat Moments, they have been very slow in releasing ad space and in very limited quantities. To date, users see only a fraction of the ad load in their feeds of Western social networks like Instagram. Specifically, they have seen since:

2015: 1 ad daily

2018: 2 ads daily

2019: 3 ads daily

2020: 4 ads daily

Compared to Instagram, which loads 20 ads daily, WeChat can surely increase their inventory if growth is needed.

The options for advertisers expanded significantly in 2018, and Moments inventory can be marketed at industry-leading CPMs. Moments advertising can be directly linked to the advertiser’s Mini Program, and transactions can be completed seamlessly via WeChat Pay. The seamless integration from the first ad view in the Moments feed to checkout in the Mini Program enables high conversions.

Mini Programs

Mini Programs were introduced in 2017 and transformed WeChat into a super app where users can do almost everything without having to leave the app. Thus diminishing the importance of Apple/Android App Stores.

To enable Mini Programs to be launched directly in WeChat without pre-installation, developers must adhere to a maximum size of 10MB.

Now, 400 million people use Mini Programs everyday and since 2020 there are over 3 million Mini Programs compared to 2 million native apps in Apple’s App Store.

Mini Programs offer several advantages over native apps. Due to their size and feature limitations, they are easier to develop and more cost-effective. Roughly speaking, they cover about 80% of the capabilities of native apps at about 20-50% of the development costs. Mini Programs are allowed to access WeChat programming interfaces and don’t require separate registration, payment information, etc.

A good example is the Chinese bike sharing market, which has more people using Mini Programs to do bookings than their native apps.

Even Pinduoduo was able to state in the prospectus before its 2018 IPO no longer notice any glaring differences in the user experience between the native app and its own Mini Program:

Buyers may also access our platform and make purchases via our mini-program within WeChat directly. […] This embedded feature is currently provided to service providers for free, and the user interface of our mini-program is substantially identical to our own mobile app with the same product offerings by the same merchants.

Tencent monetizes the Mini Programs through online advertising (revenue share: 70:30 or 50:50 in favor of the developer, depending on the revenue generated). Mini Games are also already monetized, as in-game purchases on Android devices result in a 60:40 revenue share in favor of the developer. Due to iOS’s terms and conditions, in-game purchases cannot be made within Mini Games on Apple devices (they are redirected to an external browser).

Fintech

WeChat Pay is the payment service that is second to Alipay in China. It achieved its breakthrough in 2014, when the number of users jumped from 30 to 100 million within a month. The key to this leap is the Hongbao (Red Envelopes) feature, copied from Alipay.

Eveline Chao from Fast Company explains:

Say you have a chat group with five pals. You can put $5 in a red envelope and set it to distribute equally, so each friend gets $1. Alternatively, you could stipulate that the first 2 people to tap will get all the money in equal portions ($2.50 each) or that the first 2 people get a random cut, maybe $1 for one person and $4 for the other.

The result is that any time a red envelope appears, people scramble to tap on it as fast as possible. The packets expire in a day, adding to the time pressure. Only afterwards do they see how much money they’ve won, giving it an addictive element of surprise. So addictive, in fact, that third-party apps now exist that let users grab red envelopes without unlocking their phones.

In 2017, 46.6 billion red envelopes were sent via WeChat Pay compared to 0.2 billion in 2014!

Since then, WeChat Pay has steadily gained market share from Alipay, reaching a market share of 42% by payment volume compared to Alipay’s 54%.

This also caused Alibaba and Tencent to close off their platforms against each other.

Unprofitable WeChat Pay

In offline retail, WeChat Pay still regularly refrains from collecting the full Merchant fee of 0.6% and offers discounts and coupons to end customers. For this reason, the offline payment business is not profitable on its own.

WeChat Pay subsidizes this segment to enable cross-selling of investment products, consumer loans, and insurance.

This strategy is to cement the duopoly of the two market leaders and deter new entrants like Douyin Pay.

Tencent does not break down the revenue contributions of “Other FinTech Services” compared to the payment business. The “Other FinTech Services” for WeChat Pay include LiCaiTong (理财通) (investment platform with over US$100b AUM), WeSure (insurance platform with over 100 million registered customers, 40 million have active policies) and WeiLiDai (微粒贷) (lending platform with an average ticket size of US$1,000 and more than US$20b loan portfolio).

Insider Ownership

We think these are the most important people at Tencent:

1. CEO Pony Ma owns 8.4% stake.

2. Zhang Xiaolong joined Tencent through the acquisition of Foxmail and is the visionary behind WeChat. He directs from Guangzhou on all developments of WeChat. He has no stake in Tencent.

3. Martin Lau Chi Ping has 0.6% stake and is jointly responsible for the reallocation of available funds into the investment portfolio. Tencent has been accelerating its investment strategy, particularly since 2012. The investment portfolio now accounts for 1/3 of its market cap. David Wallerstein also leads from Silicon Valley. Tencent’s investment philosophy focuses on minority investments and requires a strong decentralized management culture.

4. James Mitchell is the Chief Strategy Office supporting Martin Lau. He has no significant stake.

Network Effects

This factor is obvious: The social network with the largest user base will then attract the most developers for its platform, as it can address the most customers. Companies entering the market later often cannot reach critical mass (eg. Alibaba with Laiwang or ByteDance with Duoshan) because they cannot offer a better user experience than the market leader.

WeChat ecosystem is strong such that new apps can be launched without downloading a separate app.

Tencent regularly remains cautious about introducing new applications on WeChat to avoid upsetting existing customers.

For example:

1. WeChat users have only been able to import their complete friends list from QQ after some time.

2. Ads load in Moments continues to be kept low.

3. Video channels are not intrusively suggested to users despite the threat of Douyin.

Everyone in our team has developed a habit of ensuring every feature and every service has a meaning or a dream behind it. If a feature is made for just gaining traffic, and it doesn’t provide value to users, then it’ll have problems, it won’t last. We think about the meaning behind every detail of everything we do. This is a reason we’ve been able to make it this day, and its helped us make many right decisions

Zhang Xiaolong, 2019

Investment Advantages

The Tencent management team has good insights on disruptive products. There’s 2 notable examples:

Tencent attempted to acquire Whatsapp, Pony Ma was supposed to meet with Jan Koum in California for final negotiations. However, he had to postpone the appointment due to surgery. Mark Zuckerberg used the resulting window of opportunity to outbid Tencent by a factor of two (purchase price: US$19b).

Tencent attempted to buy a significant stake in ByteDance, but failed because founder Zhang Yimin didn’t want to become a Tencent executive.

The more than 800 investments that Tencent has successfully completed since its founding have, in some cases, created significant value for shareholders. Three of its five largest holdings (Meituan, JD.com, and Pinduoduo) are heavily integrated with WeChat, and Tencent gained early proprietary insights into the potential of these targets through their Mini Programs and shared content on WeChat.

Since many startups would benefit dramatically from a strategic partnership with WeChat, there are investment advantages that Tencent possesses.

Below are the important investments (in USD), each of these companies are basically leaders in their own fields:

Meituan 18% stake, cost $43b. Market value $80b.

SEA Ltd 17.6% stake, cost $37b. Market value $110b.

PDD 14% stake, cost $20b. Market value $186b.

JD.com 18% stake, cost $22b. Market value $51b.

Kuaishou 16% stake, cost $17b. Market value $43b.

VIE Structure

When purchasing Tencent shares, foreign investors face greater risks than when purchasing shares from their home market. In China, foreign investors are prohibited from making direct investments in various industries. The ban includes telecommunications, the internet, e-commerce, education, and media.

Variable Interest Entity structure (VIE) aims to circumvent the restrictions. The VIE structure allows a foreign-based listed company control over companies operating in China (OpCo), without direct ownership in shares.

The VIE structure undoubtedly includes higher risks than traditional share purchase, since the latter represents actual and legally enforceable ownership rights.

Shareholders of a Chinese company like Tencent, on the other hand, technically do not own the operating company directly. But merely contracts in a legal grey area, located in a shell company in the Cayman Islands or British Virgin Islands.

The most serious risk from the VIE structure is personal risk. Chinese private individuals are legally the owners of the companies. In stressful situations, the owners can easily disadvantage foreign shareholders. In extreme cases, the shareholders of the listed company can even be completely expropriated.