Study: META & Blue Owl JV

Intro

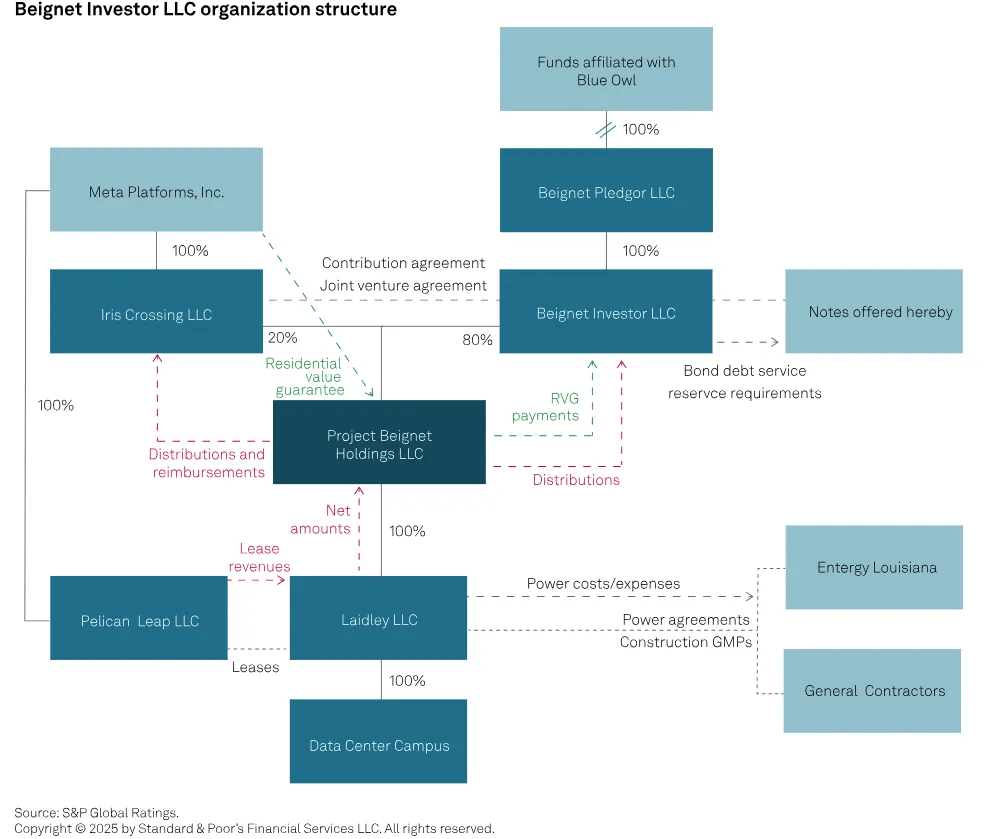

On October 21, 2025, META and Blue Owl Capital (PE firm) formed a joint venture (JV) called Beignet to fund the Hyperion datacenter construction project. The JV ownership is split 80% Blue Owl and 20% META. Total development costs is ~$27b financed through debt issued by Beignet.

This type of financing is not traditional debt where META goes out to borrow the funds needed. Instead, it’s called conduit debt financing, which is not something new, nor is it inherently problematic.

Municipal bonds have used conduit structures for decades to finance infrastructure. What makes it interesting in this current environment is the scale and speed at which this is carried out.

What is Conduit Debt Financing?

Conduit debt financing is a structure where an intermediary entity (the “conduit”) issues debt securities to investors and passes the proceeds through to an end borrower. The key feature distinguishing conduit debt from regular corporate bonds is that the conduit issuer has no substantial operations or assets beyond the financing transaction itself. The conduit is purely a pass-through vehicle, the debt repayment relies entirely on the ultimate borrower.

In our example, META wants to borrow money for Hyperion but doesn’t want the debt to appear on its balance sheet affecting its credit rating. So it works with Blue Owl, a conduit entity, which issues bonds to investors.

Blue Owl takes the borrowed capital and builds Hyperion for META. Then META enters into long-term lease agreements with Blue Owl to use Hyperion. The lease payments go to repay the debt obligations. On paper, META is just a customer making payments and not a debtor.

The main benefit for such a structure is separation. The conduit’s (Blue Owl) creditworthiness depends on the revenue stream from the end user (META). It doesn’t depend on the conduit’s own balance sheet, because it doesn’t really have anything more than being a pass-through vehicle.

This is also why conduit debt is often referred to “pass-through” financing.

A typical conduit debt transaction involves a few parties:

Conduit Entity

This entity is usually called a special purpose vehicle (SPV) which is created specifically with a narrow corporate purpose solely to issue debt, acquire specific assets, and collect payments to service that debt.

Obligor

This is the company that actually needs the capital and will ultimately be making payments to service the debt. The obligor enters into long-term agreements with the conduit with terms structured to match the debt service schedule.

Lenders

The debt comes from lenders who can be a wide range of individuals or entities. Pension funds, insurance companies, private equity, asset managers… many entities can purchase the bonds issued by the conduit. The credit risk taken is entirely on the obligor’s ability to make contractual payments.

Administrators

These are the people working for the conduit who collect payments from the obligor, passes it through to lenders, and ensures compliance. They are independent intermediaries managing the cash flows and take a fee for their work.

Structure & Implications

The main implication of this financing from META’s perspective is that operating leases don’t create a debt liability on the balance sheet (Accounting for Leases: ASC 842). The lease obligation is disclosed in footnotes (Leases and Contractual Commitments) and creates a right-of-use (ROU) asset with a corresponding ROU liability. Most importantly, it doesn’t appear as traditional debt. This can help manage leverage ratios, credit ratings etc.

Rating agencies and investors are well aware of this risk. So for conduit debt to function, certain structural features need to exist.

Bankruptcy-remote for Conduit Entity

This means that the conduit is organized in a way that makes it unlikely to go bankrupt if the obligor can’t make payments. Independent directors employed on the conduit have a fiduciary duty and cannot be compelled by the obligor to take actions that would harm lenders.

Protection for Lenders

The lenders have no claims on the conduit if things go bad, so they need assurance that payments will continue during bad times.

This can be achieved by a debt service reserve account that can cover several months of payment.

Sometimes collateralized assets and present value of lease payments can exceed the total outstanding debt by a comfortable margin.

Well-defined Credit Risk

The bond documentation needs to have necessary information needed for lenders to price the credit risk, as if the obligor were to issue the debt directly themselves. The pricing might be more stringent because lenders have fewer rights to the obligor’s assets.

Payment Obligations

The structure must state the legality of the obligor’s payment obligation. Details like these are important:

What happens if the obligor choose not to renew the leases?

What happens if the assets become obsolete?

What conditions can allow the obligor to stop payments?

Weaker conduit structures can include termination rights that transfers risk back to lenders.

META Details

The conduit financing method has become popular recently with many AI firms who need big datacenters to fuel their AI goals. META is not alone.

Tension between the need for massive capital spending on long-term infrastructure versus Wall Street’s desire for clean balance sheets have led to Big Tech reaching for non-traditional debt financing.

Below is the financing details. META owns 20% of Beignet and various Blue Owl funds control 80%. Beignet will in turn own a company called Laidley, which will own Hyperion when it’s finished and META will be a tenant.

META has committed to leasing Hyperion’s datacenters from 1 June 2029 for 5 lease periods of 4 years each (breaking up total of 20 years into 4-year pieces prevent rating agencies from categorizing it as debt).

If construction is delayed, META must still pay full leases but get credits that will be refunded gradually.

META will also cover cost overruns beyond 105% of the budget and there is a “Residual Value Guarantee” (the S&P picture above has a typo calling it “residential”) if META terminates the lease early or not renew it during the first 16 years, it has to make a capped cash payment to the JV.

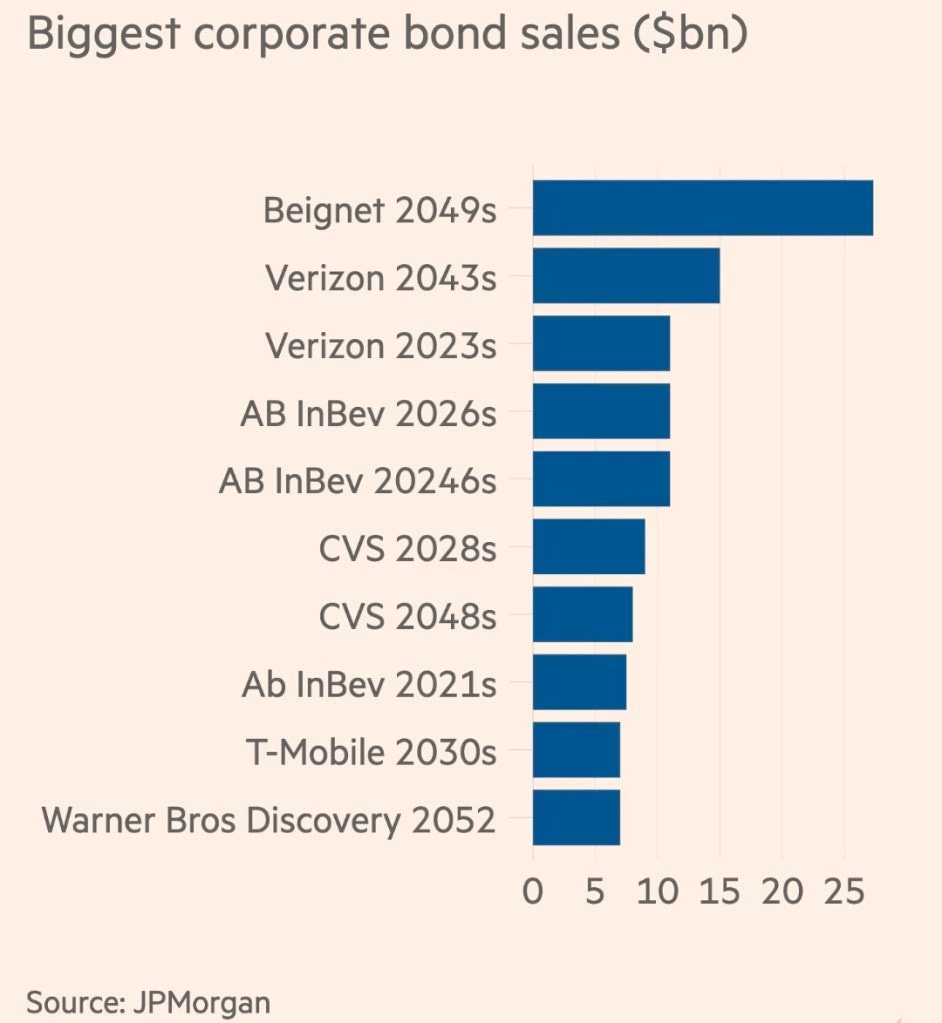

Such guarantees to Beignet resulted in S&P giving A+ credit rating, just one level below META itself. So the bankers at MS issued the record-breaking $27.3b bond priced at par with coupon of 6.58%:

The juicy coupon and solid META-backed rating sent the price of the bond up +10%.

Why META Pays More

If we look at META’s 2053 bonds, it is costing 5.44% per year, compared to this conduit debt of 6.58%. That’s ~1% difference, so financing Hyperion for 24 years (assume maturity 2049) would cost ~$6.5b (=1%*$27b*24) more than traditional corporate debt.

Why would META do this?

Well, because META knows this is just the beginning of AI buildout. They want to keep this debt off-balance sheet so that in the future when interest rates are cheaper they can borrow with a higher credit score.

The accounting treatment will show lease liabilities but it doesn’t affect debt ratios in the typical sense. We don’t know if credit rating agencies will adjust META credit rating in the future, so far nothing has changed.

xAI Example

Like we said, META is not alone in this party.

Elon Musk’s xAI is pursuing an even more aggressive version of the same playbook. In October 2025, xAI announced a $20b financing package split into ~$7.5b in equity (with Valor Equity Partners) and ~$12.5b in debt via a SPV.

The structure is remarkably similar to META: the SPV will purchase Nvidia GPUs directly, then lease them back to xAI for 5 years, with the debt secured by the GPUs rather than xAI assets. This keeps the debt off-balance sheet while the company spends about $1b per month building out its Colossus 2 datacenter in Memphis.

Nvidia contributed ~$2b in equity to the SPV while simultaneously serving as the hardware supplier.

Apollo Global Management and Diameter Capital Partners are backing the debt portion, attracted by the ~12.5% yields, although the collateral are just really GPUs.

This arrangement lets xAI access cutting-edge computing power without the full debt burden affecting its balance sheet, while Nvidia ensures steady demand and longer-term control over chip distribution.

Oracle Example

In October 2025, banks led by JPM and MUFG prepared a whopping $38b debt offering to fund 2 datacenters for Oracle in Texas and Wisconsin. The deal is structured as 2 separate senior secured credit facilities: $23.25b for Texas and $14.75b for Wisconsin.

The datacenters are being developed by Vantage Data Centers, not Oracle.

Vantage Data Centers is the conduit entity raising the debt and building the facilities, which will then be used by Oracle as part of its $500b Stargate partnership with OpenAI.

The loans are structured as interest-only during construction but begin amortizing once operations commence. Oracle gets access to massive compute capacity without the full $38b showing up as debt, while lenders get secured claims on physical datacenter assets backed by long-term contracts with Oracle/OpenAI. It’s not comforting to know that OpenAI is currently burning through tens of billions per year.

To add more leverage gunpowder, Oracle already took on $18b in corporate debt just weeks earlier in September 2025 for more datacenter buildout.

Conclusion

The scale of which these debt financing is done off-balance sheet is unprecedented:

Emboldened by the fact that META-Beignet bonds popped by +10% at the point of issuance, banks and private credit firms now are probably more comfortable with lending for AI infrastructure.

All is good if AI does deliver good returns on the investments. If not, these players are taking on significant financial risk where everyone’s balance sheet looks clean until someone can’t make their lease payments.

To end this off, we want to give a sense of how powerful is META’s Hyperion 5GW datacenter.

1GW (1,000,000kW) can:

Power 750,000 homes.

Cost $50b to $60b.

Contain $35b to $42b of Nvidia chips (~500,000 GPUs).

Now go multiply all these by 5.

Oh, and that OpenAI-Oracle Stargate project? It’s twice Hyperion!