SE: Sea Ltd (2)

Read about SE history, business model and competitive dynamics here. This post updates for Q2 2025.

Q2 2025 Update

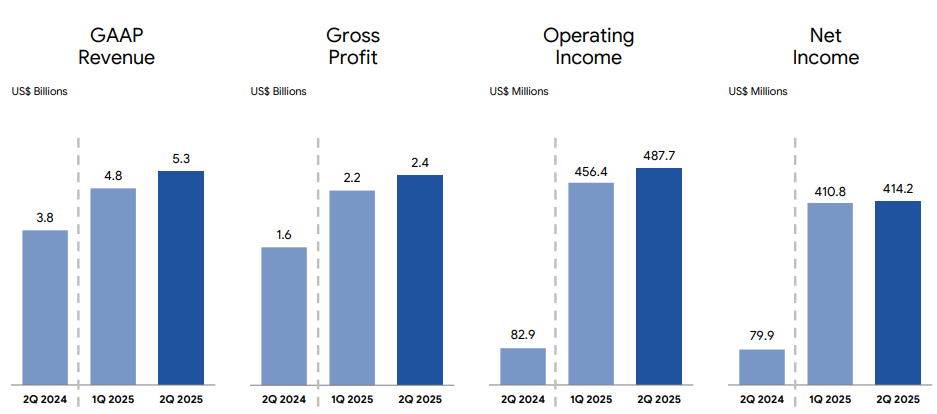

SE reported an astounding good result for Q2 2025, further solidifying the profitable growth story.

In terms of revenues, Shopee is the biggest with 71% share, while Monee and Garena account for 17% and 12% respectively.

Garena still brings in the most in terms of profits with operating income of $276m in Q2, compared to $243m for Monee and $155m for Shopee.

But as the profitability of Monee and Shopee continues to ramp up, it is expected that Garena will eventually become the least profitable segment soon.

There are close synergies between Shopee and Monee since a large majority of Monee’s revenues are earned from Shopee users and merchants. This resulted in Monee to grow at incredible rates, in just 23 quarters revenues grew from $3.2m (Q4 2019) to $883m (Q2 2025)!

One thing to take note for Q2/Q1 comparison: Chinese New Year and Ramadan fell on Q1 this year, so there will be seasonality effects.

Shopee

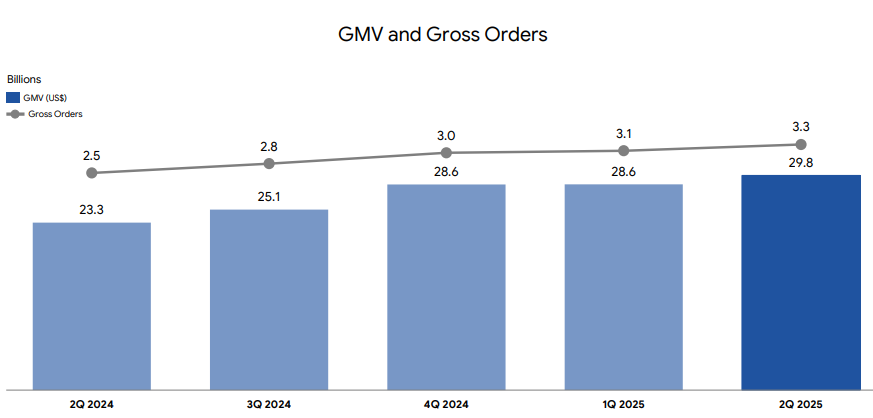

Shopee continued to grow GMV strongly, with Q2 at $29.8b, meaning we are very likely to see a FY2025 GMV of $120b.

This follows Q1 momentum where GMV came in in-line with Q4 2024 numbers which are typically stronger due to seasonality reasons.

Gross Orders for the business was equally impressive, growing to 3.3 billion orders.

This set up yet another record-breaking quarter, with management highlighting a sustained increase in active buyers and purchase frequency, extremely important key metrics for a business like Shopee.

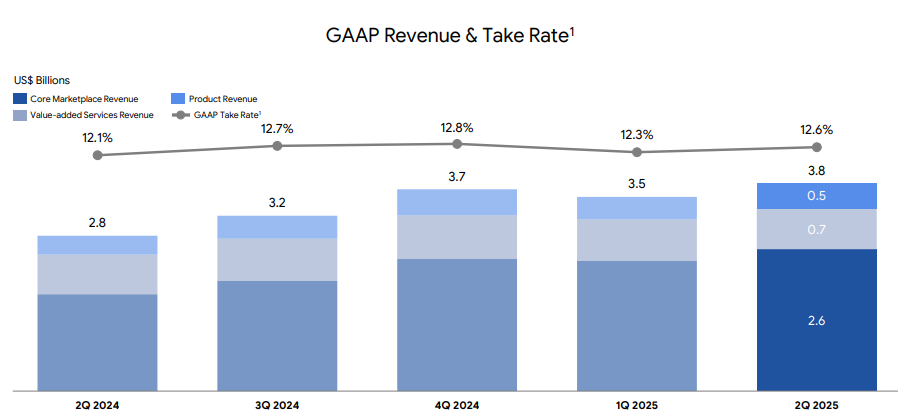

Revenues were $3.8b in Q2, with a higher take-rate of 12.6%. This sustained take-rate will lead to the continuation of the profitable growth story. In Brazil, average monthly active buyers grew over +30% YOY. This implies that Mercado Libre (MELI) success and free shipping changes did not harm Shopee’s market share in Brazil. The main losers should be from smaller competitors while MELI and Shopee continue to take share.

For Brazil, we have seen some actions from competitors in recent months. However, our business has continued to grow well, even after those adjustments, with no observable impact so far. Our focus has been on maintaining the best cost structure, particularly in logistics. Delivery speed has improved, we are now two days faster than last year, while costs have continued to decline. We believe our cost structure is significantly lower than our competitors’, even compared to their slower shipping options.

In terms of pricing, publicly available benchmarks still show we remain highly competitive across all categories. On the brand seller side, we’ve been expanding into higher-ticket items over the past few quarters, and we expect that trend to continue, unaffected by competitor movements. Overall, we are confident in our position in Brazil and expect our growth trajectory to persist, supported by our strong fundamentals in cost, pricing, and seller expansion.

Q2 2025 earnings call

There were some new initiatives:

Instant Delivery: Receive orders within 4 hours of placement. First piloted in Indonesia and has rolled out to Vietnam and Thailand.

Intelligent Demand Forecasting: Commonly ordered products are pre-shipped to warehouses closer to where they expect demand to come from.

VIP Program: Shopee’s VIP membership program has also shown extremely strong momentum in Indonesia. Total GMV from VIP members grew nearly +50% quarterly and VIP members bought a monthly average of 30% more after subscribing. VIP members have also shown a 20% higher retention rate compared to non-members. Shopee expanded the programme to Thailand and Vietnam. As of the end of June, total VIP subscribers in these markets reached 2 million, with planned roll outs to more markets in 2H 2025.

SE logistics focus has been the key differentiator for the business, with it being the second largest logistics player in Southeast Asia, only behind J&T Express.

In Brazil, logistics cost-per-order fell by -16% while Shopee reduced average delivery time by more than 2 days YOY. In the greater São Paulo region, about 25% of Shopee parcels were delivered the next day, and 40% within two days (up from single-digit percentages in the same period last year).

The impact of tariffs is almost a non-issue because it is predominantly a local/regional business model.

Monee

The most important advantage Monee has is the seamless integration with Shopee, benefiting from the large user base.

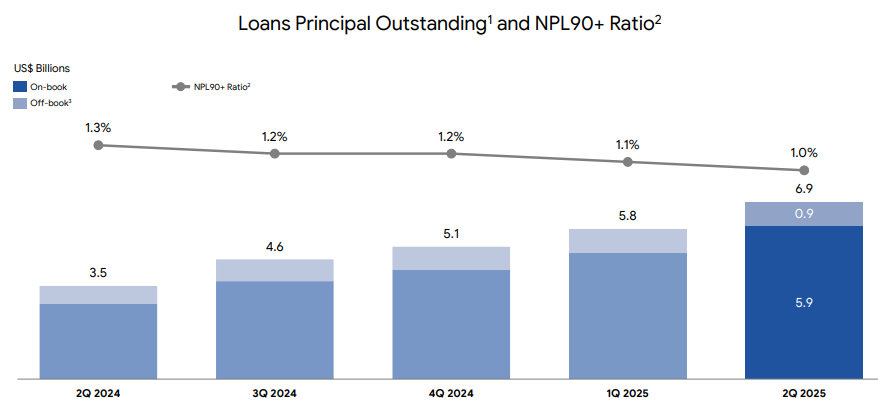

Monee continues to grow the loan book, almost doubling on YOY basis. They added 4 million new borrowers in Q2 and now have over 30 million consumer and SME loans. Despite the rapid growth, NPL90+ ratio (non performing loan past 90 days) at 1% continued to improve across time.

Malaysia was the third market after Indonesia and Thailand to have its loan book surpass $1b.

The SPayLater business continues to grow strongly, both on and off Shopee.

On-platform, credit adoption reached mid-teens GMV penetration, driven by new features like interest-free installments, tiered pricing for prime users, and credit limit increases.

Off-platform, SPayLater expanded via QR network integrations in Malaysia and Thailand.

Management reiterated guidance of loan book size growing meaningfully faster than Shopee’s GMV annual growth in 2025.

We see Brazil as a very important market for us on the finance side. We have seen very good growth on the loan books in the second quarter. Our active user for loans grew 2x year-to-year. Our outstanding loans in Brazil also grew more than 2x year-to-year.

One of the key things we did, I think we shared in the last earnings call is we combined the personal cash loan and SPayLater limit to one limit, which is different from how we operate in Asia. We also integrate more external data to our risk assessment system compared to Asia. And this is because in Brazil, there is more external data available compared to the SEA market.

We also have better integration between our Monee product offering and the Shopee product offerings. All this enables us to grow our loan book quite meaningfully and reduce our risk in the market. We have formed partnerships with some external lenders already to support the lending funds in Brazil market. So in general, we are very optimistic about the potential upside on the digital finance services in Brazil.

And I think we are still in a very early stage compared to Asia in terms of the growth trajectories. The penetration of SPayLater Shopee site is still around the single-digit to double-digit range. If you compare to Asia, we still have very large room to grow. Our personal loans are still very early stage.

We have many other products in the pipeline to be rolled out to the market.

Q2 2025 earnings call

Garena

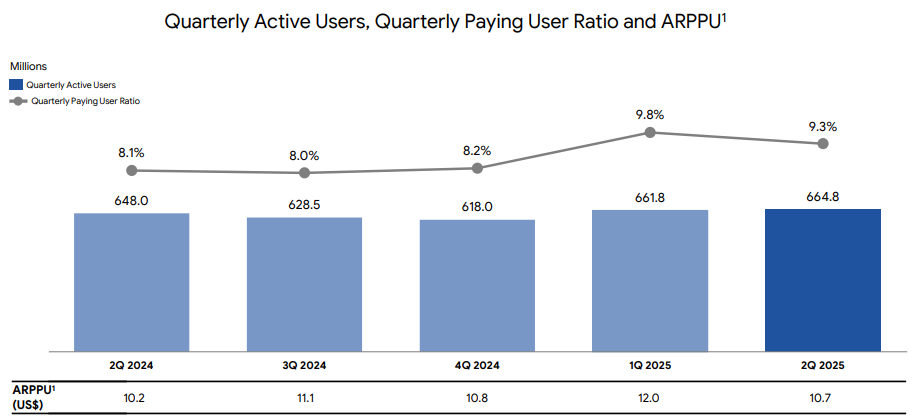

Quarterly active users (QAU) reported another multi-year high and quarterly paying user (QPU) ratio is at 9.3%. Against Q1, a lower QPU is expected due to seasonality (CNY, Ramadan).

The Free Fire game continues to have over 100 million average daily active users. This game is over 8 years old! It also launched it new map (Solara) in celebration of its 8th anniversary, it took 3 years without a new map and ~2 years of development work and has been incredibly popular among gamers.

The team also capitalised on excitement around the new map by introducing a new camera mode that lets players capture photos and videos of their gameplay more easily, which has led to average daily shares of in-game footage growing by nearly 4x. Free Fire also continued its highly successful IP collaborations with Netflix’s Squid Game and NARUTO SHIPPUDEN Chapter 2 into July which has been met with an extremely positive response.

There are other titles which delivered double-digit growth in Q2: Arena of Valor, EA Sports FC Online and Call of Duty: Mobile.

Management also raised FY2025 guidance for Garena, expecting bookings to grow YOY more than +30%.

Some comments on how AI can improve gaming productivity:

Personally, I believe game industry will be among the first batch of industries largely benefited by the AI advancements and the technologies. And so far, we have seen a lot of kind of upside on the development and the production side. And, for example, to develop any new content new map, we need to generate a lot of original arts.

And now a lot of very, very basic arts can be generated by AI. The quality is very decent in terms of the efficiency, the volumes being generated and the varieties being generated is much, much better than what humans can do. So this has largely improved our productivity, and it’s really exciting.

Q2 2025 earnings call

Revenue Expectations

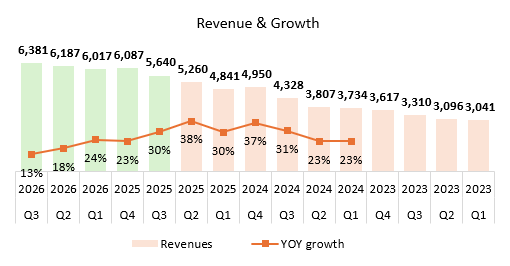

The green bars are the market expectations of revenue growth. Looks like after a few quarters of above 30% growth, analysts think that growth should slow down in 2026.

Operating Income

The last time SE was making operating losses was in Q3 2022 at -$212m. Then the strategic reset came to pivot from growth to profitability. Since then SE has been reporting positive operating income, with Q2 2025 being the record high of $673m.

All 3 segments (Shopee, Monee, Garena) reported positive operating income for 3 consecutive quarters already.

It is reasonable to expect this to continue as their operating leverage seem to become stronger over time.

Cash Position

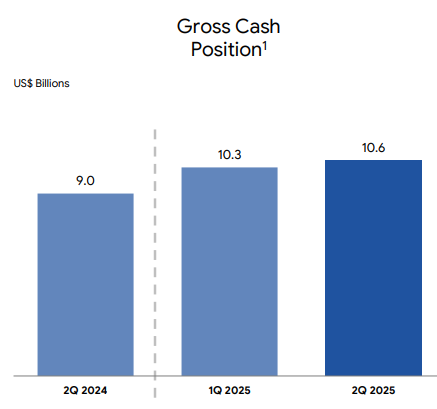

SE generated $2.4b in operating cashflows in H1 2025, compared to $1.1b in H1 2024. Cash on the balance sheet is $10.6b, that’s 10% of the $103b market cap.

Forward Looking Statements

SE just delivered one of its strongest quarters in its history. The mix got better with Financial Services being a larger piece of the pie, and credit scaling without significant credit losses yet (NPL90+ ratio less than 1.5%).

Shopee monetisation is inflecting as expected with ads and fees trending upwards while logistics helps bring costs down. With GMV tracking to ~$120b for FY2025, every +0.1% take-rate is roughly ~$120m of high-margin revenue.

Overall, all 3 segments are performing incredibly well. We think SE is set up for a very strong year.

Now, the market isn’t blind to this and the shares are quite expensive:

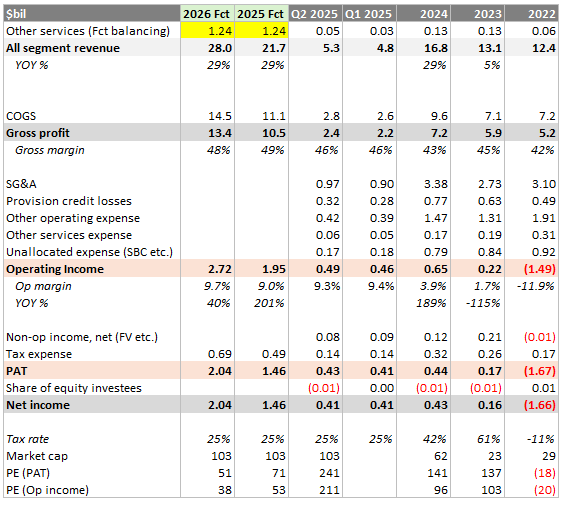

We find it difficult to be optimistic about 2026 operating margins, both Monee and Garena margins look stable at 25% and 43% respectively. We doubled Shopee’s margins to 2.8%.

If we believe these projections then the 1-year forward PE is still expensive.