Study: Large Deals at Constellation Software

Preface

We’re back with more Constellation Software (CSU) content! The more we dig into the details, the more we learn. This post will look into the recent 3 large acquisitions and learn how CSU navigates the problem of size.

Optimal Blue

On May 2022, Intercontinental Exchange (ICE) acquired Black Knight (BKI) with BKI selling their Empower and Optimal Blue businesses to CSU. They sold because of anti-monopoly concerns and selling to a diversified entity like CSU would satisfy the regulators.

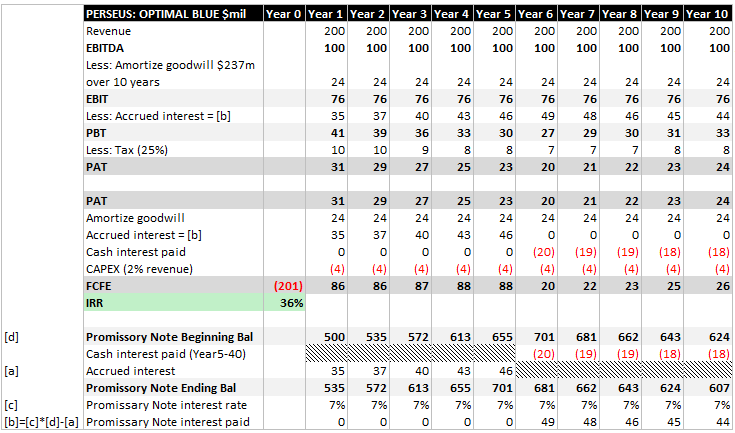

This was a large acquisition for CSU and sits within their Perseus mortgage group. But what’s amazing is that back in Feb 2019, BKI acquired 60% of Optimal Blue for $1.8b (24x forward EV/EBITDA). Then in Feb 2022, BKI acquired the remaining 40% for $2.89b (29x forward EV/EBITDA). And all of Optimal Blue was sold to CSU at $705m on July 2023, with a reported EBITDA of $100m, that would imply just 7x multiple!

Consider further that Optimal Blue grew EBITDA from $46.5m (2020) to $100m (2023), that’s above +30% CAGR. There’s even more to this deal when we examine the financing terms between CSU and BKI:

CSU only pays $200m in cash at deal closing. The remaining $500m is financed by a promissory note.

Promissory note has interest rate of 7% per year, compounded annually and payable in arrears.

The first cash interest and amortization payment is due on Year 5.

The maturity is 40 years, subject to earlier optional prepayment.

This is some ridiculously good financing terms. CSU borrowed 40-year loan at 7%, but doesn’t pay anything until Year 5. Interest will accrue until Year 5 and interest cash payments will start from Year 5 to 40.

Let’s see what kind of IRR we get from this deal.

Assumptions:

EBITDA $100m does not grow.

Cash interest paid on promissory note balance is on straight-line basis from Year 5 to 40.

CAPEX = 2% revenues.

With these assumptions we can estimate the free cashflow to equity (FCFE is levered FCF) profile. For brevity sake, we only show up to Year 10, extending up to Year 40 will improve the IRR slightly.

Because of the fantastic financing terms, we can see the power of time value of money at work. Essentially, the delayed cash interest payments are bringing forward cash flows, and results in a very high 36% IRR.

In fact, even if Optimal Blue produces zero net income after Year 5, while continuing to pay interest, the IRR is still 28%.

This would definitely pass the hurdle rates at CSU for large acquisitions.

Allscripts (renamed Altera)

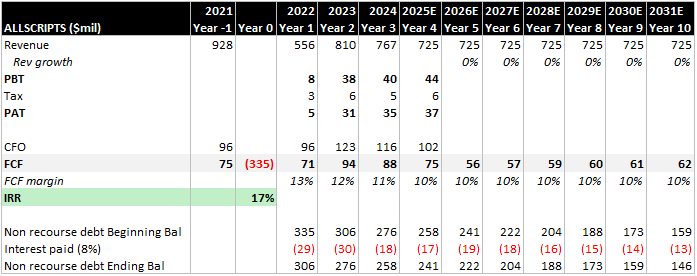

On May 2022, CSU acquired Allscripts Hospital EHR (electronic health records) business for $670m + $30m earn-out. This business has a few software solutions that play an important role in healthcare, for example, Sunrise module delivers patient records that supports in/outpatient care and supportive workflows for clinicians. This module is used by SingHealth (Singapore’s health board) across its network of hospital and clinics since 1998.

This is CSU largest ever acquisition, making up 16% of all capital deployed since 2010. The interesting thing is that Allscripts had revenues decline by -12% since 2019 and gross margins is only 35%, much lower than over 80% for CSU.

In 2021, Allscripts had revenues of $928m and EBITDA of $145m (15.7% margins). Then in 2022, it generated $71m of free cashflows, so the price paid was 10x forward FCF. This is not cheap and could not have passed the IRR hurdle rates given that Allscripts has a EBITDA margin profile in the mid-teens.

This is the first time CSU is depending on their operational expertise to turn Allscripts into a better software business. So far so good, revenues have increased and stabilized post-acquisition:

If we looked at Allscripts without operational improvements, it is indeed a “cigar butt” type investment. Mark Leonard has this comment in 2020:

In one of our declining businesses, we’ve had a wealth of talent come out of that business and go into our other business units. Some of the embedded options include knowledge of the industry, whereby you get opportunities to buy other companies that you wouldn’t have gotten if you hadn’t gotten into the industry in the first place with the cigar butt.

So not all bad… the cigar butt management look after an installed base for far longer than people expect because they provide a level of service and customization that you wouldn’t get from a normal vertical market software business. They change the lens of how they focus on the business from one of market share to one of customer share, and they just do an intense job of servicing those clients.

Effectively, CSU is buying access to the large customer base that Allscripts has, plus attempting to improve operations to lower customer attrition. In Q4 2019, Allscripts reported double the average attrition levels and announced a transformation plan; they restructured, cut costs, sold off non-core assets, and signed a deal with Azure cloud. Two years later, CSU felt that Allscripts had corrected enough errors for them to take over.

Furthermore, the EHR market is more about upselling products rather than adding new customers. We think this is the main opportunity that CSU management wants to capture.

Another thing we need to consider when forecasting IRR is that CSU financed the $670m with $335m cash and $335m non-recourse debt. This will help the IRR due to leverage.

Assumptions:

Zero revenue growth going forward due to failure to improve operations/upsell.

FCF margin unchanged at 10%.

Interest on non-recourse debt = 8% (estimated from balance sheet changes).

Not a bad outcome with levered IRR of 17% for a “no growth” scenario.

WideOrbit

We leave the most complex one for last.

The acquisition of WideOrbit was a big one at $490m in 2022, it was done together with the spin-out of Lumine, which at this point in time had historical average deal size of only $12m. Note that Lumine is a vertical specifically for communications & media businesses within the Operating Group Volaris, which is a horizontal with many different verticals under it.

So what’s the rationale for financing a big acquisition with spin-outs? Mark Miller commented on this in the 2022 AGM:

Usually, a spin out an opportunity to buy a very significant company, one that we couldn't justify if we were buying it for cash. And so what we're doing is we're putting in some cash and we're using the shares of the spin-off as partial payment.

Another reason is focus and smaller scale. Lumine as a smaller, focused VMS acquirer can grow faster while still benefiting from CSU database of targets. Since CSU owns 61% of fully diluted Lumine shares and retains super-voting rights, it has the incentives to share acquisition targets that fit Lumine’s portfolio.

Therefore, to understand the WideOrbit deal, we have to first study Lumine.

David Nyland joined Volaris in 2014 and founded the “communications & media” vertical. Eventually, the distinct brand name Lumine was created in 2020 with David as the CEO.

The organization structure under David is made up of a few Group Leaders, each responsible for a collection of business units. In typical CSU fashion, most of these managers were CEOs of previous acquisitions.

David Sharpley was CEO of Incognito (Lumine’s first acquisition, 2014).

Jonas Svenson was CEO of Netadmin which was acquired in 2015.

If you look at the customers that Lumine serves, they are actually big enterprises relative to the average CSU customer.

Incognito has more than 200 customers across North America, Europe, Asia, LATAM.

Tarantula sells to American Tower, Motorola, Telia…

Avance Metering has more than 80 customers mainly in the Nordics.

Velocix sells to Telus (27% share Canadian wireless market), Liberty Global (controls 100% of Telenet in Belgium), Proximus (45% of Belgium’s broadband market), Entel (48% of Chile’s 5G market).

VAS-X sells to some of the largest telcos in South Africa including Vodacom, who has been a customer for over 20 years.

We can expect more competition in the larger enterprise space and given that bulk of Lumine’s revenues are from a few customers, there’s a chance that competitors are able to hurt Lumine significantly. However, larger sized customers would also have bigger budgets and when mission-critical software is a small portion of total expenses, these customers are likely to stay with Lumine.

Lumine’s portfolio (before WideOrbit) is heavily skewed to recurring revenues (75% of sales). The remainder is mainly professional services which are likely a function of installing new modules. The EBITDA margins are about 30% with very little CAPEX requirements, so free cashflows margins are also in the same range.

Now, with this background in mind, let’s look at WideOrbit. The company was founded by Eric Mathewson in 1999, he built a software that ran the advertising system for local broadcast TV and radio from start to end.

It covered everything from order entry, inventories, programming, AP/AR, reporting etc. These functions are sold in modules and the entire software ecosystem acted like an “operating system”.

Over time WideOrbit grew larger and now serves national cable networks like NBC, CBS, Fox, Paramount… In 2018, Mathewson indicated that WideOrbit was used by 90% of local TV stations in the US, 50% of local radio and 30% of national cable networks.

They also created a marketplace called WO Marketplace which aggregated broadcaster inventory for advertisers to place ads. Then they integrated this with ZingX, where agencies can set budgets and automatically optimize with WO Marketplace’s inventories, there are tools that help target specific markets, analytics for ads impression data, and streamlined payments consolidating across multiple stations.

On their revenue split, in 2022, the marketplace segment only contributed 3% while the software licenses was 90%. Starting from a low base, the marketplace growth rates are the highest (+98% YOY).

WideOrbit claims to manage over $37b in advertising revenue annually, if that is accurate, then their total revenue of $167m (2021) is only 0.45% take-rate. A 0.5% increase in take-rate would double the revenues without incremental cost, which means most of the profits converts to cash. Furthermore, they could capture even more of this incremental revenues through their marketplace growth.

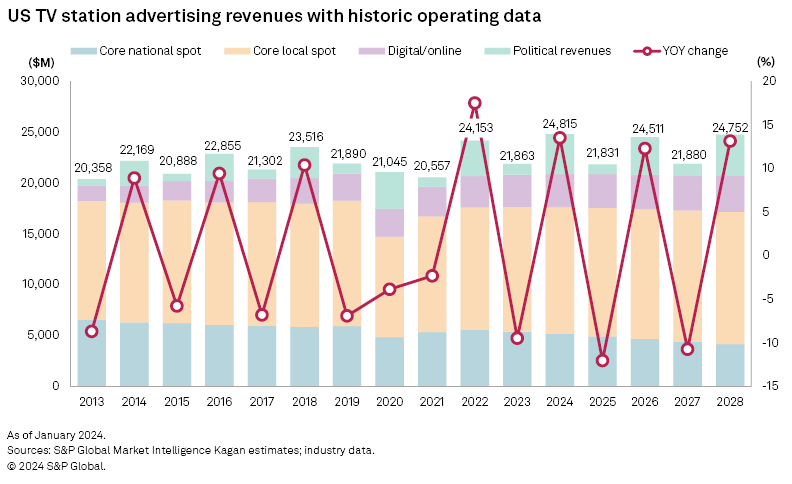

Surprisingly, local TV/radio ads are quite resilient in the US:

Put together, WideOrbit is a resilient, predictable cash flow business, with future potential of higher take-rates and ads marketplace.

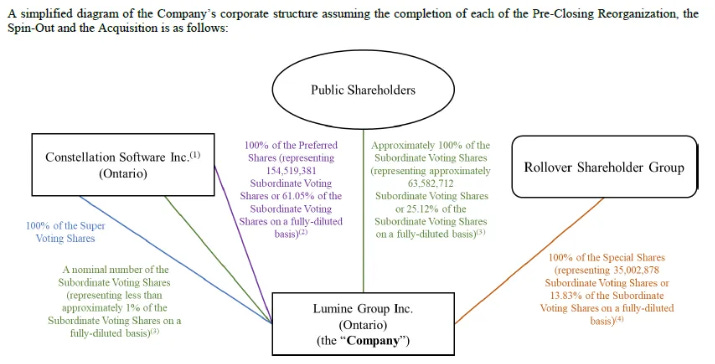

Now, back to the Lumine spin-out, the shareholder structure looked like this:

Since Lumine paid $490m as total consideration, the valuation for WideOrbit is $1.6b. This $490m was financed by $222m in shares + $180m in cash + $87m in debt.

These are the transaction details:

CSU spins out shares of Lumine as dividend in-kind. CSU shareholders receive 63.6 million subordinate voting shares in Lumine, this are the common shares.

Owners of WideOrbit (Rollover Group) will receive 10.2 million Special Shares, which are convertible to cash or subordinate voting shares. By allowing sellers to roll their equity into a new public vehicle, they can take advantage of the public vs. private market valuation.

CSU issues 63.6 million Preferred Shares, which are convertible to cash or subordinate voting shares.

CSU receives 1 Super Voting Share with 50.1% voting power as long as they retain minimum 15% subordinate voting shares on a fully diluted basis.

Special Shares convert to subordinate voting shares at ratio 3.4:1.

Preferred Shares convert to subordinate voting shares at ratio 2.4:1.

Mandatory conversion date for all Special and Preferred Shares is March 25, 2024.

Add them all up, we get fully diluted subordinate voting share count of 253.1 million. On fully diluted basis:

CSU 80.6% voting rights, 61.1% economic rights.

Public 12.5% voting rights, 25.1% economic rights.

Rollover Group 6.9% voting rights, 13.8% economic rights.

There are dividends paid on Special & Preferred Shares of $87m, but it was announced that Lumine will pay out by issuing additional 3.5 million subordinate voting shares rather than cash.

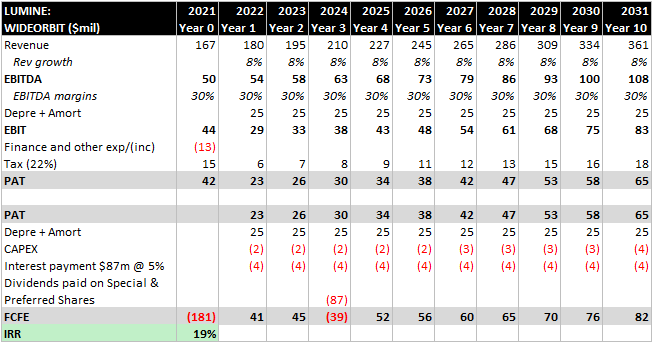

Let’s model WideOrbit’s IRR with assumptions:

Organic growth 8% and EBITDA margins 30% same as pre-acquisition.

Cash paid $181m against net assets -$68.9m, goodwill of $250m amortized over 10 years.

CAPEX = 1% revenues.

Dividends payout $87m for Special & Preferred Shares in Year 2024.

As mentioned earlier, we actually know that the $87m dividends were not paid out as cash but shares were issued at C$33.66 on March 25, 2024. This move on hindsight was brilliant because the shares were quite expensive. Free cashflow (FCF) for 2023 was C$122m but market cap was C$8.6b, that’s a 70x FCF multiple! Today, shares are trading at C$22.4.

Next, let’s consider some important strategic reasons why CSU wanted to do Lumine spin-out.

The most important reason is to keep their decentralized structure, which happens to be the biggest advantages that CSU has. Keeping individual business units (BU) on “human-scale” is the secret behind CSU success. Mark Leonard explains it best:

When a VMS business is small, its manager usually has five or six functional managers to work with: Marketing & Sales, Research & Development ("R&D"), Professional Services, Maintenance & Support and General & Administration.

Each of those functional managers starts off heading a single working group. If the business leader is smart, energetic and has integrity, these tend to be halcyon days. All the employees know each other, and if a team member isn't trusted and pulling his weight, he tends to get weeded-out. If employees are talented, they can be quirky, as long as they are working for the greater good of the business.

Priorities are clear, systems haven't had time to metastasise, rules are few, trust and communication are high, and the focus tends to be on how to increase the size of the pie, not how it gets divided.

That's how I remember my favourite venture investments when I was a venture capitalist, and it's how I remember many of the early acquisitions.

And he goes on to describe how bureaucracy creeps in…

[…] A new level of middle managers will be born, with all the potential for overhead creation, politics, and bureaucracy that comes with another tier of middle managers. The larger a business gets, the more difficult it becomes to manage, and the more policies, procedures, systems, rules and regulations are generated to handle the growing complexity. Talented people get frustrated, innovation suffers, and the focus shifts from customers and markets to internal communication, cost control, and rule enforcement.

The quirky but talented rarely survive in this environment. A huge body of academic research confirms that complexity and co-ordination effort increase at a much faster rate than headcount in a growing organisation. If the BU is small enough, and has a competent BU manager who has several years experience in the vertical, and good functional managers, then he/she will be able to cope with complexity for a while, making the right calls to optimise organic growth as the business grows.

The challenge of running a BU of this size is human-scaled.

He gives an example on high performance conglomerates (HPC):

One of the HPC’s that we studied was Illinois Tool Works (ITW). It has hundreds of BU’s. We began following the company from afar in 2005. The most relevant period in ITW’s history for CSU was the tenure of John Nichols.

Nichols began consulting to ITW in 1979, and appears to have been the primary author of its decentralisation strategy. He was CEO as the company went from $369 million in revenues in 1981 to $4.2 billion in 1995 ($6.7 billion in today’s dollars).

Prior to Nichols's tenure, ITW had acquired only 3 businesses. During his tenure, ITW aggressively acquired and often split the larger acquisitions into smaller BU’s. ITW had 365 separate operating units by 1996 when Nichols retired. I’m sorry I didn’t reach out to some of the ITW employees and ex-employees until 2015. When I did talk with one of the senior managers, he said (I’m paraphrasing) “Something wonderful happens when you spin off a new business unit.” … “With a clean sheet of paper, the leader only takes those he needs. They set up in an open office with good communication and no overheads. They cover for each other. They leave all the bureaucracy and the crap behind”.

I did record a couple of verbatim quotes from that conversation: “Don't share sales, R&D, HR, etc. because the accountants never get the allocations right and the business units always treat the allocated costs as outside their control”, and “When you get big you lose entrepreneurship”

The second reason is maintaining financial alignment. As the number of BUs increases, the link between individual BU performance gets weaker, to the point that a high performing BU performance is drown out at group level. If those managers own CSU stock and they do well, it doesn’t necessarily translate into like-for-like compensation.

Spinning out Lumine addresses both of these reasons where they can operate at smaller scale, and employees can directly invest in Lumine’s shares.

Conclusion

To close this off, we think that the Lumine spin-off highlights CSU’s ability to roll up small VMS businesses and attach themselves to a larger company under the same vertical industry.

Where else can we find a company with 100+ verticals, 800+ small VMS businesses that can readily be spun out to finance a larger acquisition?

From the 3 case studies above, we have seen the creative ways CSU have structured their deals to produce high IRRs. We think this is quite an achievement that CSU can still perform well with larger deals, while still adding on small deals every year. This creates a “pool of resources” which CSU can use as “currency” to finance future deals. Add on the reputational and expertise advantages in joining the CSU universe and we get an incredible compounding machine.

Incredible breakdown of the Optimal Blue financing structure. That 40-year note with zero payments til year 5 is basically free leverage that lets CSU pull forward all the cashflows. I ran deals like this at a PE shop once and the IRR lift from delaying payment schedules is kinda crazy, especially with compunding interest that doesnt require cash out. The 36% IRR basically means they're acquiring at what feels like 3-4x real cost.

why lumine over topicus?