Study: Insurance Loss Triangles

Introduction to Loss Triangles

In this article we are going to examine the loss triangles of 3 insurers that we hold: WRB, MKL and PGR. These are high quality insurers in the auto and P&C industry, as we will see later their loss triangles are very high quality too.

But first what’s a loss triangle?

When selling an insurance product on a future liability, insurers collect premiums upfront but do not immediately pay claims. There is a future liability that insurers have to estimate (an acturary’s job). This liability goes to the balance sheet and is re-estimated every year for each “Accident Year”.

This means that if an insurer decides to report terrific earnings in any given year, they can very easily do so: either by releasing prior year reserves, or under-reserving for current year business. This can temporarily make earnings look better than they should be, but eventually the statistical claims will catch up and losses will come. Therefore, reserving is one of the key risks when thinking about insurance companies.

We can refer to loss development triangles to assess if an insurance company is estimating their future losses accurately.

When an insurer revises prior loss estimates, prior financial statements are not retroactively modified to reflect these changes. Instead, the re-estimated amount is reported in earnings over time as components of loss and loss adjustment expenses. This means that each year, the loss reserves reported may include revisions to prior estimates as well as current year developments.

Shareholders should not want to see either overly optimistic assumptions leading to cumulative deficiency or overly conservative assumptions leading to cumulative adequacy. The goal should be to estimate losses as accurately as possible. Given the uncertainty involved in estimating ultimate losses, particularly in reinsurance lines where ultimate payouts will not be known for decades, it is unrealistic to expect perfection.

The question of loss estimation accuracy is particularly important when one evaluates an insurance company based on the value of the float it generates since the main component of float is the loss reserves on the balance sheet.

Terminology

We need to define a few terms:

1. Accident Year: The calendar year that claims are incurred

2. Adequate development: In the current year, the loss reserves are lower than initially estimated

3. Deficit development: In the current year, the loss reserves are higher than initially estimated

4. Cumulative paid claims: This is the cumulative claims that are paid out for any given Accident Year

Note that figures are not discounted for time value of money.

How to Interpret Loss Triangles

We want to see that the insurance company is accurately estimating their reserves over the period that claims are typically paid out. For long tail insurance, insurers will report a 10 year period of development, while short tail insurance (eg. Auto), they report on a 5 year period. The rationale is that most of the claims would have been almost 100% paid out during this length of time.

It is impossible that acturaries accurately predict the future losses such that there is zero movement in loss reserves. Hence we expect some adequate or deficit developments when looking at the tables. But we should not see grossly inaccurate movement.

Adequate developments are always a good sign, although high levels of adequacy also means that the insurer is too conservative and losing out on the possibility of underwriting more volumes.

Deficit developments are not necessarily a bad sign. It means that year after year the insurer had to increase their reserves due to under-estimation of potential losses, however, we have to check if the cumulative paid claims actually exceed the loss reserves. If they are below the loss reserves it is okay, because it means that the actual claims cost of underwriting was still lower than estimated.

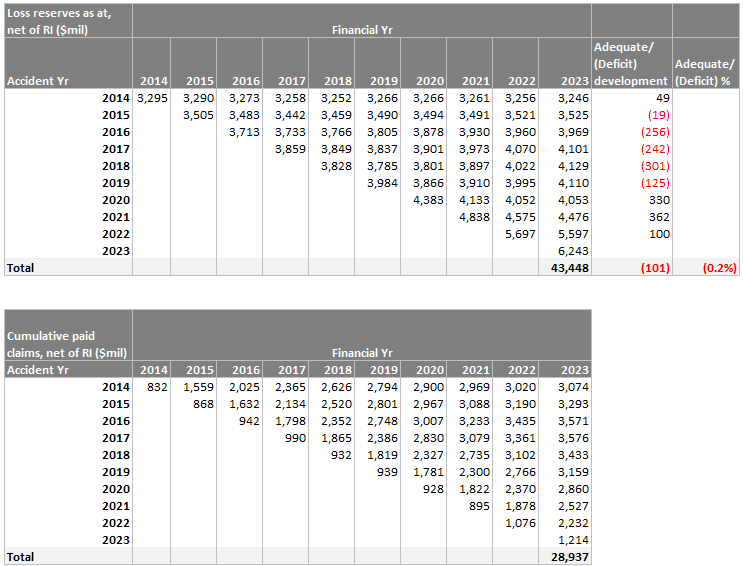

WRB Loss Triangle

On a total basis, WRB has deficit development of $101m, or -0.2% of their total reserves. This is a tiny deviation and we can say that WRB very accurately estimates the future losses, which is expected for such a disciplined underwriter; WRB recorded underwriting profits for all of the last 21 years!

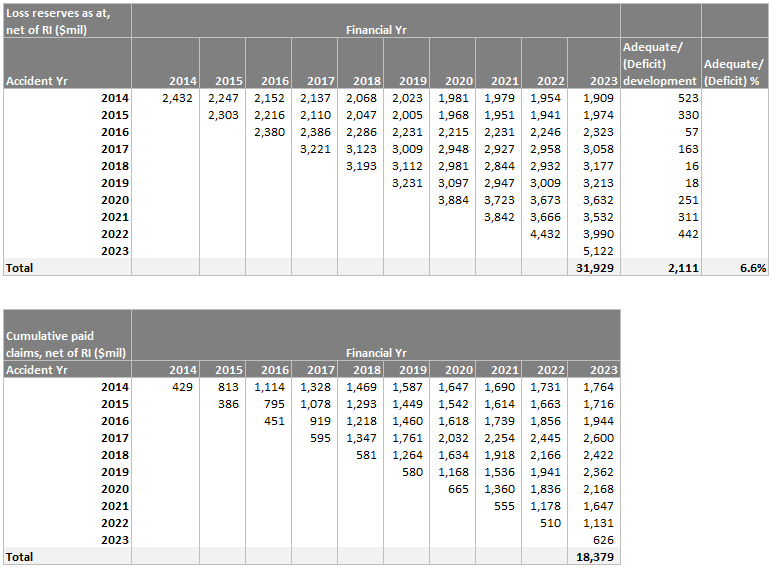

MKL Loss Triangle

MKL presents a more conservative loss reserve practice. We can see that every Accident Year’s loss reserves eventually develops to be much less in current year 2023. On total basis, MKL is 6.6% over reserved. This is a significant deviation on the conservative side.

There are reasons why MKL chooses to be conservative, because the types of insurance that MKL underwrites are very niche. For example, summer camps, horse farms, recreational boats… these risks are not easily priced and data for historical trends can prove to be insufficient. So we can understand why MKL chooses to set loss reserves conservatively.

This also means that on MKL’s balance sheet, there are liabilities from prior years that could be released. We can think of this as a buffer for difficult financial years.

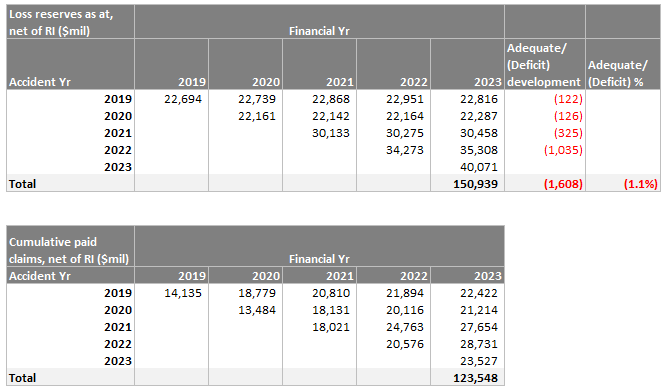

PGR Loss Triangle

PGR mainly underwrites auto insurance which are short tail in nature, when claims are incurred they are usually fully paid out by 5 years. So PGR provides us with only a 5 year table.

We can see that PGR is aggressive in loss reserving, especially in 2022 where they reported a large deficit. There are 2 reasons for this:

PGR is pursuing a growth strategy now and is taking market share. In 2022, PGR surpassed GEICO as the second largest auto insurer in America. The pursuit of volumes inevitably means that PGR will underwrite some policies that are not adequately priced.

The current unexpected inflation caused adverse deviations from initial assumptions when setting up reserves.

However on a total basis the deficit is still small at -1.1% of total reserves.

Conclusion

Insurance is a difficult and complex business in the sense that an insurer does not know the true cost of underwriting until many years later. A mispricing or under-estimation of future losses today will not show up until a few years later, which by then might be too late to salvage. Such mistakes can be costly and lead to insolvency, for example GEICO in 1970s nearly went bankrupt due to a combination of inadequate pricing and inaccurate loss reserves.

Like Warren Buffett once said, “when you have no discipline in insurance business, money comes in the door on the first day and goes out from the second day onwards”.

Loss development triangles give us the tool to check on whether the insurer is properly reserving for losses.