Study: 100 Year Corporate Bonds

Alphabet Issued 100-Year Bond

You probably heard of this already, last month Alphabet, parent of Google, issued a century bond. They borrowed £1b from institutional investors, promising to pay the principal in year 2126. The coupon rate is 6.125% compared to current 30Y gilts of 5.2%.

Alphabet said that the money will be used for building AI infrastructure, planning for $175—185b of capital expenditures in 2026.

Given that Alphabet produced $165b of operating cashflows last year, it looks like some debt is required to fund their AI projects.

It helps to examine history and see who else issued 100-years bonds.

Examples of Century Bonds

These bonds sound like unicorns but they are actually not that rare.

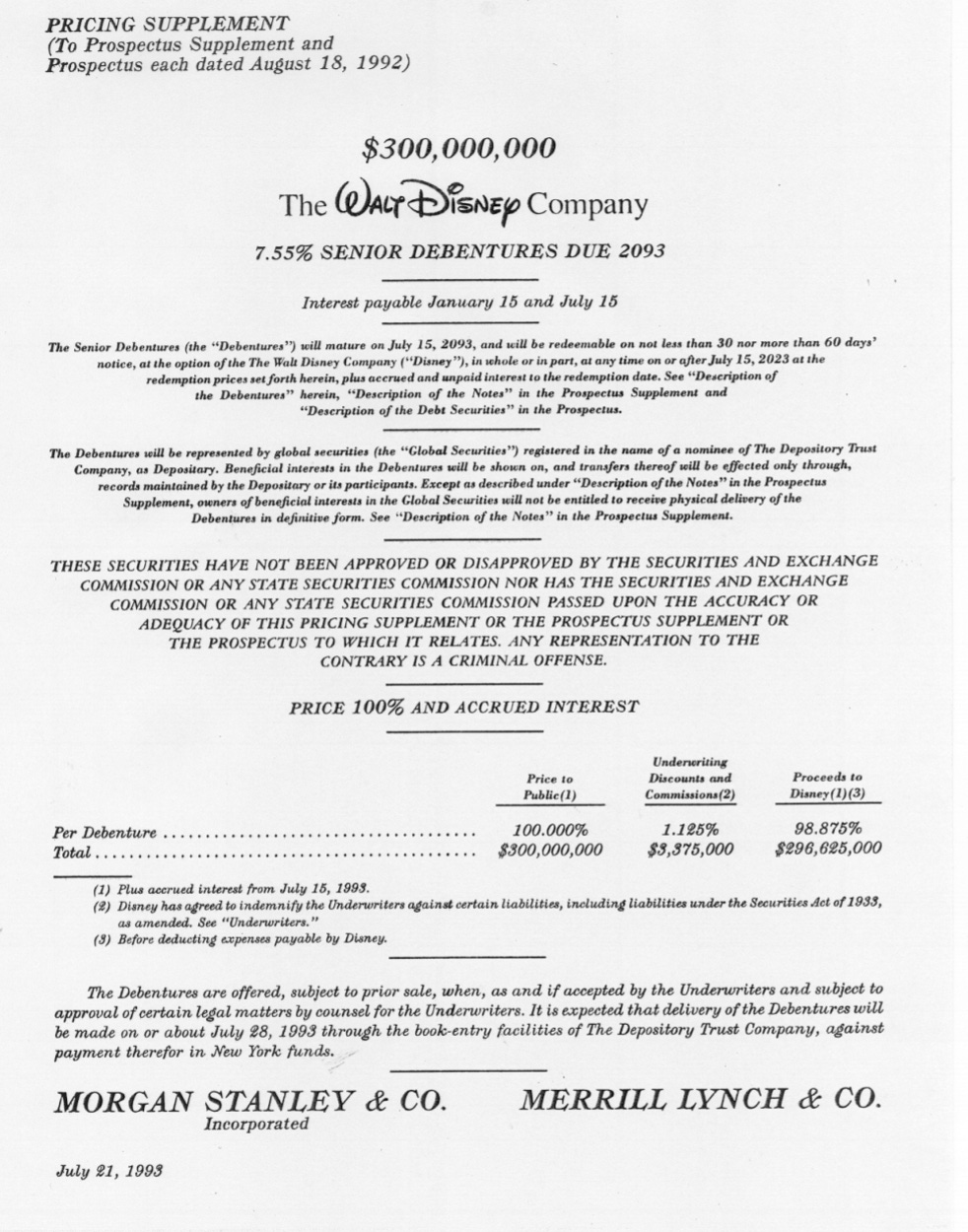

Disney (1993)

$300m, 100 years maturity, callable after 30 years.

Coupon 7.55% (30Y Treasuries 6.6%).

Called in 2023 at $103.

Total return 330%

Nicknamed “Sleeping Beauty” bonds, Disney is the gold standard: After paying 30 years of fat coupons, the bonds were called at a slight premium to par.

Coca Cola (1993)

$150m, 100 years maturity.

Coupon 7.375% (30Y Treasuries 6.6%)

Price $123.5

Total return 360%

The coke beverage invented in 1886, a company synonymous with happiness, and labelled as “The Inevitable” by Warren Buffett. In 1995, it was the 4ᵗʰ largest US company by market value and made it 2ⁿᵈ place in 1997. After 32 years, it is still quietly paying coupons.

IBM (1996)

$850m, 100 years maturity.

Coupon 7.125% (30Y Treasury 6.7%)

Price $122.5

Total return 336%

Tech giant of its time. It could issue century bonds at only 40bps above Treasuries, showing how safe the market deemed IBM's business.

In reality, IBM debt was downgraded a few times, including from A+ to A in 2018 after selling $20b of bonds to finance their RedHat deal.

Although the business went into decline, they are still making good payments on their century bond.

Norfolk Southern (1997)

$350m, 100 years maturity.

Coupon 7.9% (30Y Treasuries 6.6%)

Price $130.8

Total return 352%

This is not the first time a railroad issued century bonds. Back in 1881, Santa Fe issued 100 year bonds that finally repaid in 1995 (114 years later).

In 2023, Norfolk took a hit from the East Palestine, Ohio disaster where derailment incurred $600m of damages.

JC Penney (1997)

$500m, 100 years maturity.

Coupon 7.625% (30Y Treasuries 6.6%)

Bankruptcy in 2020

Total return 6%

Back in 1997, the markets were roaring. The Dow Jones industrial average was completing its third straight year of over 20% returns. Tech IPOs were smashing the opening bells as Amazon went public that year. The economy was expanding at a 4.4% pace. What a wonderful time.

Corporate debt markets also basked in the exuberance, even JC Penney, a retail mall business could borrow for 100 years!

Unfortunately, JC Penney went bankrupt during COVID, but debt holders did not lose money in nominal terms after 23 years of coupons.

Motorola (1997)

$300m, 100 years maturity.

Coupon 5.22% (30Y Treasuries 6.6%)?!

Price $82.4

Total return 229%

Issued at the height of Motorola’s glory years, people lending to Motorola for 100 years actually received less than lending to the US government for 30 years!

Did people think that Motorola was less risky than the risk-free rate?!

During that time, Motorola faced intense competition in the mobile phone market. They went to market with the world’s first flip phone StarTAC, weighing 95 grams and a 500mAh battery. It became a cultural icon in the 1990s:

In 1995, it was 19th most valuable US company by market cap. Motorola share price went from $47.5 to a peak of $124.3 in a short span of 2 years. After that, the shares would only surpass this peak 20 years later in 2019!

Petrobras (2015)

$2.5b, 100 years maturity.

Coupon 6.85% (30Y Treasuries 2.45%)

Price $95

Total return 164%

Brazil state-owned oil company was involved in a scandal of price-fixing, bribery and political kick-back causing $17b in write-downs. But it managed to squeeze in a century bond before interest rates started to rise.

Fortunately, it survived the 2020 oil crash caused by COVID. So far so good, lenders have 90 years more to go.

Norfolk Southern (2021)

$500m, 100 years maturity.

Coupon 4.1% (30Y Treasuries 2.1%)

Price $68.7

Total return -15% (underwater)

Norfolk railways came back again to issue another century bond. This time it was to fund ESG efforts, also known as Green Bonds. They tried to take advantage of the low rates, but subsequent rate hikes decimated the bond price and lenders are now underwater.

Observations

Looking at these century bonds, it is miraculous that only JC Penney failed to repay. Excluding the recent Norfolk bond, lenders have not lost money.

We can make 3 observations from history about why corporations would issue century bonds:

Issuers believe interest rates cycles are near bottom.

Market participants are in optimistic mood.

Credit conditions are loose.

The late 1990s preceded the dot-com crash. Also in December 1995, the Treasury proposed to eliminate the tax deductibility of interest payments of corporate bonds with maturity longer than 40 years, triggering a rush to issue super long term bonds.

The 2017 to 2021 period preceded the bond bear market in 2022.

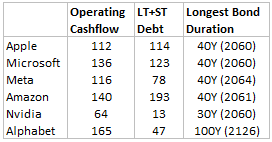

Now we have the present AI wave driven by infrastructure buildout. On top of Alphabet’s century bond, below are the longest duration bonds for Big Tech:

The yield curve in recent years have been quite flat at the long end, meaning the extra cost of borrowing for 100 years instead of 30 years was only about 50—100bps. For that tiny premium, Alphabet locked in its borrowing cost for an entire century, eliminating any risk of having to refinance at higher rates. It also gets a tax shield; interest payment reduces taxable income, effectively making the government subsidize some of the borrowing cost.

Although Alphabet plans to spend alot on AI, they are still growing operating cashflows at over 20% and have nearly $127b of cash equivalents. Therefore, we think the century bond’s motive is less financial, but more of identity signalling.

Think about what you are actually getting when buying a 100-year bond?

You don’t care much about getting paid back, because the purchasing power of $100 after a century of 2.5% inflation is only $8.46.

What you care about are the coupon payments. A century bond becomes like an annuity.

In this case, Alphabet is signalling that their business is so durable that pension funds and life insurance companies oversubscribed to their 100 year debt. Lenders feel assured that Alphabet will exist in year 2126, paying coupons to match their long duration annuity payouts.

Permanence

The average lifespan of S&P500 companies was 61 years in 1958. Today, it’s less than 18 years. How do you think about the longevity of businesses involved in the fast changing tech space?

Contrast the phenomena that Alphabet’s century bond was 5x oversubscribed with Austria, which issued sovereign century bond amounting EUR5.95b at 0.85% coupon (2020). It has been a disaster, the sovereign debt is trading at 30.9% of par.

This is a quite a structural shift in how capital markets assign permanence.

Final Notes

Here are some reasons why we think Alphabet's century bond was a good move:

The coupon rate is high enough to compress the duration (payback period) to about 17 years.

Buyers were pension funds and life insures with matching long duration liabilities.

Alphabet has a durable, high margin business model. Fortress balance sheet, remote bankruptcy risk.

Expectations of interest rates are downwards in the short term. If rates remain stable, then buyers enjoy price gains and coupons.