Study: Microsoft Diversified Strategy

Preface

Vacation provides a great time for reading. We explore 3 cases of business strategy involving diversification at Microsoft.

One of them was wildly successful, another failed, and the last one is still an ongoing story.

Case 1: Operating System Wars

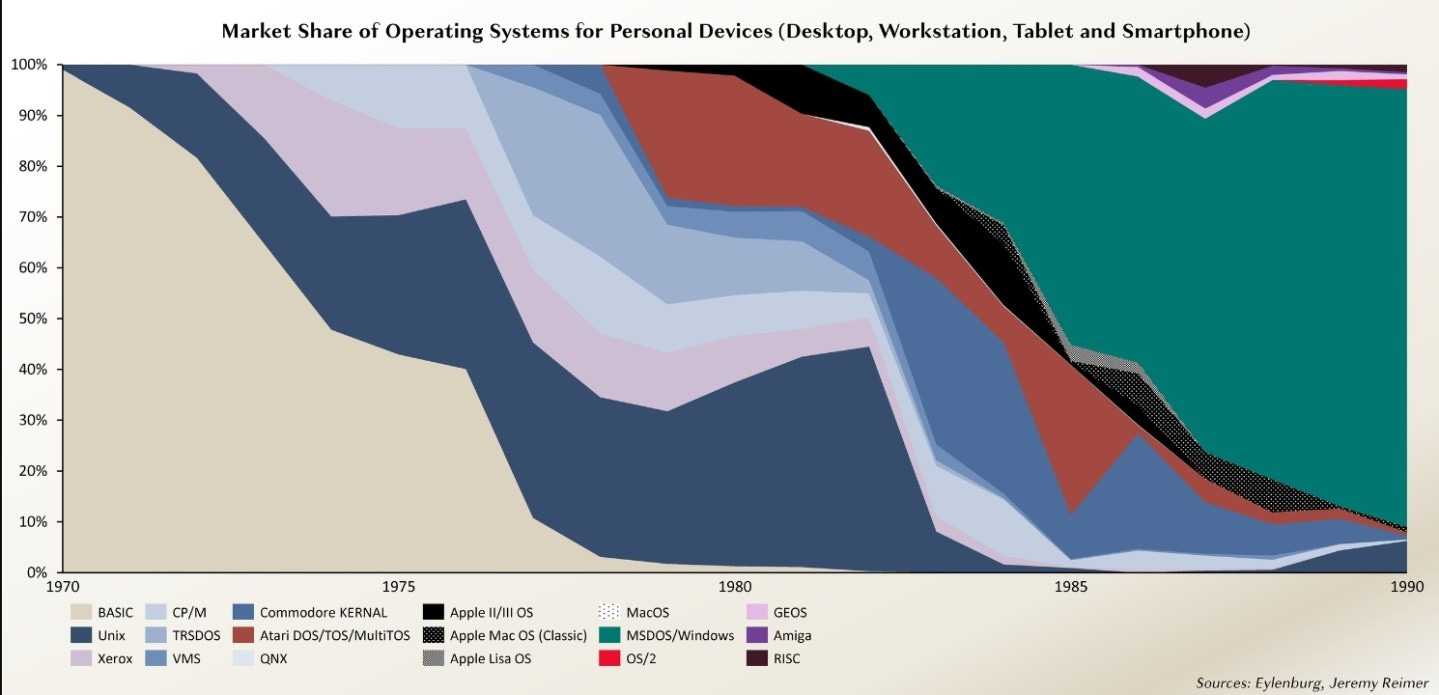

The first IBM PC debuted in August 1981. It was also the first computer to use Microsoft’s MS-DOS operating system (OS). At the time, Unix held ~55% share of the OS market, and the rest was split between a large variety:

Xerox Alto, 1973

CP/M, 1974

TRSDOS, 1977

Commodore KERNEL, 1977

Atari, 1979

Apple DOS, 1978

SOS, 1980

However, by 1985, MS-DOS had amassed more than 50% market share. By 1989, it held just under 90%.

Despite Microsoft’s success throughout the 1980s, the company’s founder and CEO, Bill Gates, suspected that DOS was approaching its end. Each year, there were more people who owned a PC, more importantly, the number of PC developers was increasing rapidly. These changes were great for the market, and Microsoft was a primary beneficiary, but it also changed the market in ways that could jeopardize Microsoft’s position.

There was also growing evidence of competitive and structural changes in the marketplace. For example, Apple’s line of graphical user interfaces (GUI) computers, which debuted with the 1983 Lisa PC, were increasingly popular and served as an obvious contrast to the command-line interfaces of DOS.

In 1984, MIT started a project to build the Window System for Unix.

In 1985, IBM had begun development of OS/2, which Microsoft signed on to co-develop, but in contrast to IBM DOS, OS/2 was spearheaded by IBM, not Microsoft, and designed to sell IBM PCs and hardware.

In 1986, a group that consisted of SunMicrosystems, AT&T, and Xerox began working on a GUI specification of Unix (OPEN LOOK, which later progressed into OpenWindows) that would make the OS more consumer-friendly.

In 1988, a similar collective, including IBM, HP and Compaq, formed to build Digital Unix.

Taken together, it was not hard to predict that platform-level changes might soon occur. In other words, Microsoft faced not just the prospect of new competitors, some of which were current licensors, but also potential disruption in its OS licensing business model, all of which threatened its growth, investment, and product strategy and might alter industry profit pools as well.

Diversified Bets

To manage this uncertainty, Microsoft undertook a portfolio of bets throughout the 1980s and early 1990s that were often competitive with one another. These bets collectively replicated the diversity, unpredictability, and dynamism of the market at large, thus maximizing Microsoft’s odds of success in any future state. These bets can be summarized:

1. Continue development of MS-DOS.

2. Collaborate with the many companies working on UNIX.

3. Major investments in Windows development started 1983, with Windows 1.0 shipping in 1985 and 3.0 in 1991.

4. Form partnership with IBM to develop OS/2 (1985).

5. Purchase 20% stake in Santa Cruz Operation, the largest seller of Unix systems on PCs (1989).

6. Develop a suite of applications (eg. Microsoft Office) that could function across OS, which Microsoft might have no ownership or influence.

While Microsoft had many parallel bets, it still had the preferred one: Winning the PC market via a licensed OS which was Windows.

As Microsoft had been so successful with Windows, the company could have proceeded with that single strategy.

Yet this wasn’t necessary, and indeed, some of those other bets failed precisely because Windows 3.0, which launched in 1990, was so successful.

One such example is OS/2. This jointly developed OS was always challenged by the conflicting priorities of IBM and Microsoft, but following the breakout of Windows 3.0, the partnership between the two companies became impossible to sustain.

By 1993, the Unix ecosystem had determined that a fully unified Unix was needed to combat Windows, prompting the Common Open Software Environment initiative, or COSE (founded by the Santa Cruz Operation, Univel, Unix Systems Laboratories, Sun, HP, and IBM). These hopes were crushed by Windows 95, which Santa Cruz, HP, and IBM had little choice but to support, especially as rivals such as Dell picked up market share.

It’s likely that Microsoft also had picked up extensive knowledge from its various bets, such as the rationale behind various technical and interface-related decisions. They used this knowledge to strengthen relationships with key industry partners, most notably those who manufactured and distributed PCs.

Even as Windows secured the market in the early 1990s, Microsoft remained paranoid about the right product offering. Prior to the launch of Windows 95, it released Microsoft Bob, which was intended to be an even more consumer-friendly GUI for novice computer users, but it failed miserably and was quickly killed the following year.

In 1995, Gates wrote his famous Internet Tidal Wave memo, in which he argued that the Internet was not just a critical new frontier for Microsoft, but one that might empower OS competitors or even displace the role of the OS altogether:

I assign the Internet the highest level of importance… I want to make clear that our focus on the Internet is crucial to every part of our business… The Internet is the most important single development to come along since the IBM PC was introduced in 1981. It is even more important than the arrival of the graphical user interface (GUI).

The PC analogy is apt for many reasons. The PC wasn’t perfect. Aspects of the PC were arbitrary or even poor. However a phenomena grew up around the IBM PC that made it a key element of everything that would happen for the next 15 years. Companies that tried to fight the PC standard often had good reasons for doing so but they failed because the phenomena overcame any weaknesses that resisters identified[…]

IBM includes Internet connection through its network in OS/2 and promotes that as a key feature. Some competitors have a much deeper involvement in the Internet than Microsoft. All UNIX vendors are benefiting from the Internet since the default server is still a UNIX box and not Windows[…]

Sun has exploited this quite effectively[…] and is very involved in evolving the Internet to stay away from Microsoft[…]

[…] A new competitor “born” on the Internet is Netscape.

Gates’ memo led to a flood of investment in the company’s digital efforts:

1. Internet Explorer (1995)

2. MSN portal search engine (1995)

3. $400m acquisition of Hotmail (1997)

4. Messenger (1999) etc.

They also remained diversified in traditional OS bets, purchasing a 5% stake in Apple in 1997 for $150m; the deal also involved Apple making Internet Explorer the Mac’s default browser.

Case 2: Mobile Phones OS

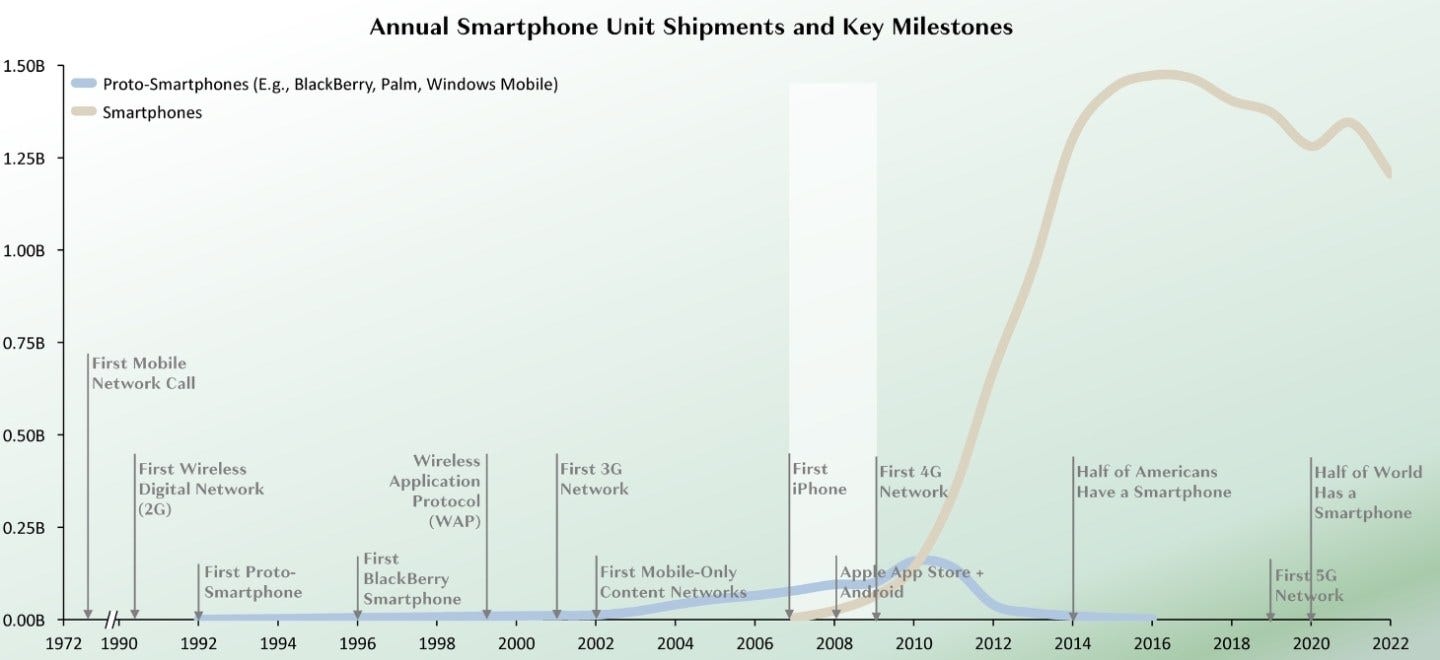

Going into the 21st century, it turned out that mobile computers would become more than two-thirds of the market, capping Microsoft’s share to a third at best.

Failure to Diversify

Crucially, Microsoft’s displacement in the mobile market resulted from no diversification.

In his infamous January 2007 CNBC interview, CEO Steve Ballmer laughs at the prospects of the just-announced iPhone, citing its high price and lack of a keyboard. It was the foundation of Microsoft’s mobile strategy, which rested on concepts that were shared by most notably BlackBerry and Palm that doomed their efforts.

They focused on ideas such as:

1. Smartphones should be $100–$200, not $500 or more.

2. Focus on business users not consumers.

3. Feature a keyboard.

4. Data usage should be minimized so as to protect scarce network bandwidth.

5. Batteries should last for days, not hours.

6. Fall damage should be minimal.

Though these bets sounded correct in the early 2000s, they proved to be grossly wrong over time.

When it came to the early smartphones, Microsoft’s approach (Windows Compact and Windows Mobile) was similar to its PC strategy, though it was cheaper at $20 per device.

The challenge here was that mobile computers were comparatively harder to build than PCs due to the vastly different constraints on size, power usage, and heat generation.

But in the mobile form factor, Apple’s vertically integrated approach led to a substantially better device. Apple built a truly mobile-native OS, rather than porting over most of the design principles of its Mac OS. The result was a device that totally outclassed Windows-based smartphones.

Pivot Too Late

Independent smartphone manufacturers rushed to catch-up to Apple’s hardware designs, and were somewhat successful, while also differentiating on other designed-related features (better cameras, larger screens).

However, these fell short on the OS and ecosystem side, there was still an opportunity for an independent OS provider.

This opportunity was lost to Google’s Android, which was not just a more modern OS but also free to device makers. In fact, Google offered OEMs and wireless carriers a share of Android-related search and Google Play app store revenues.

In effect, the OS business model had inverted from direct monetization to the sale of profitable hardware and software services, both of which Microsoft lacked.

By the time Microsoft pivoted, launching its free-to-license Windows Phone OS in 2010 and an exclusive partnership with Nokia, it was too late. Had Microsoft made parallel bets, its mobile OS might have survived. Incidentally, MacOS, iOS, and Android are all UNIX-based.

Case 3: Artificial Intelligence

When it comes to AI, it is a field with such obvious, diverse, and immense potential. It is also embedded with uncertainty around technology, business model, timing, cost, and implementation.

Given this context, it is no surprise that Microsoft is using diversified approach again to manage various uncertainties, many of which compete with one another.

Primitive AI

Though Microsoft Research was not formally established until 1991, Microsoft’s investments into AI began not long after Gates founded the company in 1975.

Microsoft’s first text processor, Word 1.0 for DOS, launched in 1983 and differentiated from competitors through the integration of “Spell Check”. At the time, MicroPro’s WordStar required users to launch a separate spell-checking program, while WordPerfect lacked the capability altogether.

Microsoft slowly grew from basic probability word-matching to a more complex system that could recognize words that were spelled correctly but didn’t suit a sentence and then eventually learning from a specific user errors as well as those of all users.

Along the way, Microsoft also added grammar checks, which started with basic corrections before moving to stylistic suggestions.

Microsoft’s Clippy, which debuted in 1996, was not a popular product, but it was a pioneer in digital assistants and using Natural Language Processing to infer what users were attempting to do in order to provide advance recommendations.

Though Clippy was removed from Microsoft’s Office Suite in 2007, the very investments behind Clippy powered Microsoft’s far more successful features, such as predictive data entry (Excel drag and fill), as well as formatting and template suggestions in Word, Mail, and PowerPoint.

OpenAI Partnership

By the 2020s, it’s likely that no company had invested more in AI than Microsoft. Still, the company’s executives had begun to fear that it was falling behind similar to the case in smartphones.

We can see this from the 2019 emails released to the public in 2024 following antitrust lawsuits.

Microsoft’s CTO (Kevin Scott), CFO (Amy Hood), CEO (Satya Nadella), and founder (Gates) express in detail this very fear.

Microsoft’s epiphany was prompted by work to better understand how Google’s parallel bets were bringing together its largely disconnected internal AI initiatives, the most notable are Google Brain and Deep Mind, as well as the advances of OpenAI, which had been founded only 4 years ago and had 100 employees.

Quoting from Kevin Scott’s email:

The thing that’s interesting about what they are doing is the scale of their ambition, and how that ambition is driving everywhere from datacenter design to compute silicon to networks and distributed systems architectures to numerical optimizers, compilers, programming frameworks, and the high-level abstractions that model developers have at their disposal.

When they took all of the infrastructure that they had built for large language models that we couldn’t easily replicate, I started to take things more seriously.

And as I dug in to try to understand where all of the capability gaps were between Google and us for model training, I got very, very worried.

We have very smart machine learning people in Bing, in the vision team, and in the speech team. But the core deep learning teams within each of these bigger teams are very small, and their ambitions have also been constrained, and we are multiple years behind the competition.

CEO Satya Nadella then replied:

Very good email that explains why I want us to do this deal and also why we will then ensure our infra folks execute.

The deal was a $1b investment into OpenAI, which had privately released its GPT-1 model in 2018 that was based on the transformer model that had been initially proposed by Google Brain and Google Research a year before.

Before shifting to transformers, OpenAI had invested in many alternative approaches to AI, including evolutionary algorithms and Long Short-Term Memory (LSTM). As part of its investment, Microsoft also granted OpenAI free access to its Bing search database, which was used to train GPT models.

Between 2020 and 2022, Microsoft invested another $2b into OpenAI while continuing to scale its internal teams. In 2021, Microsoft announced its second-largest acquisition ever, spending $20b to acquire Nuance Communications, whose engine was the foundation of Apple’s Siri and also a healthcare-specific AI.

Despite Microsoft’s various efforts, Nadella remained dissatisfied. By December 2022, he concluded that the models developed by OpenAI’s 250-person team (GPT-3.5, GPT-4) had surpassed those of Microsoft Research. Barely a month later, Microsoft invested $10b into OpenAI in exchange for 49% ownership stake in the company as well as 75% of profits until that $10b is recouped (and 49% thereafter, to an unknown cap), in exchange for broad rights to incorporate its technologies into Microsoft’s own offerings.

Only two weeks after Microsoft’s OpenAI investment, they co-branded the search engine as “BingChat with ChatGPT-4”. That same month, Microsoft announced Copilot, a GPT-powered chatbot that would be integrated across its Office Suite and GitHub.

Three months later, Microsoft announced the end of Cortana, the virtual assistant launched by the company in 2014 following the release of Apple’s Siri (2011), Google’s Assistant (2012), and Alexa (2014).

Diversified Approach

Although Microsoft makes extensive use of ChatGPT’s branding, its products technically run on Microsoft’s own Prometheus model.

Prometheus is built on GPT-4’s foundational LLM but was subsequently fine-tuned by Microsoft using both supervised and reinforcement learning techniques. As such, Microsoft not only owns the end-user of when they use “Powered by GPT” products, as well as their related engagement/query data, they also operate part of the model itself and can, if they so choose, begin to substitute OpenAI’s products out over time.

In February 2024, Microsoft invested in Mistral, another transformer-based open sourced AI company, at a $2.5b valuation. Notably, Mistral was founded 2 months after the $10b OpenAI investment.

A month later, Microsoft struck a $650m deal with Inflection AI, a startup founded by Reid Hoffman (co-founder of LinkedIn) and Mustafa Suleyman (co-founded DeepMind, acquired by Google in 2014). As part of this deal, Microsoft not only licensed most of Inflection’s models, it also took on most of Inflection AI’s staff. For example, Suleyman became CEO of the newly announced Microsoft AI, who reports directly to Nadella.

Microsoft understands that multimodal LLMs capable of understanding and generating content across different types of data, such as text, images, and audio, can replace existing software interfaces entirely. From history, we know that the interface layer tends to be the most profitable part of the digital value chain. It’s for this reason that Microsoft chooses to control the “reinforcement learning from human feedback” data in Prometheus, rather than relay it to OpenAI.

It’s also why AI is now being shoved into anything that users can touch/see/use. Microsoft’s OpenAI partnership is both strategically brilliant and also bound to collapse.

Learning Points

Diversified strategies are best suited to businesses that have these characteristics:

1. Cash-rich.

2. Assets are a good fit but may not be configured correctly.

3. High rate of change with progress often occurring out of sight.

4. Lots of competitors.

Deployed correctly, a company can cover all of the bases while also neutralizing the existential threat of a new competitor.

Hi, I really enjoyed this writeup. I witnessed the launch of Xbox first hand from my time in the games industry, and Microsoft is willing and certainly able to invest in things they care about. The current AI investment strategy seems like a return to form. I am very interested in your take on the 'doomed to fail' partnership with OpenAI and how that plays out. They were quick to react to the turmoil at OpenAI, but perhaps they were primed for action as the email exchange you shared indicates.