Study: Airbnb

History

Airbnb (ABNB) was founded in 2008 by three roommates and former schoolmates: Brian Chesky, Nathan Blecharczyk and Joe Gebbia.

Brian Chesky and Joe Gebbia have the most interesting backgrounds, their friendship started from Rhode Island School of Design in 1999. Both of them were close buddies and Joe always wanted to start a company together.

As a young enterprising design student, Joe would go on to create Critbuns during his school days, which were sitting cushions that look like this:

These cushions actually became quite popular and after college he was selling his product. Meanwhile, Brian took on a job at an industrial design firm and moved to Los Angeles.

Back in San Francisco where Joe lived, he was thinking of other better businesses to do and finally when two of his roommates moved out of his three bedroom apartment, the opportunity dawned on him.

Brian had a secure corporate office job but was fed up with it and so he made the leap and moved into Joe’s apartment. He didn’t have much money saved up but the apartment had an extra room, and so they tried to rent it out for a few days to make up for the shortfall by providing air mattresses. At the same time, there was an art design conference coming up and they knew people will be arriving in San Francisco.

Both friends mocked up a website and called it “Airbed & Breakfast” with the idea that some starving artist who wanted to travel cheaply and attend this conference will take up their offer of $80/night.

They were able to get 3 travelers to stay with them and that was kind of the first Airbnb experience, even though it wasn’t called that at the time. However, they moved on to different business ideas and eventually both of them were struggling to come up with good ideas. There was this music festival South by Southwest (SXSW) that was coming to town, they figured out there will be a shortage of rooms and the ability to rent cheaper rooms will be a selling point.

So they recruited Joe’s prior roommate, Nathan Blecharczyk, who is a skilled software engineer. Nathan was able to pay his way through Harvard by making marketing software throughout high school. This was the start of the three founders.

The trio relaunched Airbed & Breakfast with only 2 customers, one of whom was Brian himself. Reception was horrible but they tried to raise funds for this idea: 10% stake worth $150,000. Not only were investors not interested, they were actually repelled by it. They recalled meeting one investor who in the middle of it made an excuse to put money in the parking meter, instead he left his half-drank smoothie on the table and never came back.

In 2004, President Obama was set to speak at the DNC in Denver. The founders thought it was another great opportunity to test their product because alot of college students who are price sensitive were going to attend. At that time, they had personal debts of over $20,000 and they weren’t getting anywhere with fundraising. So another idea came up: selling breakfast along with stays. They went to buy the cheapest Cheerios at a discount store and had someone print their private labels across the cereal boxes.

Crazily enough, the breakfast cereals actually worked; they were able to sell the packages of cereal for $40 each and made $30,000. They then cleared their debts and set their sights on President Obama’s speech. This episode was the reason why Paul Graham, founder of Y Combinator (YC), went with ABNB. He thought it was a great idea not because it would revolutionize the way people travelled, rather he was impressed by the grit of selling cereals to continue the business. If he had to bet, these were the people he was putting his money on.

In this Obama event they managed to list 800 rooms in Denver and 80 guest bookings were done. But they started to realize that the past successes depended on events and free marketing because this idea was so novel that online blogs would write about it. Instead of just making it event focused, they wanted a platform that facilitated bookings in any home anywhere.

Out of desperation to invent such a product, Brian decides to apply to YC. Paul Graham was convinced more by their determination to not die than the business proposition. The outcome was Sequoia invested $585k alongside a few other smaller investors, valuing ABNB at $2.4m. At this time ABNB was making revenues of $10k a week on about $100k of booking volume (take-rate 10%).

In 2009, they changed their company name from “Airbed & Breakfast” to “Airbnb”. By 2010, ABNB was achieving 800% growth and Sequoia put the company at $100m valuation. The business had 800,000 nights booked, it was becoming very popular.

In November 2010, ABNB raised their Series A funding of $7.2m from Greylock Partners (led by Reid Hoffman who founded LinkedIn). The reason why venture capitalists were keen to fund ABNB was because Brian Chesky worked hard on his business, going to hosts’ homes to take photos on their behalf and upload them. Payment was also done manually, by collecting and remitting cheques. It was the willingness of these entrepreneurs that would make it possible for ABNB to bloom.

In 2011, ABNB booked more than 2 million nights and had presence in 100 countries, their website was getting 30 million monthly visitors! The business model was very simple: ABNB charged hosts 3% and guests between 6-12% of booking value, plus cleaning fees. Marketing expenses were low and most of the popularity was achieved through word of mouth.

That year, ABNB became a unicorn with a $1.2b valuation. However, their first big disaster would hit when a host was robbed and her apartment destroyed. Brian Chesky’s lawyers told him not to apologize because ABNB was not really responsible, but if he apologized, then it will open him up to liability. He listened to the lawyers and issued a statement which backfired.

Realizing his mistake, he released a statement begging for forgiveness:

I’m sorry. I feel horrible about what happened to this woman’s home. And I’m going to write an open letter and I’m gonna apologize to her. We’re gonna take responsibility and we’re gonna try to make things right.

Brian Chesky’s apology, 2011

Shortly after, ABNB rolled out a policy to reimburse hosts up to $50k in damages. They have continued to improve this guarantee and currently offer up to $1m of coverage.

This stumble didn’t stop ABNB from growing and by 2013 they were valued at $2.9b. A year later, valuations went up to $10.5b, with over 300,000 rooms available they were basically surpassing some of the biggest hotel chains.

By 2016, ABNB was worth nearly $31b with 3 million rental rooms. Brian decided to expand their products by doing flights, because people book a flight before a stay, so if they were able to capture the customer at flight purchase stage, they could direct them to ABNB. This idea didn’t materialize. But they did roll out “Experiences” which didn’t become important until recently.

We are getting closer to their IPO date. By 2019, gross booking value was $38b and ABNB processed 325 million rooms annually. Unfortunately, COVID hit before they managed to go public. The pandemic sent ABNB sales down -80%, they had to refund guests which angered the hosts because ultimately the hosts were the ones losing that potential income.

To tide through this crisis, ABNB borrowed $1b at 10% interest. This showed how cautious investors were and how little faith they had in the future of ABNB, instead of raising capital they had to incur debt. Management laid off employees and executives started to take pay cuts. Marketing expenses were cut to zero.

By end of 2020, they managed to IPO at $68/share, giving ABNB a $47b valuation, raising about $3.5b in the process. During this period, the stock market was hot with post-COVID zero interest rates, and in the same day, their newly listed stock shot up to $144.

Their wildest dreams came true; all three founders were worth more than $10b each at this point. Post-COVID, travel recovered quickly and people started to shift towards longer stays. ABNB was well positioned to capture this.

Brian Chesky remains the CEO today. Nathan Blecharczyk is the Chief Strategy Officer and chairman of Airbnb China. Joe Gebbia remains on the Board of ABNB but is no longer involved in operations since 2022.

Business Model

Being a two-sided platform, ABNB benefits from network effects where more suppliers (home stays) are attracted to the platform when there is strong demand (travelers). The feedback loop is self-enforcing. The more travelers use ABNB, the more home stays it attracts, and competition will drive down prices offering the best value for travelers.

ABNB sits in the middle as a platform without owning any of the inventory. They take a cut from the listing price, this take-rate was ~11% in 2015 and has increased to ~13% today. The exact formula on how ABNB calculates the fees for both buyer and seller is undisclosed.

Revenues are recognized after someone goes into the accommodation and funds are released to the host, usually after 1 day for the guest to complain if the home is a scam.

ABNB is the typical marketplace model. So to get more revenues, it can grow gross booking value (GBV) and/or increase take-rates. The small 2% increase over the past decade has more to do with payment processing and FX fees, and so management has not talked about raising the take-rate.

Their focus is on trying to grow GBV and provide more services. This strategy is actually quite different from marketplaces like Etsy and Amazon which have quite high take-rates, although you could argue that Amazon provides logistics and advertising services.

To grow more GBV, they have to make people love the platform, so the management team is very cognizant of that and want to design an experience that has low friction. One obvious comparison is to see the user interface (UI) between ABNB and Bookings. Generally, when people use ABNB they have a sense of exploration, and so the UI is kept clean to aid the user. Going to Bookings, people usually already have an idea of where to stay and what they want; the UI has much more filters and buttons to narrow down choices.

By region, America is the largest contributor to revenues at 45%. Second goes to EMEA (mainly Europe) at 37%. LATAM and APAC both are about 6% and 9% respectively.

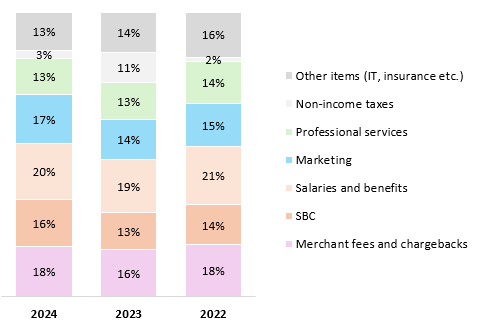

Operating results improved drastically from losses prior to 2019 to profits of $2.5b in 2024 (23% margins). The cost structure looks like this:

At maturity, we think that operating margins can be much higher because ABNB could tune down marketing expenses without hurting sales. Also, this is a very capital-light business with low maintenance R&D expenses.

Total Addressable Market (TAM)

There’s many differing sources of TAM which we don’t know how they sourced their numbers, so we will estimate ourselves using Marriott’s global average daily rate (ADR) of $190. Note that this is higher than ABNB’s ADR of $172.

There were about 9.5 billion passengers in 2024, that’s a GBV of $1.8t. If the take-rate is 13%, then revenue TAM for ABNB is ~$230b. We don’t think it’s important to get this figure precisely, we just need to know travel accommodation is a huge market.

In fact, 2/3 of markets where ABNB exist, there isn’t even a hotel (source: Q3 2023 earnings call). So if we think about it that way, there’s many markets where hotels don’t have a presence.

Competition

OTAs (Online Travel Aggregators)

OTAs are the strongest competitors that steal online traffic away from ABNB. Particularly, Bookings and Expedia are very important direct competitors in this “alternative accommodation” space.

OTAs aggregate hotel listings and charge hotel owners a commission for each sale, they become very useful when the market supply is fragmented, for example in Europe where there are many small boutique hotels.

Bookings very first mention of ABNB came in Q2 2011 earnings call when they concluded that ABNB was not really competitive to hotels. Then the topic came up again in Q1 2014, Bookings talked about renting out entire vacation homes and by the end of 2014 they had 150,000 units in this category and over 4 billion vacation rentals booked. They are taking it seriously now, rolling out a separate site called villas.com. By 2015, Bookings thought that it was a high priority for them to build out more unique accommodations. However, in 2016, villas.com was shut down because they were cross-selling the same listings on the main booking.com site.

It’s inefficient for these individual hotels and apartments managers to run their own advertising campaigns, so they are going to outsource and join the major OTAs who have the most customers. Once they join, it is quite hard to leave, because these OTAs have huge amount of resources to drive online search keywords. They will go ahead and bid for keywords and get the top result. In fact, Bookings is likely Google’s biggest customer spending $7.3b on performance marketing (2024), a large portion of that is going to Google search.

A disadvantage OTAs have against ABNB is their need for recurring marketing expenses, OTAs need a massive marketing budget. ABNB’s traffic to their site is predominantly organic. People go directly to the site to search because they want to, nobody goes on Google to search specifically for Airbnb stays. Hence, their marketing budget is arguably discretionary.

Grooming the Airbnb brand is much more important than performance marketing. This reliance of OTAs to Google is a risk because we never know what’s the advertising environment going to be in the future with developments of AI.

OTAs have 2 types of models: agency and merchant. The agency model acts as an agent on the hotel’s behalf (just like a site listing), where the hotel still sets the price and collects the money. The benefit is the customer deals directly with the hotel and the relationship is captured by the hotel directly.

The merchant model negotiates a block of rooms at a discounted price, then leveraging on their data they can mark up/down the prices of the rooms. Sometimes hotels set a price too high and OTAs can come in and resell it. This model captures customers for OTAs too.

On the UI side, we also mentioned earlier that ABNB differentiates itself by aligning the UI with the user’s intention to explore, providing recommendations, comparisons to different cities etc.

For OTAs, the UI is utilitarian with promos designed to optimize for the best price since people already know exactly what they need.

In the world of OTAs, the room is a necessity but never a reason to travel. But that’s not the case with ABNB.

Fun fact: Expedia was invented by a division in Microsoft way back in 1996.

Hotels

Hotels in general provide a different type of experience to travelers, focusing on consistency. Some people prefer a high quality experience that they can expect to be consistent and convenient. ABNB is not built to compete on consistency, they have millions of individual homes and it’s impossible to make every experience similar.

However, 90% of stays in the US market are actually in hotels. They have also tried to compete with ABNB directly, for example, Marriott has a segment called Homes & Villas which is their version of peer sharing platform of high-end homes. But they only have 140,000 listings versus over 8 million for ABNB.

Well established hotel franchises like Marriott and Hilton have managed to depend less on OTAs and compete directly with ABNB. They run their own loyalty program which customers can very easily go directly to them for the best prices. They also have over 30 different hotel brands with differing price points and qualities. For a traveler who is on their loyalty program, it is very likely that they will choose the hotel over ABNB.

A disadvantage to hotels is the need for quality maintenance to keep customers happy. ABNB doesn’t have that cost pressure, if a traveler books a badly furnished home, chances are they will just accept it. Anyways, these homes are user-rated so the bad ones will naturally go down the rankings.

ABNB recognizes that they need to be more aggressive in the hotels market. Given that their take-rate is very competitive, and a huge portion of hotels in Europe are independents, it would benefit high-income young American travelers which the ABNB brand has some influence over.

Managed Apartments

These are property managers who list on ABNB and try to take the customer off platform. This is the weakest source of competition because of 2 main reasons:

People usually don’t book the same vacation rental place a second time. The chance of recurring sales is quite low.

People want a trusted entity like ABNB to hold their payment in case something goes wrong. The property manager who wants to go direct has to give a discount to “buy” trust.

There are certainly trustworthy places but these apartment managers won’t pose a significant threat because it is difficult to scale. Think about how difficult it is to aggregate homes across different countries/regions, run their own ads and still offer cheaper prices.

Hosts Dynamics

A big portion of ABNB hosts are individuals, and majority of them only list exclusively on ABNB. They don’t cross-list across other platforms. The reason is cross-listing introduces complexity, the host has to worry about pricing on multiple sites and have a calendar system that syncs.

Professional property managers have the necessary software to do this, but the individual host does not. These hosts are not focusing on maximizing profits, they are just trying to make some extra income from their extra rooms/homes. It’s usually not their full-time job.

For that reason, ABNB platform is attractive to individual hosts. ABNB has made the process much simpler to do than VRBO (even though it has less fees). The number of reviews and inventory on VRBO are also lesser. From a host perspective, occupancy rate is a bigger revenue driver than saving on commissions. So with lesser traffic on VRBO, the network effect of ABNB makes it difficult for hosts to switch platforms.

Weaknesses

Loyalty

ABNB doesn’t have a loyalty program although Brian Chesky thinks that “if you need a loyalty program, then you don’t have loyalty in the first place”. Management thinks that this is not a priority but there is certainly the possibility of cross-selling through loyalty programs.

Regulation

Many places regulate in favor of individual hosts who own their homes and are renting out part of it. The regulations hit hardest on property managers who turn community residential areas into a business.

OTAs are not affected by this because hotel bookings will always be there regardless of regulation. ABNB has no alternative against this problem, except for a small acquisition of HotelTonight, a company that focuses on last-minute hotel bookings. They bought the company in 2019 for $450m and its operates on its own app. In April 2025, travelers in the US and UK who book hotels through HotelTonight can now earn 10% of their booking value in Airbnb credit, this is a small step towards a loyalty program.

Regulation is quite stringent in countries like Japan. In September, Osaka governor Hirofumi Yoshimura announced his intention to stop the Special Zone Tokku Minpaku (特区民泊) program, which allows short-term rentals, such as those on Airbnb, under relaxed rules. Yoshimura justified his position by stating that the supply of hotels has caught up and that there is too much community backlash. The city has already frozen new applications. Local residents are pushing back due to concerns about trash, noise, and absentee management.

The problems are much deeper as 45% of Osaka’s operators are affiliated to the Chinese. This high proportion of foreign ownership is controversial in Japan. The area of Naniwa Ward in Osaka ranks top in residential land price inflation in the Kansai region, it’s believed to be driven by these business practices.

New Expansions

ABNB currently has 3 strategic priorities:

Perfect the core service.

Accelerate growth in global markets.

Expand the business beyond stays.

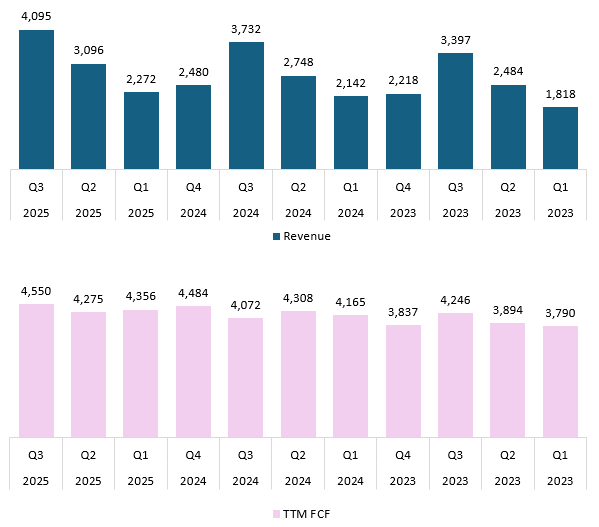

Due to this we think that management is not looking to monetize the business anytime in the foreseeable future. Plenty of R&D and marketing dollars will be spent to achieve their goals, whether or not these reinvestments will yield high returns remains a question. So far revenues and free cashflows have been growing decently:

Experience Segment

This is a relaunch of an initiative that started in 2016. It is basically a local guide who will bring travelers around and give them a tour for a fee. It’s an effort to cross-sell with a take-rate of 20%.

If you take a look at your local Experience, the prices are not really cheap. Since we don’t have reported numbers, we can’t tell if this segment actually material for ABNB.

ABNB take on reputational risk if the traveler has a bad Experience, so they need to screen for quality.

The input is that we actually vet every single Experience on Airbnb where it comes on the platform. We do not vet every home the way we vet every Experience on Airbnb. The result of that is that the average home has got a 4.8 rating. The average Experience has a greater than 4.93 rating.

We built a fairly sophisticated operation to do vetting. The first thing we do is we vet their profile, make sure everyone’s got a verified identity. We vet their credentials. There’s a number of third-party sites we can use for that. And we also make sure they have right certifications and licenses, which I think is really, really important for all these nascent different industries.

But we think we can be very, very efficient with this vetting approach. And we ultimately think that this could actually make the market more effective because quality is critical to customer satisfaction and building trust and people really trying something new on Airbnb.

Q2 2025 earnings call

There is also potential to tap into local demand.

Services Segment

ABNB also launched this new Services segment to compete with the things that hotels have. For example, travelers can hire a chef, photographer, fitness coach or hosts can hire cleaners. If they can create marketplaces for these things, then they could sell it to anyone, it doesn’t have to be confined to travelers/hosts.

About 10% of bookings for Services are actually from locals or people nearby. This is less than the 40% for Experiences.

This is where ABNB is trying to get closer to a “super-app” ambition. The idea that once their platform has a customer info and trust, it’s very easy to start cross-selling different services.

This strategy is popular in China with companies like Meituan. They offer other services beside food delivery, and they have tentacles into hotel bookings too. However, Meituan started with a high frequency food delivery business before adding other lower frequency services. ABNB is doing the opposite, booking stays is a low frequency service and it will be difficult to drive high frequency habits in other services.

Since launch, over 60,000 people have submitted applications to host a Service or Experience. Management believes both segments are scalable.

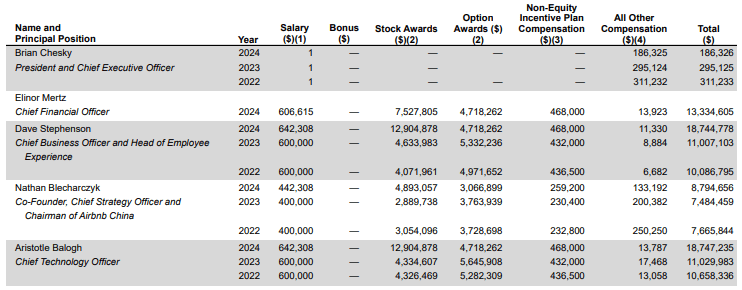

Incentives & Ownership

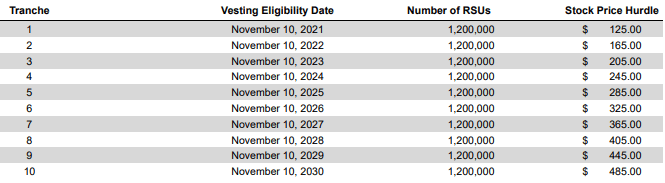

Brian Chesky continued to take a symbolic $1 salary and no stock options. However he is rewarded shares in 10 tranches if ABNB stock price surpasses the hurdles:

The other executive team members receive significant amounts of SBC:

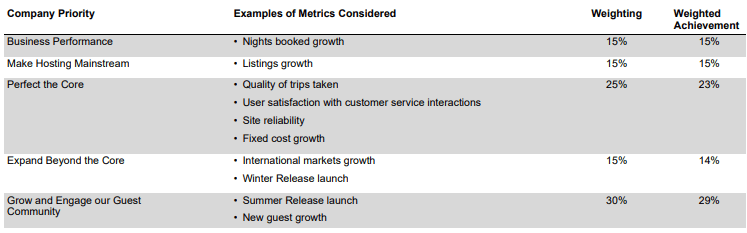

Management KPIs are:

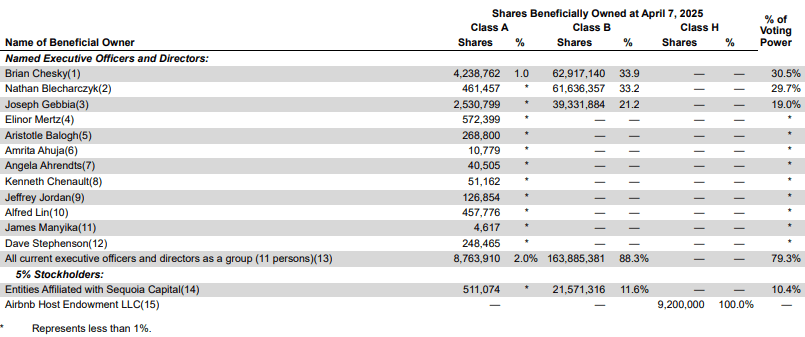

Insider ownership is high at 79.3% voting rights under all executive officers and directors. The three founders still hold significant amounts, with Brian Chesky having 30.5%, Nathan Belcharczyk 29.7%, Joe Gebbia 19%.