Study: Berkshire’s Future After Buffett

Preface: Instead of addressing the topic directly, let’s go on education tour on the acquisition of GEICO.

Lesson from GEICO

Since 1976, GEICO was a marketable security on Berkshire’s books at a tiny cost basis of $46m. The stock investment was incredible returning a CAGR of +23% for 19 years, Berkshire never added any more shares but its ownership grew from 33% to 51% owing entirely to GEICO’s share repurchases, and at year-end 1995 its market value was $2.4b.

Then in 1996, Berkshire acquired the remainder 49% for $2.3b, implying a total company valuation of $4.8b, twice of 1995 market value, and 50x more than their initial cost basis! It didn’t seem like a cheap price to pay at 2.5x its year-end 1995 book value of $1.9b.

Importantly, GEICO had $3b of insurance float and a long history of profitable underwriting.

During the 1996 annual meeting, Buffett offered an insight into his and Munger’s thinking on float, he said:

Would I trade Berkshire’s float for $7b of equity and not have to pay tax on the gain, but then have to stay out of the insurance business forever?

No. We wouldn’t even think about it for very long.

To paraphrase: They wouldn’t take the offer of magically transform $7b of insurance liabilities into $7b of equity capital.

This is quite a bold statement in 1996. Of course, today we have the hindsight of seeing the power of insurance float working for Berkshire, but at that time this should cause us to be at the edge of our seats.

Why reject the ability to get an equal amount of tax-free capital in exchange for float?

The reason Buffett would not take such a hypothetical arrangement was that he expected the float to grow over time and at an attractive cost.

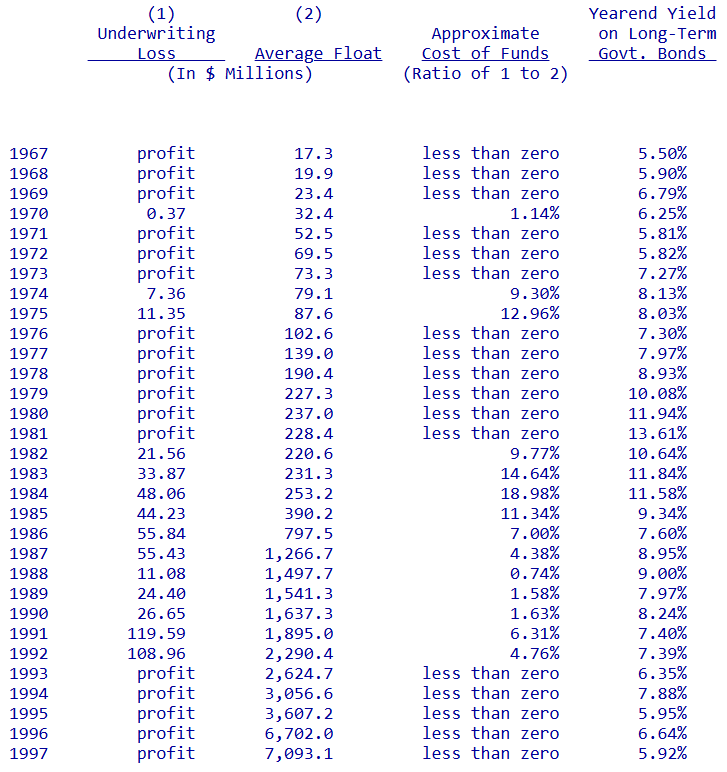

Berkshire’s insurance businesses were gems due to one simple fact: An insurance operation is valuable only if its float cost less than borrowing with government bonds.

This concept sounds easy but in practice it is very difficult to run a consistently profitable insurance operation. Berkshire is not without some bumps and lessons along the way on their quest to deliver cost-free float.

There were times when the cost of float was higher than government bonds, this is a dangerous thing because insurers write premiums at multiples of their equity, due to this leverage underwriting losses can be magnified:

However, when Berkshire can consistently produce underwriting profits on average, the float would economically be like equity rather than a liability. Moreover, if float could grow over time, it would be even more valuable.

This assertion that a liability could be considered equity can be a hard concept to grasp.

What is the definition of traditional equity?

Equity capital is funds invested by owners for ownership stakes, representing the residual interest in a company’s assets after liabilities.

Notice that equity doesn’t have due dates or covenants.

Following this definition, insurance float could be considered better than equity if it generated an underwriting profit over time. Such quasi-equity doesn’t dilute shareholders ownership like a regular equity investment would.

GEICO’s float is money owed to policyholders, but because of its revolving nature it doesn’t behave like debt or bank deposits. In other words, individual policies would be paid daily, but new premiums would be written collectively that could be expected to refill and maintain the overall level of float. Furthermore, policyholders cannot demand claims outside of legitimate insured events, unlike banks which can experience irrational runs on deposits.

Buffett assumed that GEICO will continue to underwrite profitably like how it has done, so it wouldn’t be a stretch to add it’s float to book value.

At 1996, GEICO had $3b float and $1.9b book value, adding them up will give us $4.9b against the implied valuation of $4.8b. Berkshire was buying GEICO at 1x “book + float” value, without factoring float growth and look-through earnings from its stock portfolio.

What seemed to be an expensive price-to-book multiple is now an incredibly cheap price to pay.

Buffett and Munger would go on to be proven right. After 18 years, GEICO’s float compounded at 8.7% to $13.6b in 2014, all this while providing negative-cost funds for Berkshire to invest. GEICO’s track record was superb: Out of 18 years (1996 – 2014), it only had 1 year of underwriting loss in 2000.

Now Berkshire has grown much larger, it doesn’t disclose GEICO’s float anymore. As of Q3 2025, all of Berkshire’s insurance entities provided $176b of negative-cost insurance float, it came a long way from just $7b in 1996.

Future of Berkshire

This history lesson leads us to the topic about Berkshire after Buffett, as we know he will step down as CEO at the end of 2025.

Many people tend to point towards investing acumen when assessing Berkshire’s success, although that is true during the early years, we don’t think it’s the critical ingredient going forward.

At this stage, operations excellence is much more important than investing skills. The power of negative-cost float is so great that whoever is managing Berkshire, even if they did no acquisitions, as long as the insurance operations are run profitably and doesn’t shrink, Berkshire will continue to compound at a modest pace (assuming all other segments perform average).

Berkshire will never compound at historical high rates due to its size, but we are sure that it can produce slightly above market returns because it is of higher quality than the average business.

Conclusion

If we set aside Buffett’s more recent donations, he historically controlled ~40% of the voting rights in Berkshire through his ownership of the Class A shares. He also enjoyed close personal relationships with other significant holders of the stock (often enjoying their proxies), which allowed him to effectively control the company since taking it over in the late 1960s.

Buffett is the Chairman and has appointed loyalists to it, including at times his wife, children, lifelong friends, and business partners. He is also CEO, controlling the company’s use of funds and appointing key personnel. In short, Buffett is a very well-insulated leader heading what might otherwise be termed a dictatorship. An enlightened despotism, certainly, but no one could accuse Berkshire of being a democracy.

Now that Buffett has moved into retirement, it’s difficult for him to have a true “successor” in his own image. Greg Abel may be smart, respected, and capable, but he doesn’t own a huge % of Berkshire.

Big portions of the stock will be owned by the Gates Foundation and the foundations run by Buffett’s children.

Abel won’t be able to easily control the board; Buffett’s eldest son, Howard, will still succeed to the Chairmanship. Abel is simply a CEO and a minor shareholder, enjoying possession of one of America’s largest conglomerates.

While Buffett lives, Abel can enjoy the protection of the man who still dominates each facet of Berkshire’s power structure, and perhaps for a time thereafter he can enjoy the fading nimbus of Buffett’s legend. After that, his position will understandably be much weaker than his predecessor’s.

Abel might have incentives to break Buffett’s long-time practice of not remunerating board members. Buffett was able to get away with this because he rewarded his followers with exceptional stock-price appreciation. The Berkshire of today is in no position to repeat history, but it does have access to substantial cash flow.

Having stacked the board with his loyalists, Abel should then secure the Chairmanship at the earliest opportunity. Having secured possession and governance of the company, the only way he could be removed would be if enough of the disparate post-Buffett ownership base banded together to seize control of the board.

Abel is not Buffett and should not act like him if he wants to succeed in leadership.