Study: Economic Cost to Offset SBC Dilution

Stock Based Compensation (SBC)

In a past study note, We have written about the gross inaccuracy of GAAP accounting when calculating SBC expense. But we didn’t provide a real example of how accounting does a bad job in estimating SBC true economic cost.

Let’s conceptualize why the accounting figure could be different from true economic cost.

Stock Price Effect

When a company grants SBC at a low price and its stock rises after that, more money has to be spent on offsetting the dilution when repurchasing shares at a higher price.

Withholding Tax

When a company grants stock to employees upon the vesting of RSUs, it grants those shares to the employee on a net-of-tax basis. The company then uses its own cash, as with a normal paycheck, to make the legally mandated tax withholding payments related to the RSUs.

When a company withholds tax from a paycheck and sends it to the IRS, the total cost to the company is still, of course, the whole paycheck, inclusive of the tax.

Per the FASB Accounting Standards Update 2016-19, these RSU vesting-related tax payments are a line item in the Cash Flows from Financing Activities.

Therefore, the cost to the company of SBC is the grant of stock on a net basis plus the withholding tax payments.

META Example

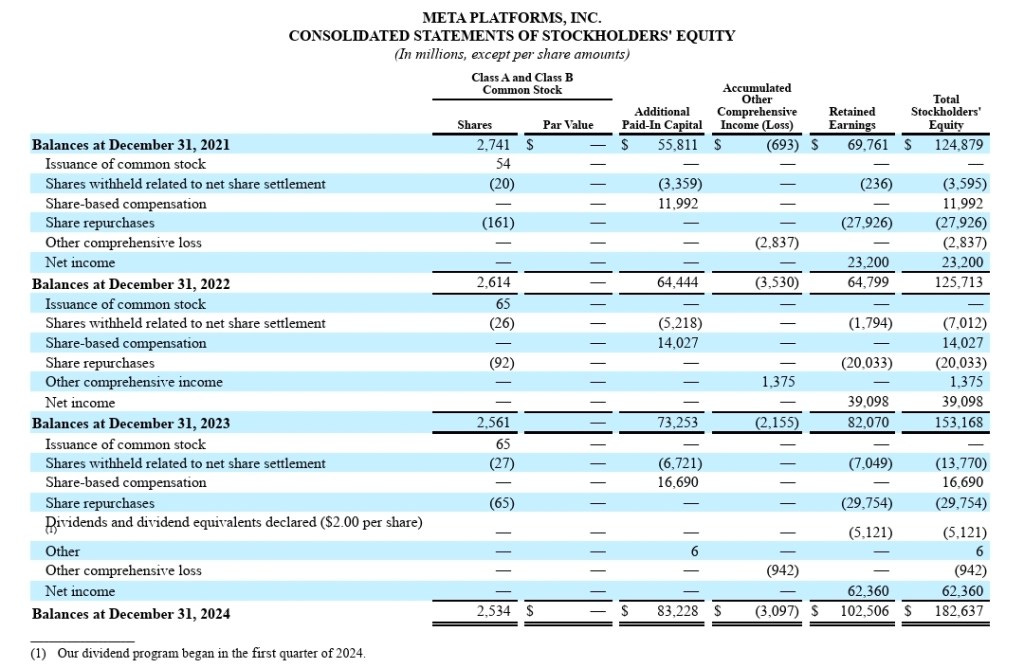

With the above 2 concepts in mind, it’s quite easy to find the economic cost to offset SBC dilution. All you need is the Statement of Shareholders Equity.

Let’s use META 10K (pg.89) as an example. For year 2024, these are the relevant figures you need:

Issuance of common stock = 65 million.

Shares withheld related to net share settlement = 27 million.

Net shares issued = 65 – 27 = 38 million.

Shares repurchased = 65 million.

Cash spent on repurchases = $29,754m.

Average repurchase price = [#5] / [#4] = 29754 / 65 = $457.75

Cash spent to offset SBC = [#6] * [#3] = $457.75 * 38 million = $17,395m.

Now, the withheld taxes related to SBC can be found from the cash flow for financing section. Or you can take it from the changes in shareholders equity due to “shares withheld related to net share settlement”.

Anyways, it’s the same at $13,770m for 2024.

We can find the true economic cost by adding #7 to the $13,770m withheld taxes.

Economic cost of SBC = $17,395m + $13,770m = $31,165m.

Compared to P&L reported = $16,690m.

That’s a huge discrepancy especially if you live by the P&L figures, or if your free cashflow calculations understate this economic cost!

If we extend this to see the cumulative amounts from 2020 to 2024:

Economic cost = $79,934m

P&L reported = $58,409m

Note: Cash flow statement shares repurchase amount is different from changes in equity statement because of accrual vs. cash accounting.

Will You Prefer Dilution?

Let’s use 2024 numbers to see if dilution is better considering the true economic cost of SBC.

At end of 2024, META had 2,517 million shares outstanding. Suppose that you own 10% shares worth $151.4b (market cap $1,514b).

If META didn’t repurchase 65 million shares to offset SBC, your 10% ownership would decrease to 9.75%.

Assume the $31,165m economic cost was saved and reinvested in the business, with returns of 10%, the market cap would increase by ~$62b at a 20x earnings multiple. Your diluted 9.75% stake would be worth $154b; more than the $151.4b if you were left undiluted.

In this scenario, the economic cost of offsetting SBC dilution is greater than ownership dilution.

Do note this what-if scenario has limitations:

1. It is based on knowledge that META share price appreciated +66% in 2024 resulting in a large cost to offset shares awarded at much lower prices.

2. Reinvesting $31b at 10% is quite impossible. If it was put into Treasuries, then dilution option is still better.

3. Paying down debt is also a good outcome.

Conclusion

This shows that when management do stock buybacks to offset SBC dilution, the true cost of such a design far larger than what GAAP accounting suggests. Especially when the stock price increases substantially, so does the cost required to offset dilution.

We should be aware that such “dilution offsetting” plans sound good on the surface, but in some cases can be detrimental to existing owners.