Study: Progressive vs GEICO

Berkshire’s Letter to Shareholders

Warren Buffett published his 2024 letter to shareholders recently, he wrote quite a bit about the role that property and casualty (P&C) insurance plays in delivering value at Berkshire.

He emphasized the growing demand for insurance as the world becomes more affluent, increasing prosperity comes with higher economic activity, which drives demand for insurance. This relationship is not going to disappear.

The most important skill in insurance is pricing, as Buffett wrote:

Properly pricing P&C insurance is part art, part science and is definitely not a business for optimists. Mike Goldberg, the Berkshire executive who recruited Ajit, said it best: “We want our underwriters to daily come to work nervous, but not paralyzed.”

Insurance companies produce float as they collect policyholders’ money upfront but only pay claims later. Meanwhile, the float has to be invested; this fact links the success of the insurance business to investing skills.

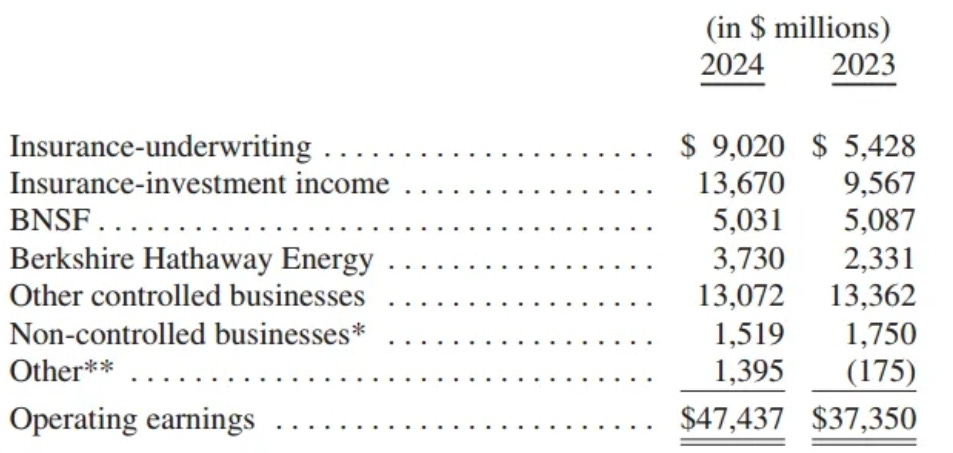

Despite Berkshire owning so many non-insurance businesses, nearly 50% of operating earnings were contributed by insurance:

GEICO

GEICO remains one of Berkshire’s most important entities. In 2024, GEICO’s net earned premiums (NEP) was $42b compared to $19b for BH Primary Group (consisting of ~10 distinct companies) and $22b for BH Reinsurance Group excluding life premiums.

Buffett gave praise to Todd Combs for improving underwriting standards at GEICO:

Our insurance business also delivered a major increase in earnings, led by the performance of GEICO. In five years, Todd Combs has reshaped GEICO in a major way, increasing efficiency and bringing underwriting practices up to date. GEICO was a long-held gem that needed major repolishing, and Todd has worked tirelessly in getting the job done. Though not yet complete, the 2024 improvement was spectacular.

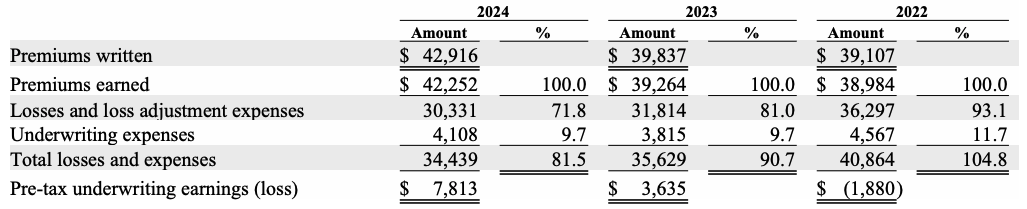

This is GEICO results for the past 3 years:

In both 2023 and particularly in 2024, GEICO delivered strong underwriting results. This was achieved primarily by removing undesirable customers and raising rates for most others. As a result, premium growth remained relatively flat. Policies-in-force (PIF) declined by -0.5% in 2024, following a sharper drop of -9.8% in 2023.

Despite better profitability, it is no surprise that GEICO lost market share.

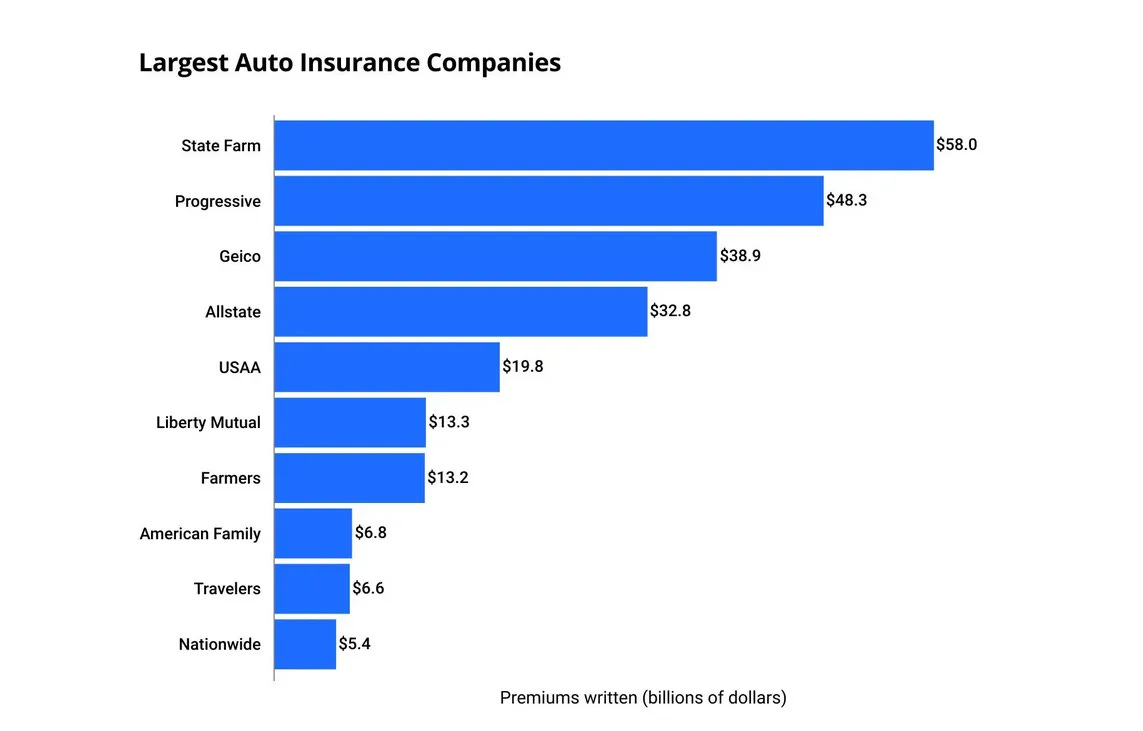

It was Progressive (PGR) who won a bigger piece of the pie and took over GEICO as the #2 auto insurer in the US.

Progressive Insurance (PGR)

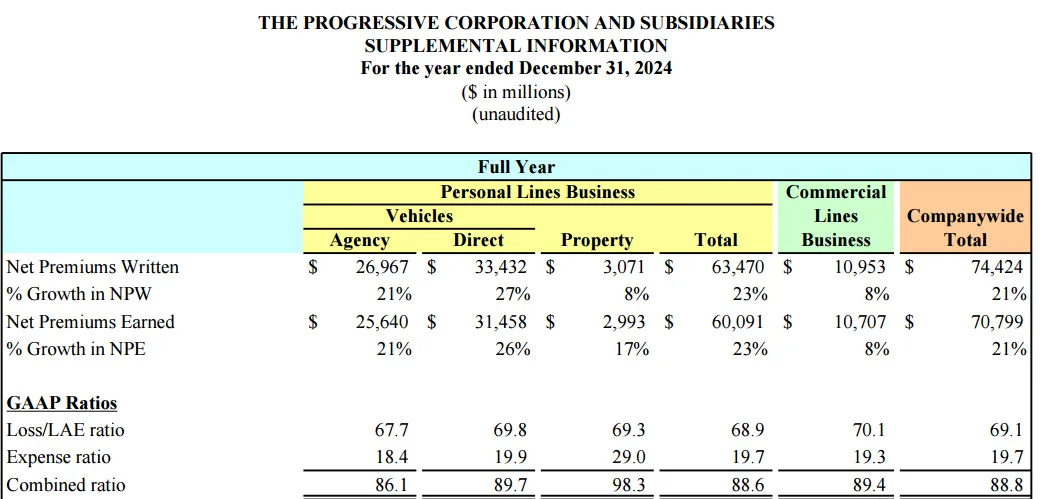

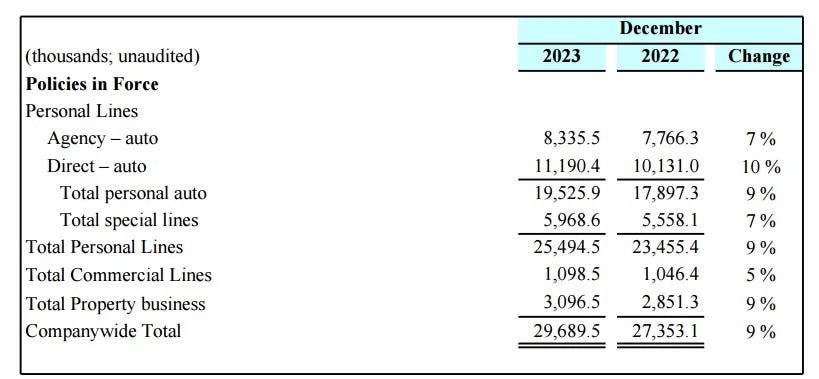

Below is the performance of PGR in 2024:

In Direct auto, PGR is still smaller than GEICO ($31b vs $42b in NEP). But when we add Agency channel’s $26b that GEICO does not have, PGR is noticeably bigger at $57b. The growth in rates was much higher too at +27% for PGR Direct; +7% for GEICO. It should not take long for PGR Direct to catch up with GEICO if nothing changes. Buffett has reasons when he said the improvements are not done!

However, GEICO was more profitable in 2024 with combined ratio of 81.5% against PGR’s 89.7% in Direct. In 2023, GEICO had a better combined ratio as well 90.7% vs 92.7%.

Although both companies emphasize profitability over growth, the degree of emphasis differs. GEICO is a subsidiary within Berkshire that has to deliver cash for reallocation. Consequently, GEICO values underwriting profits more than PGR.

PGR is a standalone insurer ready to sacrifice some profitability to achieve higher growth. Its objective is to achieve maximum growth at a combined ratio below 96%.

Buffett was interested in buying GEICO for two main reasons:

1. Auto insurance was mandatory.

2. GEICO was the first to employ a direct-to-consumer strategy via phone, and later the internet. It worked without brokers and had a cost advantage.

The first reason remains intact but the cost advantage has gradually become less obvious.

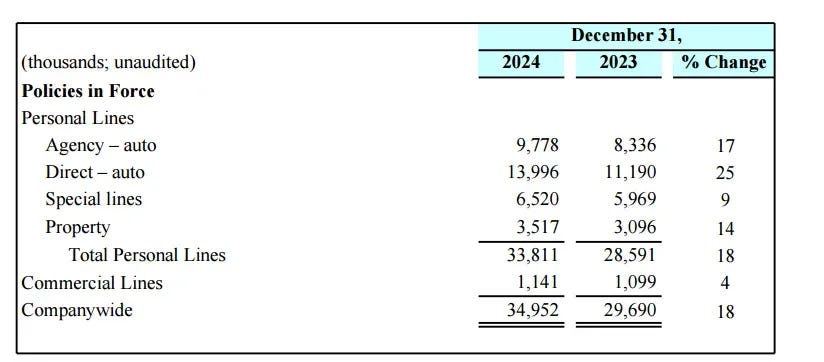

Implementing a direct channel strategy isn’t that difficult. Although PGR is still catching up in terms of direct sales, it is advancing very quickly, with YOY growth in PIF of +25% in 2024:

Going back 1 year, in 2023 the growth was also a good +10%:

However, gains in market share does not come for free. In 2024, PGR’s expense ratio for Direct was 19.9% against Agency’s 18.4%. Brokers became cheaper than advertising!

Compare this with GEICO expense ratio of only 9.7%, PGR efforts to eat into Direct consumer’s market comes at quite a cost. This shows that PGR is willing to maximize growth with the constraint on 96% combined ratio.

Market Share Dynamics

As a result of PGR aggressive expansion, it has overtaken GEICO since 2023 to be the #2 auto insurer in the US. Both companies will eventually surpass State Farm, but it won’t happen soon.

PGR has some advantages over GEICO:

It sells through both direct and brokers channels.

It bundles property and auto insurance.

It offers usage-based insurance (UBI) and has a lot of data for accurately matching price to risk.

For points #1 and #2, GEICO does not have the capability or willingness to match. The #3 advantage, though potentially temporary, remains challenging to compete against. Since PGR has been using UBI for many years, they would have collected a vast array of high quality data. This coupled with machine learning or AI tools can further widen its economic moat.

GEICO was late in implementing UBI, only starting in 2019 with an app called DriveEasy that scores drivers based on their driving stats. The advantage in loss ratio is indeed narrowing; back in 2019 PGR was 12% points ahead, now in 2024, GEICO recorded loss ratio of 71.8% while PGR had 68%, only 3% points gap.

Conclusion

Both companies have very strong qualities and are improving on their weak points. GEICO results on lowering loss ratios is impressive and if continued we can expect Berkshire to benefit greatly from the extra insurance float generated.

PGR also grabbed market share through direct consumers, although this came with high advertising costs, it can be expected to decrease if PGR manages to retain those customers they converted. They still hold the data and pricing advantage within the industry and it will take some time for this to be competed away.

In terms of economic moats, GEICO being the low-cost producer and PGR better at matching price to risk; the reality is that these factors can eventually be competed away. However, there’s one advantage for GEICO that is quite impossible to replicate, that is being a subsidiary of Berkshire instead of a standalone company.

This is why we favour GEICO more than PGR:

It writes the most premiums but requires the least capital. The statutory requirement is $3 of premiums for every $1 capital.

Since Berkshire has so much capital, the float produced can be concentrated in long-term equities. PGR as a standalone company has to invest most of the float in short term fixed income securities.

Claims can be paid by cashflows from non-insurance operations, this corporate structure doesn’t exist in PGR.