Study: Spotify

History

Daniel Ek was born in 1983 in Stockholm, Sweden. From an early age, he showed both talent and passion for entrepreneurship. As a young 13 year old boy, he started building websites for small companies from his bedroom, charging $100 per site but quickly increased prices to $5,000 as demand grew.

By the age of 14, Daniel had learned C++ and HTML CGI programming languages, making money from software development. In fact, even in middle school, he used video games, iPods, and cell phones as bribes and incentives to get his classmates to do his schoolwork and code for his early web-design business.

By the age of 15, he was earning $50,000 a month creating websites. Later, his businesses grew to the point where he could employ 30 people!

When Daniel applied for a job at Google at the age of 16, he was rejected because he had not finished university. It’s funny that around this period, Daniel was already a taxpayer before graduating from university.

Thinking that money could buy happiness, Daniel retired very young at just 23 years old, after selling his online advertising startup Advertigo in 2006 for $1.25m. After becoming a millionaire, he decided to quit and enjoy his wealth. So he bought himself a Ferrari and hung out in Stockholm nightclubs where he got his friends expensive tables and wooed attractive women with fancy champagne.

However, after a year of this lavish lifestyle, Daniel had a realization… the women he spent time with were not very nice, and his friends were only using him for his money.

They were people who were there for the good times, but if it ever turned ugly they’d leave me in a heartbeat. I had always wanted to belong and I had been thinking that this was going to get solved when I had money, and instead I had no idea how I wanted to live my life.

Daniel Ek, 2014

Afterall, money cannot buy true happiness.

So he decided to move to a cabin near a suburb called Ragsved where his parents lived. It was in this place that he talked to Martin Lorentzon about creating a product that would allow people to have seamless access to all of the world’s music.

Both men came together and founded Spotify in the same year 2006.

Piracy was rampant in the early 2000s from websites like Napster and LimeWire. For those who lived their teenage years during this period would be familiar with the memories of illegal music sharing on a dial-up modem.

In fact, The Pirate Bay emerged in Sweden. Daniel Ek and Martin Lorentzon envisioned a platform that could offer instant access to any song, anywhere, without the need for downloading. The development of Spotify was driven by a commitment to legality, fairness to artists, and user experience. Just after inception, the founders negotiated with record labels and artists to ensure a vast catalog of music while developing a platform that was intuitive and user-friendly. Spotify officially launched to the public in October 2008 after roughly two years in the development phase, initially through an invite-only system in Europe.

Spotify quickly gained popularity, largely due to its superior user experience and freemium model: a free, ad-supported service alongside a premium subscription option. Their user base grew quickly, just 8 years after initial launch they reached 100 million users worldwide. Spotify entered the US market in 2011 and continued to grow its global footprint.

Today, Spotify is available in 184 countries with 751 million monthly active users (290 million paid users). Daniel Ek still receives zero salary, no long-term incentives, no stock options. Both founders are still the largest shareholders of Spotify with controlling stakes: Daniel owns 13.9%, Martin 9.2%.

Industry Background

We have to go back to 1979 when Sony launched the Walkman. It was a portable cassette player that allowed people to listen to music at any place and time. Before this, music was mostly confined inside homes or cars.

This sparked off the creation of audio CD (1980s) and the MP3 player (1990s). Then the smartphone era came and Apple invented the iPod. It was only until 2015, when music streaming finally scaled up. Like many other forms of entertainment, music has also gone through a few decades of transformation.

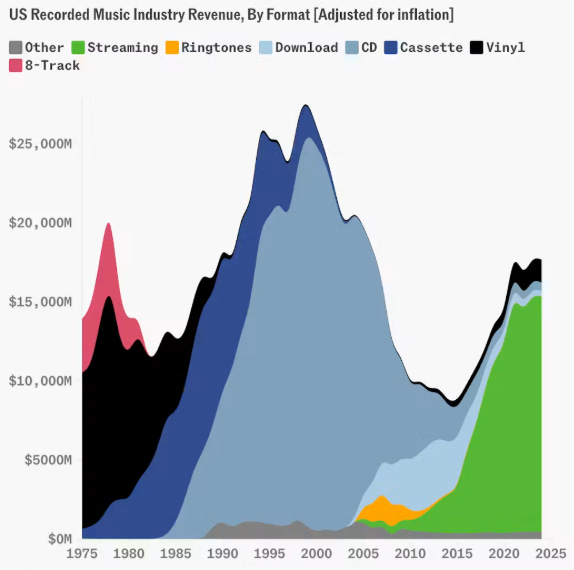

Following the rise of the internet, the music industry value chain has changed drastically. We started off with physical mediums, then downloading and piracy became rampant, in fact the whole music industry saw declining revenues until streaming took off in 2015.

![r/dataisbeautiful - [OC] Global recorded music industry revenues by format - 1999 to 2025](https://substackcdn.com/image/fetch/$s_!O1cE!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fd53e019a-3172-4c75-89c6-5723c4ccabee_11144x7790.png "r/dataisbeautiful - [OC] Global recorded music industry revenues by format - 1999 to 2025")

Although we have nominal higher revenues, when adjusted for inflation it actually shows an industry with no real growth (in the US):

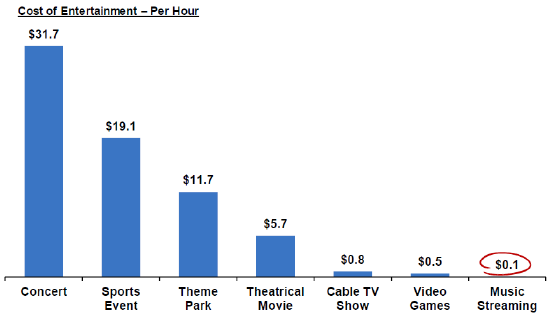

However, we need to focus on streaming because growth there is very real and durable. It’s estimated that people spend 4 hours per day listening to audio entertainment, the cost per hour of music entertainment is the lowest among different choices (Spotify has different premium plan prices for different markets, the comparison is likely to be valid):

Now that music has become even more pervasive with the rise of social media, this is adding growth opportunities for Spotify.

Value Chain

For the entire 20th century, music labels owned both the copyrights and hardware. Their business was essentially vertically integrated tech and manufacturing monopolies disguised as art companies. They controlled the entire means of music consumption:

RCA (Radio Corporation of America) owned RCA records (Elvis Presley, David Bowie, John Denver…). They also invented the 45 RPM vinyl format and manufactured the physical record players you had to buy to listen to it.

Philips owned PolyGram Records. They also invented the Compact Cassette tape in the 1960s.

Sony owned CBS Records (Michael Jackson). But they also co-invented the Compact Disc in 1982, and manufactured the Sony Walkman that played them.

But today, the labels have lost this positioning.

Now the music industry is dependent on third-party platforms to distribute its products. These are very big players like Apple, Google, Amazon, and Spotify. They own the distribution, algorithms, hardware, and most importantly, the customer data.

Music labels continue to be the constant gatekeepers, but they lost the music value chain control. The top 3 labels: Universal (UMG), Warner (WMG), and Sony Music still control nearly 70% of digital/physical music market share today. However, their scope has been reduced to artists, while paying “rent” to platforms.

Music Labels

We need to segment music into 2 separate businesses:

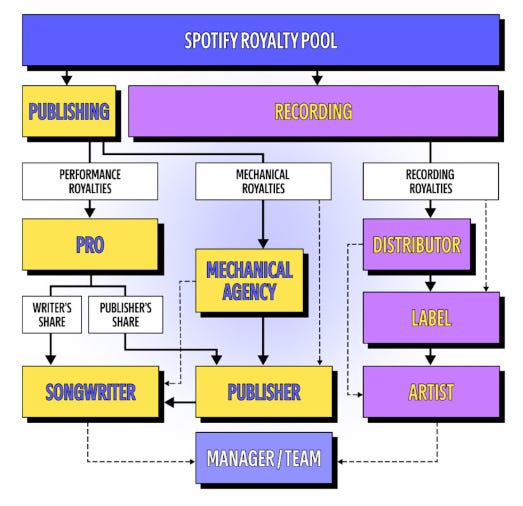

Publishers: They work with songwriters and pitch songs to artists to perform. Publishing royalties are earned for the use of a song’s composition and paid to the songwriters and their publishers. They include performance and mechanical royalties, which are earned, tracked, and collected by societies around the world.

Recorded music: This is the area music labels operate. They discover and fund artists and make agreements to share the earnings from the “master record” at a pre-determined split. Labels get paid only based on the master record, so if an artist performs at a concert, the publisher gets paid and not the labels.

We will focus on labels since they have significant impact on Spotify's gross margins.

The economics of labels are similar to venture capital; they fund lots of artists but only a small handful make it big.

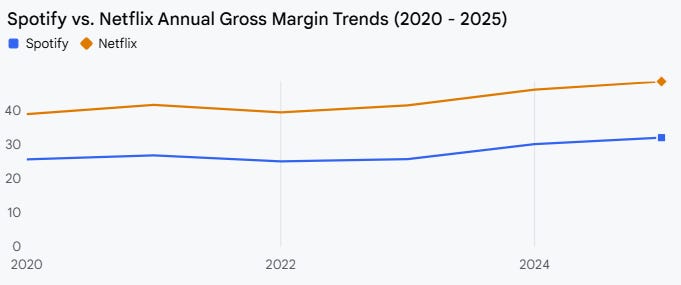

The power of labels lie in their control of music supply. Spotify’s suppliers are the music labels and such concentration of market share is usually a bad sign. You can quickly see Spotify gross margin is inferior to Netflix even though both of them have the same streaming business model:

Since it is the streaming platforms who are doing the hard work of growing the market, the labels get to enjoy a growing royalty fee.

But there’s a case of prisoner’s dilemma at work here. Since royalty fees are distributed based on market share of music streaming, if one label decides to leave Spotify, then the remaining labels will make more money because the whole pie will be distributed to whoever is left. The only way labels can hurt Spotify is for all of them to leave together.

We can illustrate the economics of Spotify vs Labels:

Suppose Spotify earns $1000 from users who only listen to 2 singers: Bruno and Taylor, in a 3:1 proportion.

Spotify keeps 30% of revenues before passing the remainder to labels (Spotify doesn’t pay the artists directly). So the labels will receive total of $700, split into Bruno and Taylor based on the stream-count share (3:1).

Bruno’s label (WMG) gets $525 (75%), while Taylor’s label (UMG) gets $175 (25%).

These labels will take their cut and distribute the money further down the funnel to artists, songwriters and other parties involved according to the contracts they signed.

As you can see, artists under labels receive a smaller portion of the pie compared to independent artists who will get royalties after the distributor’s cut which is typically far lower at 10% to 25%.

But there is a good reason why famous artists sign with labels instead of going independent. In today’s world, there are between 100,000 to 150,000 new tracks uploaded to Spotify daily. That’s a huge number of audiences. Once physical distribution has lost it relevance, the world of streaming is much more complicated and independent artists will need a team of professionals to manage this work.

Given that most artists earn their money from concerts, marketing and merchandise, they don’t have incentives to do manage distribution and will delegate it to streaming platforms. Without a distribution platform, independent artists may enjoy a larger share of the pie, but the pie itself wouldn’t be large.

A special note is given for radio. In the US, traditional AM/FM radio stations are entirely exempt from paying performance royalties to record labels and performing artists. However, they still pay royalties to songwriters and music publishers.

Put together, the entire music value chain is an uneven playing field.

Business Model

Now that the labels lost control of the formats, music as a product has become commoditized. Most people reference a parallel to the video streaming wars between Netflix, HBO, Disney… this is a wrong comparison because each of them are differentiated. For example:

Stranger Things is exclusive to Netflix.

The Last of Us is only on HBO.

Music is really commoditized with Apple, Amazon, Tidal, Spotify… all of them offering the same library of hundreds of millions of songs.

Spotify can be described as a business that streams audio on demand. It operates a freemium model and reports in 2 segments:

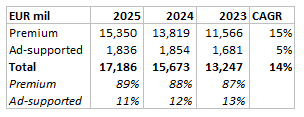

Premium (Revenues: $15.4b; Gross profit: $5.2b)

Ad-Supported (Revenues: $1.8b; Gross profit: $0.3b)

Premium Segment

Like most platform businesses, the 2 most important drivers for Spotify’s business are monthly active users (MAU) and average revenue per user (ARPU).

Spotify’s MAU went from 124 million (2016) to 751 million (2025). MAU is effectively a leading indicator for Premium subscribers, which grew from 48 million to 290 million over the same period. The proportion of Premium users have been about 39% to 48%, this has been stable because Spotify prices their subscription depending on the affordability of the general population of the country.

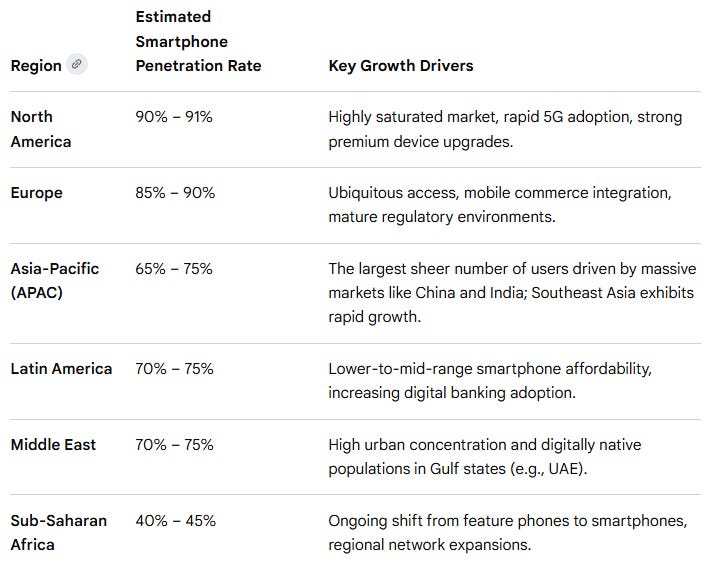

The drivers of MAU is smartphone penetration. Because Spotify cannot gain share unless users have smartphones and internet access. Both factors have seen continued structural growth:

In 2014, only 12% of the world’s population owned a smartphone, this number surged to 60% in 2024.

Since 1991 internet penetration went from zero to over 60% today.

Since music’s appeal is universal, we expect Spotify’s MAU mix will shift further into markets outside the US and Europe. Take a look at the region mix changes:

North America share: 34% (2016); 16% (2025).

LATAM: 19% (2016); 21% (2025)

Rest of World: 9% (2016); 37% (2025)

A key driver why Rest of World grew so much is because increasing smartphone penetration:

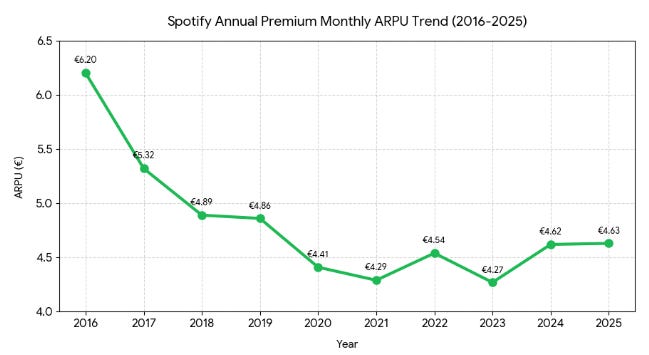

For ARPU, Spotify has many different Premium plans for every country. In the US, Spotify did not increase monthly prices since 2011 until a series of price hikes after 2022:

2022: $9.99

2023: $10.99

2024: $11.99

2026: $12.99

In emerging markets such as Bangladesh where purchasing power is lacking, Spotify has introduced daily/weekly plans. They also partnered with local telcos to let users buy pre-paid plans.

Due to the increasing number of MAUs from emerging markets, the ARPU has consistently decreased, until they increased prices recently:

Ad-Supported Segment

An Ad-Supported user is someone who is using Spotify for free, but listens or views advertisements between songs. The ARPU for ad-supported is very low at about €0.4 per MAU.

In 2025, there were 476 million ad-supported MAU. The growth is quite good; gaining 97 million users from 379 million since 2023.

Ad-Supported revenues are not a large piece, therefore Spotify have not focused on this segment:

Daniel Ek indicated before that he believes this segment should be 20% of revenues, and even more over the next 5 to 10 years.

Since the Premium segment is growing at +15% CAGR, Ad-Supported must do something special for Daniel’s statement to be true. There are a few possibilities:

Creating a two-sided marketplace where they sell ads and data insights to music labels and artists.

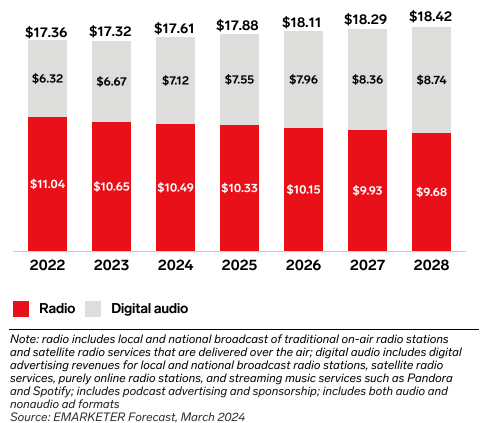

Taking radio advertising share. Radio remains the dominant medium for audio listening time, capturing ~62% of daily share. If we look only at ad-supported audio, 82% of audio time goes to radio and podcasts, while only 16% is spent with streaming music services. In terms of total ad dollars, radio’s share has shrunk as budgets have shifted to streaming.

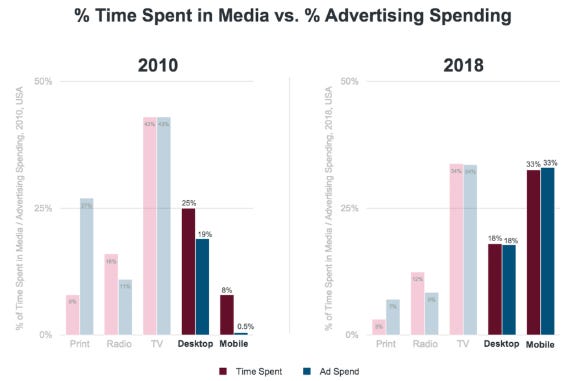

The shift is better understood looking at how advertising spend inevitably shifts to time spent over time:

One of the reasons for the persistent share of radio is because people choose to listen to the radio when they are driving. Americans drive about 13,500 miles a year, if we assume an average speed of 60mph, then people spend 19 hours per month driving!

As cars become more technologically advanced, we can expect streaming platforms to eat into radio's share. Spotify tried to launch a hardware accessory called “Car Thing” for old cars to play Spotify in 2021, however it was quickly ended in July 2022 due to poor sales. There are also Apple CarPlay and Android Auto which are big competitors.

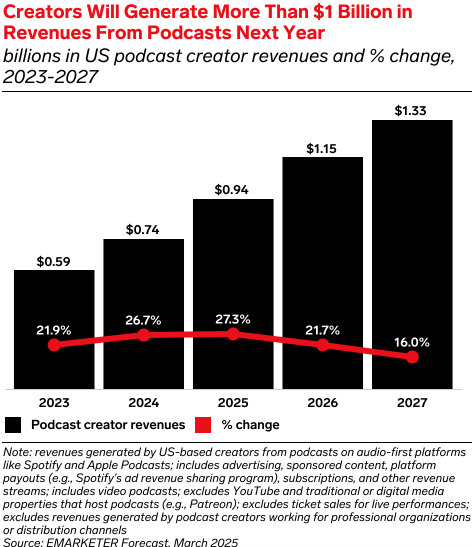

Rise of Podcast

There is a large number of podcast listeners worldwide estimated at over 500 million. 55% of the US population above 12 years old listen to a podcast at least once a month.

Below is an estimate of podcast revenues in the US:

Spotify used to significantly lag behind Apple for podcasts. Today it has grown into one of the top platforms for podcasts. They achieved this through acquiring exclusive content, copying the playbook of Netflix.

Podcasts escape the control of big labels and exclusive content not only creates more advertising opportunities but also converts free users into paid subscribers with a higher ARPU.

We have a growing body of evidence showing that there are significant benefits to engagement, retention, and conversion of users from Ad-Supported to Premium stemming from consumption of Podcast content.

We have seen benefits to retention on the order of several hundred basis points, which is a material change on a retention curve, for users that engage with spoken word content relative to those that haven’t, and early data indicates that these users are more likely to convert to Premium over time.

Daniel Ek, 2020

Acquisitions

Here’s a list of acquisitions Spotify made since 2019. The direction and ambitions of Spotify is quite clear: Empower artists to earn from their work on the platform.

Anchor

Consider their acquisition of Anchor (rebanded as “Spotify for Podcasters”) which is an introductory operating system for podcasting. It can be daunting for first-time podcasters to think about launching a show, Anchor simplifies and lower the barrier of entry.

Anchor has ~25% market share in the podcast hosting and publishing space. The other two major competitors are PodBean (34%) and Libsyn (10%).

Podz

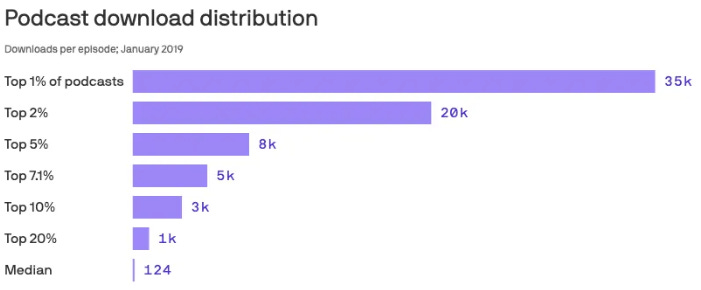

We mentioned above that music content is a commodity, but music curation is not.

When you have an enormous number of content, effective curation is critical. For curation to be good, Spotify leverages on their large user database. Since podcasts are much longer than a typical song, matching podcasts with the relevant listener is a strong value proposition.

This is where Podz is useful. It uses machine learning to pull the best clips from podcasts and deliver them to listeners in personalized feeds (AI can make this even more effective).

The idea is similar to social media feeds/reels applied to podcasts.

Take a look at podcast download distribution. The median is a miserable 124 downloads — nobody makes money on that. To solve this issue, Spotify wants to find a way to increase the reach of smaller podcasters.

On October 2020, Podz filed a patent on “audio segment recommendation” algorithm. The core of Podz product is the ability to ingest large amounts of audio and pull the signal from the noise.

Currently, Podz algorithm is trained on inputs from professionals. Over time, it will continue to improve as it learns what listeners most resonate with across categories.

Megaphone

Megaphone is technology for publishers and advertisers seeking targeted slots on podcasts.

The Spotify Audience Network is the ad network where Spotify delivers on-demand ads based on their understanding of the customer. In this sense the ads are much more akin to social media ads than webpage ads.

The problem is the only place these ads worked were with Spotify-owned podcasts played within Spotify.

This is why the Megaphone acquisition is important to Spotify’s plans. By owning a podcast host Spotify gained infrastructure to start inserting ads into podcasts played on other platforms, and also podcasts streamed on their own. These ads won’t always be quite as good given that Spotify’s knowledge of the listener isn’t as accurate, but the more inventory the better.

When the target is the listener, then every podcast can be priced perfectly, regardless of how many fans they have. This is good for the smaller players, but it’s especially good for the market maker, because there is no longer a premium being paid to larger players simply for being worth the trouble.

Challenge #1: Relationship with Labels

Spotify’s financial model behaves differently from typical software platforms. Usually in SaaS business, profit margins increase exponentially as the number of users increase. We know this as operational leverage. The cost of serving an additional user is near zero, a larger user base spread across the same fixed cost leads to higher margins.

Streaming music is not like that. They pay out ~70% of every dollar earned back to labels and publishers, hence costs scale linearly with their user base.

This model works for non-pure play music streaming platforms like Apple, Amazon, and Google. They don’t need their music platform to be profitable:

Amazon Music is a loss-leader to keep users paying for Amazon Prime subscription.

Apple Music attaches itself to sell iPhones.

For pure-play Spotify, when margins are structurally capped, it is actually the artists that suffer. Although not explicitly said, it makes sense that Spotify doesn’t want artists to have a relationship with their fans.

Of course… Spotify wants their fans to have a relationship with Spotify!

As a result, Spotify have to guard listeners’ data because it’s the most important proprietary resource.

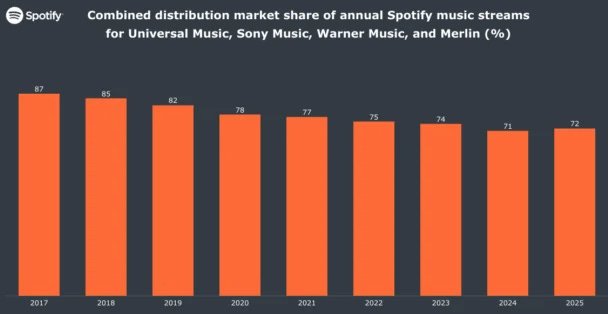

Fortunately, thanks to the rise of social media, independent artists (indies) have a much better chance to go direct to listeners. The rise of indies have taken share away from the top labels on Spotify.

The collective market share of the major labels has seen a steady decline, dropping from 87% in 2017 to 72% in 2025, as indies become more popular. This is a tailwind for margins.

Another quirk of the relationship between labels and Spotify is that subscription fees are not split between music and non-music content (see here for specifics).

Let’s say that you listen to 100 hours of audio streaming, split into 80 hours music, 20 hours podcasts (non-music). Your subscription fee goes entirely to the revenue pool to be distributed to labels/publishers/indies. So if you spend all your time on podcasts, your entire subscription fee still goes to the labels’ revenue pool.

If non-music content is growing rapidly, then we can see the vulnerability of the labels’ royalties. Why should labels receive royalties when you spend most of time on podcasts?

This is a touchy subject because the labels relationship is very much symbiotic and any large dispute can potentially hurt streaming growth for both parties. But we don’t think this equilibrium can last, the trend of non-music content will go up, and at some point Spotify should split revenue based on type of consumption.

In any case, Spotify has bargaining power simply due to the large user base.

Challenge #2: Big Tech

Competition is very strong with Google’s YouTube, Apple Music, and Amazon Music. All of them have deep pockets, low customer acquisition cost, and technological prowess.

There’s no doubt a challenge, but the details might prove otherwise.

Apple has been around the music industry even before iPhone was launched, but Apple Music was launched only in 2015. With 1.5 billion iPhone users today, Apple has an inherent advantage.

In June 2019, Apple Music mentioned that they had 60 million subscribers, today it’s estimated to be 95 million. During the same period, Spotify went from 108 million to 290 million paid users. It’s quite amazing that they added 182 million paid users, 5.2x the increase for Apple Music.

The reason is because iPhones market share is only ~20% globally although in the US their market share is much higher at ~60%. Android phones have a larger share in emerging markets, that’s why Apple Music loses out on the overseas growth.

Amazon Music launched in 2007 and charges a lower subscription fee than Spotify, but is only available in 50 countries. It is not designed to be a standalone product, and so it’s not really a serious competitor. It also has only 80 million users.

YouTube Music is probably the most dangerous competitor. Their strategy is to insert enough ads in the free version to incentivize upgrading to paid tier.

YouTube Music (and its ad-free bundle with YouTube Premium) has surpassed 125 million paid subscribers worldwide, including free trial users. Growth is significant, adding 25 million subscribers from 100 million in 2024. The potential of YouTube is their ability to buy exclusive non-music content, they can easily attack the podcast market and buy top content to become a big player.

However, video is far more profitable than audio for YouTube. So there’s a cannibalizing effect that YouTube has to think about. On the other hand, it’s easier for Spotify to move from audio to video (they launched video podcasting in 2020).

Indirect China Exposure

In 2017, Spotify and Tencent Music Group (TMG) swapped equity with each other.

Spotify received 9% share of TMG.

Tencent (parent) and TMG took 9% stake in Spotify too, which makes them Spotify’s 3ʳᵈ largest shareholder.

As far as we are aware, such equity swaps are uncommon. It made sense because China prohibits foreign investors from investing in companies engaged in audio-visual programs businesses.

We think there a several mutual benefits:

Spotify gains a lot from a closer relationship with TMG and learning from their playbook of integrating social experiences with music.

Both companies gain additional negotiating power with music labels. Tencent is extending this influence, in 2020, they bought 10% of UMG and 5.2% of WMG.

Spotify shows a novel approach to gain exposure to the Chinese market. Competing directly in China is never a good idea for Western companies.

While Spotify is the clear giant, the broader competitive landscape is fascinating. YouTube Music's aggressive growth is hard to ignore, especially given their absolute dominance in Southeast Asia and their massive 86% market share in India.

Really enjoyed the historical perspective on this one. Ek's pivot from early retirement to building a platform that essentially saved the music industry's revenue model is fascinating. Exceptional write up thank you for putting it together!