Study: Taiwan Semiconductor Manufacturing Company (TSMC)

History

Pre-1987

Taiwan’s semiconductor efforts and investments began way before 1987, when TSMC was founded.

Taiwan, for the 3 decades before TSMC founding, had long reaped the benefits of industrialisation, growing its nominal GDP between 1960 and 1987, from $1.6b to $105b. Taiwan quickly became a powerhouse in the textile, footwear, steel and petrochemical industries during those years. It later identified the fast-growing high-tech industry as its next phase for manufacturing growth.

The Ministry of Economic Affairs, led by Sun Yun-suan (孫運璿), who would later become the Premier of Taiwan, founded Industrial Technology Research Institute (ITRI) in 1973.

ITRI served as the platform for Taiwan’s semiconductor efforts, and a couple years later, they partnered with Radio Corporation of America (RCA) for a technology transfer.

Under this agreement, Taiwan paid RCA $1m per year, and in return, RCA trained staff members from ITRI and shared semiconductor and integrated circuit manufacturing techniques.

The initial 19 engineers included the likes of Tsao Hsing-cheng (曹興誠, former UMC chairman), Tsai Ming-kai (蔡明介, former MediaTek chairman), and Tseng Fanchuan (曾繁川, former vice chairman of TSMC).

Six years later, in 1980, United Microelectronic Corporation (UMC) spun off from ITRI and created its semiconductor path. After that, the Taiwanese government doubled down on its investments in supporting the semiconductor industry. One of the key strategies employed was to encourage several Taiwanese engineers to return to the country, and one of them was Morris Chang.

1987: Morris Chang establishes TSMC

Morris Chang was born and raised in China but moved to Hong Kong during WW2 and later to the US to study at Harvard University and then MIT.

Morris had risen through the ranks at Texas Instruments (TI) over a 25-year career (ended 1983). While at TI, he noticed the manufacturing success of their Japanese factory: they were twice as productive. The Japanese technicians were more qualified and had lower turnover, Morris thought that the future of advanced manufacturing would be in Asia.

In 1985, after a meeting with Hsu Shien-Siu (徐賢修, president of ITRI), Morris agreed to relocate to Taiwan and lead ITRI.

At ITRI, Morris Chang viewed ITRI as too academically driven and wanted to reorient ITRI more towards manufacturing. However, due to cultural clashes, very little was achieved. Instead, he was occupied with fulfilling requests from integrated circuit companies to build semiconductor fabs. This led to him thinking that the best approach would be a pure-play foundry, entirely focused on making chips to other companies.

These early building blocks from the support of the Taiwanese government and transfer of foreign knowledge set the foundations of TSMC economic moat.

1987 – 2000: Beginning Boom

To build TSMC, Morris Chang needed partners. After some convincing, the government agreed to invest 48% of the required capital to launch TSMC, and Morris needed to find additional partners from both the semiconductor industry and the local private investor network.

He reached out to many international companies, including his old employer, Texas Instruments, but the only company interested in investing was a mid-tier semiconductor manufacturer in Netherlands. This firm was Philips, which was looking for a way to enter into Asia’s market.

In fact, today Philips had restructured its business operations, and its semiconductor division evolved into NXP Semiconductor. It’s focused on automotive, industrial, and communication infrastructure. NXP continues to have a joint venture with TSMC in their Singaporean-based fab and the upcoming German fab.

Private investors like Wang Yung-ching of Formosa Plastics Corporation committed capital of $35m.

With the capital funding, TSMC started operations. Morris Chang still held his role at ITRI and hired Jim Dykes as the initial CEO of TSMC, only to fire him a year later.

Signing American and European clients initially proved difficult, so TSMC initially catered towards Taiwanese semiconductor companies.

Its first fab (Fab 1) was a converted research lab leased from ITRI in Hsinchu Science Park. Following the success of customised 3.0-micron node technology for Philips, more international semiconductor companies partnered with TSMC, notably Intel.

This Fab 1 was eventually returned to the government, and since then TSMC has opened many fabs. Amazingly, they have never closed a fab before. When the tech became old, the fabs were repurposed to produce specialized chips.

In 1994, it went public on the Taiwanese Stock Exchange, revenues had reached TW$19.3b (US$735m), with EBIT margins of 45%. TSMC had also reached 137 customers, including big companies such as Fujitsu, NEC, and Siemens. Meanwhile, sales were growing twice as fast as the broader semiconductor market while recording wafer shipments of 643,000 6-inch equivalent wafers.

For the second half of the 1990s, TSMC set its ambitions to build a second fab in 1995 (Fabs 2A/2B) and later Fabs 3/4/5 by 1997.

From 1994 to 2000, revenues and operating profits grew impressively at 43% and 38% CAGR respectively.

By 1999, while Philips was still a key customer, representing 3.7% of TSMC’s revenue, other customers such as Nvidia (6%) and Altera (6%) were larger. TSMC has outgrown its Dutch partner.

2000: Dot-com bubble

Semiconductors are like gasoline. Prices go up and down, but people are always going to buy them.

Donald Brooks, TSMC President, 1994

TSMC enjoyed the boom cycle brought by the internet and telecommunications. TSMC made it through the dot-com crash relatively unscathed.

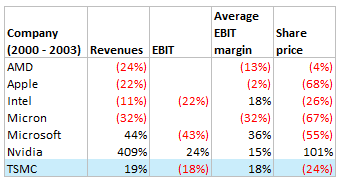

From 2000 to 2003, revenues growth was slow but positive, and EBIT fell by -18%. Its share price fell by -24%. Fabs utilisation decreased from 106% in 2000 to 51% in 2001. TSMC capital expenditures declined by -64% between 2000 and 2003.

Although the other companies above are very different from what they are today, TSMC itself hasn’t changed much since then. It still makes chips on a contracted basis but has a much larger market share and a greater focus on leading-edge chips.

It is quite amazing that during the worst tech crash, there was still revenue growth and profitability.

2005 – 2009: GFC

In 2005, Morris Chang retired and passed the reins to Rick Tsai (蔡力行) who has been with TSMC for 15 years.

Four years later, on 11 June 2009, TSMC announced that Morris would return as CEO, effective the following day, and Rick would become president of the New Business Development Organization.

Instead of cutting back on investments during the GFC, Morris saw great opportunities to take market share when the economy recovered. Despite the economic downturn, TSMC revenue increased by 3.3% in 2008, reaching NT$333b.

2010 – present: Mission Critical

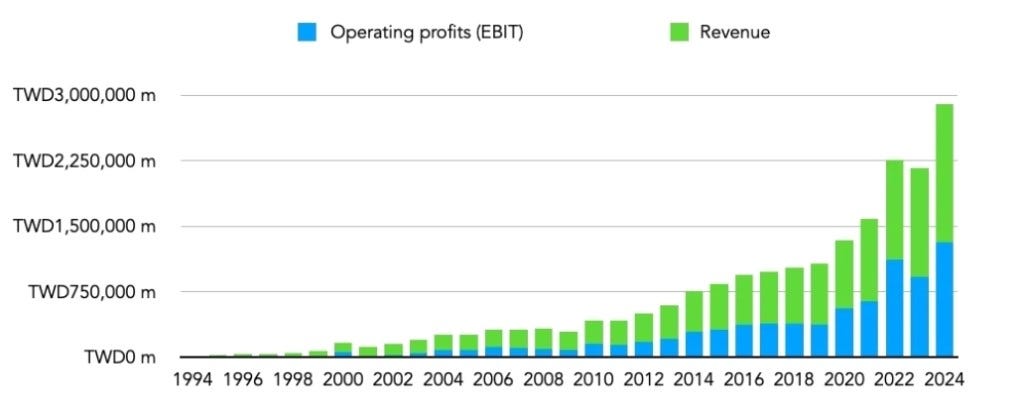

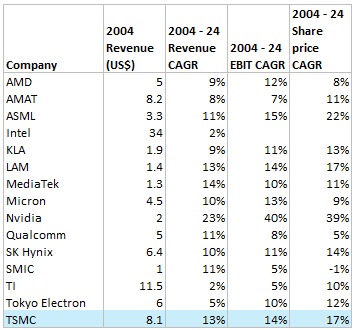

By 2004, TSMC had already become the fifth-largest listed semiconductor company by revenue and the second-largest by operating profits.

Take a look at its performance for the last 20 years among these companies:

Another amazing fact is that TSMC grew EBIT at 14% CAGR and operates in a notoriously cyclical semiconductor industry but has not incurred a single year of loss.

TSMC 37-year history has been organic-growth driven, without any major acquisitions of other foundries or fabless companies. Today, it is entirely focused on leading the chip world in productivity and innovation.

Beyond chips, TSMC once ventured into and invested in solar cells but ceased operations in 2015 due to concerns over capital allocation.

In June 2018, Morris had his second retirement and left TSMC in the hands of

Che-Chia Wei (魏哲家), who is the CEO, President and Chairman of TSMC today.

Taiwan Government Support

Taiwan spending on R&D as % of GDP ranks second at 3.6%, behind South Korea at 4.9%. Taiwan’s public-private collaboration in R&D (eg. ITRI, Academia Sinica, National Applied Research Laboratories) is very beneficial to companies like TSMC.

Since founding the ITRI, Taiwan has implemented several initiatives to support R&D and industry across electronics, manufacturing, biotechnology, and semiconductors and has seen many of these projects convert into actual companies.

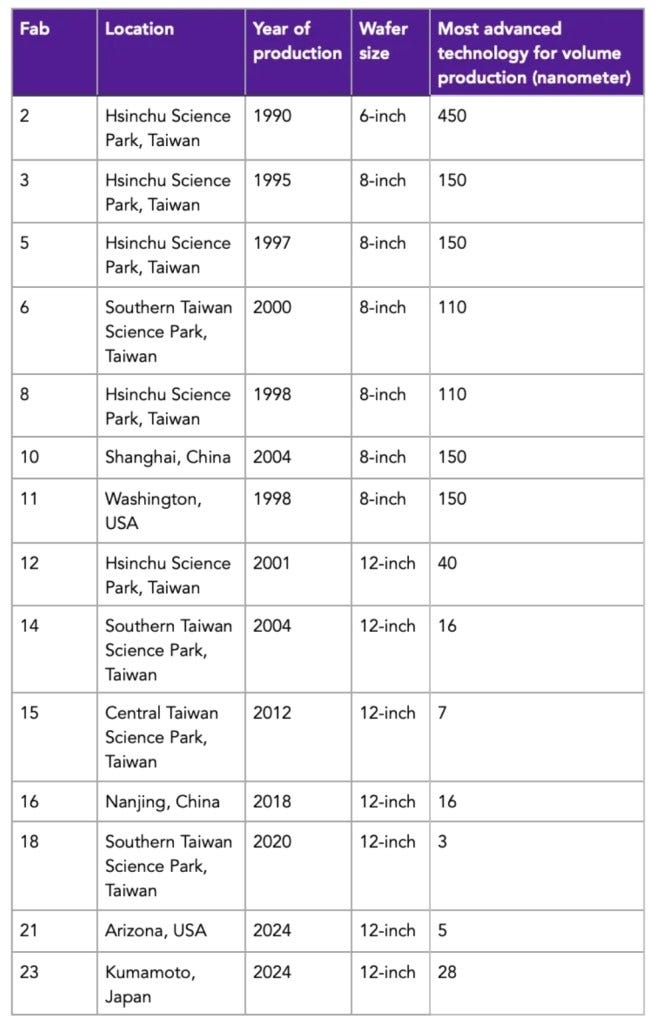

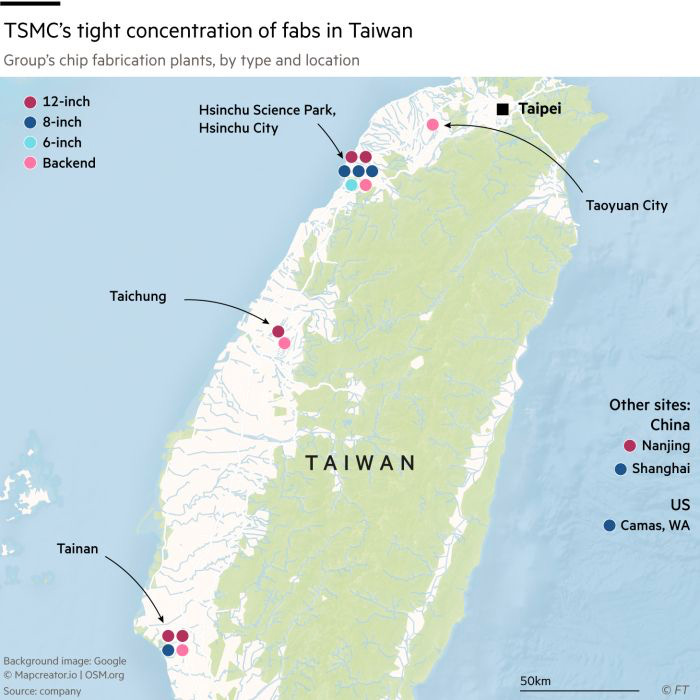

Taiwan has invested in several science parks, which helps TSMC capacity utilisation and ease of access to resources across its supply chain. The main science park, Hsinchu Science Park (1980), hosts 5 of TSMC current 14 fabs, while the Central Taiwan and Southern Taiwan Science parks host 4 other TSMC fabs.

Since the 1970s, Taiwan has implemented various strategies to support STEM (Science, Tech, Engineering, Math) education. Initially, the government sent students to the US via scholarships. Over time, they transitioned to investing in local engineering and science departments.

TSMC local access to talent is a limiting factor in its current push to create more global fabs beyond Taiwan, which highlights the importance of these supporting factors.

These factors have contributed to TSMC economics and moat, making it difficult for new players to establish competitive fabs. Not only would they be competing with TSMC expertise, but also 60 years of Taiwan’s investments.

Semicon Market

Barriers to entry

In the semicon industry, the winners of the past tend to remain winners in the future, with limited room for new players. Due to the technical capacity, R&D budgets, oligopolistic sub-market structures, and business model complexity, the barriers to entry are very high.

Growth potential

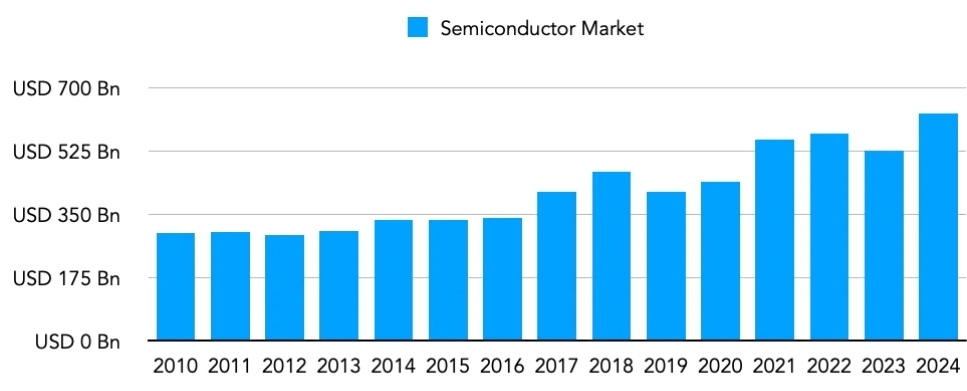

The semicon market has grown overall by 5.5% CAGR over the past 14 years, reaching $628b in 2024, with its growth rate accelerating in more recent years.

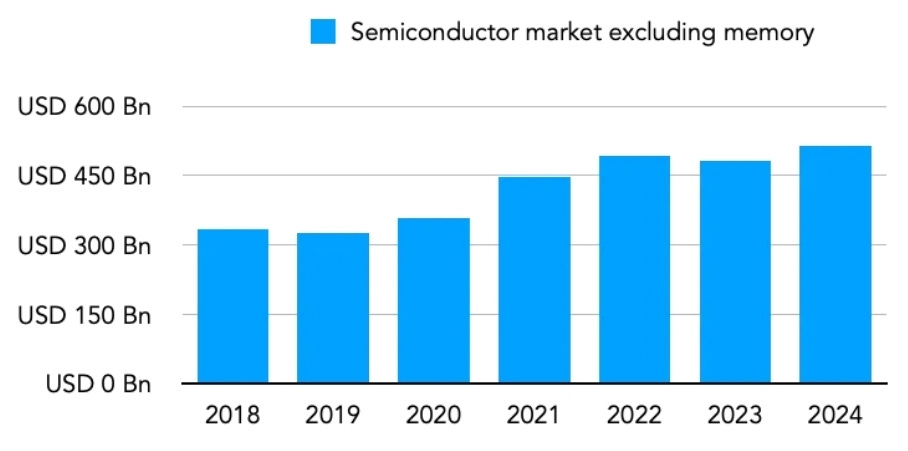

For TSMC, the more relevant market is the non-memory and foundry markets. The growth rate in the ex-memory chips market was slightly faster between 2018 and 2024:

Unlike memory, the logic chip segment has more room for product differentiation and innovation, which allows leading-edge chips (<7nm nodes) to be materially more expensive than older chips.

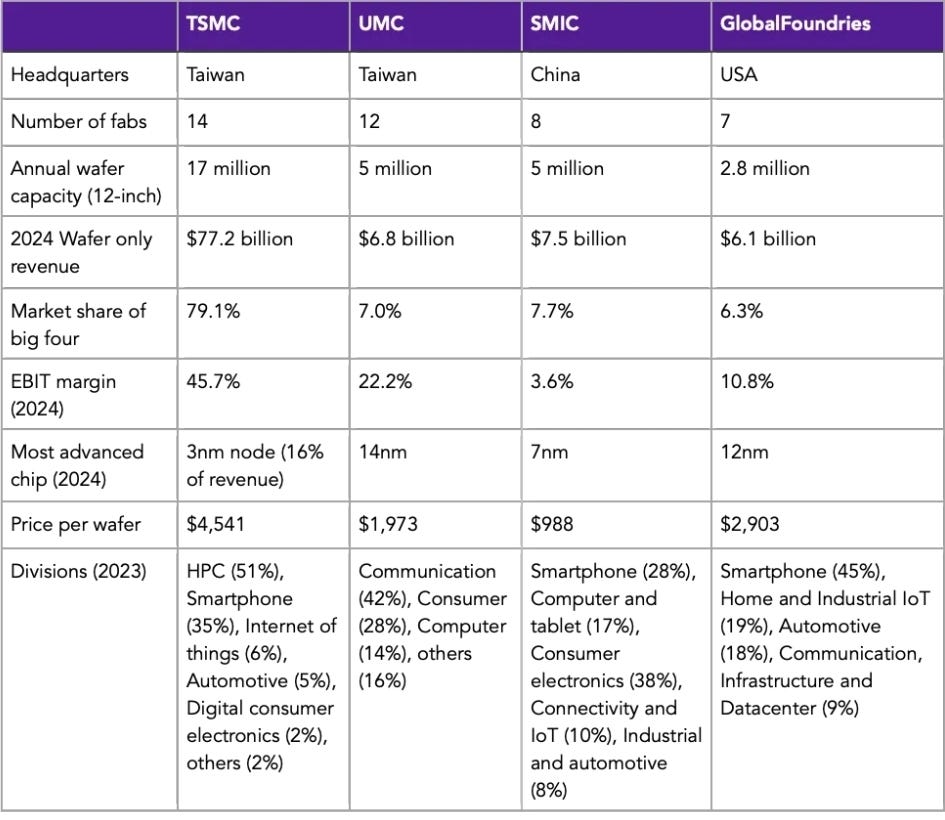

The Big Four

We compare the big four pure-play foundries:

One immediate observation is the super high EBIT margin against non-Taiwanese companies. We think this is due to governmental support.

TSMC also has very high market share and produces the most advanced chips. These advanced chips fetch a high price per wafer, which highlights how critical and beneficial it is to be innovative at mass production.

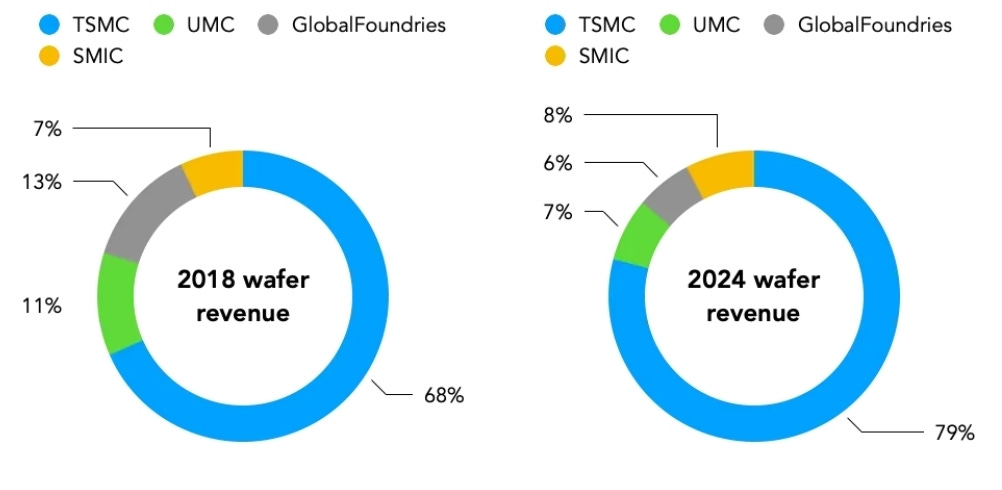

Look at how competitors ceded revenue share in just 6 years:

Intel and Samsung

In the 2024 annual report, TSMC expanded the definition of its addressable market to “Foundry 2.0”, which increased its market share from $150b to $250b. Foundry 2.0 encompasses areas of the chipmaking process, including advanced packaging and integrated device manufacturing.

Big players such as Samsung and Intel play in these fields.

Samsung is the most vertically integrated player, being the largest memory chip manufacturer globally. It is estimated to be the second-largest player globally in the leading-edge market, with 15% market share, compared to TSMC 60%.

Intel is also vertically integrated and has been a dominant player in the PC market. The key question has been whether the benefits of being vertically integrated outweigh TSMC pure-play strategy?

We think TSMC approach is more favourable.

Firstly, the world is no longer dominated by PC computing, and smartphones are not going to disappear. In this case, Intel’s position will be eroded. TSMC benefits from Apple’s demand for chips. It also produces Qualcomm Snapdragon chips used in Android phones.

Samsung produces chips for most Android devices, and this is the strongest competitor today. The dynamics can be significant as 35% of TSMC revenues come from smartphone chips.

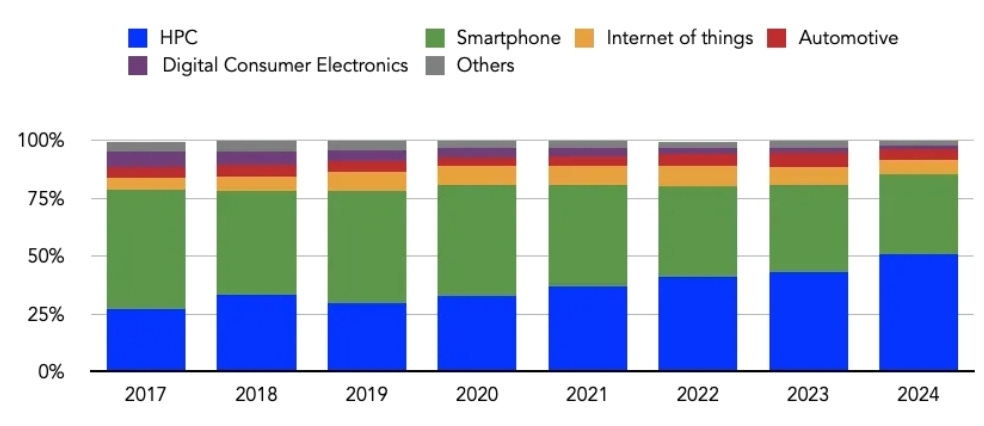

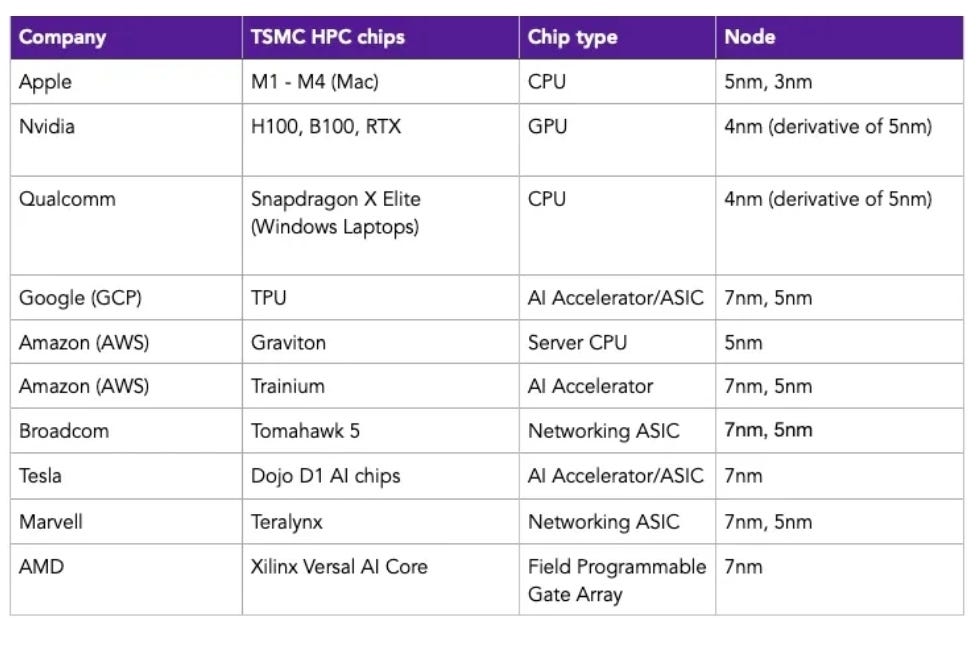

Secondly, there is a rising trend of ASICs (Application-Specific Integrated Circuits). The key growth market in recent years for TSMC is its High Performance Computing (HPC) segment.

HPC had 29.5% share of total revenue in 2019 and is now 51% share, translating to a 5-year CAGR 36%, while the other segments only 13.5%.

In the world of AI, efficiency, performance and scalability have become increasingly important. Hyperscalers like Google (TPU), Tesla (Dojo) and Microsoft (Azure Maia), create their own custom chips but designate TSMC to fabricate. They choose TSMC because it has the best and latest tech, and this is a result of their pure-play strategy.

Lastly, the role of GPUs in AI and the datacenter market was missed by Intel. As a result, Nvidia and TSMC have established very close partnerships. Over the past 20 years, Nvidia has been a key customer of TSMC. This goes way back to 2003, when Nvidia was TSMC’s largest customer (15% of sales).

The success or failure of Nvidia in the AI space will have an outsized impact to TSMC.

Overall, we can see that the tech space is no longer as monopolistic compared to the 1990s. In today’s environment, with different players presenting multiple opportunities, being a focused specialist offers a better value proposition than in the past.

Customers

We can put customers into 4 groups:

Group 1: Direct (Apple, Qualcomm, Broadcom, MediaTek)

These customers contribute the largest revenues and tend to use leading-edge tech.

Group 2: Fabless (Nvidia, AMD, Marvell, Analog Devices)

The nature of their end markets has shifted from gaming consoles and PCs towards cloud computing and AI applications in recent years. They also use leading-edge tech.

Group 3: Specialized (Google, Tesla, AWS)

Since Google’s custom-made chips launched in 2015 with TSMC’s 28nm node, Big Tech has become a growing customer base for TSMC. These are typically used in AI applications.

Group 4: Integrated Device Manufacturers (IDM) (Intel, Sony, Renesas, Infineon)

By nature, these companies have their own foundries and typically outsource some capacity to TSMC, usually in their lagging-edge chips (28nm and older).

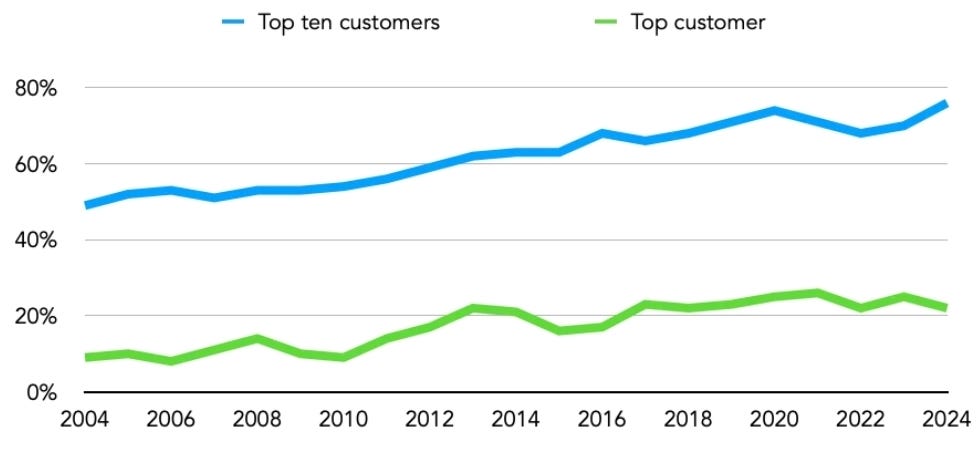

Overall, TSMC had 522 customers at the end of 2024, but the top 10 customers represent 76% of revenues:

Apple relationship

Apple is the largest customer to TSMC and their partnership is strategic. In 2014, Apple began shifting some production (A8 chips) for the iPhone 6 to TSMC, using its 20nm nodes.

The following year, Apple faced a problem that the iPhones made by TSMC was known to have better battery performance than Samsung. After that, Apple adopted a TSMC-only chip model starting in 2016 with the A10 Fusion chips.

With Apple’s guaranteed purchases, TSMC could reinvest into new technological nodes at a much quicker pace than before.

Nvidia relationship

The relationship dates back to the 1990s when Nvidia was still in its early days. TSMC was an influential foundry partner when it introduced the world’s first GPU (GeForce 256) in 1999. By 2001, Nvidia already accounted for 17% of TSMC revenue.

Despite attempts to collaborate with Intel and Samsung, Nvidia sees no alternative that can match TSMC’s technology and capabilities.

Suppliers

To make chips, TSMC needs help from equipment and service suppliers.

Facility and infrastructure

The physical buildings, cleanrooms, and utility systems can account for anywhere from 10% to 20% of a fab’s construction budget.

By nature, these are also the most localised, but it’s common for TSMC to use their Taiwanese partners in international fabs.

For example, the Taiwanese-listed United Integrated Services, a longtime partner, announced contracts from TSMC Arizona fabs with over $2.5b in cleanroom-related contracts in 2025.

Materials

Materials can be categorised into facility-wide and wafer-specific categories. The most important are the wafers (GlobalWafers, Shin-Etsu, SUMCO), the Extreme Ultraviolet (EUV) photoresists (Fujifilm, Ohka Kogyo, JSR Corp) and deposition gases (Air Liquids, Linde, Merck).

Photolithography

The company ASML is the only supplier of EUV machines in the world. TSMC began using EUV in mass production in 2019 with its 7nm+ nodes, and with the 5nm in 2020, EUV application significantly expanded.

The EUV technology was years in the making. Intel, TSMC, and Samsung each invested in ASML in 2012 to support R&D efforts. While Intel invested the most, TSMC ultimately became the largest beneficiary. Today, TSMC contributes about 17% of ASML sales.

Clearly, the web of customer and supplier relationships is wide and deep. TSMC has consistently proven to be able to manage so many different companies efficiently at scale.

These relationships are very difficult to replace because there are actually no better alternative partners. The winner in this industry (TSMC) will very likely continue to lead as they will receive the best contracts and will have resources to reinvest back into the business.

Wafer Revenues

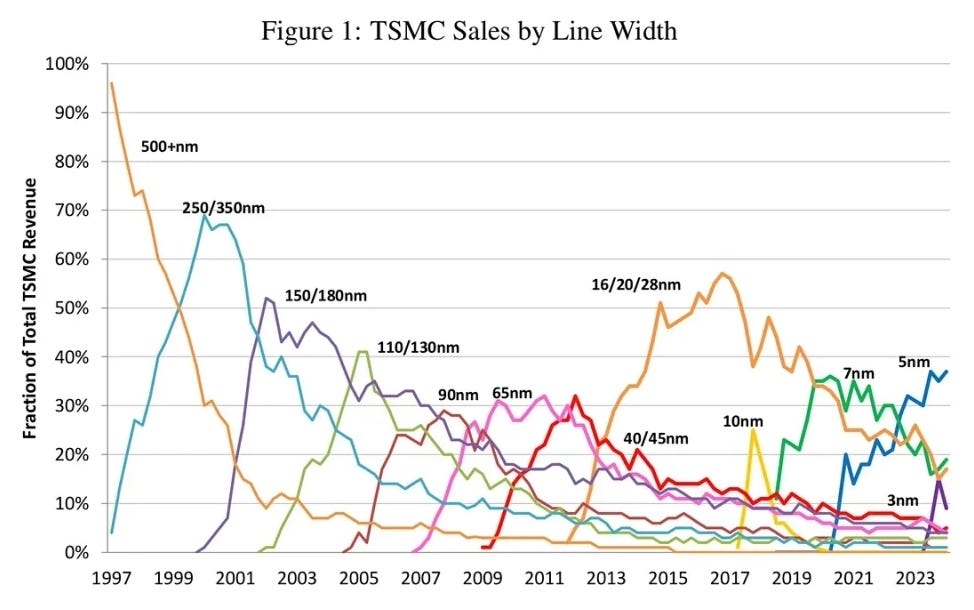

The most important goal for a foundry is to mass-produce the most technologically advanced chips within its capacity, with high utilisation and limited defects, consistently for customers. The semiconductor industry classifies these technologies by nodes.

TSMC method of raising prices involves driving industry innovation and setting higher starting prices for its most leading-edge chips.

Over the past two decades, the prices of their latest chips have increased by 12% annually, with TSMC citing improved performance and reduced energy consumption as justifications.

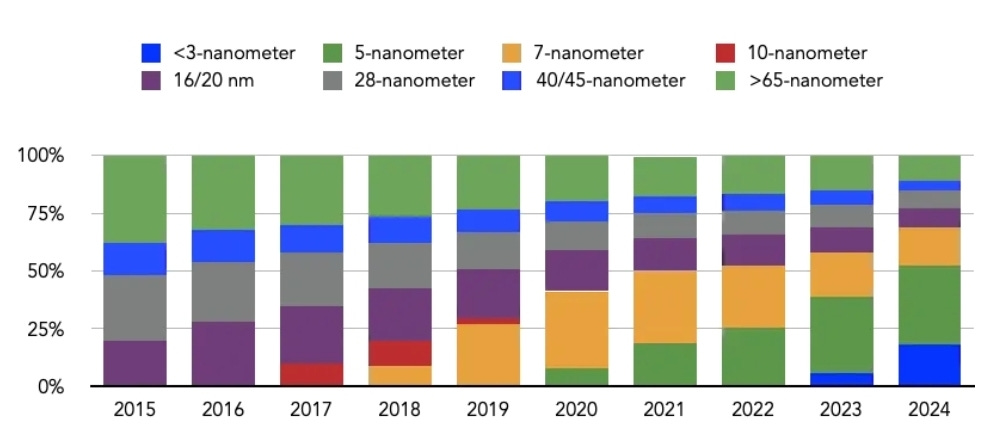

Another significant trend is that over the years, sales from the newest chips have grown as a share of revenue at a faster pace:

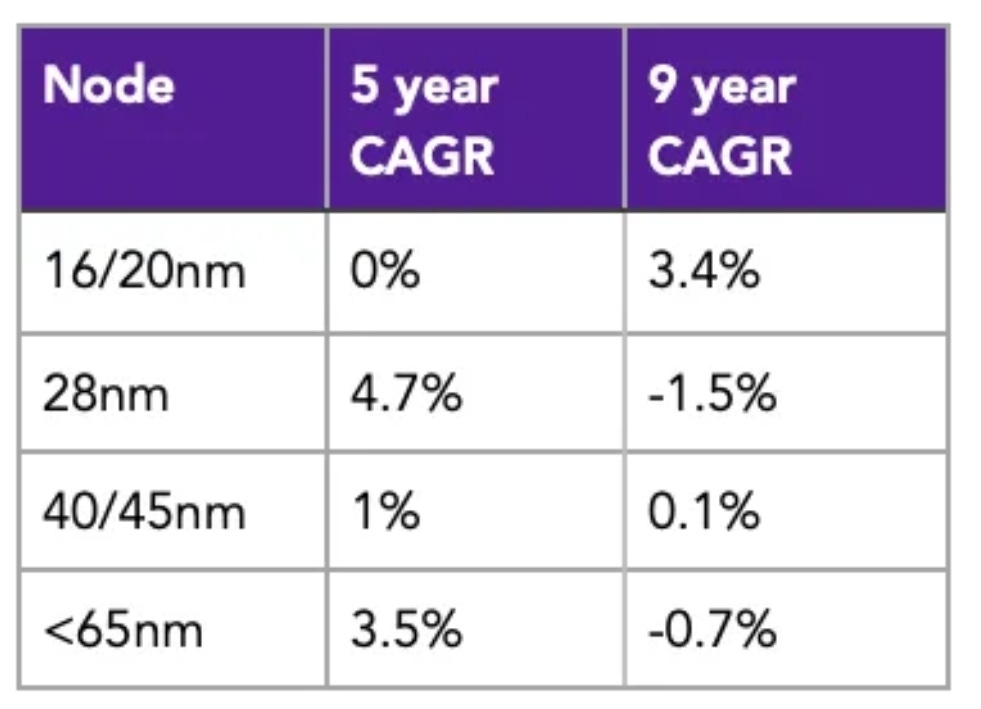

On the other hand, sales of older nodes don’t grow:

At the other end of the node spectrum, 7nm and below chips have been growing fast. In its first full production year, 3nm chips made more revenue than all chips above 40nm in 2024.

Overall, in the past 9 years, wafer revenues have grown from TW$766b to TW$2,514b (14.1% CAGR), which is well ahead of the global foundry market growth of 6% CAGR.

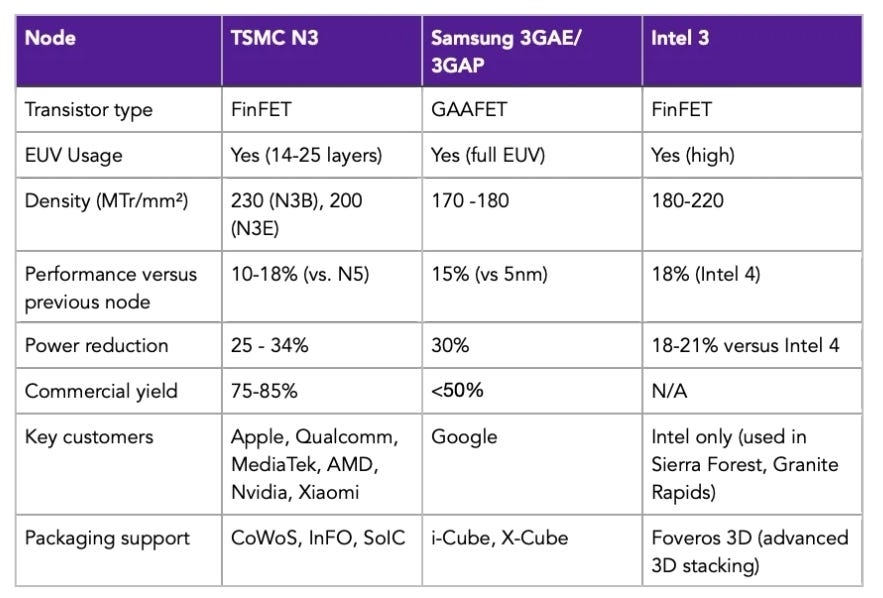

3nm (N3) node

While the 2nm chips will be in mass production by late 2025, the 3nm is the most advanced node for TSMC today.

As of end 2024, the 3nm (or N3 family), accounted for 18.3% of its revenue and is likely to account for at least 25% of its FY2025 revenue. The 3nm chips were in direct competition with Samsung’s 3GAE/3GAP chips and Intel 3 chips; these 3 companies are the only ones that can make 3nm.

Apple was the first to integrate the 3nm chip in Q3 2023. TSMC typically builds different chip variations within each family;

N3B (baseline)

N3E (enhanced)

N3P (performance)

N3X (extreme)

N3A (automotives)

Each of these has its own ideal application. For example, N3X is optimised for datacenters. N3B was for the Apple A17 chips used in iPhone 15.

Below is a comparison of competitors 3nm:

Although Samsung was first to commercialize 3nm, it actually suffered from poor yields. Looking at TSMC yields, it is fair to say that it has superior manufacturing capabilities.

HPC & Smartphones

No surprises here; high performance computing (HPC) and smartphones make up most of the revenues.

HPC uses leading-edge nodes and covers a broad range of customers, including datacenters, personal computers, cloud infrastructure and AI related:

Non-wafer Revenues

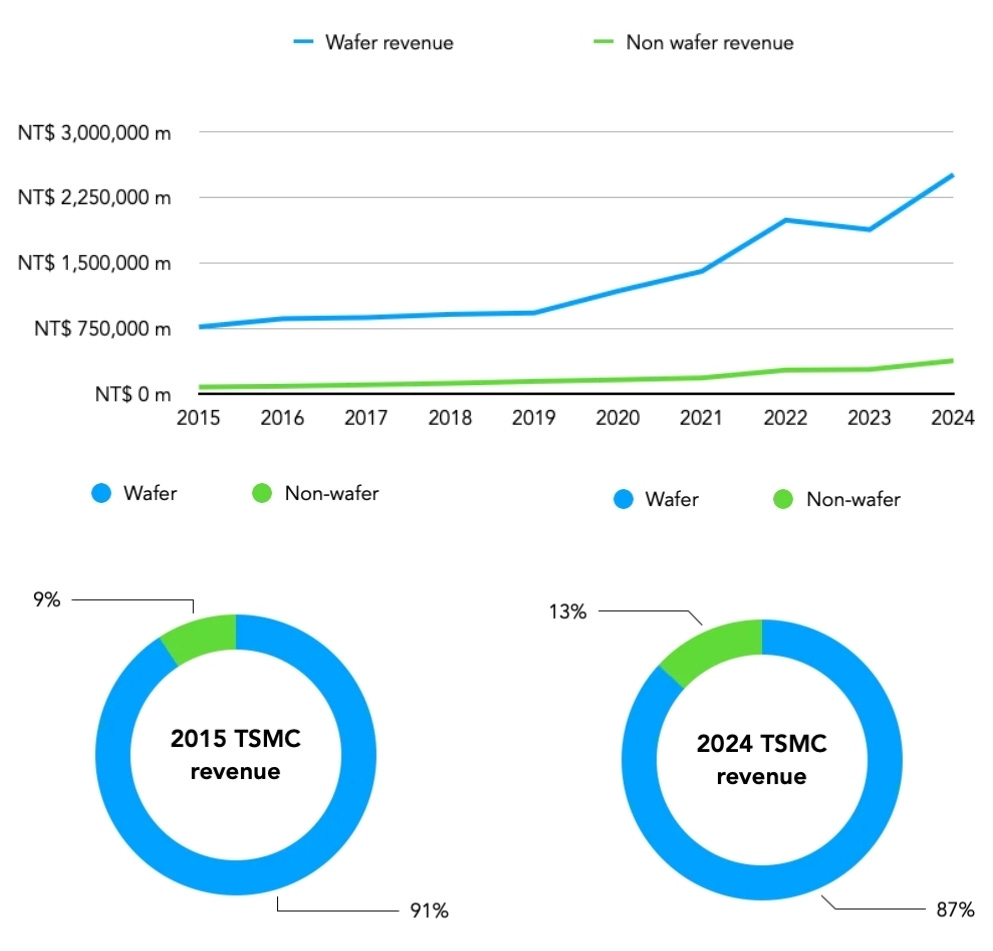

Until 2023, TSMC had described its addressable market in terms of wafer sales. However, the non-wafer side (eg. chip packaging) is actually growing faster.

Today, this non-wafer revenue segment (note 22 pg.F-54, 20F filing) represents 13% of revenues, up from 9% in 2015. The growth is 19% CAGR over the past 9 years versus 14% for wafer revenue.

There’s no details on what’s under non-wafer, but advanced chips packaging is probably the largest component.

TSMC has developed its IP on technologies to increase chips performance:

Integrated Fan-Out (InFO) 2D Packaging

CoWoS 2.5D Packaging

SoIC 3D Packaging

As a generalist, we don’t know what all these mean technically, but management expects this segment to be fast-growing, with customers such as Apple utilising SoIC, Nvidia utilising CoWoS for its Blackwell chip and AMD utilising InFO.

Among these, CoWoS is likely to have the largest revenue share, and people expect it to have the most meaningful impact.

Jun He (VP operations advanced packaging technology and services), revealed at the Semiconductor Exhibition that CoWoS advanced packaging production capacity is expected to have a compound annual growth rate of more than 50% from 2022 to 2026, and will continue to expand production by 2026.

AI has made CoWoS very popular. In contrast, more than 10 years ago, when the technology was first developed, it was quite deserted. CoWoS had no customers at the time, and only Xilinx was willing to adopt it, but only 50 pieces were needed per month, which was a pitifully small amount. This is a world of difference from the current production capacity demand that is in short supply.

Morris Chang adopted the suggestion of R&D executive Chiang Shangyi to enter the advanced packaging field. He generously gave him 400 engineers and $100m in R&D resources. But the CoWoS technology he developed had no business.

Jiang Shangyi promoted the CoWoS technology to customers everywhere, but no one wanted to use it. Later, he had a meal with one customer, and he casually mentioned that the reason for not adopting CoWoS was the expensive price. If 1 square millimeter was sold at 7 cents, it was too expensive. He would only be willing to use it if it was sold at 1 cent.

Jiang Shangyi immediately asked the R&D director to develop technology to reduce costs, which led to another advanced packaging InFO technology.

Cost structure

COGS

COGS is the largest component (80% of total cost) but TSMC doesn’t disclose much except for depreciation (49% of COGS) and employee benefits (13% of COGS).

Manufacturing raw materials (wafers, chemicals, photoresists, gases, polishing & contact pads) should be a large component and TSMC won’t have pricing power over these given the commoditized nature.

TSMC will have economies of scale as they can buy in large quantities.

Depreciation

Depreciation accounts for 42% of total costs, reflecting its asset-intensive business model. The key is that the old nodes are fully depreciated. TSMC depreciates equipment over 5 years. So 7nm, which launched in 2017, is the cutoff. Everything newer (3nm & 5nm) still carries depreciation load.

Any misalignment between capital investment and customer demand, whether due to market cycles, overestimation of customer uptake, or delays in node transitions, poses a significant risk. Since depreciation is a fixed cost, once assets are deployed, underutilisation of capacity directly compresses margins. This makes accurate CAPEX planning and demand forecasting important.

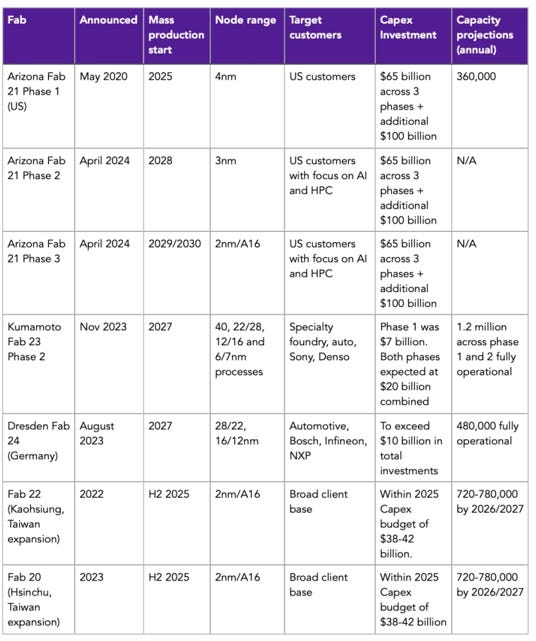

TSMC reported sharp increase in CAPEX from 2021 onwards due to growing annual capacity for Fabs 18 and 21 and its trailing-edge Fab 23 (Kumamoto, Japan) and Fab 24 (Dresden, Germany). In Taiwan, Fab 22 is dedicated for 2nm. In the US, Arizona Fab 21 is expected to make 30% of advanced chips upon completion in 2028.

Upcoming Fabs

Below are the upcoming fabs expected to start mass production soon:

Unit Economics

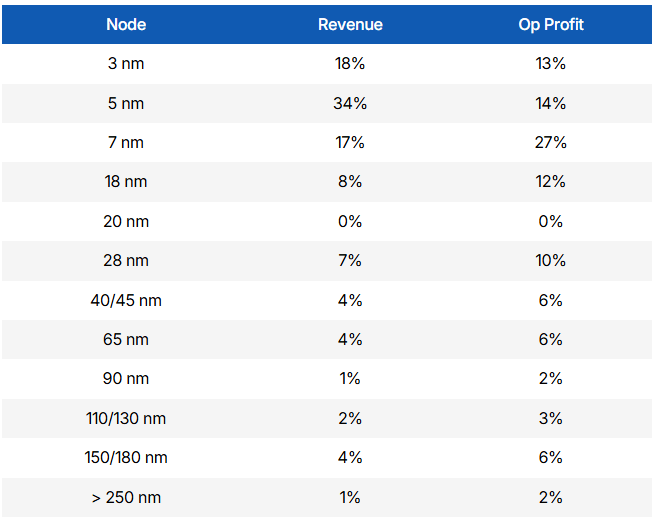

Its difficult to estimate the margins by node since we’re not experts, but online sources do provide some info. Interested readers may consider in their valuation models…

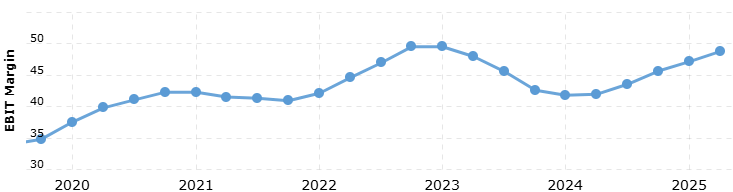

Advanced nodes generate 52% of revenue but only 27% of operating profit, but do note that 3nm are still in early stages and will become more profitable over time. In 2023, both 3nm and 5nm are actually loss-making but the next year they have become profitable. We can see evidence of this from the EBIT margin:

Peak margins was 49.5% in 2023 likely due to 5nm maturity, which was first launched in 2020 and now is the largest revenue contributor.

Management

Across all 29 executive officers, the average tenure is 24 years, that’s a long time considering TSMC was founded only 38 years ago. This means the average executive has been here for nearly 2/3 of TSMC history.

CEO C.C. Wei, joined in 1998 as the VP of the R&D division, before becoming a co-CEO in 2013.

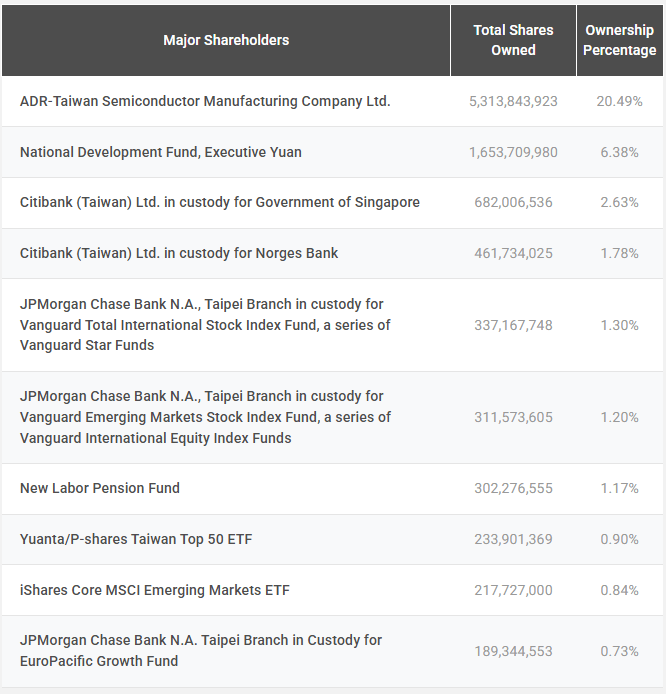

However, like many state-owned enterprises, the insiders own only 0.27% of outstanding shares. This is the list of major shareholders:

Geopolitical Risk

Given its role in society, market share and interconnectivity with global supply chains, it’s no surprise that TSMC has embedded geopolitical risks. However, an additional factor worsens TSMC’s position: its location in Taiwan, which is in high tension with China.

Unlike pure commodities, the foundry market’s barrier to entry isn’t dependent on the availability of natural resources, but rather on human capital, strategy, and long-term thinking. These three factors are areas in which Taiwan excels.

As a result, the Taiwanese semiconductor industry has established the lowest-cost, most efficient, and integrated foundry supply chain. This means that any country or company seeking to compete will need to out-invest Taiwan to be competitive, a process that can take decades. While not impossible, this is highly challenging, and it’s more profitable for governments to encourage (or pressure) foundries like TSMC to invest more in their local markets.

For TSMC, this approach hurts gross margins, as manufacturing chips internationally cannot be as cost-effective as manufacturing in Taiwan.

At the moment, international markets (mainly the US) dictate TSMC’s decision-making to some extent. One of the more difficult challenges for TSMC has been accessing the Chinese market.

In 2018, TSMC opened Fab 16 in Nanjing, China, with a planned capacity of 240,000 300mm wafers per year, focusing on more trailing-edge chips (22/16nm). However, its progress here has been capped. TSMC isn’t allowed to manufacture newer technology node chips without US export licenses, and is banned from manufacturing chips for American-prohibited companies, such as Huawei and HiSilicon. At the time of the ban in 2020, both companies were among TSMC’s major customers.