Study: Alibaba

Preface

Journaling a long list of entities under Alibaba. We don’t have much insights to the economics of their business segments, and so will only lightly comment on anything we find interesting.

History

Alibaba was founded in 1999 by Jack Ma with a group of 17 friends and colleagues in Hangzhou. Inspired by the story of “Ali Baba and the Forty Thieves” from the Middle Eastern folktales collection One Thousand and One Nights.

In October 1999, Goldman Sachs led Alibaba’s first round of fundraising. Goldman invested $3.3m, and when the tech bubble burst investors began to lose faith in Chinese start-ups. A costly mistake for Goldman who sold in 2004 for a mere $22m.

In January 2000, SoftBank put $20m into Alibaba. They held onto those shares until a peak ownership of 34% in 2014, then quickly divested its stake to less than 0.5% by 2024.

Then in 2005, Yahoo! paid $1b for 40% stake in Alibaba. By 2012, Yahoo! was a struggling business and Alibaba bought back 20% of its equity stake from Yahoo! for $6.3b cash + $800m preferred stock.

All these funding helped Alibaba realize its vision of assisting Chinese small-medium enterprises (SME) in exporting Chinese goods to the world.

Alibaba would go on to set their “New Retail” strategy and bought Intime retail stores. This also spawned the familiar names like Sun Art, Hema, Ele.me.

Alibaba Cloud was also became important around this period to support the internal infrastructure of their e-commerce business.

Just before their IPO Alibaba bought a 50% stake in Guangzhou Evergrande FC from Evergrande Real Estate Group for $192m.

Yes, a football club!

It was reported that the deal was made with Evergrande chairman, Xu Jiayin, in just 15 minutes. Evergrande Real Estate went bankrupt in 2021 and caused the football club to collapse. In January 2025, Guangzhou FC was expelled from the professional league and disbanded because they failed to pay off debts.

Anyway, in 2014, Alibaba went public raising $25b, setting a record as the largest IPO globally, surpassing the combined IPOs of Google, Facebook and Twitter.

At this period, Alibaba started to expand globally, starting from Southeast Asia. In 2016, they acquired a controlling stake in Lazada which was founded by Germany’s Rocket Internet. The next year, Alibaba put another $1b into Lazada. More money poured in from 2018 to 2022 in a price war with Shopee.

More recently, Alibaba plans to invest $52.7b to build global cloud infrastructure launching its first data centers in Brazil, France, and Netherlands, with additional data centers to be added in Mexico, Japan, South Korea, Malaysia, Dubai.

Being one of the largest tech company in China, Alibaba is exposed to regulators’ scrutiny. For example, in 2020, Chinese regulators blocked Ant Group’s IPO and imposed a $2.8b fine for monopolistic practices. And in 2022, the China Internet Investment Fund, purchased a “golden share” in two Alibaba subsidiaries, Youku (video streaming) and UCWeb (web browser).

Following these events, Jack Ma retired from the board in 2020. The CEO role held by Daniel Zhang lasted from 2015 to 2023, passing the torch to Eddie Wu.

Before stepping down as CEO, Daniel Zhang buried the “New Retail” story, and management introduced the “1+6+N” restructuring strategy, dividing the business into 6 independent entities, each with their own CEO and board:

Cloud Intelligence. Home to their AI model (Qwen) and workplace messaging app Dingtalk. CEO: Eddie Wu.

Taobao TMall. The domestic e-commerce marketplace, making up most of Alibaba’s revenues. CEO: Eddie Wu (initially Trudy Dai).

Cainiao Smart Logistics. Formed in 2013, Cainiao is now a major logistics provider in China also serving other customers. CEO: Wan Lin.

Local Services. Food and grocery delivery services, as well as its mapping app Amap. This segment competes aggressively with Meituan. CEO: Yu Yongfu.

Global Digital Commerce. Overseas e-commerce marketplaces like Lazada, Trendyol, AliExpress. CEO: Jiang Fan.

Digital Media & Entertainment. Consists of Youku, Daima Entertainment, AliMusic etc. CEO: Fan Luyuan.

E-commerce Platforms

Alibaba.com

This is the first business of Alibaba: B2B platform connecting Chinese manufacturers, suppliers, and buyers worldwide. In 2024, Alibaba.com served over 48 million SMEs from over 200 countries and regions.

AliExpress

Founded in 2010, it’s a cross-border B2C platform with over 150 million active buyers. Available in 16 languages, it has significant customer bases across Europe, Russia, LATAM and Southeast Asia.

Taobao

Founded in 2003, it’s the leading C2C retail e-commerce platform in China. Taobao connects consumers across various marketplaces, channels and services within Alibaba’s ecosystem. It also serves overseas consumers particularly in Southeast Asia.

1688.com

Founded in 1999, domestic only B2B platform. Vendors pay an annual membership fee to be listed as verified suppliers to enhance credibility and visibility.

TMall

Founded in 2008, it’s the largest B2C retail platform in China having 48% market share. Focusing on authentic, high quality, premium shopping experience. It has over 800 million buyers, mainly in China, but also has international brands through Tmall Global launched in 2014. They also operate TMall Mart (2011) for quality supermarket sales.

TMall Global came in 2014 to specifically serve as the leading import e-commerce platform. It started with 100 overseas brands and has grown to over 46,000 brands from 90 countries and regions, covering 7,000 product categories.

Xianyu

Launched in 2014, it’s a C2C platform for second-hand products. In 2023, the platform reported to surpass GMV of 1 billion RMB.

Kaola

An import e-commerce platform launched in 2015 by NetEase, the loss making segment was acquired by Alibaba for $2b in 2019. They promised Kaola to operate independently under its own brand. The platform is the 2ⁿᵈ largest platform selling Western brands in China, with this acquisition Alibaba owns the top 2 cross-border e-commerce platforms (1ˢᵗ place TMall).

In addition, it has more than 150,000m² of bonded warehouses. These are secure, customs-controlled facilities where imported goods can be stored without immediate payment of import taxes.

This logistics strategy reduces international shipping times down to 3 days and synergizes well with TMall Global.

In 2021, Alibaba's business team of over 400 people (excluding product and technology staff) operated the Kaola Global Shopping app, which saw fewer than 1 million daily visits and generated less than RMB3b in annual transaction volume. In contrast, Tmall Global achieved a GMV of over RMB60b in 2021.

As of July 2022, Kaola's business team had shrunk from over 400 people in 2021 to less than 20, focusing on membership e-commerce business primarily in the maternal and infant and beauty categories. Product and technology are now only maintained, with no further upgrades.

Surely, the Kaola mascot disappeared in the 2022 report:

Lazada

In 2018, Alibaba fully owned Lazada and by 2024 it’s estimated over $7.4b has been poured into this e-commerce platform operating in 6 primary markets: Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam. Competition is very intense with major players like Shopee and TikTok.

Lazada is an interesting case study of how being a first-mover does not necessarily lead to a sustainable leading position.

Lazada was established as predominantly a 1P inventory carrying retail model instead of a 3P marketplace. Its focus on standardised categories such as consumer electronics and building out of its own logistics made it extremely cost efficient in those categories, but at the expense of having a differentiated marketplace with lots of repeat purchases.

It helped promote e-commerce through its aggressive advertising campaigns, and there was the opportunity to leverage its position as a first-mover and expand into a broader marketplace.

However, what derailed Lazada was internal cultural issues together with integration mismanagement of Alibaba.

Under Alibaba, Lazada went through 3 CEO changes in 2 years and multiple changes of country heads. Alibaba installed middle management into Lazada, and due to their lack of understanding of unique local conditions, staff attrition spiked with a large number of people joining Shopee.

Alibaba also forced Lazada to switch to its technology back-end to the same as Taobao. However, the complexity of IT migration led to problems that disrupted operations.

All these allowed Shopee to overtake Lazada in 2017.

But big competitors in this place don’t die easily, especially with financial backing from Alibaba. There are examples of Lazada leveraging its Alibaba relationship successfully. For instance, you can now buy things from Taobao on Lazada. This allows Lazada users to access Taobao merchants directly, which has a huge number of products.

Trendyol

Trendyol is a B2C platform founded in 2010 by Demet Mutlu and based in Istanbul. In 2018, Alibaba invested $728m to acquire 86.5% stake allowing them to expand their international presence.

This Turkish e-commerce group also owns Trendyol GO, a service that delivers food in Turkey. In 2024, it had $2b in gross bookings and delivered more than 200 million orders. In 2025, Uber bought over Alibaba’s 85% stake in Trendyol GO for $700m.

Daraz

Another B2C & C2C platform created by Rock Internet in 2012 initially as a small online fashion retailer. Daraz focuses in Pakistan, Nepal, Bangladesh, Sri Lanka. In 2018, Alibaba acquires the whole platform in an undisclosed deal.

Miravia

B2C platform launched by Alibaba in 2022 in Spain, an effort to expand into Europe after Cainiao logistics set up a hub in Belgium in late 2021. Miravia Open Platform allows developers to integrate through APIs so that sellers can connect their systems for managing products, logistics and finance.

Local Services

Alipay

Launched in 2004 by Alibaba, the digital mobile payment platform is operated by their affiliate Ant Group. Alipay is the leader in China’s digital payment market, having more than 50% share with over 1.3 billion users and millions of merchants across China accept it. WeChat Pay comes in 2ⁿᵈ place. These two payment platforms play a critical role in everyday life of the Chinese consumer.

Alipay traces its history back to 2004 at a time when digital e-commerce in China was about to take off. In 2002, eBay came into China by buying 33% stake in EachNet, the leading auction site in China for $30m. Shortly after Taobao was launched in 2003, but there were two main problems to be solved.

Trust issues with e-commerce.

High cost card based payments.

Alibaba then launched Alipay to solve the trust problem. Alipay had an escrow mechanism that would receive funds from the buyer and only pay the seller once the transaction was completed successfully.

To solve the high cost associated with card payments, they created a closed-loop payment rail that charged merchants lower transactions fees.

Solving these issues not only enabled Taobao to grow, it enabled Alipay to grow as a serious payments platform in the country. In the early 2010s, Chinese banks promoted POS terminals with chip readers, hoping to modernize the retail market. But many small merchants had no access to POS hardware. New smartphones with NFC capabilities were expensive too.

There was a good solution that required no infrastructure upgrade — the QR code.

So Alipay launched their mobile payment app in 2009 allowing merchants to just print out their QR codes and people would scan and pay. By 2015, 90% of Alipay’s offline transaction used QR and it became the default standard across China, skipping the intermediaries giving Alipay control of the payment rails.

To improve transaction success rates, QuickPay was introduced in 2010 with in-app authentication, keeping the entire transaction without Alipay. By 2010, Alipay had 100 million users and was growing rapidly.

These seeds planted what would become the term “super-app” in China.

An early development came in 2013, when Yu’e Bao was launched. It was a money market fund that Alipay users could use to earn higher interest on their Alipay wallet balances than traditional bank savings.

A few more useful apps came up like MYbank, Huabei and Jiebei, which provided loans to SMEs, entrepreneurs and commercial farmers. People who were in the Alipay ecosystem generated data for Alibaba to calculate credit scores, skipping the traditional banking route.

To bring even more people onboard, Alipay went for the public services. In the past, paying for utilities was not frictionless, people had to queue at offices with cash. So Alipay spent over 10 years building relationships with 300+ municipal utilities to integrate payment systems. Although they wouldn’t make money, but it solved a real social pain and brought millions of new users onto the platform.

After their success in homeland China, Alipay planned to go international. They adopted partnership JV approach instead of direct competition. From 2015 to 2018, Alipay made many partnerships:

2015: Paytm (India). It wasn’t profitable, Alibaba fully exited their stake in 2023.

2017: Launched Alipay HK (Hong Kong).

2017: KakaoPay, subsidiary of KakaoTalk (South Korea). Invested $200m, wanted to allow Chinese tourists to use Alipay in South Korea.

2017: Launched Dana (Indonesia) through JV with Emtek.

2017: Touch n Go, subsidiary of CIMB (Malaysia). Equity JV with Ant Group as minority.

2017: GCash (Philippines).

2018: Easypaisa (Pakistan). This is Pakistan’s first digital bank, but can only be used for domestic payments. International remittances is allowed.

2018: bKash (Bangladesh). 20% stake, Bangladesh’s largest mobile financial service provider.

2018: TrueMoney (Thailand). 20% stake, it has 53% share of Thailand’s e-wallet market.

Fast forward to 2019, Alipay became a super-app with 711 million MAU and 80+ million monthly active merchants. Total revenues were ~$18b and they were sitting on $594b investment AUM, they even had insurance premiums of $7.5b!

Then Alipay+ was spawned in 2021 to solve global money movement and interoperability.

Digital payments are the key to driving the digitalization of business activities. However, the uneven regional development and technical capabilities of participants have led to a lack of interoperability between existing digital payment solutions resulting in the fragmentation of payment systems across the world.

Alipay+ provides global cross-border mobile payments solutions which enables merchants, including SMEs, to better serve over one billion consumers (excluding Alipay) from all over the world, mainly from Asia currently, by connecting merchants with multiple digital payment methods.

Besides payments, Alipay+ also provides digital marketing solutions, which help global merchants to distribute various kinds of discounts to digital payment method users, helping them to gain and retain consumers across the world.

Jia Hang, GM Alipay+

The idea of cross-border payment capabilities is similar to Stripe. Alipay+ offers standardized APIs for businesses to easily integrate into the platform. It leverages on Alibaba’s cloud hardware for high uptime and independent scaling.

Alipay+ harvested the JV investments made earlier by integrating all those wallet providers into the Alipay+ ecosystem. Merchants can transact from every other Alipay+ wallet. The cross-selling value proposition is very strong.

Under payments, there are 4 core products within the Alipay+ ecosystem:

Cashier Payment: Enables merchants to receive online payments from any Alipay+ wallet across the world. For a merchant acquirer, this simply means adding the Alipay+ option at checkout.

Auto Debit: Enables clients to make recurring payments at a merchant website. This is useful for subscription type products.

User-Presented Payment: In-store payment mode where the customer presents a code to the merchant and the merchant scans it to initiate payment.

Merchant-Presented Payment: Customer scans the merchant’s QR code to initiate payment.

With these payment types, Alipay+ can support not only e-commerce but global peer to peer payments. It is not hard to imagine B2C payments such as payroll.

Under Marketing, Alipay+ is solving for a very critical pain-point. In an online world, discovery is as important as payment capabilities. Building the capability for merchants to market their products offers a very strong wedge. For instance, if a Kakao user from South Korea travels to Malaysia, Alipay+ enables them to see what products are available and what discounts they can get. This is all enabled through the marketing services on the platform. Merchants can now not only accept payments but they can run targeted ads that drive customer acquisition.

Cainiao

Cainiao is a logistics and supply chain management company launched in 2013. It operates a network of courier pickup points known as Cainiao Stations across China, and Cainiao Express functions as a dedicated courier service.

At its founding, Cainiao was backed by a host of illustrious logistics shareholders, which included Yintai (银泰), Fosun (复星), Fochun (富春), SF Express (顺丰), STO Express (申通), ZTO Express (中通), YTO Express (圆通), and Yunda Express (韵达). Among these investors, TMall made a significant contribution, injecting RMB2.15b to secure a 43% stake.

Fast forward to September 2017, Alibaba invested an additional RMB5.3b, raising its stake from 47% to 51% and earning another board seat. Then in November 2019, Alibaba put in another RMB23.3b for a total 64% stake.

In March 2024, Cainiao IPO was cancelled and Alibaba announced plans to buy out the remaining 36% stake from minority shareholders.

Cainiao also operates a logistics network across over 200 countries and regions, including 18 overseas sorting centers. In 2024, Cainiao delivered over 5 million cross-border and international packages on average daily.

Ele.me

Founded in 2008 by Zhang Xuhao and Kang Jia in the Minhang Campus of Shanghai Jiao Tong University. The acquisition cost was not disclosed but Ele.me was valued at $9.5b in 2018. Competition has been fierce for more than a decade, with players engaging in heavy discounting, Meituan was one such player facing off against Alibaba and Baidu. Afraid of these big players, Meituan merged with Dazhong Dianping in 2015, and received RMB3.3t investment led by Tencent and other investors.

Initially as a digital tool for ordering services that connected restaurants and eaters, Meituan and Ele.me also proactively explored various ideas like group discounts and paid membership.

Finally, with bad performers quitting the market, the takeout delivery market became a duopoly of Meituan versus Ele.me. With traffic from Dazhong Dianping along with streamlined management, Meituan’s market share exceeded 65% compared to Ele.me 27—33%.

Fliggy

Fliggy (formerly known as Alitrip) is a Chinese online travel service platform launched in 2014. Competitor CTrip dominates the online travel agency market.

Amap

Amap was formerly known as China Datoong Industrial, founded in 2002 by Jun Hou, Congwu Cheng and Jun Xiao. Alibaba acquired it in 2014 and integrated it into apps like Ele.me and Koubei (restaurant review platform).

Media & Entertainment

Youku

Inspired by YouTube, Youku was founded in 2006 by Gu Yongqiang, former President of Sohu. In 2012, Youku merged with Tudou in 2012 becoming China’s dominant online video platform. In 2014, Alibaba purchased a stake in Youku and later a fully buyout in 2015, proposing a valuation of $4.8b. Due to the merger, Tudou was delisted and became a wholly owned subsidiary.

Youku market share is #3 behind Tencent Video #1 and iQIYI #2 (Baidu).

It tries to differentiate through high production value dramas and culturally rooted content, positioning itself as long-form content as opposed to the popular short-drama hype.

Alibaba Pictures (Damai Entertainment)

Originally established in Hong Kong (1994) as ChinaVision Media Group. In 2014, Alibaba purchased 60% share for $804m and renamed the company. They wanted to improve content for their smart TV and smartphone

In June 2025, Alibaba Pictures changed its name to Damai Entertainment. Its business has expanded from film to a diversified ecosystem including performances, IP commercial derivatives, TV series, artist management, and ticketing platforms.

AliMusic

The music platform was founded in 2015 by merging Xiami Music and Alibaba Planet. They were unable to compete against Tencent and shut down the service in 2021. Prior to this failure, Alibaba went to invest $700m into NetEase Cloud Music in 2019 for minority stakes.

Damai

Damai is China’s largest entertainment ticketing platform with over 170 million registered users, founded in 2004 by Zhou Huilin. It offers ticketing for concerts, dramas, exhibitions, sports events, theater performances, and other entertainment activities. Alibaba initially invested $133m in 2014 and completely bought the company in 2017 with an additional $393m. Damai’s main competitors are Maoyan Entertainment, Piao.com, ShowStart, WePiao.

Orange Lion Sports

Originally known as Alibaba Sports, this entity is an event operator founded by Alibaba in 2015. It operates Hangzhou Olympic Sports Center which served as central venues for the 2022 Asian Games.

It also manages a network of 75,000 sports centers across China.

Lingxi Games

Originally known as Guangzhou Ejoy, the gaming platform was founded in 2011 and acquired by Alibaba in 2017. Lingxi Games operates many high-quality mobile games, including Three Kingdoms Tactics (三国志战略版), Three Kingdoms Fantasy Land (三国志幻想大陆), Ru Yuan (如鸢), Travel Frog (旅行青蛙中国之旅), Forest Kingdom (森之国度), and Dawn of the Wasteland (荒原曙光).

Cloud & AI

Aliyun

Alibaba is the largest cloud computing company in China with 36% market share. It was founded in 2009 and operates globally. Huawei and Tencent are far behind in terms of market share.

DAMO Academy

The DAMO abbreviation stands for Discovery, Adventure, Momentum, Outlook. It focuses on advancing cutting-edge technologies and innovations across several domains, including AI, cloud computing, data science, quantum computing, robotics, semiconductor technologies, and cybersecurity.

Qwen

In March 2023, OpenAI released the milestone model GPT4, and Zhipu AI open sourced its ChatGLM model, which kicked off the beginning moves in the open sourcing of China's large models. Shortly after in August 2023, Tongyi Qianwen (Qwen) announced that it was open source.

Since then, Qwen has been on the “all sizes, all modalities” open source path. The open source models cover multiple categories such as LLM, mathematics, coding etc. The size spectrum was wide, from 0.5B to 110B, meaning that Qwen can provide whatever developers want.

The LLM has seven sizes: 0.5B, 1.5B, 3B, 7B, 14B, 32B, 72B. From these model sizes, we can see that the Qwen team has probably fully considered the different scenario requirements of downstream applications, and thus made the above open source strategy, which roughly corresponds to the three most popular scenarios at the moment: end-side model, small model, and large model. For example, 3B is the best size for devices such as mobile phones.

Since its open source release in August 2023, Qwen has been continuously working on the base model and has opened up all model capabilities for the industry to use. This is supported by Alibaba Cloud’s open source strategy in the era of AI big models.

Ultimately, cloud computing vendors, serving as AI infrastructure, will be the most important providers of computing power for the entire industry.

However, although the concept of open source is elegant, but in an open source community where all models are free and all users can come and go, developers have too many choices. If the model is good, developers will stay, but if the model is not good, developers can choose other companies without hesitation.

T-Head

Semiconductor chip maker subsidiary spun out of DAMO Academy to support self sufficiency. There are plans recently to IPO.

Retail & Others

Hema

China’s largest high-tech supermarket chain, developed by Alibaba Group in 2015. It operates over 300 supermarkets across China and is designed to integrate online and offline shopping experiences, as part of Alibaba’s “New Retail” strategy.

It has several store formats, including Freshippo Xiansheng (盒马鲜生) for fresh and packaged foods, Freshippo Mini (盒马迷你) as a compact store, Freshippo Outlet (盒马奥莱) for budget-friendly items, and Black Label (黑标) for luxury international products.

However, it’s loss making and they are shutting down the membership Hema X stores.

Sun Art Retail

Also part of “New Retail” strategy, Sun Art Retail is a hypermarket founded in 2000 through a JV between Aushan Group and RT-Mart. Alibaba spent $3.6b for 72% stake in this publicly traded retailer.

It operates 500+ hypermarkets, 32 supermarkets, and 7 membership stores in 205 cities across 29 provinces.

This retailer is loss making and at end of 2024 Alibaba sold Sun Art at a $1.8b loss.

Taoxianda

Online-to-offline fresh food delivery service developed by Alibaba in 2017, primarily integrated with Freshippo, Ele.me, Sun Art, Taobao.

The main competitors include JD Daojia, Meituan Maicai, Dingdong Maicai, 7Fresh, and MissFresh.

AliHealth

AliHealth is a specialized platform for digital healthcare services and solutions, founded in 2014 by Alibaba. It combines e-commerce, technology, and healthcare to provide a comprehensive ecosystem that sells healthcare items, including medications, nutritional supplements, medical equipment, and health-related services. AliHealth competes with several major players in China’s digital healthcare and pharmaceutical markets, including PingAn Health, JD Health, Tencent’s healthcare services, and Miaoshou Doctor.

DingTalk

This is a work collaboration platform developed by Alibaba in 2014. Used by over 700 million registered users and 25 million corporate clients. It does things like messaging, video conference, task management, cloud storage, document sharing, and workflow automation.

Vendio & Auctiva

Vendio is an e-commerce software platform that allows SMEs to sell products online through different sales channels, including Etsy, Amazon, and eBay. It was founded by Mark Dodd and Rodrigo Sales in 1999 under the original name AuctionWatch.

Vendio was acquired by Alibaba in 2010.

Auctiva is an e-commerce software platform and eBay auction management system founded in 1998 by Jeff Schlichting. It offers free and fee-based services, including listing templates, inventory management, image hosting, and marketing tools.

Auctiva was also acquired shortly after to contribute to the international expansion.

Shenma

Mobile-first search engine developed by Alibaba and UCWeb in 2014 for the purpose of search functionalities within their other platforms.

South China Morning Post (SCMP)

Another surprising acquisition. In 2015, Alibaba bought SCMP for $266m. A Chinese company buying Hong Kong newspaper?

Alimama

Digital marketing and advertising platform launched in 2007 that provides advertising solutions across its ecosystem.

Umeng

Mobile analytics and marketing platform that provides app developers and organizations with tools and services for tracking, evaluating, and optimizing the performance of their mobile applications. It was founded by Liu Hui and Zhang Xialin in 2009. Alibaba acquired Umeng in 2014 for undisclosed amount.

AI Impact on E-commerce

Firstly, we have to understand that Alibaba is an aggregator. It builds infrastructure that consolidates fragmented supply into one place, as a result captures the consumer. As the number of consumers grow, suppliers will rationally participate on Alibaba’s terms.

Alibaba’s success is not due to best products, but rather a large assortment of products plus it has locked the Chinese consumer into a habit of searching on Alibaba.

This is the fundamental flywheel of the e-commerce business.

An aggregator business model is a combination of advertising, selling visibility on its platform to the suppliers it commoditizes, and margin capture by using its bargaining power to extract favorable terms.

This creates a system where suppliers pay twice, just to be visible once.

To make the aggregator model better, Alibaba must invest in logistics (warehousing, transportation, last-mile delivery). Because Alibaba lacks genuine supply-side loyalty, sellers were captive but have no reason to be committed to Alibaba. If logistics are done well, then the bottleneck becomes consumers’ discovery.

The aggregator model scales exponentially with discovery because each additional customer and supplier makes the ecosystem more valuable to every existing participant.

Now with the arrival of agentic AI, the discovery bottleneck will be changed. Traditionally, users are trained to start their shopping journey on Alibaba, the power of behavior lock-in is strong. However, AI breaks this habit because they don’t have habits in the first place. AI also doesn’t care about UX optimization.

When AI bypass Alibaba’s discovery gate, the advertising revenue is at risk, because the thing being sold becomes less valuable when AI doesn’t express intent within Alibaba’s ecosystem.

We can see this from Amazon actively blocking 3P AI agents from accessing its product data, prices and reviews. The strategic is to protect their ecosystem and the billions of high margin advertising revenues.

But what is AI limited by?

Data legibility!

It’s obvious, AI is a machine that reads machine language. So Alibaba needs to have the most comprehensive, structured, real-time dataset. Fortunately, it owns this walled garden.

Now instead of human behavior lock-in, the game changes to agentic AI lock-in. Alibaba must make its own AI agent the one that everyone uses. No doubt this is harder than before, machine preference is harder to achieve because you cannot hide behind habits and UX design, it needs truly superior outcomes.

How does Alibaba promise superior outcomes?

It goes back to logistics. People will always want cheap, reliable and fast things.

There is also a new source of revenue that might replace advertising. Instead of charging for ads, Alibaba could monetize data legibility — making sellers legible to AI.

If Alibaba is going to make its AI agent the preferred one, then which strategy should it pursue? Open or closed source?

It seems like closed source is a logical one. If humans delegate through Alibaba’s AI, then they keep the e-commerce business alive. But it demands that Alibaba excels in logistics because users can easily switch to another AI agent that queries the internet and escape Alibaba’s reach.

Going open source implies that you believe that agentic AI will not be winner-take-most unlike Google search. This stems from the logic that AI only have requirements, whichever protocol satisfies those requirements will win regardless of the counterparties. Put another way, open source is like building the plumbing — the best pipes are irreplaceable.

Alibaba has committed to the open source model with Qwen. But it’s hard to say which model will emerge as the best pipes.

Capital Allocation: New Retail Case Study

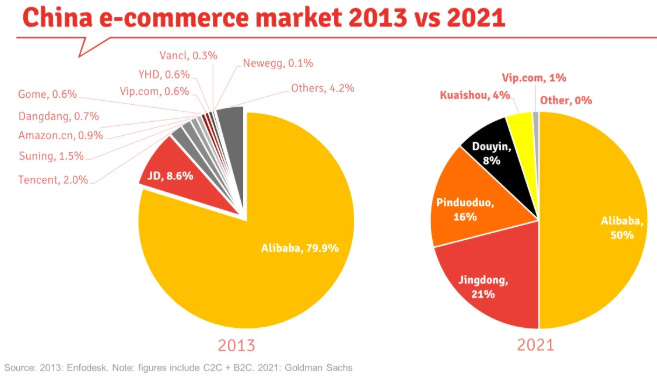

The recent events of restructuring and breaking up their segments into “1+6+N” is the consequence of the bad outcomes of Alibaba’s “New Retail” strategy led by Daniel Zhang, who left the CEO role.

This e-commerce market share report shows how Alibaba ceded share to PDD:

PDD was dismissed as catering to the low-tier cities and low-income groups, but it eventually managed to get branded products on its platform and stole business from Alibaba.

Taobao was key to Alibaba’s early success. In the early days, Alibaba was still a B2B platform, until eBay tried to enter the Chinese market, then Taobao was launched to counter it. But Taobao did not make much money, it was TMall (2008) that brought in the profits through commissions and advertising.

Daniel Zhang was promoted to the President of TMall in 2011 and Alibaba restructured Taobao into 3 separate groups:

Taobao Marketplace (C2C)

TMall (B2C)

eTao (search engine)

However, there was a problem because TMall actually sold stuff that replicated in Taobao. It didn’t make sense for both groups to have two mobile apps.

For many years the split of Taobao/TMall revenues was 2:1. Taobao generated advertising fees, while TMall collected commissions from merchants.

Then in 2014, Alibaba started to expand overseas to find brands that wanted to sell their products to Chinese consumers through TMall Global. This is where the income distribution turned to 70% from TMall by 2022.

As a result, TMall squeezed out Taobao’s smaller merchants as they found it harder to sell and moved to PDD. Alimama, their advertising platform, was supposed to help small merchants but instead made easy money by selling traffic on TMall.

This was when things took a strange turn, Daniel Zhang became CEO in 2015 and Chairman in 2019. He started allocating capital to their “New Retail” strategy, starting with buying the departmental chain store Intime (银泰).

We don’t divide the world into real or virtual economies, only the old and the new. Those who cling on to the old ways of retailing will be disrupted, and brick-and-mortar businesses will be able to create value for consumers if they are integrated with the power of mobile reach, real-time consumer insights, and technology capability to improve operating efficiency.

Daniel Zhang, 2017

Back in 2013, Intime was a brick-and-mortar department store that was slowing down from changing consumers behaviour. They saw Alibaba as a solution and partnered to provide online-to-offline (O2O) transactions during Double 11 (Singles Day). This was also the year that logistics firms STO, YTO, ZTO and Yunda came together to back the Cainiao JV.

In 2014, Alibaba spent $629m for 27.8% of Intime. Then a chain of cooperative moves happened:

In 2015, Intime joined Alibaba’s new location based mobile app Miaojie and went on to integrate into products of Intime stores.

In 2016, Intime’s online supermarket launched on TMall Supermarket.

In May 2017, Alibaba invested another $2.6b and owned 73.7%, after that Intime became a private company. For context, Intime sales in 2017 was RMB6b with about 62 stores in 33 cities, Alibaba paid RMB17.7b for the whole company.

On the bright side, it looks like synergies were everywhere:

Intime offline shopping could be revitalized.

Alibaba could benefit from Intime’s retail network.

Supply chain and big data efficiencies between both.

But if we dig underneath, many Intime senior employees were put in from Alibaba. The founder, Shen Guojun, stepped down from Intime to help establish Cainiao. In the end, the shopping mall business became managed by Alibaba.

These were some of the innovations:

TMall pop-up stores.

Smart nursing rooms for mothers.

Smart Ladies’ Room: Virtual trying on clothes, make-up, and samples from vending machines. They ran a promotion of RMB0.01 on Alipay.

In a Tmall Service Center, customers could book an appointment in the app to have clothes tailored, handbags cleaned, or a watch fixed while they shopped.

Mini-programs on WeChat and Alipay and created a scheduled delivery service, with 80% of its stores able to deliver within one hour.

Despite the COVID crisis, in March 2021, Alibaba published a glowing article about how well Intime was doing with New Retail:

We were lucky to come out on top of this crisis thanks to years of digital innovation and transformation. At Alibaba, we always say believing is seeing instead of the other way around.

For Intime, everyone from CEO to store staff embraced digitization very early on, when few believed in the power of new retail.

Yan Xuekun, Intime CTO

But this is not true.

From 2016 to 2019, Intime invested more than RMB100m annually in digital transformation, with budgets increasing every year. However, the new retail format that Alibaba envisioned was never fully built, and Alibaba’s strong online channels drive very limited traffic to Intime.

Furthermore, Intime Retail established an MCN (multi channel network) company in 2021, attempting to cultivate offline sales staff into online livestreamers and leverage Tmall for growth. However, after three years, their MCN company has failed to cultivate a single top-tier livestreamer, and its performance remains mediocre.

In a 2018 interview, Intime CEO Chen Xiaodong had conflicting expectations:

Jack Ma says it takes 12 years, and we’re two years in. I think too many people will overestimate what we can change in one or two years but underestimate the changes possible in a decade.

A lot of people chase me every month, every quarter for updates, but it’s just not realistic. Here’s an example: A supermarket has just 5,000 SKUs. A department store like Intime has 50 million SKUs per season. And there are four seasons a year. Think about everything we need to do to digitize that. It’s a huge challenge, but we’re working to figure it out. We think the supply chain is the most important thing to work on.

It’s true that not everyone believes in New Retail. Our goal is to have 400 stores in five years and a thousand in 10 years. We’re only at 60 right now. But it’s like Jack says, most people need to see the future before they can believe such things are possible. But for us, we believe in the future and make it happen.

In 2024, after more than 5 years, Intime has shrunk to 50 stores. Now they have only 27 stores. The trend of retail stores failing from e-commerce pressures was inevitable. At least 11 department stores in China closed down in Q1 2023, including well-known names such as Pacific (太平洋百货) and New World (新世界百货):

Intime was eventually sold in December 2024 at a $1.3b loss.

Qinchengli (亲橙里) was another New Retail experiment.

Alibaba opened its 40,000m² shopping mall on 28 April 2018 next to its Xixiyuan in Hangzhou. The building had seven floors including two underground, housing Hema and 700 parking spaces. It had a cinema, gyms, educational institutions and lots of catering facilities from Alibaba’s Koubei platform.

The mall had 8 different New Retail initiatives upon its opening:

Hema store in the basement.

TMall Global.

TMall Genie (smart speaker).

Taobao Xinxuan (淘宝心选) launched by Alibaba in 2017, is a curated, private-label lifestyle brand focusing on high-quality, minimalist, and affordable daily necessities (similar to Muji).

MISHOW (谜秀) a women’s clothing store with a virtual mirror.

Taobao 2D.

Alibaba Small Kitchen (阿里小厨).

Second V Palace (a shop with products largely based around internet memes and emoticons).

The Tmall Global store’s assortment was based on consumer consumption data from a 5km radius around the mall. If ordered before 2pm, consumers could also arrange same-day delivery or pick-up from the stores in the mall. Meanwhile, promotionals discounts on parking fees would be automatically settled when making purchases. The parking lot also offered AR-enabled reverse car search.

One year after Qinchengli’s opening, some of the Alibaba-related stores had already disappeared. Only Taobao Xinxuan, TMall Genie, Hema, and MISHOW remained.

By 2023, only Hema in the basement and a small Xianyu pop-up store remained.

Dianping data shows that Qinchengli currently has 84 stores, of which 56 are food and beverage establishments (there are at least 11 coffee and milk tea shops), accounting for 67%, while the remaining stores are retail, lifestyle and entertainment facilities. When it’s not meal time, there are no shoppers.

What remained of New Retail strategy was the mascots:

That’s not the end of the New Retail story!

Alibaba buying spree extended into equity stakes in furniture and supermarket companies:

2019: RMB4.4b convertible bonds + 3.7% equity. Total (if converted) 10% stake in Red Star Macalline (RSM) (红星美凯龙).

2018: RMB5.45b for 15% stake in Easyhome (居然之家).

2016: RMB2.1b for 32% stake in Sanjiang Shopping Club (三江购物俱乐部).

2017: RMB0.5b for 18% stake in Lianhua Supermarket (联华超市).

RSM shares collapsed 75% since then:

Easyhome earnings fell after 2020 as China’s property market slumped. In 2024, Easyhome had about RMB4.3b short term loans due within 1 year but only RMB2.2b in cash. Despite this, Wang Linpeng (CEO, founder) began to monetize its assets by selling shares and increasing dividends. In 2023, he pocketed over RMB2b from equity sales and distributed more than 90% of net income as dividends from 2019 to 2023.

He was then detained by Wuhan’s Jianghan district authorities, and his remaining 372 million shares in Easyhome were frozen. Then he died on 19 July 2025, rumoured to have jumped to his death.

Alibaba’s equity investment fell off a cliff too:

At the end of 2023, Alibaba transferred RMB1.05b of RSM shares and RMB2.05b of Easyhome shares to Hangzhou Haoyue (杭州灏月). Compared to the RMB11b initial investment, the total transfer of RMB3.1b showed how much value was destroyed.

This Hangzhou Haoyue entity was newly created by Alibaba just earlier on 24 October 2023.

Alibaba also transferred shares in logistics company YTO Express, cosmetics retailer Liren Lizhuang, advertising media company Focus Media, smart security company Qianfang Technology, and physical examination chain Meinian Health.

Together, Alibaba transferred 7 companies worth RMB19.4b to Haoyue. By 2025, Haoyue has cashed out over RMB3b through selling shares. Clearly, capital allocation in New Retail was not paying off, so they wanted to separate loss making investments from its main e-commerce business. The statement on the transfers:

In order to realise the independent development of Alibaba Networks’ main business and non-main business, each company has its own business, employees, improve operating efficiency, further achieve asset value preservation, appreciation and sustainable development, and build a competitive enterprise.

The last two investments (Sanjiang & Lianhua) did poorly as well.

There’s much more other details involved in this New Retail move (Hema, Sun Art) but they tell the same outcome.

In short, retail in China is super competitive and pricing is irrational. “New Retail” initiative was bad capital allocation.

This funny quote from Buffett describes the situation well:

Many managers apparently were overexposed in impressionable childhood years to the story in which the imprisoned handsome prince is released from a toad’s body by a kiss from a beautiful princess.

Consequently, they are certain their managerial kiss will do wonders for the profitability of the acquisition target. […]

We have observed many kisses but very few miracles. Nevertheless, many managerial princesses remain serenely confident about the future potency of their kisses — even after their corporate backyards are knee-deep in unresponsive toads.

Investment Portfolio

This is another way to look at how Alibaba performed on their capital allocation. The results were quite bad:

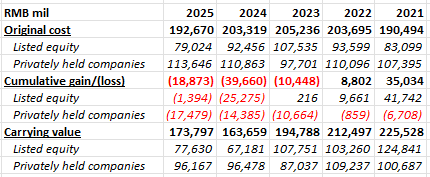

Cumulative gains in listed equities went from RMB41.7b in 2021 to a loss of RMB1.4b in 2025. That’s a RMB43b loss over 5 years.

Privately held companies didn’t do well either. Cumulative losses went from RMB6.7b to RMB17.5b.

On total, the swing was from RMB35b gains to RMB18.9b loss! We can’t tell how much of this RMB54b loss is realized and unrealized. For context, their equity capital of RMB1,087b, it’s about 5% drag.

It seems like these losses don’t deter management from continuing to put money in. Over the past 5 years, they have put in RMB31.4b of fresh funds:

Consolidated Entities

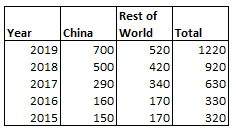

If you read through all that, then you would have noticed there were many acquisitions. All these are consolidated entities and we can see their increase since 2014 IPO.

But if you go to the section “Organization Structure” note in their 20F filings, for some reason they stopped disclosing the numbers after 2019. This was the reason given, but the definition had already existed before:

Other subsidiaries and consolidated entities of Alibaba Group Holding Limited have been omitted because, in the aggregate, they would not be a “significant subsidiary” as defined in rule 1-02(w) of Regulation S-X.

What’s clear is that the number of subsidiaries rose sharply after 2016. Note that most of Alibaba’s business is conducted in China, yet the “Rest of World” number of subsidiaries (primarily in tax havens countries) have significantly increased.