Study: Coca-Cola & Pepsi

Emergence of the Duopoly

Coke and Pepsi were both invented in the late 1800s as a fountain drink. They each expanded through franchised bottlers; Coke with its uniquely contoured 6-ounce “skirt” bottle and Pepsi with a 12-ounce bottle; both sold for a nickel. Robert Woodruff, one of the most dominant figures in Coke’s history, worked with the company’s franchised bottlers to make Coke available wherever and whenever a consumer might want it. He argued that if Coke were not conveniently available when the consumer was thirsty, the sale would be lost forever.

Woodruff developed Coke’s international business principally through export. One of his most memorable decisions, made at the request of General Eisenhower at the beginning of WW2, was to see that every man in uniform gets a bottle of Coke for 5 cents wherever he is and whatever it cost.

Coke was exempted from wartime sugar rationing beginning in 1942, when the product was sold to the military or retailers serving soldiers. Coke bottling plants followed the movements of American troops, with 64 bottling plants established during the war largely at government expense. This led to Coke’s dominant market share in most European and Asian countries, a lead which the company still has today 8 decades later.

In contrast to Coke’s success prior to WW2, Pepsi struggled, nearing the brink of bankruptcy several times in the 1920s and 1930s. By 1950, Coke’s share of the soft drink market was 47% and Pepsi’s was 10%.

In the 1950s, Coke used advertising slogans such as “American’s Preferred Taste” (1955), “Be Really Refreshed” (1958), and “No Wonder Coke Refreshes Best” (1960). In the 1960s, Coke along with Pepsi began to experiment with new cola and non-cola flavors, packaging options, and advertising campaigns. They pursued market segmentation strategies, leading to new product introductions such as Pepsi’s Mountain Dew and Coke’s Fanta and Sprite.

Coke and Pepsi both looked outside the soft drink industry for growth in the 1960s, with Coke purchased Minute Maid, Duncan Foods, and Belmont Springs Water. While Pepsi merged with Frito-Lay to become PepsiCo, claiming synergies based on shared customer targets, store-door delivery systems, and marketing orientations.

Throughout most of this period, Coke did not aggressively attack Pepsi and maintained a highly fragmented bottler network. In fact, much of Coke’s efforts was in foreign markets where it generated almost 66% of its sales volumes. Pepsi, however, was aggressively taking market share in the US, doubling its share between 1950 and 1970. Their bottling network was larger, more flexible, and often offered lower prices to national chain stores.

Slowly but surely, Pepsi caught up with Coke. In 1963, the “Pepsi Generation” campaign targeted the young and emphasized a consumer lifestyle. It gave Pepsi an image that was distinct from Coke’s nostalgic, smalltown America image. Pepsi’s ad agency created visual commercials using rock-stars like Britney Spears and Michael Jackson with a catchy phrase “Come Alive – You’re in the Pepsi Generation” (watch it here, very entertaining featuring Britney Spears).

The campaign was so successful that Pepsi narrowed Coke’s lead to a 2-to-1 margin. But the most aggressive move by Pepsi was yet to come.

The Pepsi Challenge

In 1974, the first collision between Coke and Pepsi came in the “Pepsi Challenge” campaign. It was a comparative taste test where consumers showed a clear preference for Pepsi. This campaign led to a rapid increase in Pepsi’s market share, from 6% to 14%.

Coke tried to defend itself by conducting its own taste tests. However, these tests had the same result, people liked the taste of Pepsi better. By 1979, Pepsi was closing the gap on Coke, having 18% of the soft-drink market, to Coke’s 24%. By 1984, Coke had only a 2.9% lead. Further indication of the diminishing position of Coke relative to Pepsi was a study done by Coke’s own marketing research department. The study showed that in 1972, 18% of soft-drink users drank Coke exclusively, while only 4% drank only Pepsi. After 10 years the statistics had changed greatly with only 12% claiming loyalty to Coke, while Pepsi almost matched with 11%.

Despite Coke spending much more than Pepsi in advertising, having twice as many vending machines, more shelf space and was competitively priced, it still lost market share to Pepsi. The marketing dollars spent by Coke were simply not as effective as Pepsi.

Nevertheless, both companies understood the importance of marketing and increased spending from 1975 to 1980; Coke went from $34m to $70m and Pepsi $25m to $67m.

Coke’s new CEO

Paul Austin, chairman of Coca-Cola, was nearing retirement in 1980. Donald Keough, president of the American group, was expected to succeed him. But a new name, Roberto Goizueta, suddenly emerged.

His background was far different then the typical Coke executive. Goizueta was the son of a wealthy Havana sugar plantation owner, he came to the US at the age of 16 without knowing a word of English. By using a dictionary and watching movies, he quickly learned the language and graduated from Yale in 1955 with a degree in chemical engineering. Returning to Cube, he went to work in Coke’s Cuban research lab. In 1959, Cuban communist, Fidel Castro seized power in the country and Goizueta fled with his wife and 3 children to the US. Goizueta would climb the corporate ladder and eventually became chairman of the board 13 years later in 1981.

The winds of change also brought in the first flavour changes in Coke’s 99 year history.

Tampering with Traditions

After Roberto Goizueta took over, Coke launched “Diet Coke” in 1982. It was a phenomenal success and by the end of 1983, it was the most popular diet soda. The next year, it became the third largest seller among all US soft drinks. Coke also introduced 11 new products including Cherry Coke, Caffeine Free Coke and Minute-Maid Orange.

Pepsi followed with 13 products including Caffeine Free Pepsi-Cola, Lemon Lime Slide and Cherry Pepsi. The competition for shelf space became increasing intense. During this period, new brands emerged and price wars eroded margins for all soft drink players. The industry experienced a sharp increase in level of discounting as everyone was chasing market share.

The most disastrous strategy came in 1985 when Coke changed the formula of their syrup. In a Wall Street Journal article in 24 April 1986, Goizueta quoted:

[…] value of the Coca-Cola trademark is going downhill as the product and the brand had a declining share in a shrinking segment of the market.

In September 1984, the taste researchers developed a sweeter flavoured Coke and the marketing department launched the biggest taste test ever costing $4m. The results were 55% of the 191,000 participants approved it over Pepsi and the original Coke formula. So management decided to take “Old Coke” off the market and replaced it with “New Coke”.

Protests quickly ensued. By May 1985 calls were coming in at the rate of 5,000 a day, in addition to a barrage of angry letters. Anger spread across the country for fiddling with the formula and Coke was worried about a boycott. Just 79 days later on 11 July 1985, Coke’s management apologized to the public and reinstated Old Coke.

Critics called it the “marketing blunder of the decade”:

Strangely enough, the mistake by Coke turned out to be positive for sales. By keeping the new flavour in addition to bringing back the old one, sales for 1985 rose by 10% and profits by 9%. By 1988, Coke had 40% of US market share while Pepsi lagged with 31%.

Bottlers Franchise

In the 1980s, Coke and Pepsi began a process of altering the structure of the franchise system. The price wars weakened many independent bottlers, leading franchises to seek buyers. Some of the bottlers were small, producing under 10 million cases a year, and did not have the capability to handle large corporate goals. Others were bought because they were located near a company-owned bottler, or they were under-investing in plant and equipment.

Both companies saw advantages in controlling bottlers under franchise agreements. Pepsi decreased the number of bottlers from 435 to 120, owning 56% of them outright and equity positions in most others. Coke bought together several bottlers into Coca-Cola Enterprises (CCE) and sold 51% of it to the public while retaining 49% share.

This consolidation movement meant that smaller soft drinks companies had to sell their products through Pepsi or Coke bottling system. Both companies continued to look at the industry as a total system rather than individual markets, and despite greater vertical integration, they continued to run their bottlers as independent businesses.

International Expansion

In 1994, Pepsi started an ambitious entry into Brazil. The country had hot weather and a growing teen population, it was positioned as one of the world’s fastest growing soft drink markets. Brazilian consumers at that time averaged only 264 eight-ounce servings of soft drinks a year, far below the US average of 800.

Buenos Aires Embotelladora SA, or Baesa, was to be the key to Pepsi’s entry into Brazil. The strategy was that Baesa would buy small bottlers across Latin America to expand their marketing and distribution.

Charles Beach, the CEO of Baesa, was the person around whom Pepsi planned its strategy. He borrowed heavily to expand Pepsi franchises in Chile, Uruguay and Brazil where he built 4 giant bottling plants.

However, they underestimated Coke’s strategy. Coke spent heavily on marketing and cold-drink equipments for its customers. As a result, Baesa was shut out of small retail outlets which were the most profitable for bottlers. Goizueta used his Latin American background to influence the Argentine president to reduce taxes on cola from 24% to 4%. This move strengthened Coke’s position against Bresa which was earning most of its profits from non-cola drinks.

By 1996, Pepsi new Brazilian plants were running at low capacity and Baesa lost $300m for the first half of 1996 and Pepsi injected another $40m into Baesa.

Pepsi also failed in Venezuela when Oswaldo Cisneros, head of one of Pepsi oldest and largest foreign bottling franchises, suddenly abandoned Pepsi for Coke. This happened because Cisneros felt that Pepsi management paid little attention to Venezuela, and as he was growing older, he wanted to sell the bottling operations, but Pepsi was only willing to acquire 10%. Seeing this as an opportunity, Coke agreed to buy 50% of the business and paid an estimated $500m, effectively taking Pepsi out of the Venezuela market.

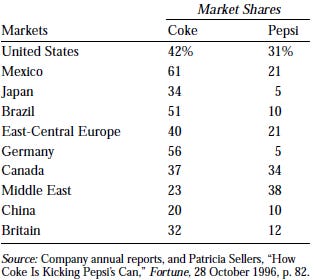

Pepsi problems in South America mirrored its problems worldwide. It had lost its initial lead in Russia, Eastern Europe, and parts of Southeast Asia. Even in Mexico, its main bottler reported a loss of $15m in 1995. The contrast with Coke was significant: Pepsi generated more than 70% of its beverage profits domestically while Coke got 80%

overseas.

Below is the 1996 global market share, we can see that in countries like Japan and Germany, Pepsi is non-existent:

Diversification

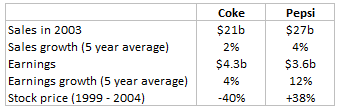

At the turn of the new millenia, consumers began to be more concerned with health. Pepsi, with its diversified products, started to produce better business results than Coke:

Coke’s focus on carbonated soft drinks was at a disadvantage compared to Pepsi diversified products. Pepsi had pushed into non-carbonated market with Tropicana juice, Gatorade sports drink, and Aquafina water.

Coke remained fixated on its flagship brand with sodas contributing 82% of sales, while Pepsi only 29%. Pepsi also had its salty snack division with brands like Lays, Doritos, and Cheetos. In 2001, they went further and acquired cereal brand Quaker Oats.

The reluctance to diversify was evident when Coke decided against acquiring

South Beach Beverage Company (SoBe) after negotiating for 2 years. Pepsi made an offer

and quickly acquired the SoBe brand, which gave Pepsi access to tea and fruit juices.

Coke’s management continued the conservative mindset and missed the chance to acquire energy drink company Red Bull. Because of this conservatism, Coke missed a highly profitable segment that Red Bull dominates today.

Lessons from History

Consumer taste is Fickle

Brand image is superior to taste tests. Gaining mind share is far better than market share. Advertisements that cultivate a desirable image or personality are more effectively in creating product value than trying to fit a product with consumer taste.

Don’t change Traditions

“New Coke” might have been successful if they did it quietly, instead of announcing it to be “new”. When there’s a product with a super long life cycle, it’s best not to tamper with traditions.

Also Coke could have introduced “New Coke” without removing the original one. The fear of New Coke competing with the original is a flawed rationale.

Margins is not Everything

Pushing for high margin products is not always the best. Because low margin products can yield more total profits with greater sales volume. Coke focused on their high margin sodas and failed to diversify, neglecting other growth opportunities.

Find Inevitable Companies

Coke’s history is filled with several disastrous events that could’ve crippled any other company:

Branding blunder of New Coke

Douglas Ivester (CEO, 1997 – 2000) over invested in Russia right before its economic collapse. He illegally avoided Polish taxes and was forced to resign.

Douglas Daft (CEO, 2000 – 2004) failed to diversify products. Resigning only after 4 years.

Contamination health scare in Belgium, 1999.

Despite that, Coke today still has 47% of global market share in soft drinks, while Pepsi has only 19%.

Bill Gates put it best when he said: “Coke is a company that a ham sandwich can run.”

Cultivate a Consistent Brand

Sponsoring is at the heart of Coke’s strategy, through long-standing partnerships with events like the World Cup and Olympic Games. At these major events, the advertisement is always delivering a consistent emotional message: Coke equals happiness.

This is difficult to replicate even if a competitor has the financial resources because Coke has developed its marketing practice for more than a century.