Study: Pharmacy Benefit Managers (PBMs)

Preface

In the course of our reading, we found that PBMs capture a lot of value by playing a major role in the provision of pharmacy services. It functions as an intermediary between pharmacies, insurance companies, big pharma and drug wholesalers.

PBMs emerged in the late 1950s in response to specialized management of prescription drugs. Over time, they expanded into the supply chain, claims processing, pharmacy networks and drug delivery.

This extensive influence caused insurers to vertically integrate PBMs into their businesses. Today, every major insurer has their own PBM responsible for negotiating prices and determining which drugs go into the approved list.

In this post, we explore their history, the services they provide and the economic moat they possess.

History

Before 1960s, people purchased their medications by walking into their neighbourhood pharmacy and dropping off their prescriptions for a reasonable price. In 1968, the first PBM was founded when Pharmaceutical Card System (PCS) provided a plastic benefit card that could be used to purchase medications at certain pharmacies. By the 1970s, they served as intermediaries by negotiating prices of drugs. It wouldn’t take long, in the 1980s when cost of drugs started to inflate, before PBMs started to exert their power and control over the pharmaceutical business.

Diversified Pharmaceutical Services (DPS) was one of the earliest examples of a PBM that entered the healthcare market from within a leading national Health Maintenance Organisation (HMO) called United HealthCare. Yes, this is the UnitedHealth Group that we are familiar today.

DPS initiated many strategies that are now core PBM services, for example clinical programs that helped insurers who don’t have the necessary medical expertise. SmithKline Beecham acquired DPS in 1994 and by 1999 UNH accounted for 44% of DPS total memberships. Then Express Scripts acquired DPS and consolidated its position as a leading PBM.

This trend of mergers and acquisitions is not uncommon. The above mentioned PCS was purchased by McKesson in 1972, then sold to Eli Lilly for $4.4b in 1994, then sold to Caremark for $5.3b in 2003. Eventually, CVS acquired Caremark in 2007 for $26.5b.

At this stage, the function of PBMs evolved into managing pharmacy benefits for health plans, negotiating drugs discounts with manufacturers and they provided drug utilisation reviews. They even created disease management strategies for chronic illnesses.

PBMs began creating lists that forced patients to use preferred products instead of newer, more efficacious drugs for the sake of profits. In 2012, Express Scripts and CVS Caremark began excluding drugs from their lists, so that any drug not included would not be claimable by the patient.

In 2015, the 3 largest public PBMs were Express Scripts, CVS Health (formerly CVS Caremark) and Optum (UNH subsidiary). The largest private PBM was Prime Therapeutics, owned and operated for state-owned Blue Cross Blue Shield plans. In 2024, these 3 PBMs generated ~$300b in revenues. On a total basis, prescription dispensing revenues were ~$680b.

Services Provided by PBMs

Formulary Design

The most important service provided by a PBM is the development and maintenance of a drug formulary. The formulary specifies which drugs the PBM will cover and the associated patient costs when the drug is dispensed. Formularies are typically developed by a committee of pharmacists and physicians, often called a pharmacy and therapeutics committee, who review clinical trials, US Food and Drug Administration approvals, and scientific literature to assess the value of different medications.

Formulary determinations are multifaceted and incorporate medication safety and efficacy, ease of use, adherence factors, cost considerations, and preferences of plan sponsors.

Formulary design varies from less restricted “open” systems, where almost all drugs are listed and available, to a more restricted “closed” system, where relatively few drugs are approved for patient access. The PBM manages all processes of evaluating drugs to be included in the formulary, determining what tier an included drug will be placed on and what incentives are placed to encourage use of preferred drugs.

Formulary tiers vary from 2 tiers (preferred and non-preferred) to multiple tiers that allow for more tailored restrictions and incentives, including higher out-of-pocket spending. The PBM typically maintains multiple formularies, each tailored to the preferences of a plan sponsor. Formulary design has a direct effect on whether patients can obtain prescribed medications and the associated out-of-pocket spending.

Utilisation Management

This includes practices like pre-authorisation, step therapy requirements, supply limits, insurance related (deductibles, co-payment…).

Pre-authorisation refers to evaluating the appropriateness of the prescribed therapy, often requiring the doctor to submit additional information before the PBM will approve payment.

Step therapy requires the patient to try a preferred medication and experience failure before approving non-preferred ones.

PBM can also set limits on the amount the patient can receive from a retail pharmacy, often requiring patients to obtain maintenance doses for chronic illnesses from an affiliated mail order pharmacy.

Price Negotiation

PBM negotiates with pharmacies, wholesalers, and drug manufacturers on behalf of insurers. Through this process the PBM earns rebates offered by drug manufacturers as they want to ensure their expensive branded drugs are included in the formulary and placed on a preferred tier.

Pharmacies negotiate the terms on which they will be paid for both brand and generic drugs to ensure that they are included in the network covered by insurers. The result of these pricing negotiations is that the net price to the insurer may be substantially less than cited prices. The net price is known to the insurer but not publicly known.

Pharmacy Network

Another service provided by the PBM is the creation and management of a network of pharmacies at which policyholders can access prescriptions. By restricting access to the network, competition is heightened, and pharmacies are encouraged to offer the lowest possible prices for the chance to serve the PBM’s patient network. The PBM generally ensures that policyholders have access to a mix of local retail pharmacies, specialty pharmacies, and mail order pharmacies. Some PBMs own pharmacies and encourage use of their affiliated pharmacies.

PBMs have played a major role in the expansion of mail order pharmacy services. As mail order pharmacies expanded, concerns regarding conflicts of interests and generic dispensing rate differences led to regulatory concerns. While mail order pharmacy has become synonymous with PBM ownership, prescription delivery has been a common practice for more than half a century.

PBM Economics

PBMs rely on 3 strategies to generate profits.

Rebate retention where the insurer pays the list price and the PBM is entitled to the rebates it negotiates with drug manufacturers. Research indicates that PBMs retain 0.4% of rebates in Medicare Part D and 9% (2012) to 22% (2016) of rebates in the commercial market.

Spread pricing where the insurer pays a fixed amount for each drug no matter how much or little the PBM pays the pharmacy for dispensing. The difference is the PBM’s gross profit on that claim.

Administrative and service fees collected from insurers.

These strategies create predictable income for PBMs, but also perverse incentives. Rebate retention incentivises the PBM to maximize rebates, even if doing so results in offering a preferred formulary position to drugs with higher list prices.

Spread pricing incentivises the PBM to squeeze lower costs out of their pharmacy networks.

All these benefits create the desire to vertically integrate across the healthcare value chain. We can see why the largest health insurers all have their own vertically integrated PBMs.

For drug manufacturers, PBMs have control over branded drugs’ sales volume through formulary design and utilization management. They also affect branded drug manufacturers’ net sales revenue through price concessions.

For pharmacies, PBMs can affect sales by influencing patient access to retail, mail order, and specialty pharmacies.

Ultimately, for patients, both premiums and out-of-pocket spending are largely determined by PBMs. These are reasons why this business receives regulatory and public criticism.

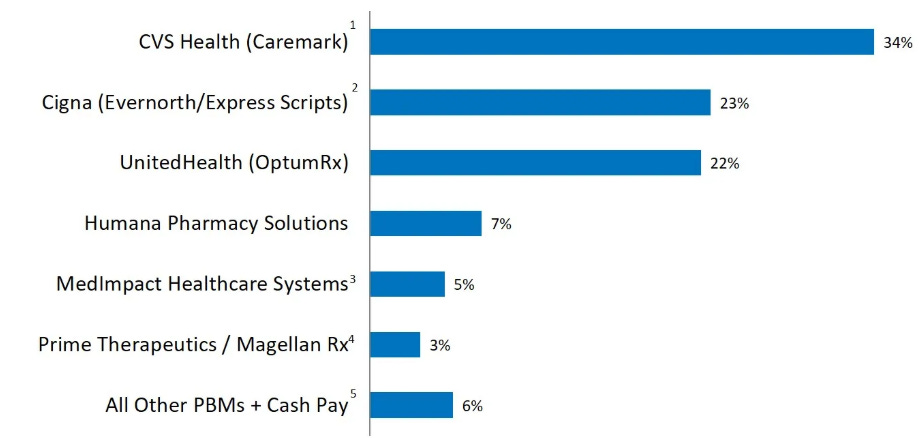

Competitive Landscape

The PBM industry is concentrated measured on equivalent claims managed:

The top 5 entities are vertically integrated with their health insurer. Mergers between insurers and PBMs have great synergies. Since PBMs earn rebates from drug manufacturers, they have incentives to place high-list-price/high-rebate therapies on lower formulary tiers. Although formularies generally enhance the efficiency of drug markets, when the PBM market is highly concentrated, the value created by these formularies can be captured by the PBM.

Several new business developments are increasing competition within the industry. In the generic market, GoodRx offer competitive PBM-adjudicated net prices to direct-pay patients. In response, OptumRx launched Price Edge to lower out-of-pocket spending for beneficiaries. Amazon Pharmacy’s RxPass Program also provides a $5/month direct-pay subscription, using its own PBM to adjudicate transactions.

In big pharma (Eli Lilly, Novo Nordisk, and Sanofi) announced up to a 75% reduction in the list prices of their insulin products and a monthly cost cap of $35 for commercially insured and uninsured patients. Additionally, Novo Nordisk announced a partnership in 2021 with Walmart to launch private brand insulin products, discounting list prices from 58% to 75%.

Conclusion

PBMs don’t necessarily aim to inflate healthcare costs, but rather they exist due to a logical, albeit complex, consequence of the fragmented and market-driven US healthcare system. They emerged from the need to manage administrative burdens and rising drug costs in a decentralized environment, PBMs have evolved into powerful intermediaries performing essential functions: negotiating prices, managing formularies, and streamlining the flow of prescriptions.

Their economic moat is built from economies of scale, established networks, and operational complexity. While regulatory risks exist, particularly concerning government intervention in drug pricing, the current political and fiscal landscape makes a radical overhaul unlikely. Furthermore, the vertical integration of PBMs within larger healthcare conglomerates reveals the lucrative effects of controlling most of healthcare’s value chain.