Study: International Container Terminal Services (ICTSI)

Preface

ICTSI is the world’s largest independent terminal operator founded in the Philippines. The stock returned 523x since 2000 in PHP currency. That’s 28.5% CAGR for 25 years! If we calculate in terms of USD, the result is the same since USDPHP appreciated just 5% since 2003.

However, ICTSI journey has been anything but smooth…

1. It exited Syria in 2012 as the civil war escalated.

2. Its 20-year concession in Sudan, secured with an upfront payment of $500m, was unexpectedly cancelled, with the Sudanese government failing to pay them back in full.

3. In Brunei, it relinquished operations following a government policy shift to favor state-owned operations.

4. More recently, after winning the concession bid for South Africa’s first port privatisation in Durban, the South African government reversed course and withdrew.

Despite the difficulties, ICTSI has remained remarkably resilient. It has posted operating profits, net profits, and positive free cashflow every single year since 2000. It paid dividends in all but two years, grown operating profits by 15.4% CAGR over the past 25 years!

ICTSI consistently delivered good margins and efficiency, reporting EBIT margins of 53.5% in 2024 and ROE averaging 21.5% since 2000. The current market cap is US$18.4b.

History

Early Growth (1994 – 2000)

Very little is known about ICTSI founder Enrique “Ricky” Klar Razon Jr. Today, Razon oversees 4 listed firms in the Philippines. His largest holding is ICTSI which is 4 times bigger than his other 3 listed companies combined: Bloomberry Resorts, Apex Mining, and Manila Water.

For decades before ICTSI founding in 1987, Razon’s father and grandfather both managed their family business doing marine cargo. In 1977, at age 17, Razon left Bowdoin College and returned to the family’s port business, where he started at the bottom.

In a rare interview, he recalled this stage of life and mentioned he always wanted to work on a pier. His dad was disappointed with his academic decision, and he thought that the best way to change his mind was by frustrating him at work. He paid Enrique minimum wages and forced him to do tough jobs, such as operating cranes and driving forklifts.

Enrique persisted and rose through the ranks within the family business, eventually assuming leadership in 1994 following his father’s death.

Before transitioning to the CEO role, the Philippines underwent a sharp government transition in the mid-1980s led by Corazon Aquino, who sought to privatise various government-owned companies as part of her bid to shore up government finances. One of these assets was the Manila Port.

The Razon family created a new vehicle and partnered with the Soriano family of San Miguel Corp (who later sold most of their shares in 2006) and SeaLand Orient, a major shipping company (now under Maersk), to bid for the Manila port concession.

Their bid was successful, and they received a 25-year concession (1988-2013) from the Port Authority. In return, the new vehicle renamed Manila International Container Terminals (MICT), it was obligated to pay the government $550m over the concession period and invest $54m in new cargo handling equipment.

To raise capital, ICTSI went public on March 23, 1992. The early 1990s saw the privatisation of various emerging market ports, and Razon realised he was one of the few people who knew how to operate ports in emerging markets. He launched a global concession spree, and within 3 years, they acquired port concessions in Pakistan, Mexico, Argentina and Saudi Arabia.

In most of these concessions, ICTSI operated as a joint venture and took on high levels of debt for the sake of expansion.

There was intense competition for these port concessions, led by CK Hutchison, P&O (now owned by DP World), and SSA Marine. Razon was often at the port’s terminals around the clock, sleeping on his couch in the office.

Between 1994 and 2000, revenues grew from PHP1.3b to PHP9.4b, and operating profits increased from PHP429m to PHP3.4b, without significant share issuance. The growth story was explosive.

Asian Financial Crisis

Debt had swelled in the ASEAN region, and the countries had maintained fixed exchange rates, which encouraged external borrowing. ICTSI debt more than tripled to a debt/equity ratio of 246% by 2000.

Faced with financial stress, Razon had to sell assets.

In 2001, he sold the company’s international assets to its largest global competitor, CK Hutchison, for $400m.

This episode taught Razon a painful lesson in leverage and JV operations.

It marked the turn to a new approach: full port ownership where possible, reduced debt, and a focus on longer-term concessions. Its first win was a 30-year concession for the Suape Port in northeastern Brazil, followed by the concession to operate the Gdynia terminal in Poland for 20 years (currently extended to 2053).

Renewed Strategy (2001- today)

Emerging out of the crisis, ICTSI continued to operate in emerging markets. The more challenging an economic environment is, the more profitable a port can be.

First, they are less likely to compete with other ports internally, which supports existing volume growth and pricing per container.

Second, these frontier markets are more reliant on imports to support domestic consumption, which similarly increases the profitability for ports as imports generate more revenue from shipping lines than exports.

These experiences led ICTSI to pursue higher-risk concessions in Iraq and Congo, both of which became high-return investments.

There were also others that lost money, such as Syria, Sudan, and Brunei.

One bad investment was actually in a developed market: the port of Portland in Oregon, where labor challenges and strikes forced them into terminating their 25-year concession early in 2017.

On the other hand, Iraq provides a compelling case study of the potential in these high-risk countries. In 2014, ICTSI won a 26-year concession to operate and expand Iraq’s biggest and only deep-water port, Umm Qasr Port. ICTSI quickly improved its productivity, as quay crane productivity increased from 15/hour to 53/hour, while its annual capacity increased by an additional 1 million TEU (Twenty-foot Equivalent Unit, standard unit of measure for cargo capacity).

From 2001 to 2024, revenues grew from $54m to $2.7b. Interest expense/EBIT ratio improved from 53% to 25%. EBIT margins have doubled from 26% to 52%.

The Philippines Economy

To understand the context under which ICTSI operated, we can go back to its country of origin.

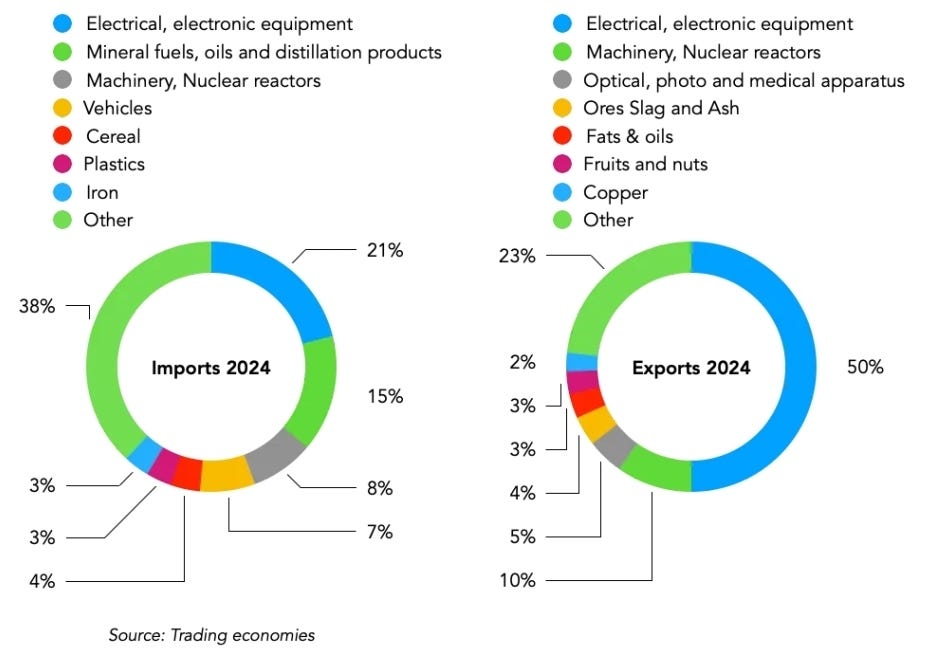

The Philippines has experienced fast growth in recent years, averaging a 5.6% 10-year GDP growth rate, the fastest among the major Southeast Asian countries. Yet on per capita income and development metrics, the Philippines lags behind its Southeast Asian peers.

As you can see, the Philippines doesn’t rank highly as a place to do business. But it’s very dependent on imports. In 2024, imports represented 40.7% of its GDP, well above the world average at 28% and 74% higher than its export value.

Electronics plays a significant role in the Philippines trading activity, accounting for half of the country’s exports. Major companies involved here include STMicroelectronics, Texas Instruments and Integrated Micro-Electronics (IMI) (subsidiary of Ayala Corp). These companies rely heavily on parts and sales to the semiconductor industries in South Korea, Japan, and China and consider the Manila port a key part of their value chain. For example, it’s estimated that Texas Instruments alone is $3b of all electronics exports in 2024.

Privatization of Manila Port

The key reason to privatize the Manila Port was to reduce the fiscal burden on the government. Other factors, such as service quality and economic liberalization, further pushed the Philippines towards privatisation. To date, the power, telecomms, water, and transportation sectors have been privatized.

PH Peso

Since the end of the 2008 GFC, a period during which the PHP lost half of its value, it has actually performed better than most emerging market currencies. PHP depreciated just 30% against the USD over this period.

There’s some fundamental reasons for this:

1. The Philippines economy is quite diverse in terms of export products and its broader economic activity. It doesn’t rely on exporting a narrow set of commodities and has non-commodity exports, such as electronics, machinery, optical and medical apparatus, representing nearly 2/3 of its total exports.

2. Overseas Filipino workers send home nearly $35b annually in remittances, the third-highest in the world after India and Mexico, accounting for around 9% of the country’s GDP. This brings a steady source of foreign currencies.

3. The Philippines is currently ranked 85th among all countries, with a debt-to-GDP ratio of 60%. The nature of its debt is mainly domestic. Foreign government debt is less than half of domestic debt, while its external debt is 31.5% of GDP, among the lowest in the world.

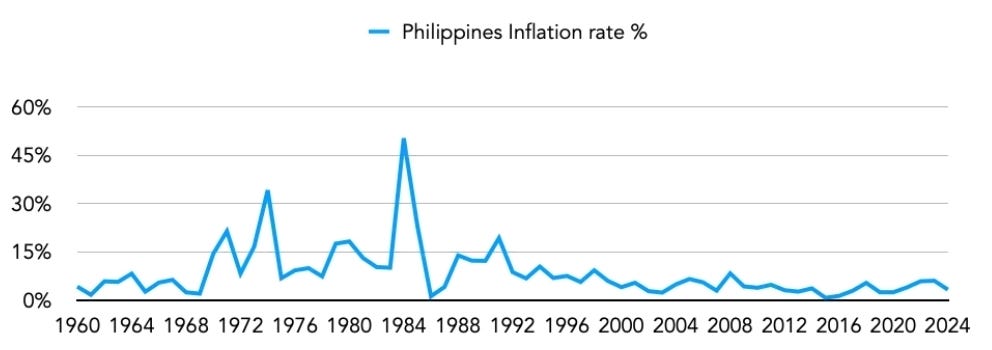

Inflation

Tied to the topic of currencies is the history of inflation:

Since 1992, its annual inflation rate has been below 10% and much less volatile than that of many other emerging economies.

There is certainly some country risk involved when looking at the Philippines, but we don’t think it’s entirely uninvestable.

Global Ports Industry

Ports often have the good qualities of being durable, defensible, and produces high margins. But few can consistently reinvest at high returns.

ICTSI stands out not just for its resilience but how it allocates capital around the world. To get into the details, let’s examine the global ports industry.

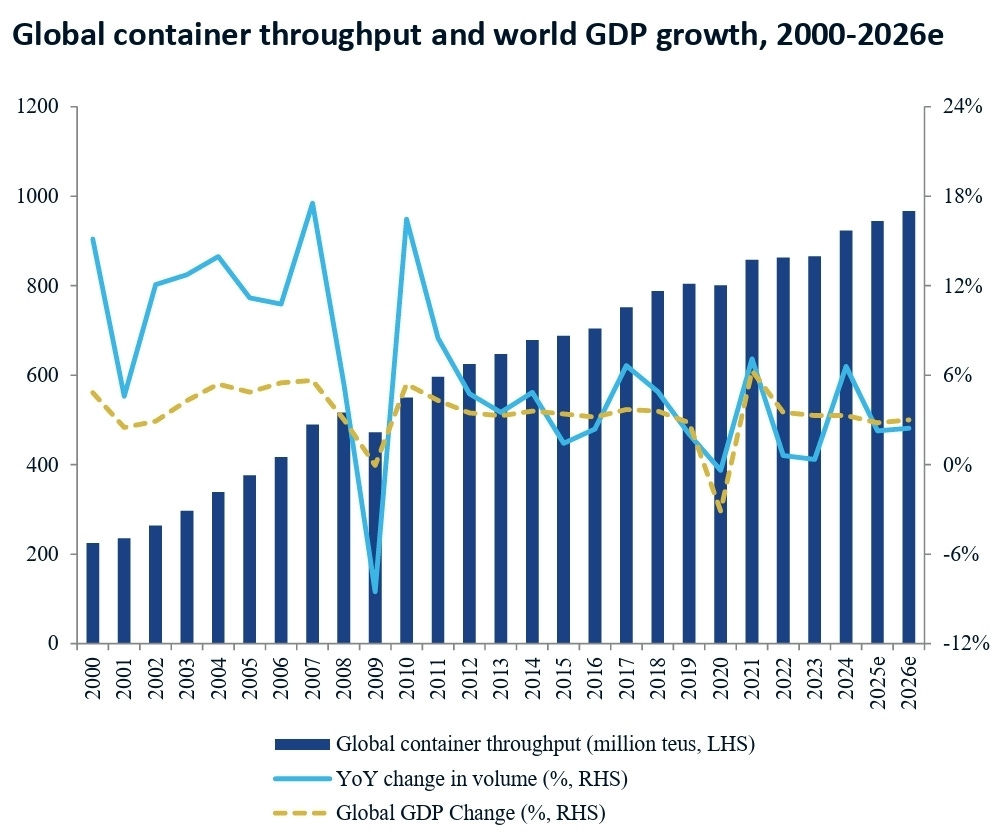

Volumes Trends

Since the advent of containerization in the 1950s, shipping port traffic has experienced growth that’s faster than the economy as a whole. Volumes (measured in TEU) have compounded at 6% since 2000.

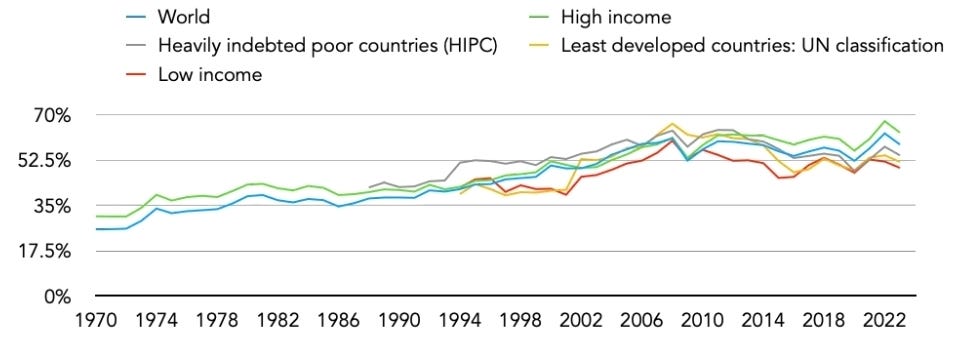

Trade as a % of global GDP has nearly doubled since 1970, a structural tailwind that benefitted port operators. The penetration is notably higher among higher-income countries compared to lower-income countries (63% versus 50%). This means that developing nations likely have room for expansion.

Lately, however, growth has slowed due to onshoring efforts among developed economies, China’s economic slowdown, and increased tariffs.

Port Economics

In global trade, ports and shipping lines form the two dominant nodes. But from an investor’s perspective, ports are structurally superior: pricing is steadier, capital outlay is longer-dated, and returns are less cyclical. In some cases, the port operators and the shipping company may be the same entity (eg. Cosco Shipping). However, there is an increasing trend for independent port operators (eg. ICTSI) to be appointed by port authorities.

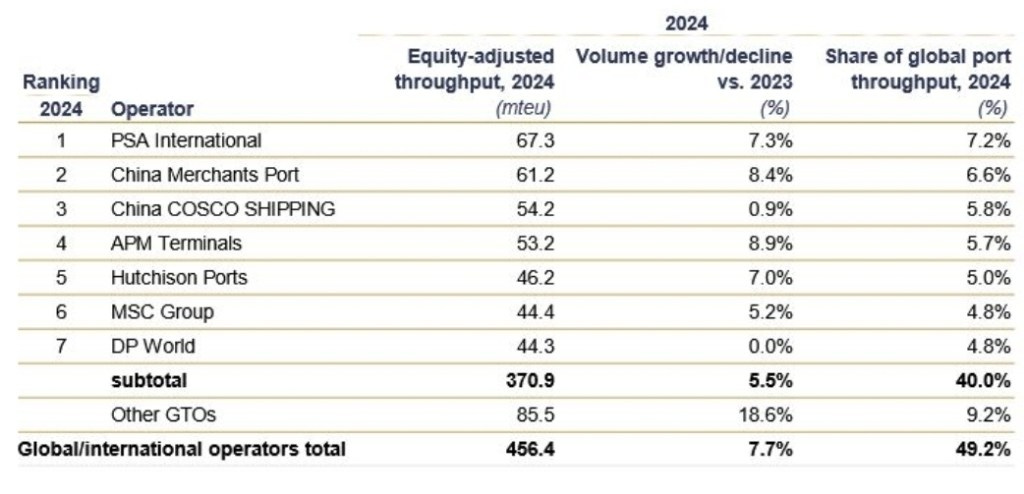

In the port industry, they have their own “Magnificent 7” which are the 7 largest ports around the world, accounting for 40% of global equity-adjusted throughput in 2024.

Looking at the scale of these top 7 operators, we can appreciate the tough environment that ICTSI has to navigate.

While ICTSI is the market leader in Philippines, on a global scale it has only a tiny ~1% share. The top 7 operators, led by Singapore’s PSA International, dominate the global port industry.

This means it is difficult to win concessions for ports. These huge operators have financial means to negotiate and put pressure on profit margins.

Outside of the 7 major players, we have a dozen of smaller ones actively trying to win concessions too. For example, CMA CGM currently manages the Nigerian Lekki Port, which ICTSI had previously withdrawn from. There’s also increased collaboration among these players. For example, Yildrim Holdings owns a 24% stake in CMA CGM and has extended its relationship, which was initially intended to last only 5 years.

Next, there is increasing vertical integration of shipping lines that own ports. Some of the fastest-growing major port operators are also key players in the shipping industry (eg. MSC, COSCO, Evergreen). This gives them increased bargaining power as they direct millions of TEU annually.

Consolidation also contributes to the competitive landscape. For example, the recent MSC-Hutchison acquisition for $22.8b is a sign that even the biggest players are consolidating together, although it seems like the deal would not materialize.

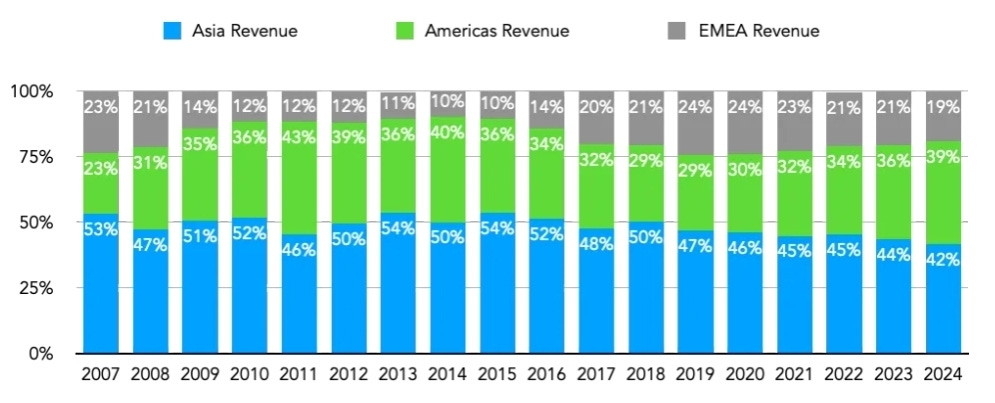

ICTSI Operating Regions

ICTSI divides its operational regions into three areas:

The Americas have shown the strongest growth, particularly Mexico and Brazil, driven by nearshoring dynamics and deepening local ties, including the appointment of regional veteran Anders Kjeldsen. Competition is also attracted to the increased appetite for port privatization. For example, CGA CGM recently acquired a 51% stake in Santos Brasil, the operator of South America’s largest container terminal.

EMEA, historically the smallest contributor, remains the most volatile due to political risk in Sudan, Nigeria, and Syria. However, ICTSI has found success in frontier markets where it holds a near-monopoly market share, such as Madagascar and Congo, and is now exploring Djibouti (June 2025).

Port Types

ICTSI primarily focuses on mid-to-large gateway ports, which are more profitable than transshipment ports (moving cargo from one vessel to another without clearing customs).

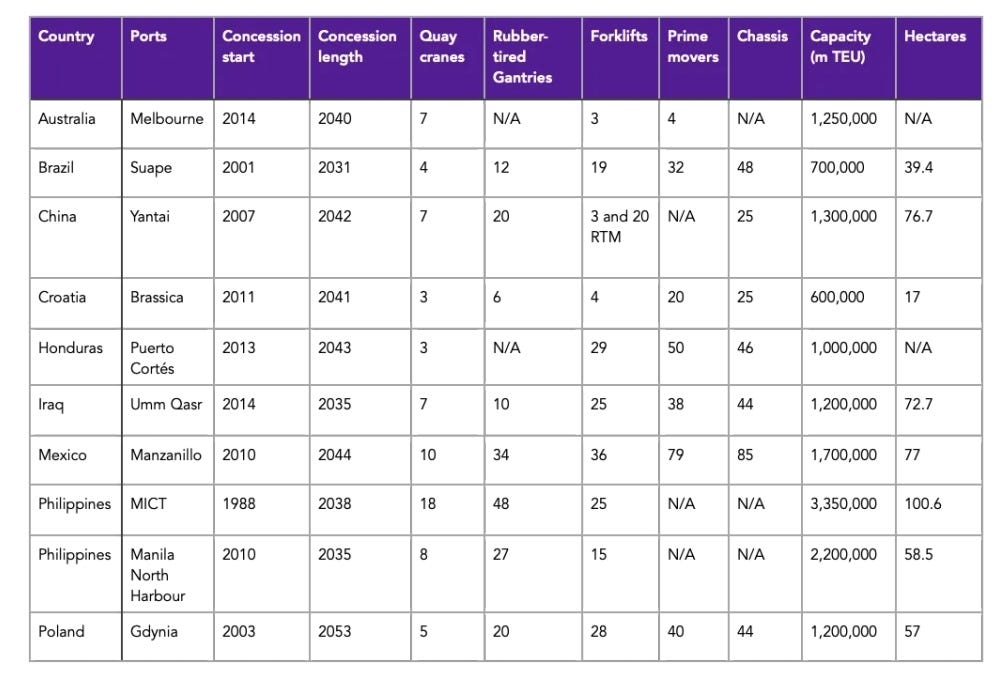

Below are the top 10 ports run by ICTSI, with their concession years, capacity and various equipment details:

The size and facilities reflect the demand in that area. The bigger the regional market, the greater the demand for port services. Thus, more investments are required to manage the port. ICTSI’s biggest port by TEU is its flagship Manila port (MICT), which currently has a capacity of 3.35 million TEUs and is expected to grow to 3.5 million TEUs.

On average, ICTSI’s top 10 ports have 15 years of concession life remaining, which is enough to secure multi-cycle cash flow visibility.

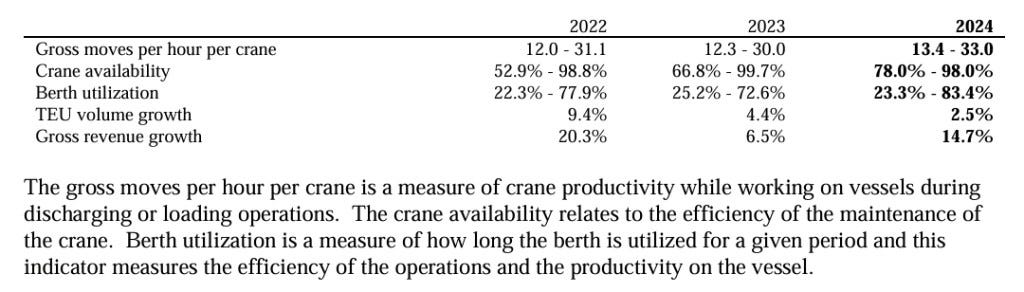

The key competitive advantage is how efficiently ICTSI runs their ports. They no longer reports this data in its accounts, but based on its last reported figures in 2019, Asia and the Americas performed significantly better than EMEA in utilisation, averaging ~60% throughput/capacity in both markets while ~50% in EMEA.

Below is the reported key efficiency indicators:

Presence in High Tier Ports

Ports can also be classified by their importance to ICTSI. They can be ranked by Tiers 1/2/3 (critical: Tier 1). Below are 17 ports across ICTSI portfolio and their importance:

A high market share in Tier 1 ports is desirable.

10 out of the 17 ports are considered Tier 1 ports: mission-critical, limited substitutes, and favorable market share. Among these Tier 1 ports, its Madagascan port in Toamasina has a 100% market share with no competitors. In other Tier 1 ports, ICTSI competes with a wide range of players.

Tier 2 mainly consists of ports where ICTSI either lacks market leadership or competes with nearby or alternative ports. In Poland, they compete with adjacent ports managed by Hutchison Ports (12% market share) and Deepwater Container Terminal (70% market share). These ports tend to be less profitable, as shipping lines often have alternatives, leaving ICTSI with less pricing power.

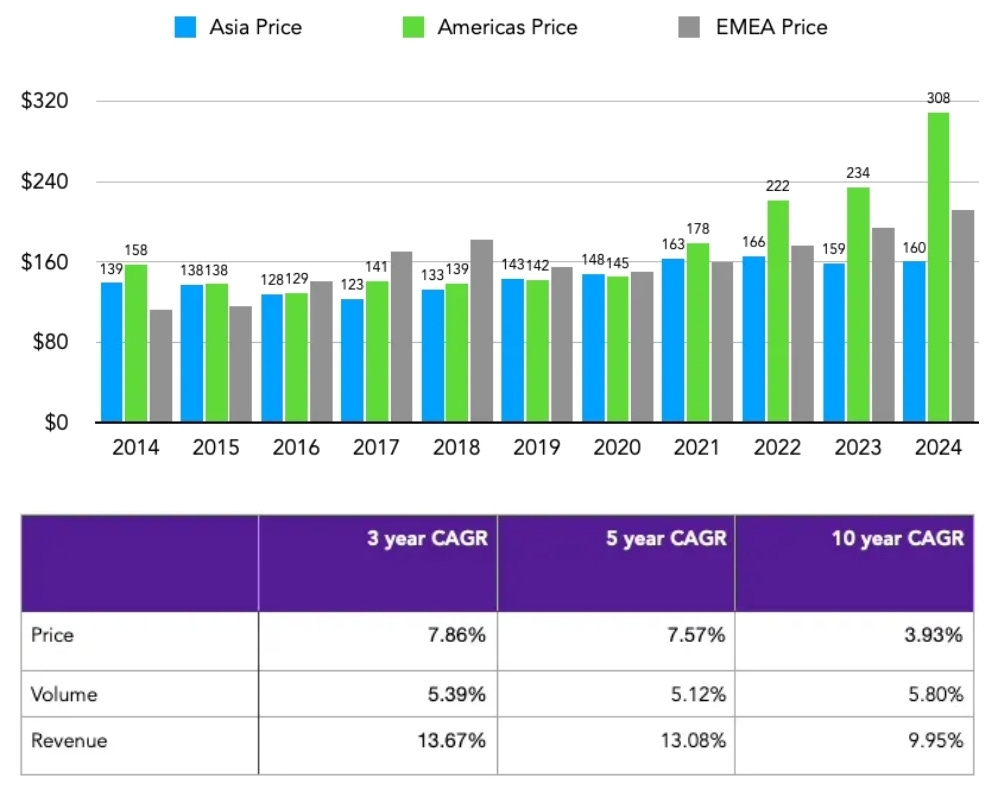

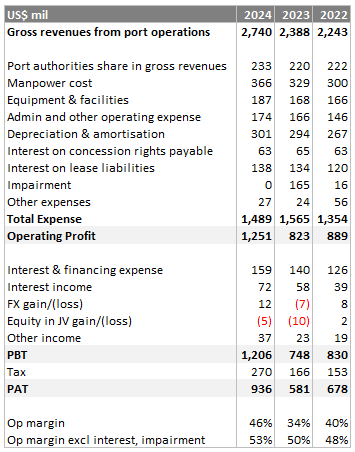

Revenues (2024: $2.5b, 2023: $2.2b)

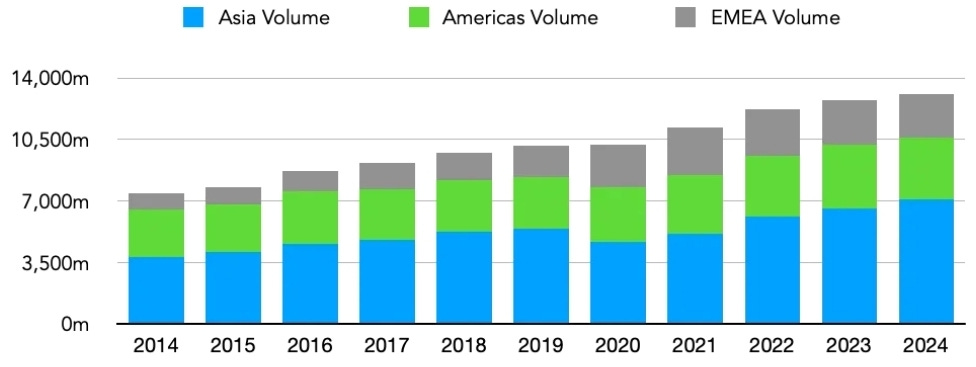

ICTSI reports volumes by region:

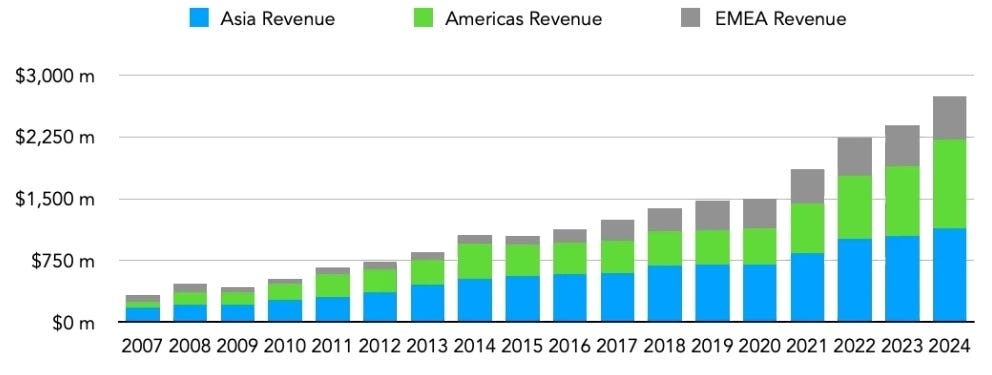

They also report net revenues by region:

With these 2 data sets, we can break down revenues into price and quantity.

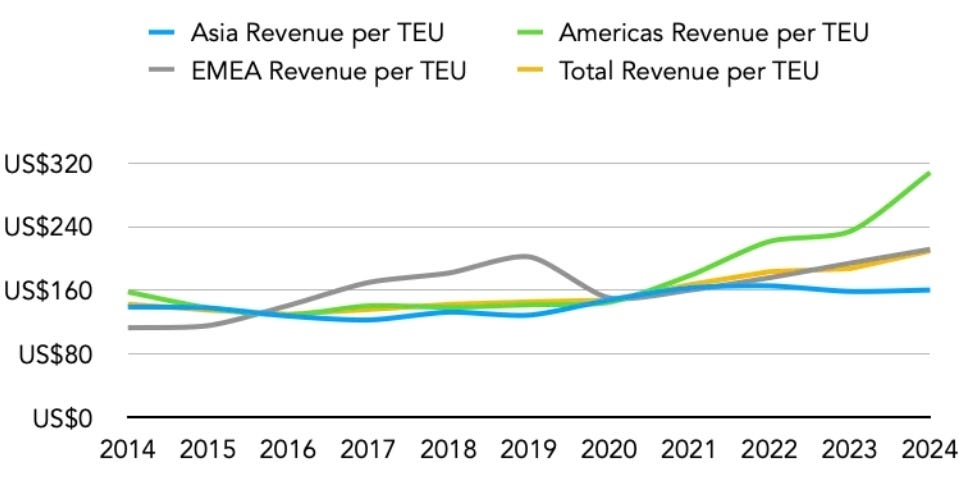

Overall, there has been a long-term trend of growth, with prices increasing by +3.9% per year across all regions.

Note 1: Revenue data includes non-containerised and passenger figures, which means the actual revenue per TEU is lower.

Note 2: The Americas region pricing increased by +26% in 2024 alone, likely due to a tariff increase in Port of Manzanillo, Mexico, but such spikes are unlikely to persist.

Those trying to model the P&L should suspect that the recent price increments cannot be sustainable.

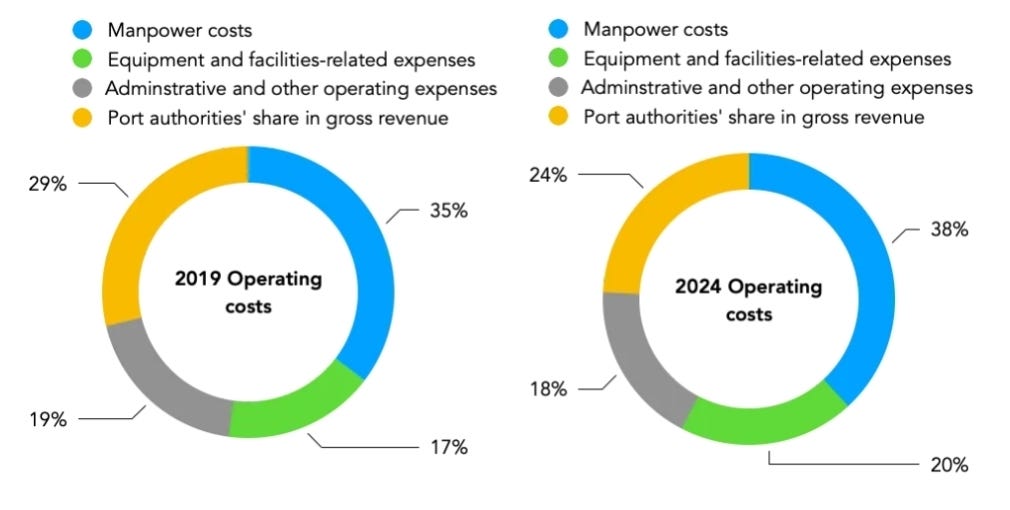

Expenses (2024: $1.4b, 2023: $1.5b)

Note: IFRS16 leases accounting reclassifies payments from annual expenses to right-of-use assets and lease liability. Expense lines before 2019 is not comparable, so we use 5 years data only.

Expenses can be split into 3 categories:

Operating costs

Depreciation

Financing cost and one-offs (eg. impairments)

Operating costs

Below is the further breakdown of operating costs between 2019 and 2024:

In many regions, port operators are subject to government mandated salary adjustments of 3-4 % per year.

Manpower costs have increased by +6% per year, driven by the addition of operations employees in ports in Brazil and Mexico and the consolidation of Manila’s North Harbour in 2022. Over the long term, both employee count and total manpower costs grow slower than revenue, resulting in margin expansion as ICTSI increases volume across its ports. We expect this trend to continue.

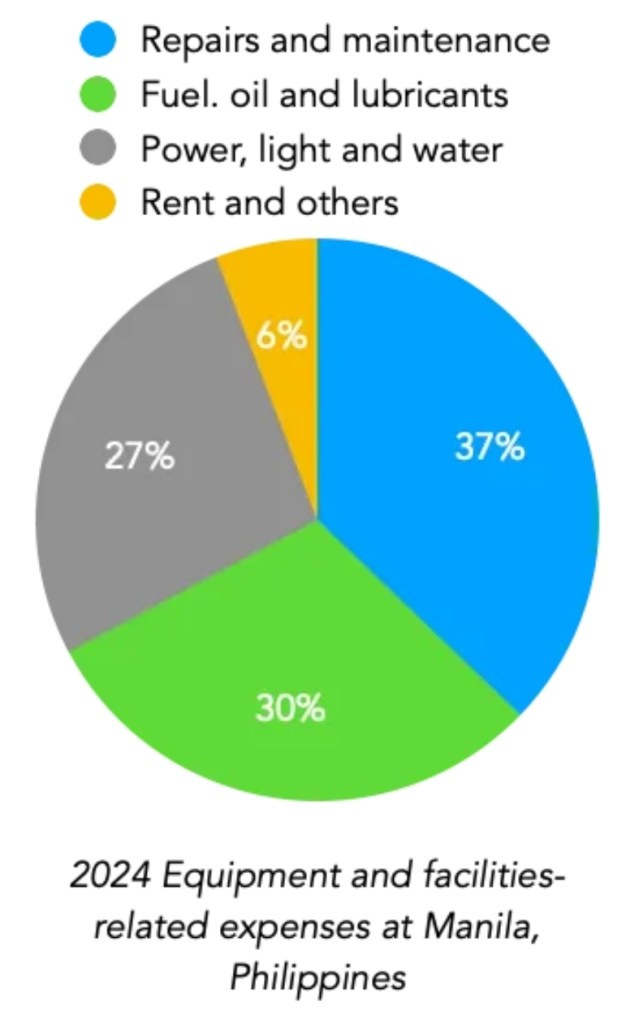

Equipment and facilities expenses are the fastest growing, reflecting the capital-intensive nature of ports. In MICT report for 2024, this segment is split into 4 further components:

Fees to port authorities can either be fixed or minimum guaranteed variable fees. Given that no significant concessions are due for renewal in the near term, this decreasing trend is expected to continue.

Depreciation

In 2024, depreciation and amortisation charges were 11% of revenues.

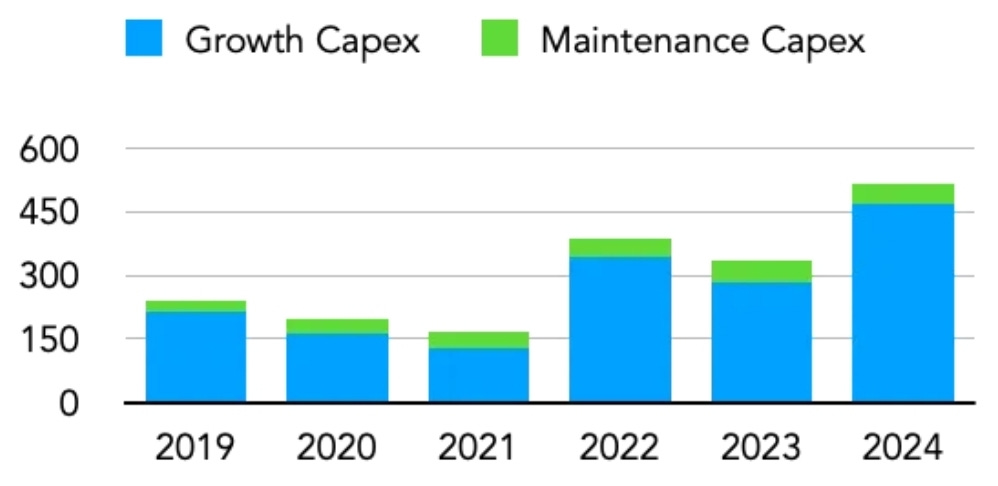

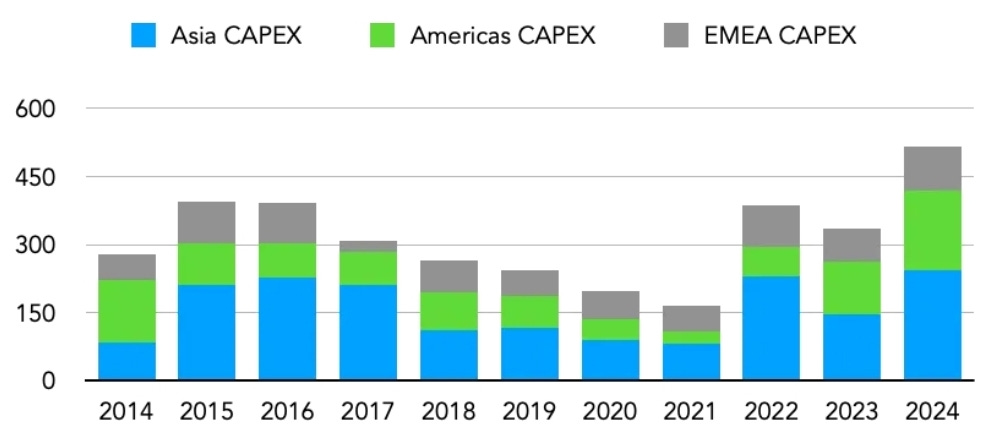

CAPEX can be categorized by 10% for maintenance, 90% for growth:

CAPEX by region shows bulk of capacity expansion is in Asia:

Port operators record the amortisation of intangible assets over the remaining years of their concession contracts with port authorities. As we approach the concession end dates, these charges decrease as a share of revenue.

For 2025, management has guided CAPEX of $580m. This is a record high figure, reflecting the expansion opportunities.

Financing & other costs

These are mainly impairment charges, interest, and lease payments. FX impact is also recorded here.

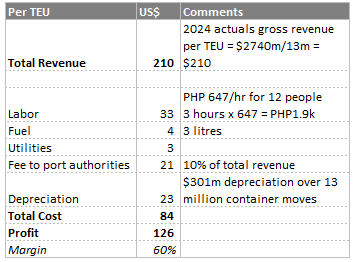

Unit Economics

We make these assumptions to model 1 TEU:

According to the reported financials, we can rearrange the P&L to get a overall 53% EBIT margin:

If our estimates are directionally correct, the economics of moving containers is a very profitable business at scale.

Growth Opportunities

As mentioned, management expects to spend a record amount on CAPEX and we want to know where are these opportunities.

Existing Capacity

ICTSI has several ports with announced capacity expansions. These investments are primarily focused on Tier 1 ports with longer concession end dates, providing an even greater return on investment. Some announced projects:

Philippines (Manila): Recently commenced construction of Berth 8 at MICT, which will add 200k TEUs and is designed for ultra-large container vessels with a capacity of up to 18k TEUs.

Philippines (Bauan, Batangas): Investing $800m to develop a 2 million TEU terminal in Southern Luzon, making it the second-largest facility in the country. Completion is expected in 2028, with the first operations in late 2027.

Australia: Install new hybrid automatic container carriers from Kalmar, increasing the port’s capacity by 20% to 1.5 million TEUs annually.

Mexico: The Port of Manzanillo’s CMSA recently added quay cranes as part of its current expansion plans to increase the port’s capacity to 2 million TEUs annually. A new berth is also expected to be completed later this year to support vessels with a 24k TEU capacity, and ICTSI has committed $300m between 2023 and 2026 to expand the port’s operations.

Poland: ICTSI recently completed Phase 1 of its reconstruction and upgrade projects at BCT, costing $42m. Once Phase 2 is completed, it’s expected to add 400k TEUs.

Technology & Efficiency

In 2021, ICTSI began migrating various ports to a unified data platform powered by Microsoft Azure. The impact of these technological improvements is primarily evident in the back end where transactions between shipping lines and ports become faster, and also in enhancing visibility for tracking or booking deliveries, resulting in efficiency gains once they arrive and depart the port.

However, not every investment necessarily has a significant impact. For example, the ICTSI app launched a couple of years ago and was expected to be utilised by truck drivers, but it continues to have a minimal impact on the overall booking and delivery system.

One of the most significant challenges for ports is congestion. It’s estimated that a 1-day increase in port dwell time can result in nearly 6 million TEUs of lost revenue globally for ports.

A recent example is the road improvements at the Port of Matadi in Congo, which handles nearly 200k annual TEUs. ICTSI is currently constructing a 2.65km road that will further link the port to the national highway network, which is expected to reduce dwell times and streamline cargo deliveries. The first phase was completed in 2024, and the second phase commenced in February of this year.

Price Hikes

Over the past decade, ICTSI has raised average revenue per TEU from $130 to $210, (+3.9% CAGR) through strategic tariff adjustments. Port operators can possess characteristics like regulated utilities where the more CAPEX they commit results in authorities allowing for price hikes.

New Concessions

Historically, ICTSI has added 1 new concession roughly every 2 years. While unpredictable, these wins tend to be margin-accretive and strategically located in underserved markets. Over a 5-year holding period, 2–3 new ports could conservatively add 5–8% to TEU capacity.

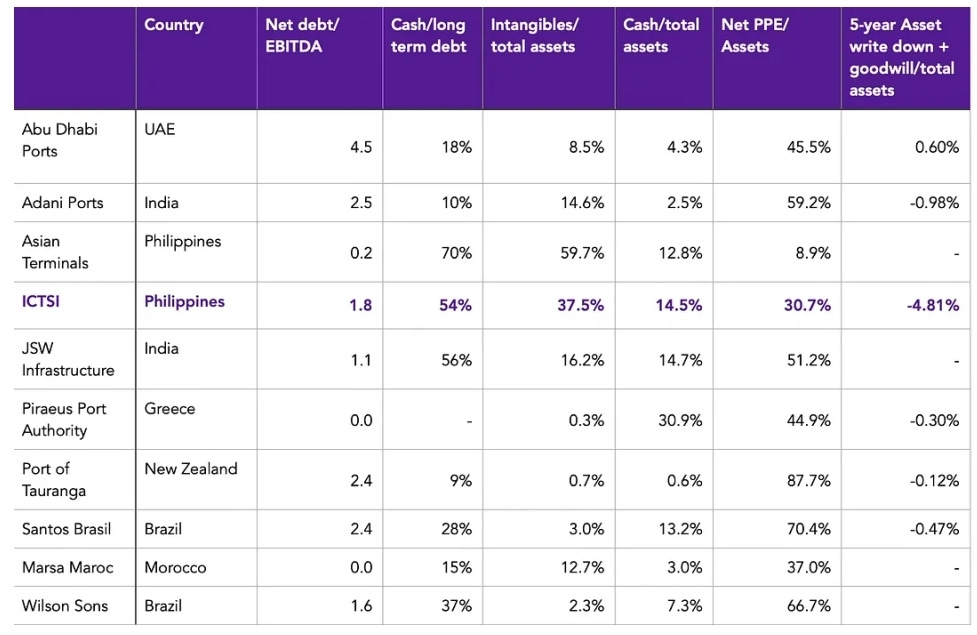

Debt & Intangibles

ICTSI reliance on concession rights means that intangible assets comprise a significant portion (37.5%) of its balance sheet, creating vulnerability if contracts are revoked or challenged.

Over the past 5 years, impairment charges were $368m (~4.8% of total assets), significantly above peers.

While its 1.8x net debt/EBITDA is reasonable, ICTSI remains more leveraged than competitors:

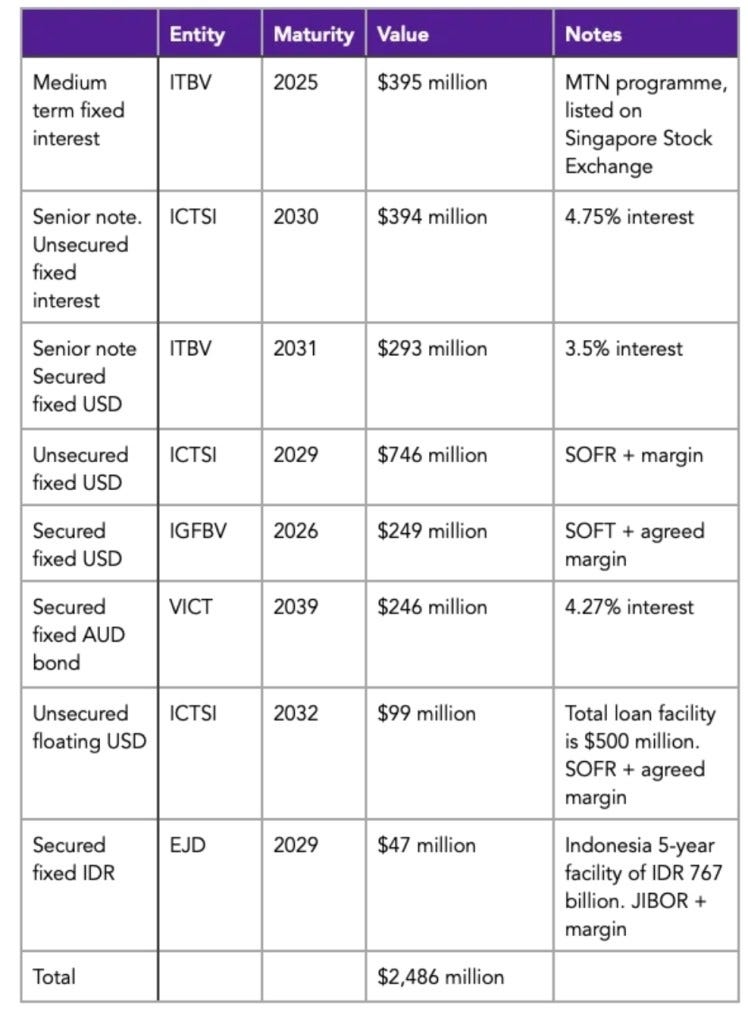

The details of their long-term debt:

Risk #1: Political

The Philippines has a history of political instability. Although it is currently experiencing more peaceful times, there is still a tail risk to investors.

ICTSI operates in several other risky countries like Congo, Georgia, Iraq, and Cameroon.

Risk #2: Currency

By operating in less developed countries, there is FX risk against USD. Fortunately, the shipping industry prefers to work with USD.

Risk #3: Tariffs

Clearly, trade is at the heart of ICTSI business. If trading is discouraged through the use of excessive tariffs, then ICTSI will also be negatively impacted.

Risk #4: Labor Unions

ICTSI has to deal with a long list of labor unions in the areas they operate. Workers going on strike is particularly harmful when operating employees make up 70% of their headcount.

1. The Asia region have renewed all their contracts.

2. The Americas and EMEA regions recorded no strikes and stoppages in recent times.

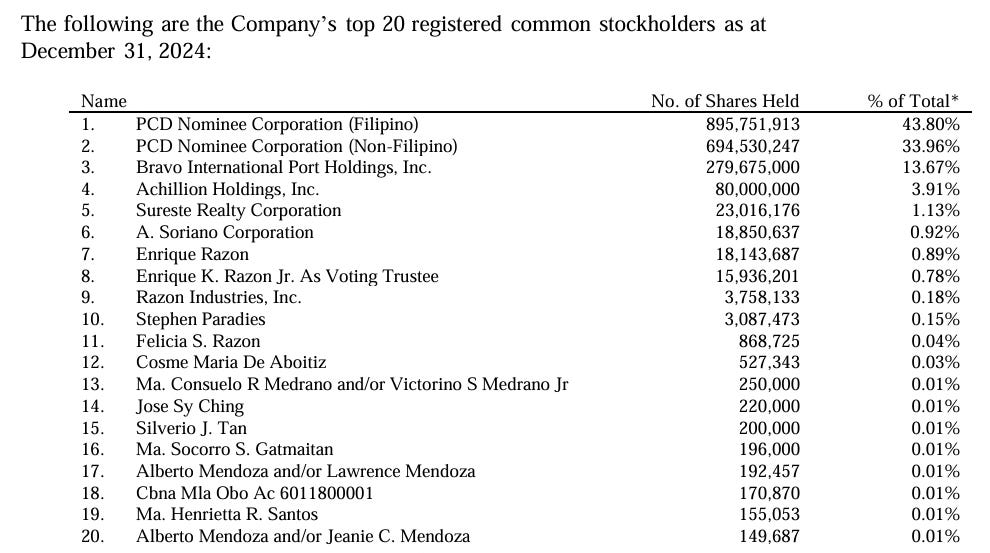

Ownership

ICTSI discloses their top 100 shareholders on their website.

Enrique Razon directly holds 34 million shares, ~1.7% ownership.

Below are the top 20 shareholders: