SE: Sea Ltd (1)

History

Sea Limited (SE) is a business that spans e-commerce (Shopee), digital financial services (Monee), and gaming (Garena). Founded in 2009 and based in Singapore, SE has grown from a pure game publisher into Southeast Asia’s dominant online marketplace.

2009 – 2014: Garena

In 2009, Forrest Li, a Stanford MBA graduate born in Tianjin, China, founded Garena.

Initially short for “Global Arena”, Garena started out as a game distribution and social platform, bringing hit titles like League of Legends to Southeast Asian gamers. It became the go-to hub for online gaming in the region, known for its local servers and community-first approach.

During these early years, Garena proved adept at operating Western games under localised strategies, forming partnerships with developers like Riot Games and Electronic Arts. This allowed Garena to scale fast without building proprietary games.

It got its breakthrough in 2010 when it secured the rights to publish Riot Games’ League of Legends in the region. League of Legends is one of the biggest multiplayer online battle arena (MOBA) titles to this day, and this deal got the attention of Tencent, who was an investor in Riot Games.

Soon after, Tencent bought a 40% stake in Garena and began a long-standing strategic distribution relationship with the company. In 2018, Garena entered into a 5 year exclusivity agreement with Tencent which gave them the right of first refusal to distribute any Tencent game in the region.

By 2014, Garena’s valuation reached ~$1b, making it one of Singapore’s first tech unicorns.

2015 – 2016: Shopee & AirPay

Seeing the rise of mobile-first consumers in Southeast Asia and taking cues from Alibaba’s success, SE launched Shopee in 2015 as a mobile-first C2C platform. Growth was rapid, driven by chat-based UX, social features, integrated payments and logistics.

SE scaled quickly with logistics partnerships, seller tools, and heavy marketing. Within 3 years, Shopee became the top e-commerce platform in several Southeast Asian markets. Around the same time, Garena began testing a payment service called AirPay, laying the groundwork for their future fintech arm.

In May 2017, Garena undertook a major corporate rebranding after closing a fresh $550m funding round. The parent company then adopted the name “Sea Limited”.

The Garena brand was retained solely for the gaming arm. This rebranding signaled to investors that SE was more than a game publisher; it was beginning to position itself as a consumer internet conglomerate akin to China’s Tencent or Alibaba.

2017: IPO

SE went public on the NYSE in October 2017, raising $884m in its IPO, pricing at $15/share and valuing the business at around $5.4b. This was one of the largest tech listings from Southeast Asia, the capital allowed SE to further expand Shopee and Garena game developments.

It was around this period that Garena launched its first major proprietary game: Free Fire. Initially seen as a low-budget PUBG clone, Free Fire became a surprise global hit, especially in Latin America, Southeast Asia, and India. Its lightweight size, fast-paced gameplay, and localised content proved effective in emerging markets with lower-end phones.

2018 – 2019: Regional Expansion

With Shopee scaling and Garena printing cash, SE launched SeaMoney to build out financial infrastructure. Originally designed to support Shopee transactions (AirPay), SeaMoney expanded to digital wallets, payment gateways, and micro-loans.

By end of 2019, SE was operating a full stack. The strategy was working. Revenue grew from $400m in 2017 to $4.3b by 2020.

2020 – 2021: COVID boom

During COVID, lockdowns in Southeast Asia spurred even more online activity.

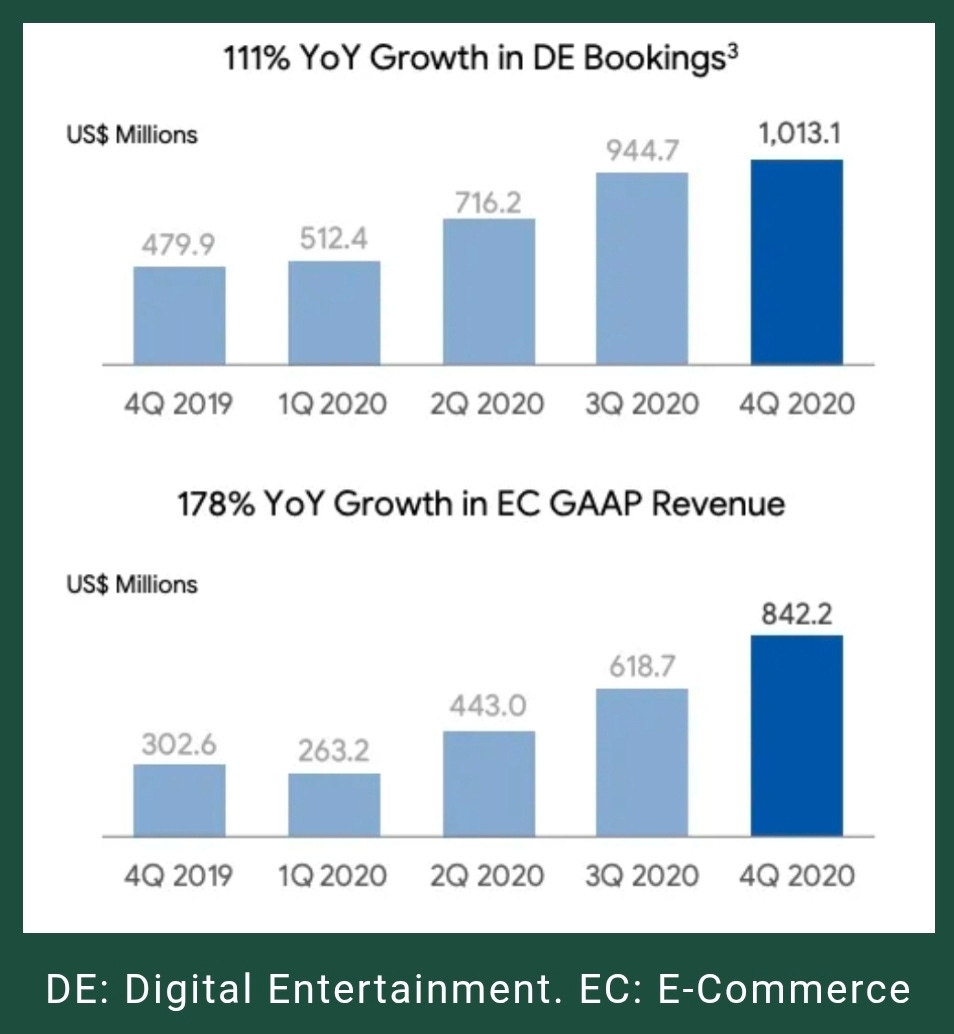

Garena’s Free Fire game surpassed 100 million daily users, with bookings (GAAP revenues + change in deferred revenue, approximation for user cash spent) over $1b that year.

SE share price went from $40 at the start of 2020 to $350 near the end of 2021!

SE ramped up SeaMoney, integrating payments into Shopee and launched digital lending. In December 2020, it secured a Digital Full Bank license in Singapore and acquired Bank BKE in Indonesia, rebranding it as SeaBank.

By late 2021, SE also obtained a Malaysian digital bank license and was building SeaBank Philippines. The FinTech space was growing fast, and as a result SeaMoney’s revenue rose 155% YOY in 2021.

In the same year, SE raised $6b in an equity and convertible bond sale to fund further expansion into LATAM and Europe, starting from Poland. This increased its cash reserves to $13b.

Their stock price would peak at $372, with a market cap over $200b.

Flush with capital, SE began aggressively expanding Shopee beyond its ASEAN base. Shopee entered Europe for the first time by launching in Poland, followed shortly in Spain and France. In November, Shopee entered India with a pilot initiative, leveraging Garena’s Free Fire user base to build initial brand awareness.

On the other side of the world, Shopee expanded further into LATAM, launching cross-border operations in Mexico, Chile, and Colombia.

However, the growth did not bring along profitability, even though revenues grew +127% in 2021, net losses were -$945m.

2022: Strategic Reset

In early 2022, Tencent cut its stake in SE by $3b, reducing ownership from 21% to 18.7% amid China’s tech crackdown. The move was seen as de-risking, SE already expensive stock price fell -11% in a day.

Another blow followed in Feb 2022, when India banned Free Fire over security concerns tied to Chinese-linked apps. Despite SE being Singapore-based, its ties to Tencent led to inclusion. Free Fire lost one of its biggest markets overnight, the stock fell -18% in a day.

In March 2022, Shopee withdrew from India and exited France and Spain in Q2. At the same time, their financial momentum reversed. Shopee’s YOY revenue growth slowed to 21% in Q2 2022, while Garena’s revenue fell -40% after India’s ban. With growth stalling and costs still high, the aggressive expansion model became unsustainable.

In June 2022, CEO Forrest Li announced a pivot from growth to profitability, triggering major cost cuts. SE froze hiring, slashed marketing, and laid off ~7,000 employees (~10% of its workforce) across Shopee, Garena, and SeaMoney.

In September, the leadership team would waive salaries and bonuses until SE reached self-sustaining cash flow, calling for cost discipline. This marked a clear strategic shift, signaling to investors that management was serious about curbing losses.

The austerity measures began to show results by Q3 2022. Operating losses narrowed significantly. In November 2022, SE reported that Shopee’s Southeast Asia/Taiwan e-commerce business turned adjusted EBITDA positive for the first time in its history. Although on a net basis SE still lost money in Q3, the company’s commentary projected confidence that the worst was over. Forrest Li announced that self-sufficiency was within reach, emphasising disciplined growth going forward.

SE stock price jumped 36% in a single day after the Q3 results, its biggest ever daily gain, as the market embraced the profitability pivot.

SE made the tough call to exit or suspend several non-core initiatives:

(1) Discontinued its investment arm (Sea Capital) in 2022, halting new equity investments in startups to conserve cash.

(2) Shopee closed its operations in Chile, Colombia, and Mexico in September 2022, reverting to a cross-border model serving those markets from abroad. It also fully exited Argentina.

(3) Exited France, Spain and Poland.

With these strategic resets, SE returned to its core markets in ASEAN and Brazil.

2023 – 2024: Profits!

Finally, SE posted its first GAAP profit in Q4 2022 and then reported after-tax profits of $162.7m in 2023.

By Q4 2023, Shopee’s orders surged 46% YOY, and SE stayed profitable.

By Q3 2024, Shopee was profitable in Asia and Brazil. Shares rebounded to over $100, as investors regained confidence in their balanced growth strategy.

Garena stabilised in 2023. Free Fire remained resilient, hitting over 100m daily active users again by Feb 2024, boosted by new content like the NARUTO collaboration.

With League of Legends rights lost in 2023, SE focused on developing their own games to reduce reliance on Free Fire. Garena was no longer a growth engine but remained a profitable, cash-generating core.

In Brazil, Shopee’s local marketplace flourished with over 3 million local sellers and more than 90% of sales coming from domestic merchants. This local traction helped Shopee Brazil improve unit economics. Investors started to assign value to SE international operations again, seeing Brazil as a potential second pillar for long-term growth.

In Q3 2024, SE announced that Shopee had achieved profitability at the segment level across Asia and Brazil. It recorded an adjusted EBITDA of $34.4m in Q3 2024, a stark turnaround from a loss of -$346m a year prior. This showed that growth was indeed profitable (Q3 2024 e-commerce revenue growth +42.6% YOY). The stock jumped over 17% on this news, reaching its highest level in over two years.

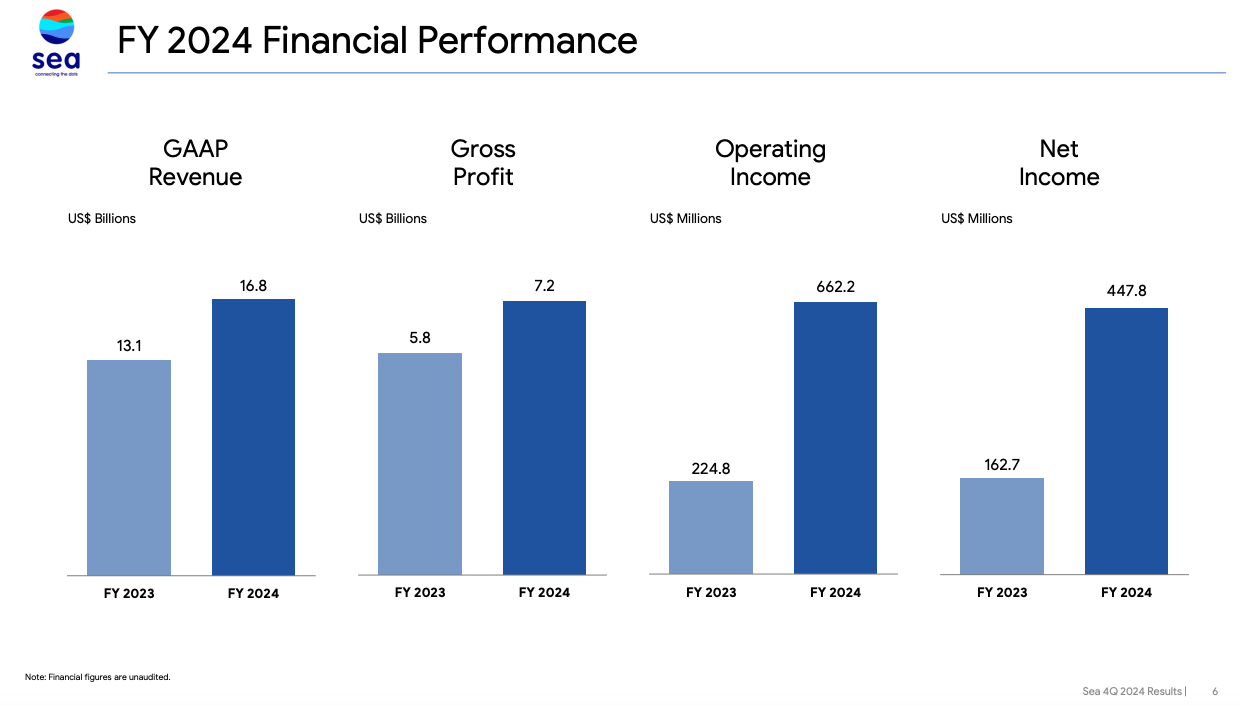

Ending 2024, total company revenues grew by +29% to $16.8b and it remained profitable, showing 2 consecutive years of profits.

2025: More Profitable Growth

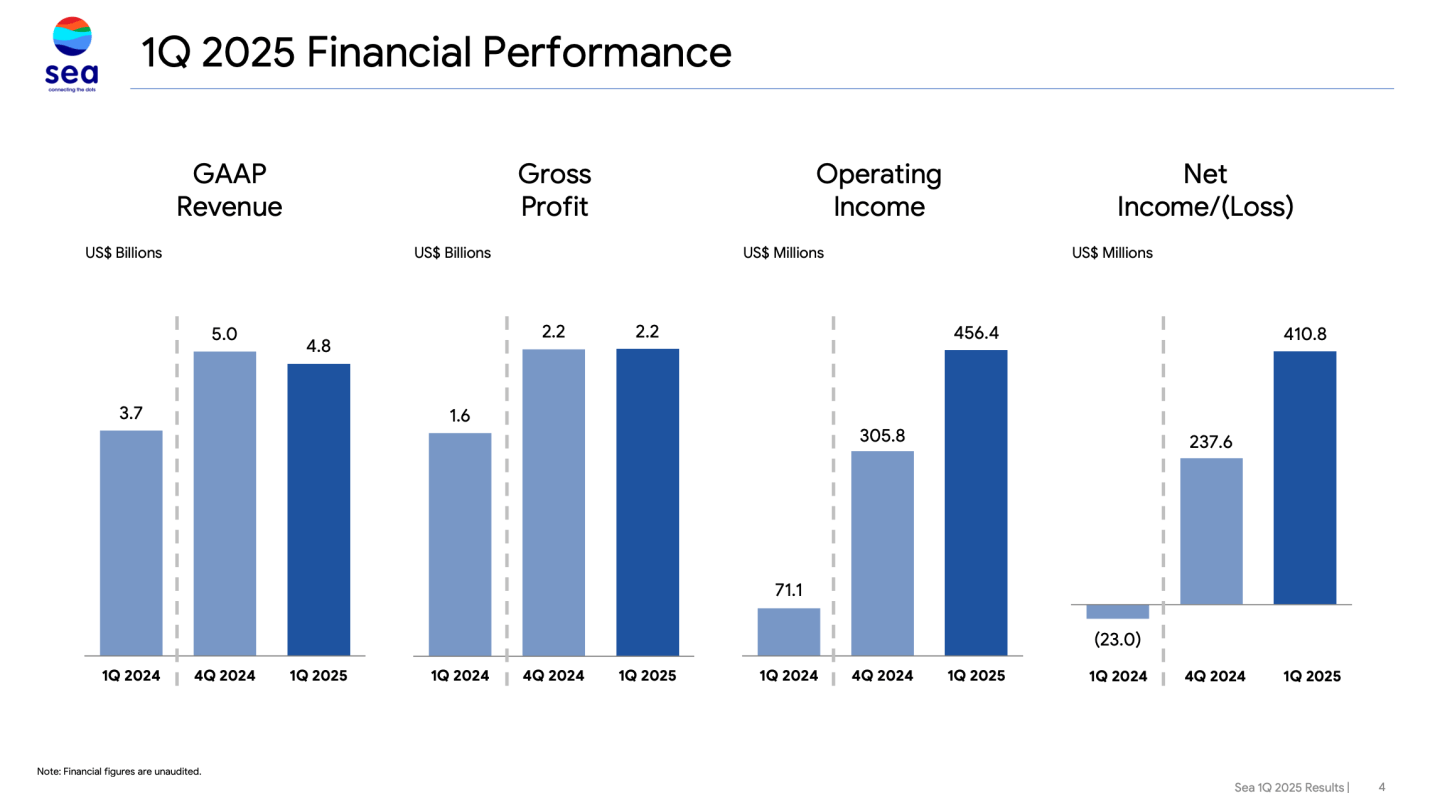

On May 8, 2025, SE celebrated their 16th birthday and they rebranded SeaMoney to Monee. In Q1 2025, Monee’s revenue rose +57% YOY, with $241m EBITDA.

Q1 results showed growth across all segments and reported $411m of profits. Shopee’s GMV hit $28.6b, up +21% YOY.

Garena reported impressive results with bookings +51% YOY and adjusted EBTIDA +57%. With average daily active users nearing the all-time highs and new games like Delta Force Mobile gaining traction, SE anticipates continued double-digit growth for the rest of the year.

Business Segments

SE splits their business into 3 parts: e-commerce, digital entertainment and financial services.

E-Commerce: Shopee

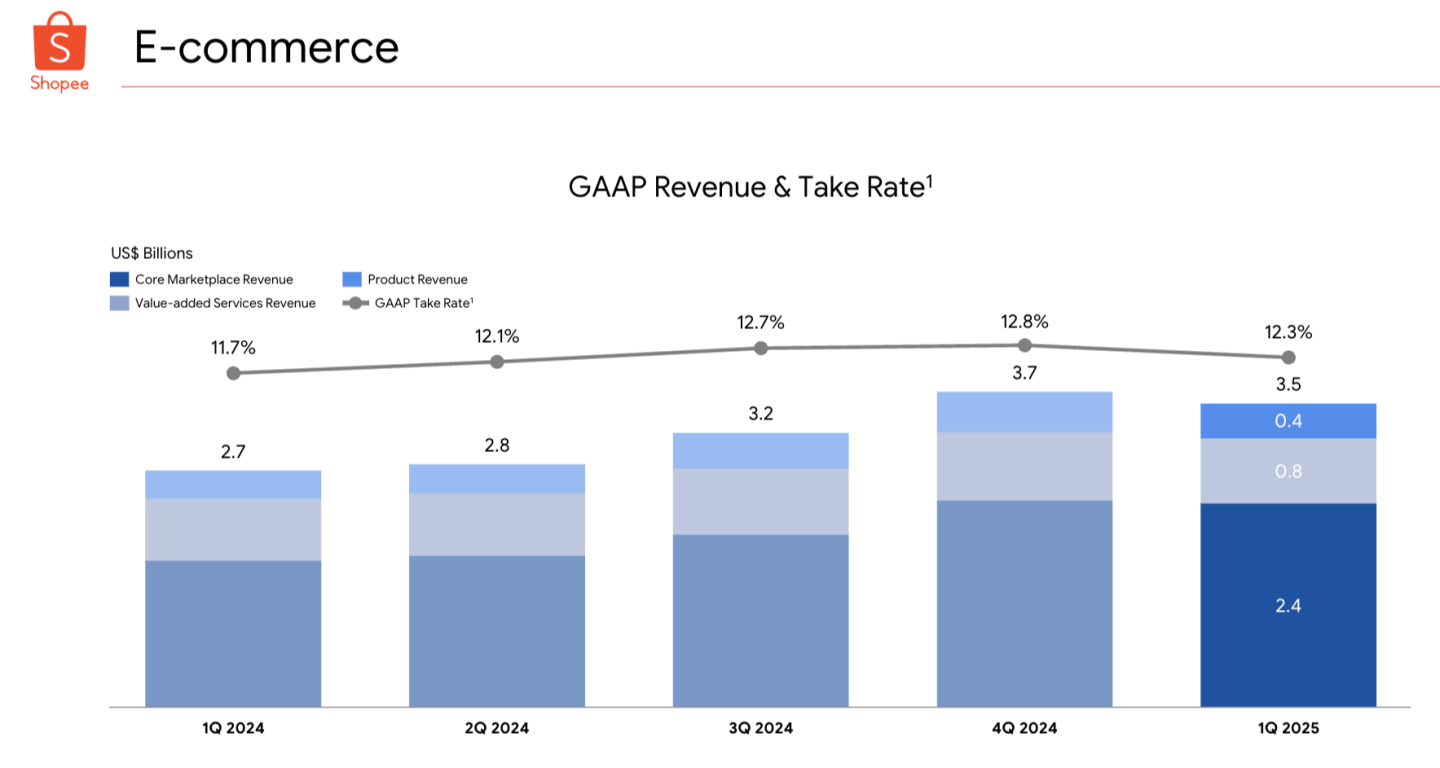

Shopee is the largest revenue contributor at 65% and has turned profitable. It is Southeast Asia’s largest e-commerce platform, accounting for over 50% market share.

A key part of its success has been the investment by management into its logistics business: SPX Express, which is now the 2nd largest logistics player in Southeast Asia. It handled 3.1 billion orders in Q1 2025.

Southeast Asia and Taiwan remain Shopee’s stronghold, but its recent success in Brazil will play a key part in the growth story. In 2024, Shopee was the 3rd largest online marketplace in Brazil with an estimated $15b GMV (~15% market share).

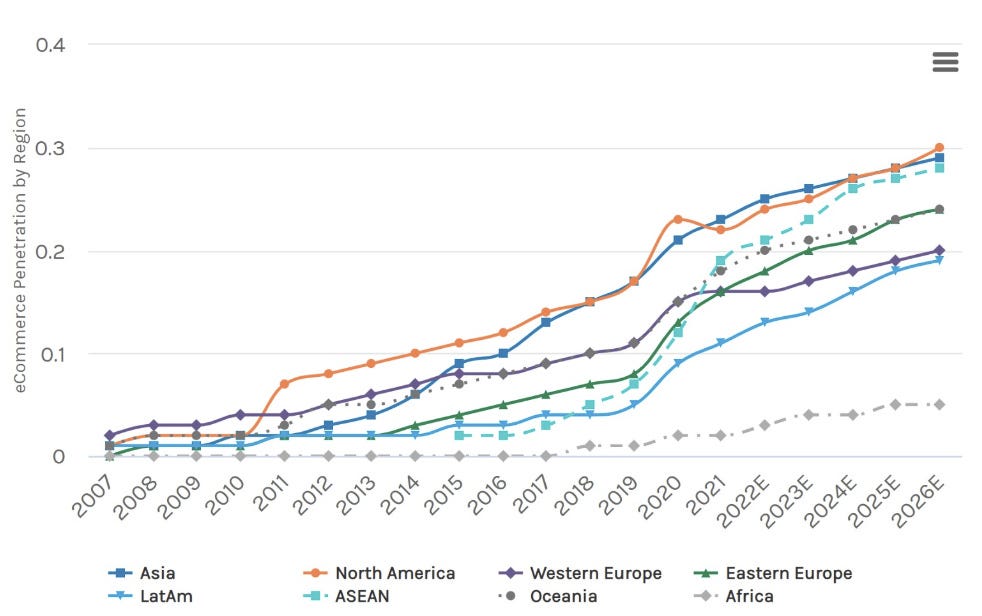

Below is the projection of e-commerce penetration by region:

There are some naunces about this projection. About half of the retail market is groceries and fresh food, a segment which according to the Bain/Temasek 2022 SEA report has low single-digit online penetration due to its expensive requirements for cold chain logistics.

Some estimates suggest that the non-grocery segment where Shopee predominantly plays has probably over 30% online penetration. This implies that the non-grocery segment that is relevant to Shopee may grow even slower than the overall e-commerce TAM given its much higher penetration.

Shopee turned its first-full year of adjusted EBITDA profit in 2024, and its take rates have continued to climb despite competition. That is certainly a positive sign:

Blueprint for Success

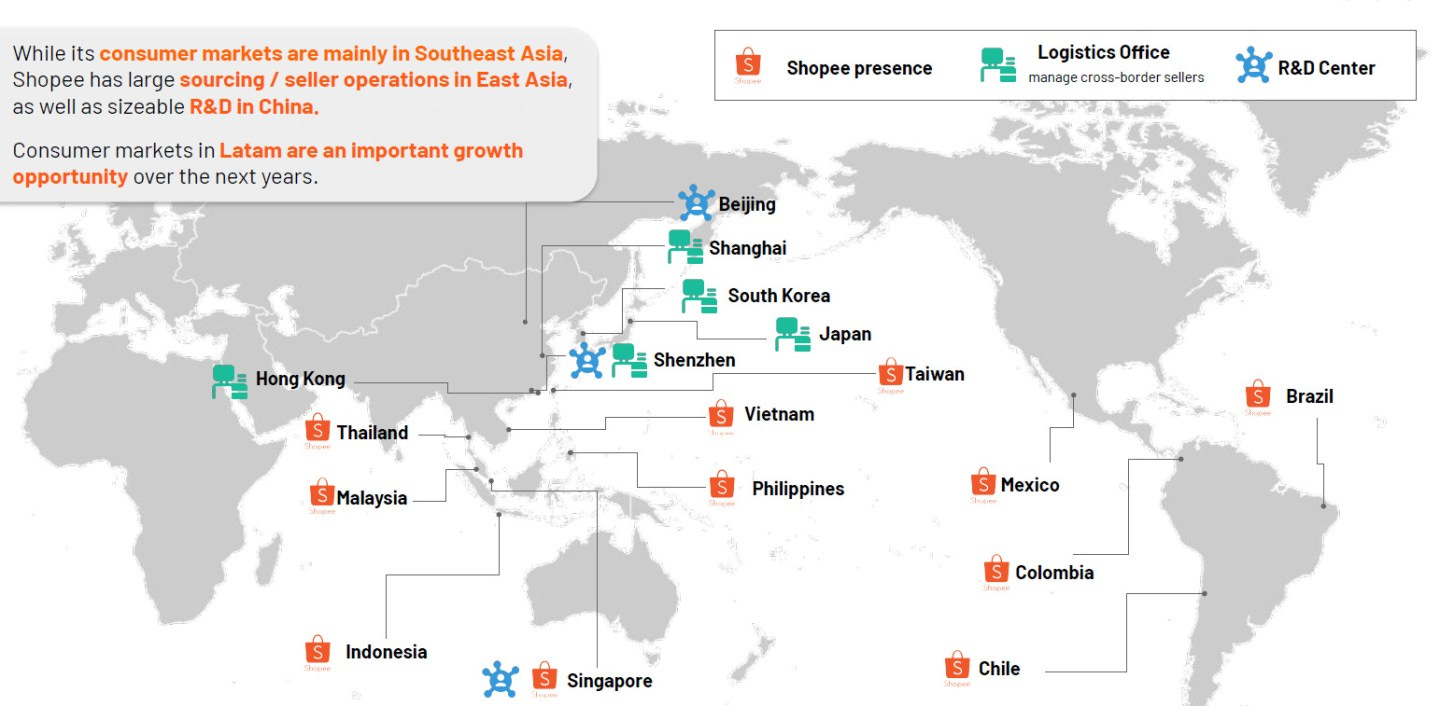

Shopee relies heavily on its logistics and R&D offices in China, Korea and Japan. The overseas logistics offices are important as they help drive the cross-border e-commerce trade, which is a critical part of Shopee’s product offering, particularly in the early stages of entering a new market.

The blueprint for their success can be summarized into a few key components, none of which are irreplicable:

Mobile first, hyper-localized approach.

Cross-border merchants to scale up the supply side and then add local merchants with low/no commissions.

Focus on fashion, apparel, health and beauty.

Leverage third-party (3P) logistics and subsidize shipping fees.

Aggressive marketing using celebrities.

Increase user engagement through gamification.

Logistics

Logistics has always been a problem for Southeast Asia due to the relatively complex landscape structure. Shopee’s strategy has been to rely on local 3P logistic partners. Its two main partners are the two biggest Indonesian delivery companies, J&T and JNE.

These logistic companies grew as Shopee volumes scaled up. Economies of scale, in terms of greater network density and optimised routes resulted in lower logistics costs. This further benefits Shopee and its customers.

Shopee has also started building out its own express delivery services (Shopee Express, SPX). At this point, this is largely restricted to trucking fleets in metro/tier 1 cities within its ASEAN markets, and is largely complementary support to the 3P services.

Taiwan Shopee has been implementing a network of physical stores. In 2021, there are ~150 stores, and they not only act as delivery pickup points, but you can actually also buy things like snacks and basic food items.

Digital Entertainment: Garena

Garena contributes 11% of revenues with its crown jewel mobile game, Free Fire, as the value driver. It has proven to be an evergreen franchise going into its 8th year.

The “battle royale” genre is popular now with games like PUGB and Free Fire. Prior to that, MOBAs were popular like League of Legends and DOTA 2; and before that, MMORPGs dominated with World of Warcraft and Guild Wars. As usually happens during these popularity cycles, a number of games emerge trying to grab their share of the market, however most don’t survive.

Being one of the first to market and with a focus on mobile has been beneficial to us. All of our designs and product features are made specifically for mobile users, so we didn’t have to translate anything.

Harold Teo, Garena Producer

The population is made up of mostly Brazilian and Middle Eastern people. Just 2.5 months after Garena soft-launched Free Fire in Southeast Asia (October 2017), it launched globally in 130 countries, with a particular focus on the emerging markets.

Free Fire, which was mobile-exclusive and designed to work on low-end phones, was essentially created with emerging markets in mind. It also poured significant resources into marketing and localising the content to better engage local gamers. With such a heavy focus on these regions from the start, it is no surprise that Free Fire quickly became the most popular game in those regions.

If you walk down the street today in São Paulo or Mexico City, you are just as likely to see someone playing a Garena game as you would in Bangkok or Ho Chi Minh City…

What we have seen from this global success is that many of the factors that drive a game’s success in our core market in Southeast Asia are the same as those in other parts of the world.

Forrest Li, Q2 2018 earnings call

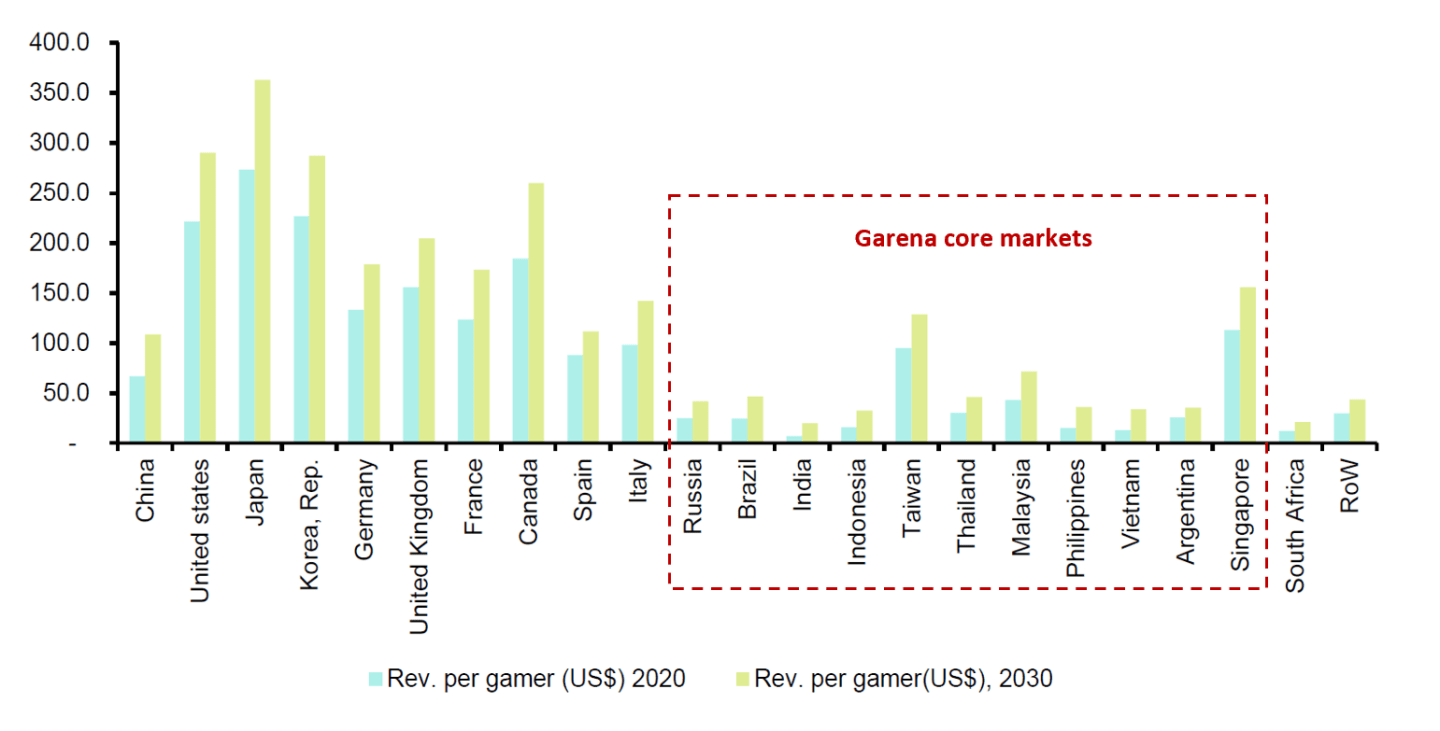

Future growth in Garena should outpace the rest of world, because of its core markets:

In the past, Free Fire was the cash generating business that funded the loss-making Shopee. Longevity was a real concern. Today, that risk is lower since all other segments have been profitable.

Financial Services: Monee

This segment was previously called SeaMoney, it was renamed in 2025 to Monee. It contributed 14% of revenues in 2024.

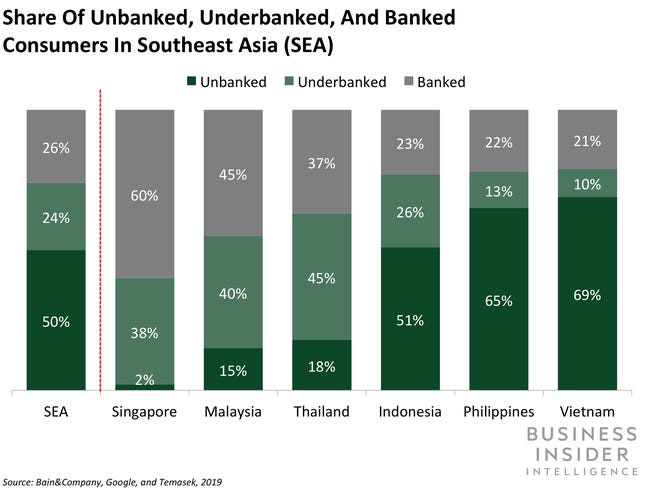

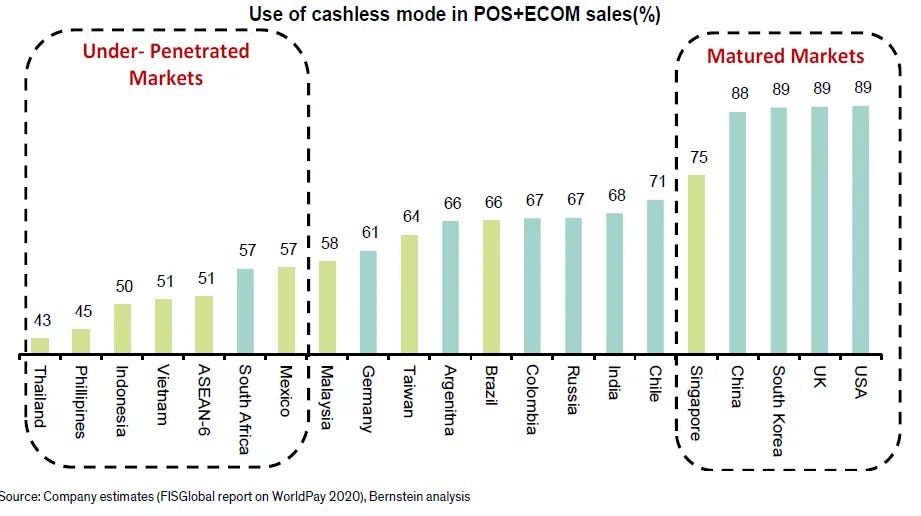

Estimates in 2019 showed that 74% of the SEA adult population is either unbanked (no access to basic bank accounts) or underbanked (not well served by financial services such as credit cards, insurance, loans):

Key reasons for this are usually insufficient banking infrastructure particularly in rural regions and hard to reach places (Indonesia islands), lack of trust of financial institutions, and in some countries low financial literacy.

These are also the same markets that are still heavily reliant on cash transactions:

There are reasons why internet companies like SE are attracted to financial services, the main one is a large customer base and data about customer habits. More people have smartphones than bank accounts in emerging markets, so these internet companies are in an unique position to provide financial services to people more effectively than traditional banks.

Benefits of running their own payment network are obvious; reduce payment friction, increase user lifetime value, reduce operating cost.

Monee houses the e-wallet ecosystems ShopeePay and AirPay along with digital banking.

It started in 2014 when AirPay was launched as a tool that allowed users to exchange cash for digital currency on their smartphones and used in games on Garena. Before this, Garena users would top up digital currency through cash payments at counters at thousands of local convenience stores. This was a driver for e-wallet adoption.

The AirPay app was eventually migrated to ShopeePay in all markets except Vietnam and Thailand where the AirPay brand is strong and well recognised. ShopeePay is the e-wallet that is linked to Shopee and represents the core of the Monee segment today. Being able to leverage on e-commerce was a very efficient way to build adoption on both the consumer and merchant side.

Like most digital payment networks, initially it was a closed-loop ecosystem. As adoption increased, they would open it to third-parties and offline merchants.

We are quickly expanding off-platform digital payment use cases. For example, besides increasing our payment touchpoints at convenience stores, F&B chains and on the Google Play store, our mobile wallet service recently expanded its partnership with Mastercard in Thailand. This will allow our users to pay at any of the 200,000 plus offline outlets that accept Mastercard Contactless. We are also partnering with Puregold, one of the largest supermarket chains in the Philippines, to accept our mobile wallet payment at over 400 of its stores.

Forrest Li, Q2 2021 earnings call

Examples of offline merchants (this is just a small sample):

Indonesia: Indomart, Wendy’s, Domino’s Pizza

Malaysia: Lotus, KK, Familymart

Singapore: ShopeePay is behind GrabPay but has launched promos in F&B chains like Boost Juice and BreadTalk.

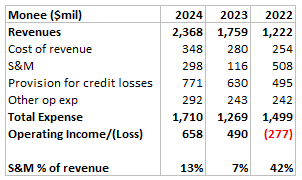

A key driver of the e-wallet usage has been aggressive promotions and cashbacks. SE incentivizes usage by offering Shopee Coins cashbacks, which can be used to make purchases on the Shopee platform. This is an expensive strategy that comes out of the sales and marketing expenses. This is similar to the spend-to-scale strategy of Shopee, after gaining traction, S&M expenses have been decreasing since 2022:

In some markets like Malaysia and Thailand, Shopee has released co-branded credit cards with bank partners, which allows users to collect Shopee Coins with every purchase.

BNPL, Consumer & Merchant Loans

BNPL services are available in Indonesia, Malaysia, Thailand and Philippines via SPay Later. They monetize by charging monthly interest, effectively turning it into a short-term consumer loan.

Monee also lends to SME merchants to help with working capital needs. These services are in Indonesia and Thailand only.

The model which SE takes with lending seems to be both on-balance sheet and partnering with a variety of local lenders, such as KBank in Thailand. We don’t know exactly how much credit risk is taken by SE, but typically at the nascent stages of ramping up a digital banking business, the majority of the loans would probably need to sit with SE until their credit scoring and risk algorithm gets proven good enough to be trusted by banks.

In December 2020, SE was awarded a license to operate a digital bank in Singapore.

In January 2021, SE acquired a local Indonesian bank (Bank BKE) with the aim of transforming it into a digital bank. It is a small Jakarta-based private bank chain which can be used for securing a bank license.

In April 2022, Malaysia allowed SE to operate a digital bank too.

Competition

All players in the e-commerce space start out with a core business, and eventually expanded adjacently. They all try to be the super-app for the consumer.

In e-commerce, each country has several players competing intensely for market share. With each country being its own distinct market, the competition and network effects are highly localised.

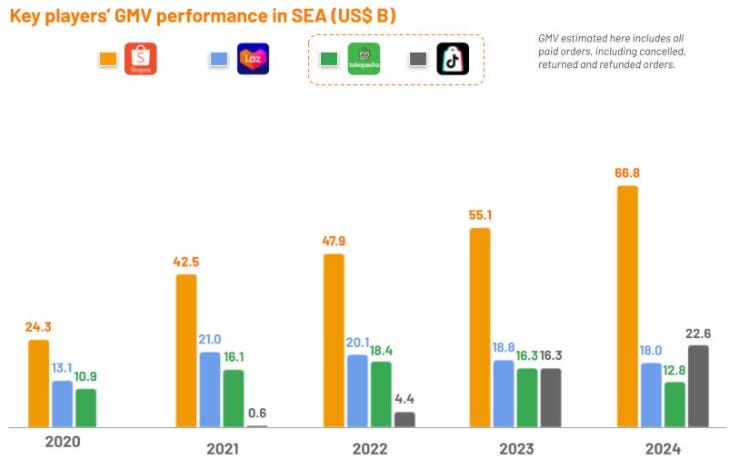

The largest markets: Indonesia and Brazil, have seen the emergence of strong local players; Tokopedia and Bukalapak in Indonesia, Magalu and B2W in Brazil. Excluding these local players, we have large regional players; Shopee and Lazada in Southeast Asia, MercadoLibre in LATAM.

In LATAM, there isn’t a strong contender, leaving an opportunity for Shopee.

The two biggest competitors to Shopee in Southeast Asia are Lazada and Tokopedia. Lazada was founded by Rocket Internet in 2012 and was acquired by Alibaba in 2016. It plays in all of the major Southeast Asia markets like Shopee (except Taiwan) and for a long time it had enjoyed an advantage as the first-mover and the largest player in each market, until Shopee surpassed it in 2017.

Tokopedia is the incumbent Indonesian e-commerce player who started operations in 2009. It is the second largest unicorn in Indonesia after GoJek.

The apps for all these players are largely similar. Using elements of gamification and live-streaming to promote purchases. In a way, this reaffirms Shopee’s success as it was the first to implement these features in Southeast Asia.

This also means that players have to continuously innovate just to keep slightly ahead of the competition who can easily copy most elements of app design.

Lazada

Lazada is an interesting case study of how being a first-mover does not necessarily lead to a sustainable leading position.

Lazada was established as predominantly a 1P inventory carrying retail model instead of a 3P marketplace. Its focus on standardised categories such as consumer electronics and building out of its own logistics made it extremely cost efficient in those categories, but at the expense of having a differentiated marketplace with lots of repeat purchases.

It helped promote e-commerce through its aggressive advertising campaigns, and there was the opportunity to leverage its position as a first-mover and expand into a broader marketplace.

However, what derailed Lazada was internal cultural issues together with integration mismanagement of Alibaba.

Under Alibaba, Lazada went through 3 CEO changes in 2 years and multiple changes of country heads. Alibaba installed middle management into Lazada, and due to their lack of understanding of unique local conditions, staff attrition spiked with a large number of people joining Shopee.

Alibaba also forced Lazada to switch to its technology back-end to the same as Taobao. However, the complexity of IT migration led to problems that disrupted operations.

All these allowed Shopee to overtake Lazada.

But big competitors in this place don’t die easily, especially with financial backing from Alibaba. There are examples of Lazada leveraging its Alibaba relationship successfully. For instance, you can now buy things from Taobao on Lazada. This allows Lazada users to access Taobao merchants directly, which has a huge number of products.

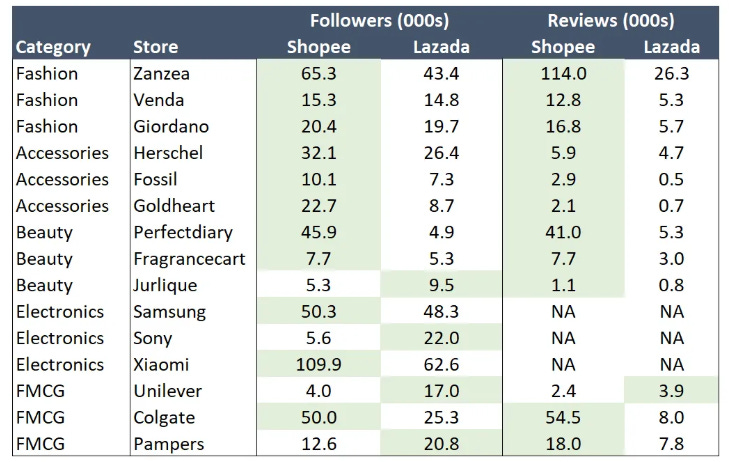

Ultimately, we think that user engagement is the differentiating factor between these players. By looking at the number of followers/reviews across some popular categories, we can see that Shopee is much stronger:

Tokopedia-GoJek (GoTo)

Tokopedia started as a marketplace, then expanded to other digital services including grocery delivery (TokoMart), food delivery, online pharmacy, travel and ticket bookings, and a whole suite of financial services such as payments, lending, investments, tax, and insurance.

For its e-wallet, it has a strategic investment in OVO, a leading Indonesian mobile wallet, of which it owns 41% with Grab being the other major shareholder.

Other services are offered through collaborations, for example, the travel service is a partnership with Traveloka.

In comparison, Shopee only launched its food delivery business in Indonesia (ShopeeFood) and a grocery business (Shopee Segar) in 2021. Thus, Tokopedia has significantly greater offerings.

In 2020, GoTo bought 22% of Bank Jago to offer digital finance services through GoJek app.

Mercado Libre (MELI)

Both MELI and Shopee are 3P marketplaces focusing on the C2C/B2C model. However, they are not in head-on competition due to their different positioning.

Shopee is using a similar strategy in LATAM, where it initially focused on bringing low-priced categories such as fashion and apparel from predominantly Chinese and Korean sellers.

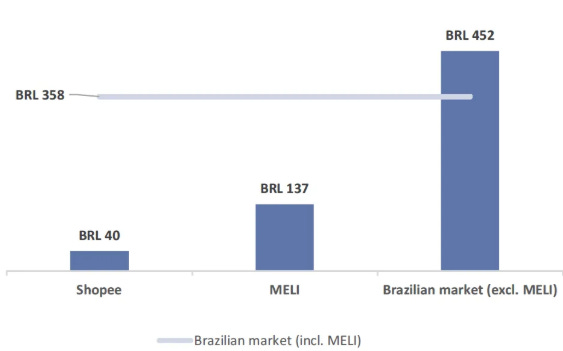

This contrasts with MELI, which began with a focus on consumer electronics. The MELI website is very heavy on smartphones, computers and peripherals, which are all fairly large ticket items that have low purchasing frequency.

The difference in category mix reflects in the price points:

So while Shopee might be winning in app downloads and user count, it is not reflective of the real market share differences between them.

The other key difference is that MELI has been investing heavily in logistics. MELI has an unbeatable delivery system built from scratch that doesn’t rely on state-owned postal services. Shopee will be relying on its usual 3P strategy of using local shipping companies. This means longer fulfillment time for Shopee.

Another advantage is MercadoPago dominates the digital payments space. The competitive landscape was not intense when MercadoPago opened up its payment solutions to off-platform merchants, and it was largely the only player offering a large e-commerce marketplace accompanied with e-wallet service. This gave MELI a significant first-mover advantage in scaling up its offline merchant base.

Digital Payments

In Indonesia, the largest ASEAN market, the key wallets are ShopeePay and GoPay, which are the two embedded wallets leveraging their Shopee and GoTo (Tokopedia-GoJek) ecosystems respectively.

There are also major independent wallet companies OVO and Dana. OVO is now predominantly owned by Grab who recently bought Tokopedia’s 40% stake in it, and Dana is owned by Alibaba’s Ant Group and Indonesian media conglomerate Emtek.

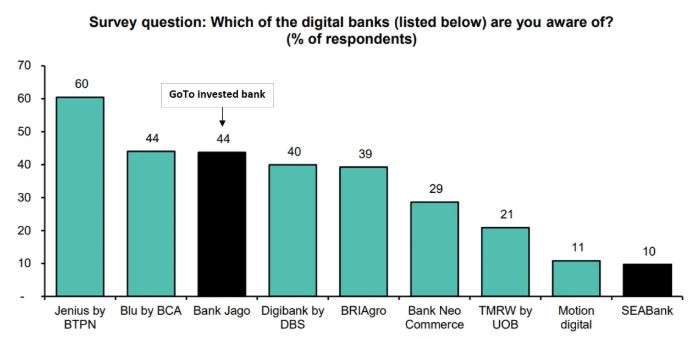

For digital banks, there are surveys suggesting how SEABank ranks among peers:

Other tech players competing in digital banking include:

(1) Alibaba-backed Indonesian fintech startup Akulaku, who became the largest shareholder in Bank YudhaBhakti, which later changed its name to Bank Neo Commerce.

(2) Japan’s LINE, through its affiliate LINE Financial Corporation, and PT Bank KEB Hana Indonesia have jointly launched LINE Bank in Indonesia.

(3) Bukalapak, an e-commerce company, partnered with Standard Chartered to launch BukaTabungan, a digital banking service aimed at providing financial inclusion to Bukalapak’s extensive user base and underbanked populations in Indonesia.

(4) Emtek Group acquired Bank Fama International (now known as Superbank) in 2021, and through a strategic partnership with Grab, the bank has been rebranded and integrated into the Grab ecosystem in Indonesia, offering various banking services directly within the Grab app.

In summary, there’s no shortage of tough competition in fintech space.

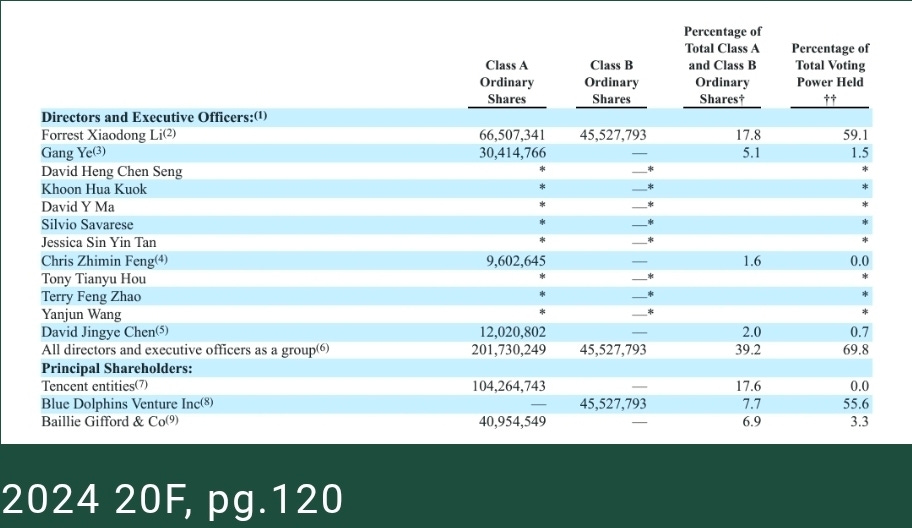

Management Ownership

Class B shares are 3 votes each, not publicly traded. Class A shares are publicly traded with 1 vote.

Tencent pledged all their voting power to Forrest Li.

Garena co-founder Gang Ye is the next largest insider with 5.1% ownership.

Chris Feng, CEO of Shopee and Monee, is the second most critical person to the business, but he only has 1.6% ownership.

He started off working in Garena. When they got the idea to start Shopee as an adjacent business in 2015, Forrest entrusted Chris to run with this new venture. Later in 2019, Chris was given the role of CEO of SeaMoney (Monee) as well.