Study: Price Matters (Home Depot)

Home Depot in 1999

The internet bubble in the late 1990s affected tech companies, but did you know that there were some non-tech companies that had stock prices detached from fundamentals too?

Let’s look back at Home Depot in their FY1999 when they had 930 stores. As the saying goes, “a rising tide lifts all boats,” the stock market was booming and even Home Depot’s management was wildly optimistic.

Home Depot ended FY1999 with stores growth of +22% from previous year. Net sales have grown from $24.1b in FY1997 to $38.4b in FY1999 (+59%). Earnings per share grew even faster, from $0.55/share to $1/share (+82%). Margins went from 5.1% to 6%.

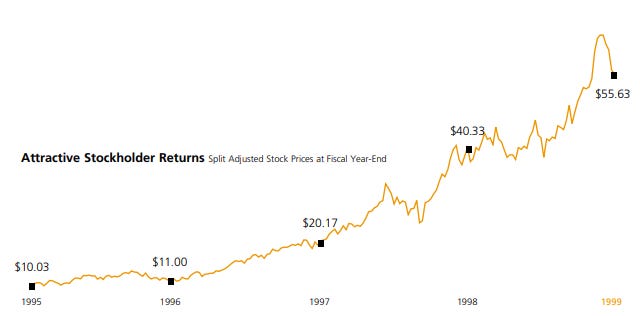

The market rewarded the stock with higher multiples, and its stock price flew up +180% from $20 to $55 in 3 short years.

All these good news boosted management’s confidence to target operating over 1,900 stores by FY2003, more than double the stores count in 4 years.

Our current plans call for consistent 21—22% annual growth in store openings going forward, taking us to more than 1,900 stores by the end of fiscal 2003.

Home Depot annual report FY1999

In this exercise we want to estimate what Home Depot is worth if they achieved 1,900 stores. As an investor, we want to be paid because Home Depot delivers high business growth and not due to price multiples.

Picture Perfect

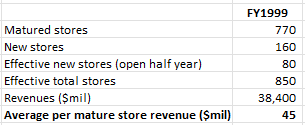

First, we need to estimate what is the revenues per mature store. Home Depot doesn’t disclose the average mature revenues per store, but we can make some guesses.

A simple average on 930 stores and $38.4b revenues gives $41m per store. However, they also opened 160 new stores that year and those would have been ramping up, at maturity they should produce more sales. Suppose new stores were only open for half year, the average revenue per mature store would be $45m.

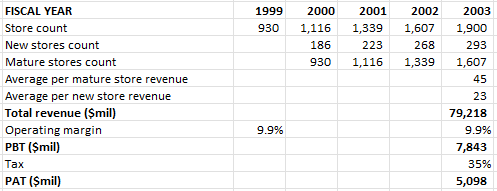

Now we can project to FY2003 where Home Depot achieves 1,900 stores.

These are our assumptions:

+20% store growth per year, end up with 1,607 mature stores plus 293 new stores.

New stores produce 50% less sales than matured stores. Total revenues = $79.2b.

No improved operating leverage, same operating margins 9.9%.

Corporate tax 35%.

Estimated profit after tax (PAT) = $5.1b.

What earnings multiple should be applied to this $5.1b earnings? It depends on your opinion on Home Depot’s future after they reach 1,900 stores.

Below are a few questions you could ask… the better your understanding of the business, the more accurate your forecast:

Can they have new product lines, pushing more sales through the same stores count for higher margins?

Can they continue to expand at this high rate after 4 years?

Can new e-commerce innovation improve their brand leadership and market share?

Depending on your assessment, you would come up with a range of earnings multiples. There’s no “correct” number, it’s always a range of outcomes. Let’s say a conservative investor settles for 20x earnings, while a bullish investor thinks 25x.

The valuation would then range from $102b to $128b, the market valued Home Depot at $128b. No surprises, as we have hinted at the start, the market was bullish on almost everything in 1999.

Interestingly, on page 5 of their annual report, they proudly displayed this stock price chart for the last 5 years:

And they had this comment about the dot-com mania:

During this period of dot-com mania, we firmly believe that, in the long run, the most successful online retailers will be those who know how to extend to the Internet the power of their brands, the leverage of their brick-and-mortar assets and the value of their customer service.

Think Carefully

Imagine looking at Home Depot’s report at FY1999, how comfortable would you be paying $128b which implies that the company must hit their 1,900 stores target?

Let’s say Home Depot really got to 1,900 stores and improved operating margins to 12% because of e-commerce.

Earnings would be $6.2b, at 25x multiples, Home Depot would be worth $155b.

Even so, the price return would be only +21% over 4 years, or about +5% CAGR. Add on some dividends and stock buybacks, you could possibly get +7% CAGR.

Is that a good return in a wildly optimistic scenario?

Obviously not.

Actual Outcome

So what actually manifested?

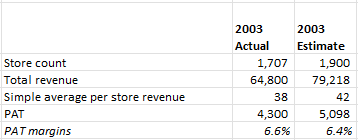

In 2003, Home Depot operated only 1,707 stores!

Management commented on the disappointing results:

[…] new stores cannibalized approximately 17% of existing stores and reduced fiscal 2003 comparable store sales by 2.7%.

Below is a summary of the actual outcome versus our estimate, our average per store revenue is higher because we didn’t consider cannibalizing effect:

That’s right, paying $128b at end of 1999 and hoping for a good result was foolish. Turned out that a $128b price tag meant that the 4-years forward multiple was 30x (against $4.3b actual earnings)!

Such an elevated starting valuation for retailer will not work out well.

Home Depot removed their proud stock price chart after their stock fell from $55 to $35 at the end of 2003. The market cap was $87b, earnings multiples contracted from 50x to 20x over those 4 years.

Recall the conservative investor who assigned 20x multiple? Even if he managed to buy Home Depot for $102b, he would’ve still lost money.

Think about that — even without the downside of lower multiples, investors who believed in their picture perfect story lost money!

Price Matters

We’ve come full circle to an old investing lesson:

Price is what you pay, value is what you get.

It’s a bad idea to think that you can buy a great company to hold for the long term.

Home Depot is indeed a great company, it's the largest home improvement retailer in America today worth over $314b. It endured the 2008 housing bubble and survived, having a dominant market share of over 50%.

But if you had ignored the price, bought the stock in 1999 at $55/share and held it till today's $316/share, your price return would be +6.7% CAGR.

However, if you waited for a more reasonable valuation in 2003 at $35/share, your price return would be +10% CAGR (add on dividends and you could beat the market).

The difference of +3.3% returns over 23 years is not trivial: $100 would have turned into $211, more than double!