Study: Incentives Pitfalls

Common Misconceptions

Most investors assume that remuneration linked to an increase in earnings per share (EPS) or free cash flow per share (FCF/share) sounds fantastic. What shareholder wouldn’t want their cashflows to increase?

However, management teams can increase FCF or earnings while destroying value. Increasing such metrics does not necessarily always equate to a good thing for shareholders.

An example to Illustrate

Imagine you are the newly appointed CEO of a company. The company has a market cap of $200m and last year the profit was $5m. A few years ago, it developed a tremendously successful product that generated very high margins and returns for the company. However, it seems that the penetration boundaries might have been reached and expected future growth is very limited.

The Board of Directors hires you to find new growth segments. Your compensation and incentive scheme is as follows:

Annual basic salary $200k

Short-term incentives: Yearly bonus up to 200% of base salary based on revenue growth, EPS growth, and FCF/share growth, each of them evenly weighted and upon achievement of a particular threshold.

Long-term incentives: 400% of base salary in stock options vested over 4 years and depending on total shareholder returns (TSR) compared to an Index.

This certainly sounds like what most corporations are incentivizing. So let’s break down why such metrics can destroy value.

Pitfall #1: EPS and FCF

As the new CEO, you are tasked to produce growth and you need it quick. So usually this is what happens:

1. You design, develop, manufacture, distribute a new product.

2. You go out and acquire another company that already has a ready-to-go product.

Firstly, because you are incentivized on short-term earnings, you chose to acquire a company for quick results. Even better, you may add some debt to finance the deal to improve the returns.

Secondly, you also develop new products, but to prevent a drag on profits, you decide to under invest in CAPEX and R&D.

Lastly, to juice up the per share numbers, you use excess cash to repurchase shares.

After all these actions you would’ve achieved higher revenues, EPS and FCF per share. Moreover, you will be proud of a new product launch and lower shares outstanding; on track with everything the Board had asked for.

However, did you create value for shareholders? We simply don’t know. The only thing we know is that you have assumed more financial risk. And that’s just the plain reality. Neither revenue growth, nor EPS growth, nor FCF/share measure whether you have created value or not.

Pitfall #2: Total Shareholder Return

You might think that if those decisions mentioned above are not generating value, you would be penalized in the long run. Because the share price will not increase and you will not receive your long-term incentives.

This is typically far from the truth.

Most of the long-term incentives that are determined by TSR schemes are benchmarked to an Index, not by setting minimum returns. If the long-term incentive linked to a TSR of 15% CAGR, it would be nice, but this is almost never the case. Usually it’s referenced to a benchmark, which most of the time is not a fair comparison.

In most cases, executives will receive 100% of the incentive if the TSR is the same as the benchmark! You don’t have to outperform, it suffices to simply be like the rest. And what is even worse, in most cases, executives will receive part of their incentives even if the TSR is much lower than the benchmark.

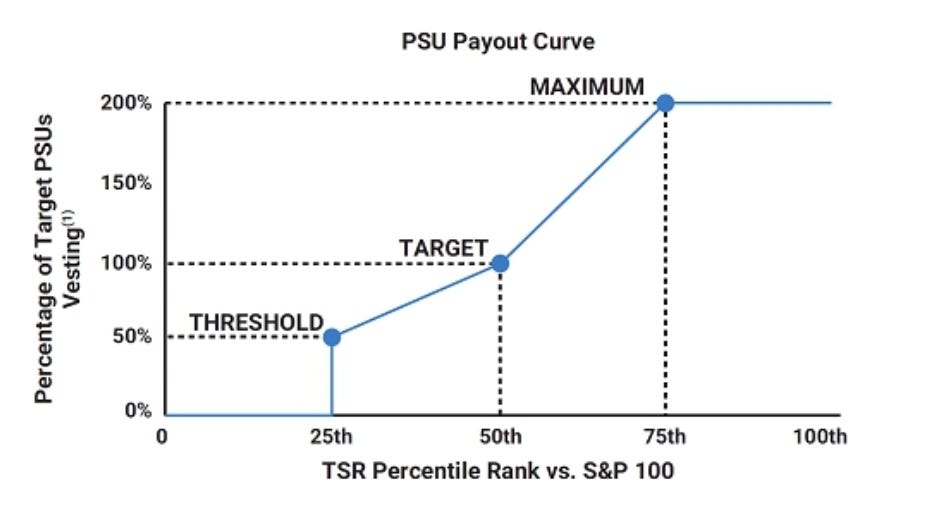

Below is an example of Alphabet’s TSR payout measured against an index:

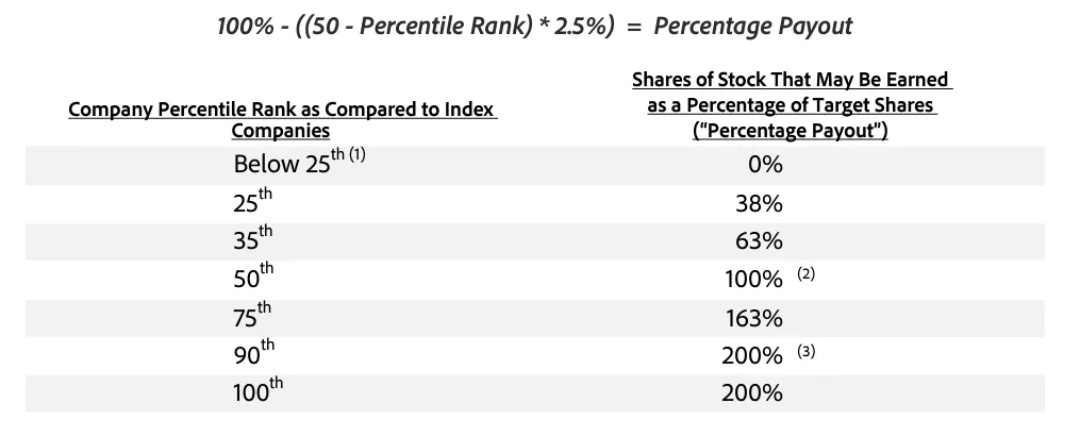

Another example from Adobe:

Pitfall #3: Return on Capital

Even metrics like ROIC can be not ideal, although it is much better than revenues and earnings. Consider the real example of NVR where they are incentivized on being the highest ROIC in their peer group.

Historically, NVR has been able to achieve this due to its asset-light model. There might be a case that NVR rejects a project that offers higher return on capital versus cost of capital. NVR could default to repurchasing shares to satisfy ROIC.

Admittedly, this gets theoretical and is quite impractical from a business point of view. To begin with, we doubt the management team engages in such short-term thinking. Otherwise NVR wouldn’t have compounded so well.

Conclusion

We can’t possibly give a list of what exactly are ideal incentives. The general principle is that it must incentivize for value creation accrued to the shareholders.

Different businesses have different value drivers for long-term results, and executives should have the best knowledge of these drivers.

Communication to shareholders about these metrics should be at the forefront of the proxy statement. Instead, we usually see hundred plus pages of theory crafting from compensation consultants. The lack of corporate governance turns us off.

To make things more difficult, we know that most management teams think about their own short-term gains, treating shareholders like a faceless crowd more than partners.

Investors must learn how to filter out such fallacies in incentives that seem beneficial but actually have the potential to destroy value.