Study: Novo Nordisk

Preface

This is a update and collation of study notes, we have no insights for the pharmaceutical industry, this post is just a preliminary factual introduction to Novo Nordisk (NVO).

Because of this, we don’t include valuation, readers who are interested and have the necessary expertise can draw their own models and conclusions.

Pharma Industry

Size and Geography

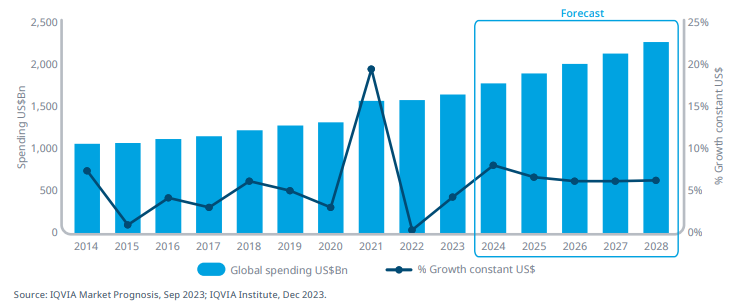

The size of the pharma industry is huge with an estimated global market size of US$1.6t, about 50% is contributed by the US, followed by Europe and emerging markets.

Below is the historical and forecast by regions:

Approval Process

Generally, there are 2 type of companies in this industry:

Producers of raw ingredients used in medicine.

Producers and distributors of final products.

It is the second type that can be further split into generic or innovative companies. Clearly, NVO lands in the innovative category. These companies rely heavily on R&D, patents and pipelines.

In the US, the approval of a new drug is made by the FDA and so they also design the approval process. Without going into the details, generally there are 5 steps:

Discovery & Development: Laboratory research for new drug starts.

Preclinical Research: Laboratory and animal testing for basic safety.

Clinical Research: Drugs are tested on people for safety and efficacy.

FDA Review: FDA examines all submitted data and decide whether to approve or not.

FDA Post-Market Safety: FDA monitors the products that are available for public use.

The clinical trials are the most important highlights, it is also the one that we hear often reported. These trials are divided into 3 phases:

Phase 1: Consist of 20 to 100 participants, mixed between healthy volunteers and people with the disease. Duration lasts over a few months to gather data on how the drug interacts.

Phase 2: Consist of up to several hundred people with the disease and lasts from several months to two years. The goal is to provide researchers with additional safety data such that they can refine their research questions and methods.

Phase 3: Consist of 300 to 3,000 volunteers who have the disease and lasts 1 to 4 years. This phase provides most of the safety data due to the fact that these studies are larger and longer, which means that the results will be more likely to show long-term or rare side effects.

If a drug successfully completes all 3 clinical trials, it goes to FDA for approval which takes about 6 to 10 months. The last phase is post-market monitoring.

R&D, Patents, Pipelines

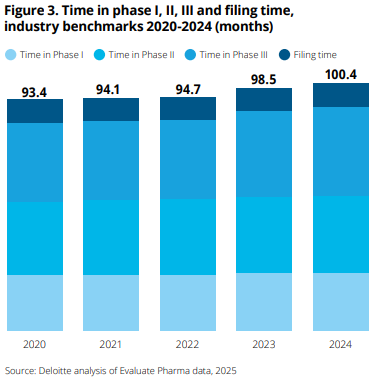

R&D spending is a large part of the pharma business taking up 15% to 25% of revenues. The average cost to develop a drug from discovery to launch grew from $1.3b in 2013 to $2.2b in 2024, nearly doubling over the past decade. Time spent on clinical trial phases have also increased over time and now the full process exceeds 100 months, with Phase 3 showing the greatest increase:

The reason why the pharma industry can afford high amounts of R&D is because patents on a drug gives the owner exclusive rights to sell for a predetermined time period, which is often 20 years after the patent is filed. This is the reward for R&D and it keeps generic competitors away for some time.

However, developing drugs is costly in terms of time-to-market too. Eli Lilly estimated that the time from discovery to patient is ~10 years and only ~8% of newly discovered drugs complete all stages of approval process. This means that a lot of R&D money will not materialize in profits, highlighting the fact that innovative companies rely heavily on drugs that eventually make it to market.

Since the patents today will eventually expire, innovative companies will face risk of revenue declines in the future. This brings us to the importance of drugs pipelines which is like the future roadmap. It must have a strong and diverse plan to help lower the risk of patent expiring drugs.

To understand the threat of competitors when a patent expires, we have to know the difference between generic and biosimilar drugs. Both are unbranded versions of existing medications sold at a lower price, making them attractive to consumers.

NVO portfolio of drugs is primarily protein-based (biological), this means that the main threat is from biosimilar drugs.

Generic drugs are typically made from chemicals and have a straightforward molecular structure. So they are often easy to reproduce and do not differ in terms of active ingredients. Generics can be cheaper by up to 85% than the original and are cheaper and faster to produce (~2 years) than biosimilars. In other words, manufacturers have to simply demonstrate that the generic drug is bioequivalent to the original.

Biosimilars have bigger and more complex molecular structures, making it much harder and more expensive to develop. The process can 5 to 9 years, while the product comes out to be 15% to 20% cheaper than original. Manufacturers have to prove that there are no clinical meaningful differences in terms of safety, purity and potency.

Therefore, there is a huge difference in how big the threat of new drugs after patent expiration is for pharma companies. It depends if it’s chemical or biological, the latter being far more expensive and difficult to produce, indicating that biological drugs are usually less threatened by patent expiry.

NVO History

In 1922, Nobel Prize-winning physiologist August Krogh and his wife, Marie Krogh (the fourth Danish woman to earn a medical doctorate) traveled to the US. Marie had type 2 diabetes, and during their trip, the couple learned of a literal life-saving breakthrough: the first successful insulin extraction in Toronto.

Canadian scientists Charles Best and Frederick Banting had discovered the molecule insulin, capable of treating diabetes, a condition that had previously resulted in death.

Soon after, August Krogh contacted Professor John Macleod, head of the institute in Toronto where the discovery had been made, and received permission to produce and sell insulin in Scandinavia.

Back in Denmark, Krogh partnered with Dr. Hans Christian Hagedorn, a colleague of Marie, and with financial backing from pharmacist August Kongsted, they founded Nordisk Insulinlaboratorium in 1923.

At Nordisk, Krogh and Hagedorn had hired brothers Harald and Thorvald Pedersen to help with the necessary equipment for insulin production and chemical analysis. The brothers did not get along with Dr. Hagedorn and left in 1924.

Together, the Pedersen brothers began manufacturing their own insulin, founding Novo Terapuetisk Laboratorium in 1925.

Nordisk, because of its earlier establishment, dominated the Scandinavian markets, while Novo sought growth internationally and by 1936, 90% of Novo’s production was exported.

In the decades that followed, both companies constantly pushed each other to innovate in the insulin market. In 1936, Nordisk introduced a longer-lasting insulin by adding protamine, reducing the number of daily injections needed by patients. In response, Novo marketed zinc-protamine insulin in 1938, which only needed to be shaken before use rather than mixed with a neutralizing liquid.

In 1946, Nordisk produced crystalline protamine insulin, which proved to be more reliable and effective, leading to its widespread use in the Western world. Again, Novo responded, this time by introducing its Lente products in 1953. These insulin variants had different durations of action and didn’t use protamine, which was beneficial for patients who were allergic to it.

In the 1970s, both companies focused on purifying insulin to address the issue of antibodies forming against insulin products, which made them less effective over time.

The next step was the production of human insulin which is identical to what the human body naturally produces. Before this, insulin was derived from animal sources, like porcine insulin from pigs. Human insulin is ethically more appropriate and, being identical to our own insulin, offers better tolerance and minimizes antibody formation.

In 1982, Novo successfully converted porcine insulin into human insulin. Nordisk followed two years later. In 1987, Novo began production of human insulin using genetically modified yeast cells. This allowed for the production of human insulin without relying on animals, enabling the company to produce insulin in nearly unlimited quantities.

In 1989, Novo and Nordisk merged to form Novo Nordisk A/S. By that time, Nordisk was the world’s third largest insulin manufacturer, and Novo was second.

In the following decades, Novo Nordisk continued to grow and innovate. In the 2000s, the company expanded its focus beyond insulin to include glucagon-like peptide-1 (GLP-1) receptor agonists. GLP-1 is a hormone that helps regulate blood sugar by supporting insulin production, slowing gastric emptying, and reducing glucagon release.

While insulin helps the body use sugar to give you energy, GLP-1 works to support insulin production, regulate the timing of insulin release, and slow the movement of food through the stomach, plus the added benefit of weight loss.

After extensive trials, it introduced Victoza in 2009, a GLP-1 receptor agonist aimed at diabetes patients.

In 2014, Victoza was followed by Saxenda, a GLP-1 variant designed to treat obesity.

Both Victoza and Saxenda used liraglutide, a GLP-1 receptor agonist, which required daily injections. In 2015, Novo Nordisk introduced a different type of GLP-1 called semaglutide, which allowed for weekly injections. This version led to the approval of Ozempic in 2017 for the treatment of type 2 diabetes. In 2021, Novo Nordisk released Wegovy, a higher-dose semaglutide designed specifically for weight loss.

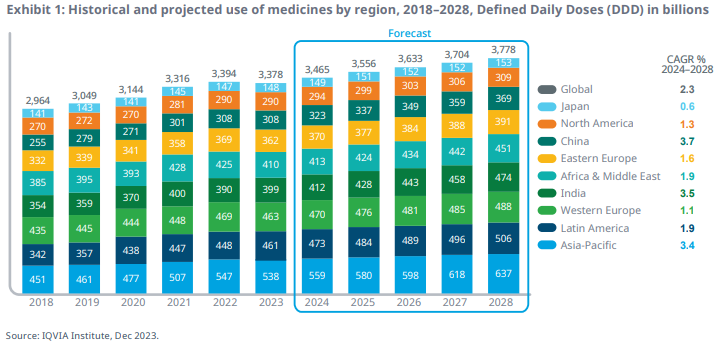

In recent years this trend of obesity therapy has become the second most important revenue source in the industry:

Business breakdown

Dual class shares

NVO has Class A and B shares with 1,075 million and 3,390 million shares outstanding respectively as of 2024 (AR, note 4.3). Each A share carries 100 votes and each B share carries 10 votes. It’s the B shares that are listed publicly and the A shares are held by Novo Holdings, whose ultimate parent is the Novo Nordisk Foundation, with effective voting control of 77.3%.

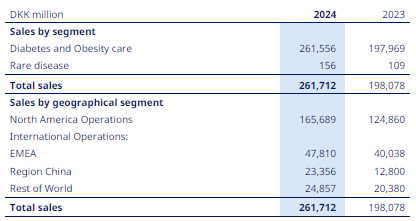

Sales by regions

NVO sells their products globally with the largest portion coming from North America (US and Canada). International operations are split further into EMEA (Europe, Middle East, Africa), China and Rest of World.

Product types

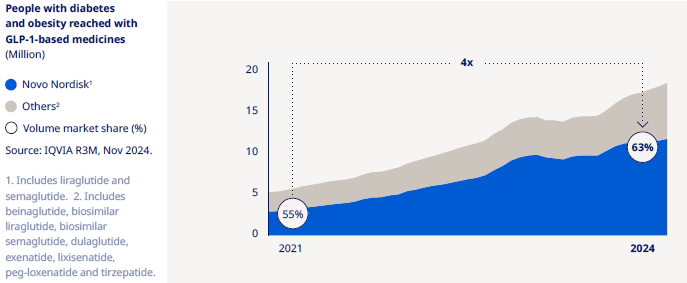

As we can see above, within the 2 segments of sales, “Diabetes and Obesity care” is almost 100% of sales. In 2024, NVO treated 45.2 million people (2023: 41.6 million, 2022: 36.9 million) and they have grown GLP-1 market share quickly in just a few years:

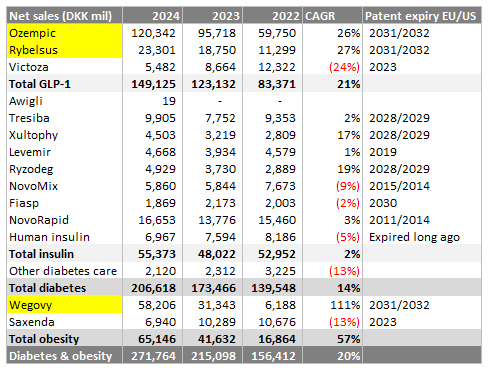

Within Diabetes and Obesity, the current products are (we recommend reading 2024 AR pg109 for sales by product/region):

GLP-1 products (Ozempic, Rybelsus, Victoza)

Long acting insulin (Awigli, Tresiba, Xultophy, Levemir)

Premix insulin (Ryzodeg, NovoMix)

Fast acting insulin (Fiasp, NovoRapid)

Obesity related (Wegovy, Saxenda)

Out of all these products, the most successful one is GLP-1 category. From 2022 to 2024, Non GLP-1 net sales only grew from DKK53b to DKK55b. Compared to GLP-1 it increased from DKK83b to DKK149b.

Clearly we can see the best revenue producing drugs highlighted in yellow with patents expiring 7 years from today.

Total insulin as a group has not grown much, with some products declining in sales as patents expire.

For the future pipeline projects, there are a whole list of products and descriptions of what they are in the 2024 AR pg23. We don’t have any special knowledge of how these drugs will translate in business opportunities, but here are some facts we learnt:

GLP-1 is NVO most successful product so far and it’s not surprising that there are 5 drugs projects running. IcoSema, a combination of GLP-1 receptor agonist semaglutide and insulin icodec intended for once-weekly subcutaneous treatment is currently at submission and/or approval stage. The rest are phase 3 and below.

Potential of IcoSema to simplify insulin intensification by reducing the injection burden to a single injection per week while providing glycaemic control and weight benefits.

In 2024, semaglutide 2.4mg went public as a patent update for Wegovy (obesity drug). Current pipeline are phase 3 and below.

Acquisitions

It is common for big pharma companies to acquire smaller innovative companies to either strengthen their current position or improve pipelines.

In 2023, NVO completed 3 acquisitions:

BioCorp for €154m, consisted primarily of patents and knowledge regarding Bluetooth enable add-on device for injection pens.

Inversago (Canadian company) for $1.07b & Ocedurenone (from KBP Biosciences) for $1.3b were pipeline related drug acquisitions. In 2024, CLARION-CKD phase 3 trial failed and NVO recorded an impairment loss of DKK5.7b related to the intangible asset ocedurenone.

In 2024, NVO completed acquisition of $11.7b related to three Catalent manufacturing sites from Novo Holdings, mainly financed by debt. These sites are specialised in the sterile filling of drugs and located in Bloomington (Indiana, US), Anagni (Italy) and Brussels (Belgium).

Business Economics

High Barriers to Entry

An obvious advantage NVO has is economies of scale, being able to produce large quantities of drugs in an cost effective way is a barrier for new entrants.

The capital requirements to create new drugs is also very costly and not all of them make it to market. With the patent system, new entrants will operate with negative cash flow until they have a marketable product, this also creates a barrier to entry.

However, the real high barriers are related to knowledge, as the raw materials used in drugs manufacturing is not very costly. The elusive resource is production methods and R&D, this learning curve widens NVO moat the longer they are in business.

Product Substitutes

Substitutes for NVO drugs come from biosimilars will only threaten sales upon patent expiry, and biosimilars only compete on price, they are not better quality than originals, so it doesn’t mean the original drug will face complete loss to biosimilars.

If NVO pipeline is strong enough, the threat of biosimilars can be minimized.

Customers Bargaining Power

End users of the product don’t have the option of choosing what treatment to use. When treatment is necessary, patients have to choose one that is prescribed by doctors. These patients are also single individuals who do not purchase in bulk.

Similarly, doctors do not have an economic incentive to sell one company’s product over another, they choose the most suitable drug for their patient’s needs.

Therefore, patients and doctors have low bargaining power with NVO.

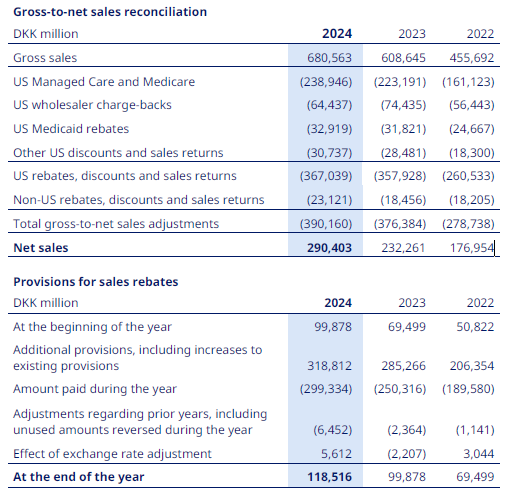

The interesting part is for government buyers, they are the public health insurance entities like Medicaid and Medicare. By having a large pool of consumers, they are able to negotiate prices directly with suppliers and in fact they receive substantial rebates from NVO:

Another group with bargaining power are private insurers. Pharmacy benefit managers (PBM) are companies that, on behalf of health insurers, manage prescription drug benefits. As they are also big buyers of drugs, NVO are forced to provide rebates in order to secure access to their markets.

Underlying Drugs

We don’t see patents as an economic moat for big pharma. The sustainable moat is actually the underlying drugs. The ability to produce strong and reliable drugs is still the underlying strength rather than refreshing patents.

A narrower focus on therapeutic areas gives NVO a sustainable competitive advantage in terms of R&D costs relative to revenue. For example, the average 5 years R&D cost percentage of revenues for NVO is 12% compared to Eli Lilly 25% and Sanofi 15%. Even with the lowest portion spent on R&D, NVO has very competitive portfolio of drugs. We can see this as better unit economics.

Human Capital

Pharmaceutical companies rely heavily on human capital referring to the skills, knowledge, expertise and experience of their workforce. This means that the long-term success of NVO and the rest of the industry are dependent on the ability to keep and attract high-quality workers for key roles.

Competition

The industry faces high competition between pharma giants, we examine the dynamics of their main products.

GLP-1 competition

The global market for GLP-1 products have increased significantly in the last few years and the market is expected to continue its growth in the future. NVO has been able to take advantage of this by entering the market at an early stage, establishing itself as the world´s biggest producer of GLP-1 products. The GLP-1 market is currently the most profitable for NVO.

The company started with the product Victoza, which has since then been surpassed by Ozempic. The biggest current competitor is Eli Lilly’s Trulicity selling about DKK35b compared to Ozempic DKK120b.

Both Trulicity and Ozempic are once-weekly injection treatments, and regarding both efficacy and administration there is little difference to be found between the two. Trulicity comes in packages of four injection pens, with one week’s injection in each pen. Ozempic comes with all four injections delivered in the same pen making storage easier.

Both treatments are deemed as “ready to use”. The price of a monthly supply of Ozempic in the US market in 2023 was listed at $1,326, with Trulicity listed at $1,315. The price points are very similar but it is reported that Ozempic users have lesser side effects.

The second fastest growing GLP-1 product is Rybelsus approved in 2019, it’s the first ever oral GLP-1 analogue product for type 2 diabetes treatment, creating a competitive advantage against competitors as the treatment came in form of pills instead of injections.

Until now, Rybelsus has been unchallenged except for Eli Lilly’s Orforglipron which just completed phase 3 trial in April 2025.

In 2022, Eli Lilly announced the approval of once-weekly GIP/GLP-1 co-agonist Mounjaro for injection treatment. It’s a new form of treatment and works differently by directly activating GIP and GLP-1 pathways to help regulate blood sugar. However, it is also more expensive than current products.

In response, NVO is also working on a GIP/GLP-1 co-agonist currently in phase 2. Another product, IcoSema, a mix between GLP-1 and insulin is also a competing product with Mounjaro. The competition of big pharma to outdo each other is intense, Eli Lilly is developing Retatrutide which is an extended version of Mounjaro, being a GIP/GLP-1/Glucagon receptor agonist and has shown increased efficacy.

Long acting insulin competition

This market is led by Sanofi and their product Lantus, it has been the most sold product for long acting insulin for the last 10 years. NVO has Levemir which patent expired in 2019 and Eli Lilly’s Basaglar (approved 2016) have captured some market share.

As the patents for NVO’s Tresiba and Xultophy are set to expire in 2028/2029, NVO has a late-stage product in their pipeline to compete in the long acting insulin market. Currently, Icodec is the product for growth waiting for approval. It is the first insulin product to be administered once-weekly instead of daily. This could create significant advantages for NVO.

Again, the competition is intense; Eli Lilly has a phase 3 Efsitora Alfa which is also a once-weekly injected insulin for treatment. Eli Lilly has not completed all of the planned phase 3 trials and will still need to await approval after that, whereas NVO is expected to have the first-mover advantage.

Fast acting insulin competition

All major products of fast-acting insulin had eminent patent expiration 10 years ago and NVO’s Fiasp was the only developing product in the market, which was approved in 2017. However, Fiasp did not become the high selling product they had hoped for. Even though NovoRapid’s patent expired in 2014, it is still the most sold product in the overall segment.

These products are on the list among top 10 drugs that Medicare is required to renegotiate prices which will be applicable from 2026 onwards. We can expect lower market share for NVO in the US market for this.

Human insulin

The market for human insulin is relatively small. NVO has a market share of 31%, with all of their current products within the segment having expired patents. Therefore, NVO does not possess competitive advantages on product differentiation, even though they are the largest supplier of human insulin in the world.

NVO has devoted their human insulin segment to those in need, through their Access to Insulin Commitment, where they sell human insulin to least developed countries at a highly reduced prices.

It has no products left with valid patents and no clinical projects in their pipeline. We expect that NVO will slowly lose market share in the segment in the future due to biosimilars.

Obesity care

NVO is the market leader and Eli Lilly is next. The potential within obesity market are significant, based on the number of people living with obesity and the small fraction being treated medically.

NVO has two products in the obesity care segment taking over 90% of the value in the obesity market. NVO entered the market in 2015 with the once-daily injection product Saxenda, which quickly reached a market leader position. In 2021, Novo Nordisk launched the once-weekly injection product Wegovy. Sales of Wegovy has increased significantly over the last three years since it was launched and surpassed Saxenda significantly.

The biggest competition is Eli Lilly and their Zepbound weight managing drug. Zepbound was launched in 2023 and is also a once-weekly injection treatment, it is priced cheaper than Wegovy.

Due to increasing demand, both companies are spending significant investments on production sites to increase supply. Price wars are not uncommon and we could see price hikes for Zepbound.

NVO has a patent update for Wegovy, if this is approved then it will be the first weight loss drug that reduces risk of cardiac injury (heart attack, strokes).

Eli Lilly is also hoping to set a high standard for the next generation obesity care treatment with their once-weekly product Retatrutide. It is currently in phase 3 and showed promising results from phase 2 trials. Retatrutide showed significant weight loss compared to the current products on the market and Eli Lilly is expecting Retatrutide to be their new bestseller in the obesity care market in the future.

Both companies have experienced huge financial gains from their products and has developed a substantial and promising pipeline. However, as the potential of the obesity market is becoming clear, they should expect a more severe competition in the coming years from other companies.

For example, Amgen with their weight loss drug MariTide is currently in phase 3 trials. Another example, Roche has purchased their way into the obesity care market with the acquisition of the private biotech firm Carmot. With this acquisition, Roche added 3 clinical-stage obesity care programs to their pipeline.

Rare diseases

We will skip this product segment economics as the size is very small.