Study: Sogo Shosha

Japanese Trading Firms

Sogo Shosha (総合商社) is a japanese term that roughly translates to “General Trading Company”, this category is used to refer to the 7 large publicly listed companies on the Tokyo Stock Exchange.

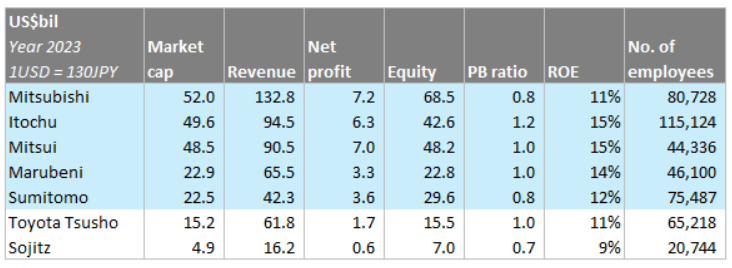

The 7 are Mitsubishi, Mitsui, Itochu, Sumitomo, Marubeni, Toyota Tsusho, Sojitz. Among them, the Big 5 were investments that Berkshire started buying in 2019:

At the end of 2024, these holdings amounted to $23.5b at a cost basis of $13.8b. These purchases were funded by JPY denominated all fixed rate bonds, as we know the cost of debt is very low relative to the dividend yields of these companies. Quite a good decision considering an unrealized CAGR of +11% before dividends & financing cost.

Moreover, these businesses are quite large collectively the big 5 market cap is more than $300b today.

Importance to the Japanese Economy

The Sogo Shosha are at the top of the Japanese business pyramid and are considered prestigious in Japan. One reason was the important role they played in the economic development of Japan. During the 1980s, Japan’s economy was the world’s second largest, and Sogo Shosha sales was over 30% of Japan’s total GDP!

An even more impressive figure is total amount of Japanese imports and exports they handled. As a group, these companies accounted for 65% of Japan’s imports and 50% of exports, bringing in mostly raw materials, commodities and exporting manufactured products.

As time progressed, their share of GDP decreased as structural changes to Japan’s economy allowed for foreign direct investments. Starting with pressure by the US over trade, particularly related to cars, and combined with the depreciation of JPY, Japanese manufacturers began to move overseas.

Their portion of offshore trade increased from ~8% of their total sales volume in the 1980s to nearly 40% in 2017, as they continued to supply Japanese manufacturers overseas, expanding their presence outside of Japan in the global supply chain.

History

Before World War 2

During the Edo period, the Tokugawa Shogunate (1603 – 1868) united Japan under an isolation policy. After this regime ended with the Meiji Restoration, trading companies first came into existence in the mid-1800s, as Japan re-opened its ports to the outside world.

Powerful family-run conglomerates called Zaibatsu (財閥, lit. “wealthy clique”) came to power and operated the trading businesses with foreigners. Mitsui and Mitsubishi were the earliest such firms. Zaibatsu operated like monopolies until the end of WW2 when Japan’s anti-monopoly laws came into force in 1947.

Because Japan possessed little natural resources of its own, the country imported raw materials from overseas, added value through manufacturing, and then exported the finished products. This economic model resulted in trading companies taking advantage of the booming business opportunities.

Textiles were the first major business. Trading companies would import advanced equipment and machinery from Europe, and cotton from India. They then sold these to the nascent domestic textile industry, and provided the industry with funding support. Once the manufacturing was done, trading companies sold the finished products overseas.

Trading companies had other businesses like shipping and the importing of commodities and food too. These were successful, making them powerful and rich, and allowed them to grow even bigger by expanding into banking and insurance in the early 20th century.

Due to their economic influence, they had close ties with the government and corruption was rampant. They enjoyed a cozy relationship with Japan’s wartime government and supplied war efforts during WW2.

Post World War 2

After Japan’s defeat in WW2, General MacArthur ordered those Zaibatsu to be dissolved due to their close ties with Japan’s military government. Mitsui and Mitsubishi were broken into hundreds of entities, this was the big bang that gave way to the industry structure as we currently know of today.

Keiretsu

Although the Zaibatsu were dissolved, these entities still maintained loose ties and evolved into organized alliances known as the Keiretsu (系列, “grouping of enterprises”).

A Keiretsu contained companies that held each other’s stocks (cross-ownership). It typically consisted of a bank, a trading company, some insurance companies, and a large number of manufacturing companies. It was like an ecosystem; the group’s bank and trading company sat at the center and did business with everyone.

There used to be 6 major Keiretsu: Mitsui, Mitsubishi, Sumitomo, Fuyo, Sanwa, and DKB Group. Over time, some of these groups were broken up and today only the first three still kept their original names.

It is worthy to look at Mitsubishi as it is considered the most prolific Keiretsu. Under the group these are the well-known entities:

MUFG bank, along with Sumitomo Mitsui Bank and Mizuho Bank, are recognized as Japan’s mega-banks. It’s ranked the largest in Japan and third largest in the world.

Trading arm Mitsubishi Corp. This owns many energy, mining, chemical and infrastructure projects abroad and has 50% share in the convenience store chain Lawson.

Insurer Tokio Marine (P&C). Founded 146 years ago, it is the largest P&C insurer in Japan in terms of revenue.

Mitsubishi Electric: A world leading manufacturer of home electronics.

Mitsubishi Estate: One of the largest real estate developers in Japan.

Kirin Holdings: Beer company.

Mitsubishi Motors: Car manufacturer.

Nippon Yusen: Japanese shipping company founded in 1885, operating a fleet of over 800 ships.

Looking at this Keiretsu structure, we can see why the Sogo Shosha are so diversified. Because a Keiretsu group keeps all dealings within its own circle and locked outsiders out, they prevented specialized trading companies from becoming more dominant in Japan.

Even though there are many specialized trading companies in Japan that focus on specific niches, they do not have the scale nor reputation that diversified trading companies possess, and so are disadvantaged when hiring talent.

Keiretsu provided a model for Japan’s post-war growth. The advantage is that it allowed for faster information sharing and coordination within the group. The criticism of this model is that it breeds insularity and complacency within the group which implied bad corporate governance. This is a problem for minority shareholders.

There are cases when the trading firm “sacrificed” for the Keiretsu, investing in projects that would advance the group’s collective interests but were questionable for its own minority shareholders.

Fortunately, these governance issues are less of a problem today, as the Keiretsu has been relegated to more of a legacy structure. Cross-shareholdings have also been significantly reduced. Corporate governance has been the core subject of reform, and there has been real progress.

Nonetheless, it’s still fun to understand the path which the Sogo Shosha took to get to where they are today, as the Keiretsu was the defining feature of how business was done in Japan during its rapid post-war growth.

Problems in 1980s

As technology advanced, Japan’s growth engine shifted away from old industries to newer consumer electronics and cars. The winners of this shift were companies like Toyota and Sony which pursued a strategy to be closer to consumers and directly managed their own sales network.

The need for a middleman diminished and gave way to a wave of disintermediation within the Sogo Shosha.

Another macroeconomic impact was the strengthening of JPY following The Plaza Accord in 1985 which weakened Japan’s export industries.

Finally, Japan’s real estate bubble burst in 1991, causing many Sogo Shosha to bear losses due to bad loans and speculative investments.

Transformation

It would take this near-death experience for the Sogo Shosha to evolve into better capital allocators. First, they began taking larger concentrated stakes in companies rather than a large number of minority stakes. Second, they invested more in service industries like retail and healthcare.

What is more important is a restructuring of incentives; they no longer reward based on topline growth and focused on profitability and capital efficiency. Management incentives were changed to variable bonuses linking to financial performance. In the past, CEOs of the Sogo Shosha only earned a base salary, now they make as much as 80% from variable bonuses dependent on net income growth, and nothing is tied to topline growth.

Management teams also own more of their companies’ shares today. For example, Itochu’s CEO (Masahiro Okafuji) earned JPY649m in cash compensation but owns JPY3.6b worth in shares.

Overall, the organizational reforms made management incentives more aligned with shareholder interests.

The result of this transformation was astounding: In 2000, the Sogo Shosha group made zero profits, then 20 years later they made JPY2.1t !

However, the legacy of Keiretsu still lingers and quoting Katsuya Nakanishi (Mitsubishi Corp CEO):

Our problem is that we’ve overinvested in the past. Within Mitsubishi Corp there are around 800 subsidiaries. There are companies in here that we need to re-think their place in the business portfolio. In order to improve our capital efficiency, we need to be divesting some of them.

These companies acknowledge the problem and have worked on it. For example, Mitsubishi sets quantitative targets for divestments. This is a big difference from the past, when they spoke only of making new investments and never about exiting businesses.

Another example, in the last 10 years with thoughtful use of capital, Itochu grew shareholder’s equity more than 300% while returning JPY1.3t to shareholders through dividends and buybacks. Its ROE went from 10% to 15% to over 20%.

Business Economics

The Sogo Shosha have a stake in a wide variety of industries:

For such big conglomerates, it is challenging to understand each individual part. But broadly speaking, they do 3 things:

Trading, wholesale, distribution.

Investing.

Operating the different businesses they have a controlling stake.

Trading, Wholesale, Distribution

Think about selling Norwegian salmon to Japanese supermakets, or distributing bananas from the Philippines. Basically, they act as the middleman, earning a spread in the process. This is a remnant of the old business model before 1990s, as time progressed, they turned to investing capital as a way to create value.

Investing

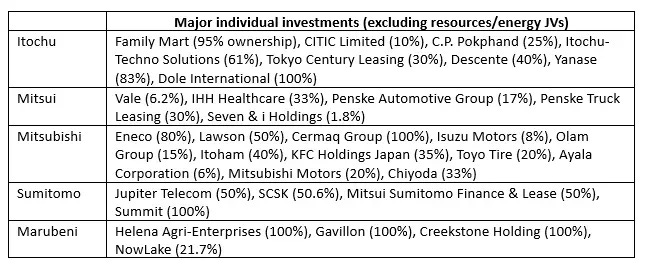

Using their own capital they make investment in places where they have experience operating. For example, Itochu acquired Family Mart in 2020, but prior to that they have already done business with Family Mart for decades. If we look at the entire value chain:

Itochu Feeds (100% owned) provided the animal feed at source.

Prima Ham (50% owned) processed the meat.

Nippon Access, Itochu Plastics (100% owned) handled the logistics and packaging.

In the earlier years, the Sogo Shosha saw investing as just a way to secure distribution rights for its trading businesses. Today, as trading operations declined over time, they are incentivized to allocate capital in a way that generates attractive returns.

Operating

The Sogo Shosha can either be hands-on operators or passive, it depends on the importance of the subsidiary. For example, Itochu is very engaged with Family Mart because it is a big and important business in Japan.

Talent Magnet

You might think that the Sogo Shosha is an old-fashioned, unattractive place to work. However, the fact is they attract great talent all over Japan. Look at this brand survey conducted for graduates:

The Sogo Shosha also rank among the highest in compensation:

Comparing the Big 5

Business Portfolio

Everyone in the Big 5 group has sizable exposure to resources & energy sector. Mitsui, Mitsubishi and Marubeni have over 50% to 60% while Itochu and Sumitomo have 30% to 40%.

Itochu is best known for the strategy to move away from resources, resulting in lower earnings volatility and likely the reason why the market gives it a higher valuation multiple.

Although each of them is highly diversified, there are industries where each company places greater strategic focus than others.

Itochu is more focused on services and consumers. Mitsui and Mitsubishi are known for their high commodities exposure, but they’ve also been historically big in the automotive space.

Mitsui has the Penske partnership in North America, while Mitsubishi has significant distribution interests in Southeast Asia for commercial trucks and pickups (subsidiary Tri Petch Isuzu has monopoly over all sales of Isuzu trucks and aftermarket parts in Thailand).

Sumitomo has been more focused on media and digital transformation through its ownership of JCOM (Japan’s largest cable TV) and SCSK (system integrator).

Marubeni is overweight agriculture through its US subsidiaries Gavilon and Helena.

Management Quality

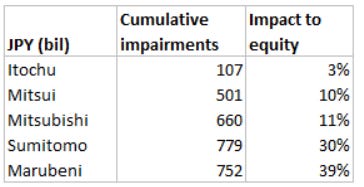

If we plot the cumulative impairments from 2010 to 2022 and the % impact to shareholders equity, we can see that Itochu has the best result:

The difference is very large, especially at the bottom Sumitomo and Marubeni has incurred significant amounts of impairment charges.

We think this also signals the difference in management quality within this group.

Incentives

All of the Sogo Shosha pay a substantial portion (60% to 80%) of total compensation as variable tied to financial performance. Some of them benchmark against net income, some use cash flows. None of them use revenues.

Mitsubishi has the most impressive one stating that variable compensation is zero if net income is below its cost of capital. They calculate a quantum for this cost of capital but we can work backwards to find the implied cost of equity of 7% to 8%, which is a fair benchmark.

Why Berkshire is Interested

The investment was funded by fixed JPY debt at near 0% interest rates, while the group were delivering 2.4% to 5.5% dividend yield at that time.

There is definitely a quantitative reason behind why Berkshire bought these companies because they were so cheap.

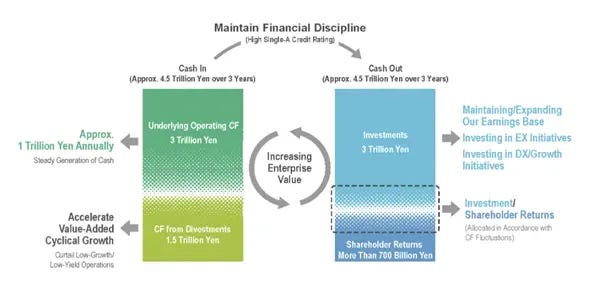

However, we have mentioned above that capital allocation is now the focus of the Sogo Shosha and it shows up in the results and incentives structure over the years. In short, Berkshire bought in cheap and is staying to enjoy improvements from capital allocation.

Berkshire also decided to buy a basket of them instead of individual bets, which is usually not what Buffett does. We think that he observed these companies from afar and did not have meaningful interactions with management before buying.

In a press release (Aug, 2020) Buffett wrote:

I am delighted to have Berkshire Hathaway participate in the future of Japan and the five companies we have chosen for investment. The five major trading companies have many joint ventures throughout the world and are likely to have more of these partnerships. I hope that in the future there may be opportunities of mutual benefit.

We think this may be a prelude to more investing activities in Japan, since for foreign investors the Sogo Shosha have business dealings with so many industries and could serve as a bridge to get into Japan’s economy.