Study: Advanced Auto Parts (AAP) Problems

Industry Intro

We have a position in Autozone (AZO) and have admired its largest competitor O’Reilly (ORLY) from the sidelines. Readers can refer here for a good introduction to AZO. See here for economics of auto parts retailing in general.

The ideal capital cycle opportunity for us has often been one in which a small number of large players evolve from a situation of excess competition and exert pricing discipline.

The US aftermarket auto parts industry is a good example of this.

In the early 2000s, the auto parts market was fragmented and regional. Since then, it has gone through an acquisition-driven consolidation around a few notable large players who make up the majority of the US market.

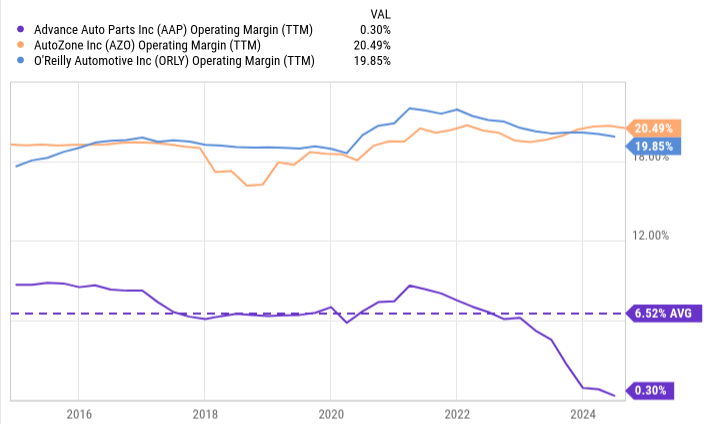

The top two players, AZO and ORLY, have been profitable every year since going public in the early 1990s. In about 25 years, they doubled EBIT margins from 10% to 20% today. As we know, this industry is characterized by decreasing units sold, because technology improves car parts and makes them more durable. Yet improving margins shows their immense pricing power.

In fact, AZO margins increased every year through the 2008 GFC!

The industry has a unique barrier to entry given the large count of SKUs demanded by customers. ORLY supplies same-day or overnight access to an average of 153,000 SKUs. Even the third largest player, Advanced Auto Parts (AAP), manages 75k to 85k SKUs in their hubs. This is a key reason the industry incumbents have been able to maintain pricing power.

Even with the recent tariffs, while 45% of auto parts are sourced from China, the industry still maintains their margins profile. When drivers can’t afford to replace their old cars, they must replace faulty parts, there’s no alternative.

AAP Problems Summary

AAP has been disappointing despite employing the same acquisition strategy, their historical average EBIT margins is only 6.5%. But it’s not a surprise when we look at their acquisition integration process.

A few years ago, AAP had 4 different ERP systems, 2 separate supply chains, and high employee turnover. Whereas ORLY and AZO can offer same-day delivery, customers of AAP suffer from long waits and out-of-stock parts. Even with such lackluster operations, AAP is still making operating profits, which is a testament to the strength of the industry.

Notice margins fell drastically in the past few years? This follows former CEO Tom Greco’s multi-year plan to modernize systems and consolidate the supply chain. He came from Pepsi and P&G, so he borrowed the ideas of a two-tiered distribution model from consumer products industry. This doesn’t work in auto parts where the most efficient distribution model is a hub network which focuses on placing inventory closer to local markets to enable faster fulfillment.

Eventually, Greco was replaced by Shane O’Kelly in September 2023, who has an extensive background as CEO of distribution companies and a military past. Over a year since his start, he has executed a strong plan that included the sale of Worldpac (subsidiary) for $1.5b, a reorganization of the team, and the start of a conversion of the supply chain to the industry standard hub and spoke model.

AAP has already seen significant improvements in customer experience, including SKU availability and service time. If executed properly, his restructuring plan has the potential to finally position AAP competitively.

O’Kelly has provided expectations for the next few years, guiding a return to 7% adjusted operating margins by FY2027.

Business Model

AAP sells aftermarket auto parts to both professional repair shops and DIY customers through retail stores, online sales, and commercial delivery to professional mechanics.

As of October 2025, AAP operated 4,297 stores, 814 of which are franchised Carquest stores that cater to professional mechanics. AAP claims that more than 75% of their store footprint will be in designated market areas with the number one or two positions based on store density. Their revenue mix is split around 50% professional and 50% DIY.

Operational Failures

AAP acquisition strategy started out good. Its first major acquisition was getting Western Auto in 1998 from Sears with its 600 stores. They cleaned up 100 unprofitable stores, promptly converting them within 1 year into Advance Auto Stores format. More importantly, this acquisition came with wholesale distribution network which supplied professional customers.

Next came the Discount store acquisition in 2002 with 600+ stores, but this time with strong exposure on DIY customers especially in Florida. AAP used the same playbook to convert these stores and integrate its distribution, they gained massive bargaining power while improving lead times in parts availability. AAP expanded stores count from 650 in 1996 to 2,500 in 2002 while achieving 7% same-store sales growth, resulting in revenues growing 5x.

After 2002, many acquisitions led to integration challenges. In particular, the acquisition of General Parts International (2014) left AAP with 2 separate supply chains and incompatible systems.

Under previous CEO Tom Greco, who joined in 2016, there were many signs of pressure from this operational mess.

Having worked on updating systems, Greco announced and hosted a call for a “Strategic Update” in 2021. Greco planned changes that included consolidating the supply chain to a two-tiered distribution center model and aimed to reach 10-12.5% in operating margins by 2023.

However, actual operating margins went down instead. Two activists investors (Third Point and Saddle Point) took board seats to push for changes and then replaced Greco.

Turnaround Plan

Enter Shane O’Kelly who was previously CEO of HD Supply, a distributor of maintenance, repair, and operations products owned by Home Depot.

Before that, he was CEO of PetroChoice, the nation’s largest distributor of lubricants. In the past, he was also CEO of AH Harris, a specialty construction supply distributor. Clearly, he was the desired person to fix the supply chain problems.

AAP embarked on a 5 step plan:

Sell Worldpac and Canadian businesses (they changed their mind on selling Canadian subsidiaries).

$200m of cost cut by eliminating redundant roles and a reinvestment of $50m into employee retention in 2024.

Organization structure changes.

Close underperforming stores.

Consolidate supply chain.

Worldpac was first to go. It was acquired through General Parts International and ran its own systems, so it had been problematic. They sold it to Carlyle for $1.5b at 15x EBITDA, and reinvested into employee retention.

The management team has also been revamped and includes a new CFO, Chief Accounting Officer, Chief Data Officer, and Chief Merchant.

Antiquated systems like the POS and warehouse management systems are in the process of being updated.

Most importantly, he is driving the reorganization of the distribution system into the hub-and-spoke model employed by AZO and ORLY.

AAP closed over 500 underperforming stores and 200 franchisees. Additionally, the supply chain structure appears to be finalized. Originally operating 38 distribution centers, the plan consolidates to 12. Along with that, the supply chain will have 60 market hubs by mid-2027. Less distribution centers and more market hubs will improve SKU availability; exactly what customers want.

Management expects 2-3% operating margins excluding restructuring costs in FY2025, and hopes to get 7% by FY2027.

Inventory Turn

AAP has a inventory turnover of 1.7x while AZO and ORLY is much higher at 2.7x. Since auto parts stores enjoy high margins, the impact of weak inventory turnover is more significant than product margins.

The key is to recognize not just inventory days but inventory quality. Holding a large inventory makes sense if you can negotiate high payable days to lower working capital.

ORLY has improved its payable days from 120 days to over 300 days.

AZO cares less about payment terms and more about cost containment, requiring its vendors to notify them within 90 days of any cost increase.

AAP has suffered from weaker bargaining power that is mostly attributable to their poor execution.

This shows up in the negative cash conversion cycle for AZO and ORLY, but for AAP cash is tied up in operations for ~49 days.

Franchise Disadvantages

Auto parts supplies could come from both OEM and re-manufacturers. The latter is taking a core part and refurbishing it into new conditions for parts replacement, and finding a core to replace is not easy, adding uncertainty to the planning process.

Suppliers care about plant utilization, and hence depend heavily on the demand forecasts of auto parts retailers. AZO and ORLY have advantages in this area due to fully owning all their stores and can leverage on a centralized data coordination.

AAP operates some franchise stores (Carquest) in Canada and America, which come with the disadvantage of franchisees not carrying enough inventory and not being trusted by vendors on the supply forecast. This feeds into weaker supplier relationships.