Study: Inflation Deflation Insurance

Causes of Inflation

The most basic explanation of where inflation comes from can be traced back to economies that transacted using physical commodities such as gold. In the absence of paper currency, there are 2 ways inflation can occur:

Demand-pull: Excess demand pulls prices higher as consumers express their confidence in the labour market due to economic expansion. This is the basis for the Phillips Curve which implies an inverse relationship between inflation and unemployment. As more workers are employed, additional demand is created and leads to upward price pressures.

Cost-push: Exogenous shocks that affect the factors of production (raw materials, labour, commodities). If we assume imperfect substitution of goods, then producers can pass the increased production cost to consumers.

In the fiat currency world, we have monetary economists who argue that inflation is caused by money supply. If central banks increase money supply without increasing aggregate demand, then inflation happens because there’s more money chasing the same amount of goods and services.

Impact on Insurers

The way the financial markets measure inflation is through changes in CPI (consumer price index). In the US, this CPI figure is published by the Bureau of Labour Statistics (BLS).

One important key to note is that CPI separates the increase in retail prices into pure price effects and additional manufacturing costs as a result of product improvement. For example, car prices in the US surpassed $50,000 in 2025, a significant increase of +32% from 2019 when average prices were closer to $38,000. But the new vehicles CPI only went from 148 to 178 (+20%).

This is because the CPI strips out the extra costs embedded in new products that reflect product upgrades. In other words, this year’s cars are not the same as those manufactured earlier. This is called hedonic regression.

However, when insurers pay claims they don’t reduce payments for car repairs to adjust for differences in quality. When technology improves and causes repair prices to go up, the insurer has to pay for the whole cost.

A better example is medical insurance. The increased claims cost for insurers are affected by improvements in medical technology, and not because the same outdated procedures are more expensive today.

Housing costs is also a good one. The CPI measures the cost of “Owners Equivalent Rent” which is the value of renting a residence and doesn’t consider the selling price of the home. Because of this, CPI did not incorporate the rapid increase in housing prices before the 2008 GFC, nor did it cater for the drop in prices after. But when home insurance claims are triggered, the payout covers the full cost of the home, including the selling price!

These disparities explains why claims cost inflation is much higher than reported CPI numbers.

Another impact is that inflation have various degrees of interaction with the economics of an insurance company that makes risk assessment complicated. For example, when an insurer experiences claims cost inflation, it can be offset by lower unemployment which can impact workers compensation claims. Low unemployment can also improve sales and retention. It can also have positive effects on an insurer equities portfolio. Therefore, effects of varying degrees leads to no clear cut answer.

To further refine the analysis, we need to think about P&C (property & casualty) versus L&H (life & health) insurers.

P&C Insurers

All P&C insurers don’t know the ultimate cost of writing a policy, they can make educated estimates, but nobody knows for sure. The difficulty lies in estimating the expected inflation. During the most recent inflation period, car manufacturers tried to minimize price increases on new vehicles, but made up the lost profits by increasing the cost of replacement parts for frequently damaged items. Since most of these repairs are covered by insurance, the consumers don’t directly feel the pain.

As a result, insurers and car manufacturers often go into disputes on using OEM parts — this is an age old problem.

Another major component is for casualty related claims. This can come in the form of workers’ compensation, homeowners or car insurance. A significant portion of medical expenses in the US are covered by government programs that impose constraints on reimbursements to medical providers.

When injury of a third-party is caused by an insured, the claimant has no incentives to control costs when almost everything is paid by the responsible party’s insurer. For example, the inflation in the 1980s caused a liability insurance crisis, it was a period of extreme premium hikes and severe coverage shortages in the US, particularly for medical malpractice, municipal, and product liability insurance.

A more recent example was Florida’s car insurance market which is among the most expensive in the US, with premiums 40% higher than national average. In 2022, a tort reform bill was passed to curb litigation cost, insurers could then reduce insurance prices and return nearly $1b in credits to policyholders.

P&C insurers who write long duration policies are also exposed to adverse development on loss reserves during inflationary periods. Loss reserves are usually set based on assumptions that historical inflation rate will continue until these claims are settled. However, this is not the case when inflation proves to be higher than assumed, such scenarios will cause reserves to be inadequate.

Most P&C insurers match their liabilities with fixed income assets. When persistently high inflation happens, central banks will raise interest rates to cool down the economy. Higher rates means lower fair value for fixed income securities, combine this with inadequate reserves we have a dangerous situation where the insurance company is forced to sell assets at a loss to pay for inflated claims — a recipe for bankruptcy.

L&H Insurers

L&H insurers are actually less affected by claims inflation because most of their products are fixed payouts. Think about your life insurance policy, it pays out a fixed amount on death or permanent disability. To satisfy consumers’ needs for inflation protection, most of these policies have an investment element which is tied to the performance of equity markets.

The impact to L&H is indirect. High inflation erodes the current value of fixed future payments, creating a disincentive to buy life policies and can increase lapse rates.

On the health side, the most common are hospitalization insurance plans. Although they are very much exposed to medical inflation cost, but they have very short renewal periods, typically 1 year. This allows insurers to re-price their products as loss experience comes through. They can do this through a combination of premium hikes and/or increased deductibles and co-insurance.

Higher interest rates caused by inflation helps life insurers as their liabilities are often much longer duration than assets. So the net effect is lower present value of liabilities, while fixed income assets get rolled over into higher yields.

Deflation

Deflation is the opposite of inflation, defined by negative inflation rates. When prices are falling, consumers are incentivized to delay consumption which causes the economy to slump further. Producers react to decreased consumption and reduces investment, leading to further decline in aggregate demand.

In such an environment, fiat currency actually increases in value over time. This means that people will be encouraged to hold on to money, resulting in a liquidity trap. The monetary solution is to reduce interest rates by increasing money supply (quantitative easing), in extreme cases pushing rates near zero, as we have seen in Japan for a long time now. But this creates a carry trade where investors sell cheap Yen to buy another country’s currency that has higher interest rates. This leads to currency devaluation and hurts foreign trade competitiveness.

Japan: Deflation Case Study

Deflation and consequently long periods of low interest rates are harmful for L&H insurers. Japan serves as a good example for the implications of deflation for life insurance companies.

Japan is recognized as the third-largest globally in terms of life insurance premiums. While the US and China lead in total premiums, Japan has an exceptionally high penetration rate, with ~90% of Japanese households holding some form of life insurance.

After WW2, life insurance companies in Japan focused on selling profit-participating savings type products through a unique sales channel of “insurance ladies”. In the early stage, this channel included widows from WW2 who wanted to earn some income for their families. Then it evolved into housewives who had little training and paid on commissions. They targeted their friends and relatives who bought life policies out of a sense of compassion rather than need.

Typical policies sold were endowment and whole life products. Fixed annuities were also popular.

The late 1980s came with Japan’s real estate bubble, confidence was high and life insurance companies issued long-term policies that guaranteed fixed interest rates of 4—6%. At this time, Japan Post Insurance was offering high rates on 10-year insurance policies.

To finance these guarantees, insurers went into the booming equities, loans and real estate market.

As we all know, the bubble burst and Japan’s life insurance companies had liabilities that they couldn’t pay. The asset portfolio yields dropped continuously from about 6.5% in 1990 to 2% in 2000. This means a negative spread between what life insurers earn and what they promised to pay out.

In 1996, Prime Minister Hashimoto announced the “Japanese Big Bang” with plans to reform the financial services market by 2001, modelled on similar reforms in the UK. Insurance regulation shifted away from the structured European insurance system followed since 1945, in favour of a more liberalised insurance market.

This introduced foreign competition and the number of life insurance companies increased from 30 in 1990 to 47 in 2000.

All these factors resulted in the first ever insolvencies of 7 life insurance companies since WW2.

The start of the new millennium in Japan was marked by deflation; continued low interest environment, further declining real estate markets and a stock market that did not recover to historical levels until only recently.

How did Japanese life insurance companies manage to overcome the challenges of deflation in an increasingly competitive environment?

Portfolio Shifts

Life insurers shifted asset allocation towards bonds, increased the duration of their bond portfolios to narrow the duration gap between liabilities and assets.

They also allocated more into foreign bonds which offer much higher rates than Japan.

Product Shifts

The product mix has shifted in various ways to transfer investment risks to policyholders:

Variable life insurance products.

Foreign currency denominated policies.

Variable annuities are popular retirement products mostly sold through banks.

Health insurance, critical illness, and long term care products.

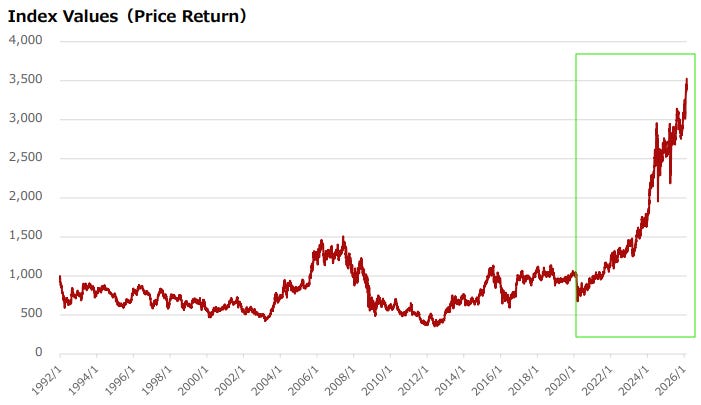

However all these actions couldn’t fight against the pressures of a deflationary economic environment characterized by declining interest rates. Look at the TOPIX Insurance index of market weighted Japanese insurers, it’s essentially flat from 1992—2020:

Now, for the last 5 years Japan has left the negative rates regime and hiked rates aggressively to combat inflation:

Guess what it does to insurance companies?

They flew up in value!

Finally, after nearly 30 years of low rates in Japan, insurers are able to see the light at the end of a long tunnel.

Thank you. For anyone interested in real-time figures, we have the Feb CPI coming up today.

Here are my Feb CPI estimates, which have, since mid-2023, been better than Wall Street 70% of the time:

https://arkominaresearch.substack.com/p/feb-2026-cpi-estimate