Study: Payment Networks (Visa & Mastercard)

Conviction by Reduction

Over the last 3 years, Visa (V) and Mastercard (MA) have grown EBITDA by 17% and 19%, respectively, even with Russia revenue (4% for both) reduced to zero, and we think there’s plenty of reasons to think profits will continue to grow at a similar rate for the foreseeable future.

Rather than expound upon V/MA moats, which are widely understood and appreciated by now, we thought it’d be more useful to discuss potential challenges. This is conviction by reduction; seeing how much is left after chipping away at competitive threats.

Digital Wallets

The most immediate bear case is that digital wallets would eventually disintermediate credit cards. PayPal could encourage users to directly link bank accounts to their wallets, which could then be used to transact with a PayPal-accepting merchant, creating a closed transaction loop that bypassed V/MA. Indeed, to avoid interchange fees, PayPal encouraged this behavior in its early days. Then in 2016, with customers complaining about being defaulted to automated clearing house (ACH), PayPal agreed to present V/MA credit and debit as “clear and equal” payment instruments inside the wallet.

Today every major digital wallet we can think of including PayPal, Apple, Samsung, Grab, MercadoPago… embeds or issues V/MA credentials. It’s easy to see why. Consumers want the assurance of knowing they can spend at just about any merchant around the world, online and offline, and earn interchange funded rewards along the way. A digital wallet that didn’t plug into V/MA would soon find themselves at a steep disadvantage to competing wallets that did.

The relationship between card networks and digital wallets is a symbiotic one. V/MA with their combined ~130 million merchants, enable immediate global acceptance that results in lower churn, larger order values, and more profit dollars for digital wallets. In turn, digital wallets, with their direct consumer relationships, expand distribution for card networks. Instead of taking away transactions from V/MA, digital wallets have pulled more transaction activity onto them.

Buy Now Pay Later (BNPL)

In a BNPL funded purchase for example a $1,000 sofa, the BNPL provider will pay $950 to the merchant and keep $50 for itself, then collect 4 separate $250 payments from the shopper over time.

The easier BNPL is to use and the more ubiquitously adopted it becomes, the more it behaves like a payments network than it does a loan. Unlike traditional lenders who live on net interest income, the vast majority of BNPL revenue comes from merchant fees. The more transactions a BNPL facilitates, the more SKU-level and repayment data they have to underwrite risk and offer a greater variety of payment options to consumers at checkout.

It may sound like BNPL systems can threaten V/MA networks, but we argue it is not true:

More than 80% of BNPL installments are repaid with debit, and due to fixed per-transaction fees, V/MA make more from multiple repayments than a single payment.

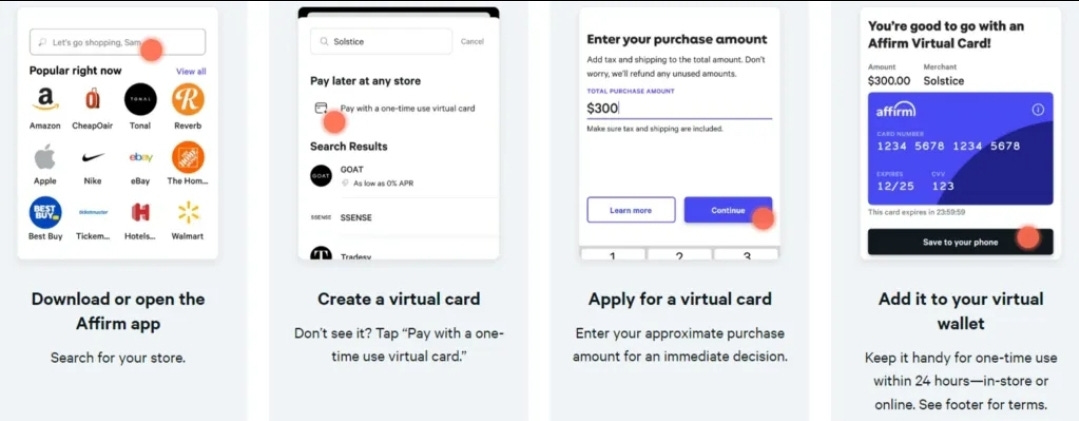

BNPL providers are now using virtual cards (a single use card for a specific amount) to settle with merchants. Example from Affirm (fintech with BNPL services):

The reason that BNPL fintechs are partnering with V/MA is simple: widespread merchant acceptance. V/MA are accepted by millions of merchants globally. Rather than integrate with merchants one by one, BNPL fintechs can partner with V/MA and reach immediate global scale.

Admittedly, pre-loading a virtual card isn’t a seamless user experience versus having it available at online checkout. And in the case where a consumer BNPL at checkout and repays with ACH, the card networks are indeed skipped. But in the increasingly common scenario where the BNPL provider settles with the merchant through virtual cards and the consumer pays off BNPL balances with debit, V/MA make money twice on the same purchase. As with digital wallets, BNPLs may ultimately reinforce rather than disintermediate the card networks.

Cryptocurrencies

For purposes of this discussion, we can segment the universe of digital assets into:

Cryptocurrencies with no fiat backing (Bitcoin, Ethereum)

Private stablecoins (Tether, USDC)

Central Bank Digital Currencies (China’s e-RMB)

Non-fungible tokens (NFTs)

V/MA touch all these categories. For example, they serve to purchase crypto assets on crypto exchanges. Additionally, with practically no merchants natively accepting crypto of any kind as a form of payment, V/MA serves to transit from the self-contained crypto universe to the real world. For instance, when a Coinbase customer uses their Coinbase debit card to purchase a cup of coffee, Visa will convert some of the customer’s crypto to a fiat currency that Starbucks can actually accept.

When it comes to CBDCs (digital tokens issued by a central bank) V/MA will directly settle those just as they would any other government-backed fiat currency.

We doubt V/MA care as much about crypto as the skeptics and optimists. V/MA see themselves as payments infrastructure and are philosophically agnostic to whatever form factor payments take. We can be cynical about the whole crypto complex and still agree that V/MA should lay the groundwork for playing a role in it. There is no contradiction here.

In owning ubiquitous payment infrastructure, the card networks can absorb frontier payments technologies without bearing much risk, adjusting their investment based on how things play out. In fact, it would be worse if the card networks took the strong dogmatic view that all this crypto stuff is garbage and ignored it completely.

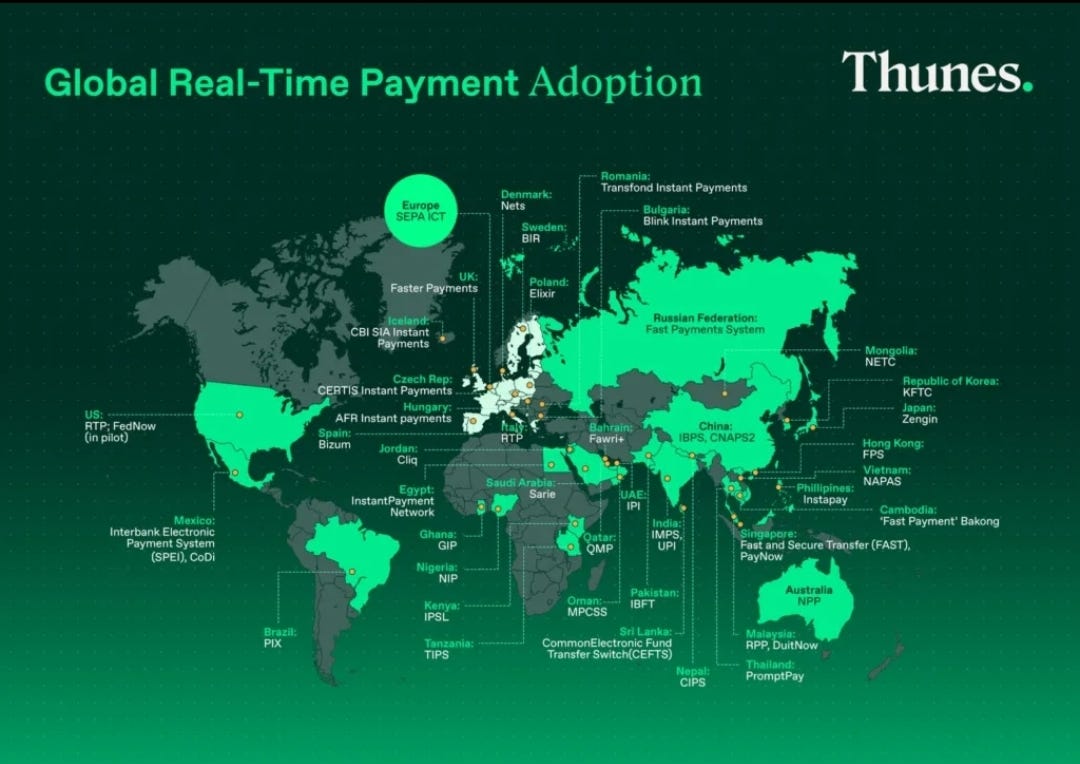

Real Time Payment (RTP)

A number of government backed RTP networks, which facilitate the transfer of funds from one bank account to another in real time 24/7, has gained popularity over the last 7 years:

In most countries, RTPs have mostly been relegated to peer-to-peer (P2P) transfers, bill payments, and business-to-business (B2B). But there are several notable exceptions in Netherlands, Brazil, and India, where ease of use and commercial bank sponsorship have spurred significant person-to-merchant (P2M) use.

In the Netherlands, iDEAL is an online payment system launched by a consortium of banks in 2005 that today has more than 70% share of the country’s e-commerce transactions, though debit cards still account for 85% of point-of-sale transactions and point-of-sale still comprises more than 80% of retail purchases. (Source)

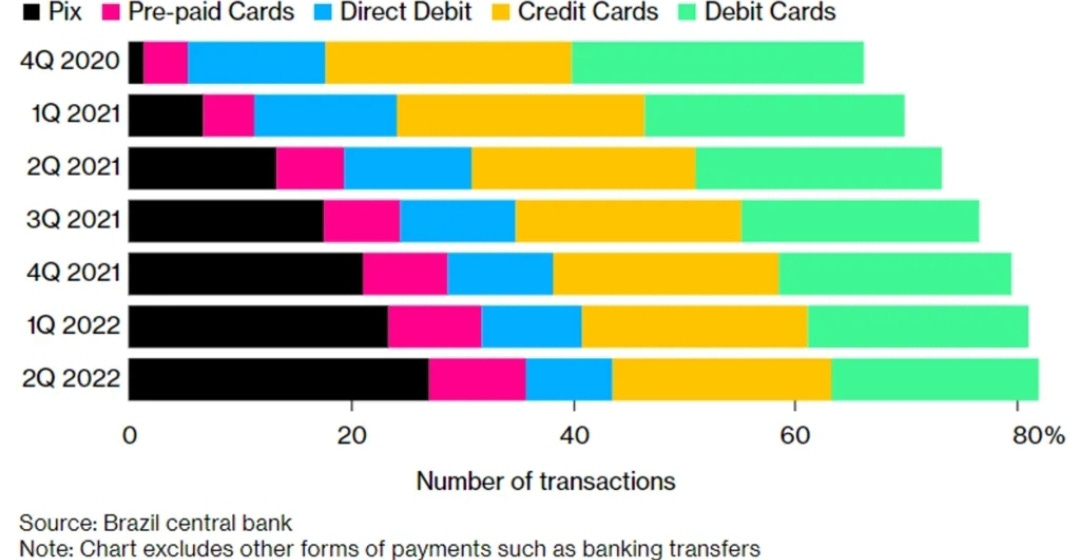

Pix, designed and managed by Brazil’s central bank, has become the most popular form of payment in Brazil, claiming ~30% of the country’s transactions in less than 2 years since launch. It has been used by more than 70% Brazilians, who need only enter a phone number, email address, or taxpayer ID from their banking app or wallet to send payments instantly.

In India, Unified Payment Initiative (UPI), launched in 2016 by the National Payments Corp of India, a non-profit retail payments organization created by the Reserve Bank of India, has exploded in popularity. UPI is the payments layer of the India Stack, a massive government sponsored project conceived in 2009 to usher the country’s 1.2b+ citizens into the digital economy. Over the last 3 years, its transaction volumes soared by 9x, UPI has become the most common electronic payment method in India, accounting for 63% of India’s non-cash transactions. It claims 41% share of P2M transaction value (56% by volume), on pace to overtake debit and credit, which still capture 53% of merchant acceptance by value (26% by volume). (Source)

India and Brazil, these are two countries long hailed by both V/MA as growth drivers. For the foreseeable future, we don’t think there’s much to worry about because cash transactions in these countries are still significant.

The rising tide of cash-to-digital payments has lifted all boats. While V/MA are less entrenched and face more direct competition in developing economies, those disadvantages have been more than offset by greater gains in per capita spending and electronic payments growth.

Consumers could increasingly use RTP to pay at online checkout or to fund digital wallets, which can then be used to pay for things, cutting card networks out of the transaction loop entirely. But in both cases we are still faced with the problem of merchants adoption.

V/MA functions globally while government-sponsored RTPs are for the most part, only useful for domestic transactions. Local readers would know you can’t use PayNow (Singapore) in Malaysia (Touch’n’Go). In theory, countries could solve the cross-border problem by integrating their RTPs, but in practice this hasn’t worked out.

In Southeast Asia, efforts have been on-going but it is obviously difficult to think that dozens of siloed RTPs across the world will agree to common standards, either through a series of bilateral arrangements or a common global hub.

The other way card networks are protecting themselves from competing networks is by climbing up the payments stack. Value-added services (VAS) have long been a part of V/MA offerings. For example, leveraging big proprietary spend data, the card networks help merchants and issuers detect fraud. They also offer marketing and business intelligence services that, for instance, can show a large fast food chain how much share they’re taking in a certain market compared to peers and how much of their spend comes from foreign card holders. For a card issuing banks, it reveals which rewards programs are popular with customers or how their card programs rank in terms of spend or retention relative to peers. V/MA compete fiercely for the business of card issuers, especially that of large banks, the incentives offered to card issuing banks have climbed dramatically as a percent of gross revenue over time, they will use VAS as an incentive to retain business.

Regulation

V/MA are greeted with varying degrees of regulation by foreign governments who would prefer their critical infrastructure be locally owned. In the extreme, foreign cards are blocked in China and Russia.

But even without outright banning, governments can still exercise soft power by promoting local schemes. In India, Rupay (the local card scheme launched in 2012), has captured the highest share of debit and credit cards.

Yet, even with 60% share of issued cards as of 2020 (up from 15% in 2017), Rupay handles less payment and transaction volume than V/MA combined. The disparity comes from the fact that credit cards account for a disproportionate amount of spend; so while India is contributing less to V/MA’s payment flows than it otherwise would absent government-backed competition, with cash giving way to electronic payments and consumer credit adopted by a growing middle class, the country is still additive to the card networks’ overall growth.

Opponents of the V/MA duopoly will emphasize the huge fees paid to banks and card networks. However nearly all interchange fees go to preventing fraud, servicing cardholders, and subsidizing consumer rewards.

In a 2014 study, the Federal Reserve Bank of Richmond found that the 2011 Durbin Amendment capping debit interchange “has had a limited impact on prices. Averaging across all sectors, it is estimated that the majority of merchants (77.2%) did not change prices post-regulation, very few merchants (1.2%) reduced prices, while a sizable fraction of merchants (21.6%) increased prices”.

The Durbin Amendment is the latest legislative proposal, Card Competition Act (CCA) of 2022, introduced by Senator Dick Durbin. It prohibited banks with more than $100b of assets from restricting the processing credit card transactions to V/MA network. This means merchants can route V/MA credit transactions, introducing more competition among credit card networks that will translate to lower interchange fees for merchants. The CCA builds upon the Durbin Amendment of 2011, which cut debit interchange for certain transactions from ~1.55%-1.6% + 4c/5c to 0.05% + 21c, reducing interchange fees per covered transaction by 45% on average. (Souce: here)

Thanks to the card networks, merchants realize more sales volumes than they otherwise would and consumers enjoy rewards, convenience, and global acceptance. Because of continuous investments in fraud management and the collateral requirements that card networks set for member banks, we can transact with any of the millions of merchants around the world, complete a transaction within seconds. The merchant, without knowing anything about the customer, can rest assured that money will flow correctly. For enabling all this, the card networks take just ~0.2% of the transaction value. That’s a marvel!