Principles: ROE, Growth & Required Rate of Return

Intro

This post will explain the relationship between return on equity (ROE), required rate of return (RRR) and growth.

Once you understand how these variables interact, you can quickly do valuations in your head without needing a calculator.

The basics boils down to how ROE compares with your RRR; whether it is equal, above or below. Let’s assume for this whole exercise that your RRR is 10%.

ROE = RRR

Suppose that a business earns 10% ROE, which is the same as your RRR. Then the fair valuation must be 1x book value and 10x earnings.

Since book value is the capital invested in that business, a 10% ROE means that $100 of equity generates $10 of earnings. At 1x book value, you are paying $100 for that $10 of earnings which equates to 10x earnings. Now, 10x earnings is the same as 10% earnings yield which is exactly your RRR.

Therefore, when ROE = RRR (10%), the fair valuation is PB = 1x and PE = 10x such that you will earn your RRR.

What happens when you add growth into this scenario?

If reinvested earnings compound at 10%, then multiplying a growth rate just extends the same 10% return. Furthermore, whether the business distributes its earnings or reinvests them, your long-term return converges to 10%. So, other than for tax reasons, you should be indifferent to payout policies when ROE = RRR, because growth neither creates nor destroys value, it simply keeps earnings yield at the RRR.

ROE > RRR

Suppose a better business earns a 15% ROE against a 10% RRR, then with no growth it deserves to be valued at a premium to book. Because $100 of equity generates $15 earnings, for you to get 10% RRR the business should trade at PB = 1.5x.

At PB = 1.5x, you will pay $150 and earn $15 profits. That’s 10% earnings yield; exactly your RRR.

Notice that the PE ratio is still anchored at 10x, but the higher profitability shows up in the premium to book value. The higher ROE translates directly into a richer valuation of equity capital.

You may ask, in what scenario will the PE ratio change?

This is when growth comes into the picture. If ROE > RRR, a positive growth rate means that growth creates value. Compounding at 15% against the 10% RRR obviously creates for value for you and so the fair PE ratio should be higher than 10x.

ROE < RRR

Lastly, suppose a lousy business only produces 5% ROE against 10% RRR, then with no growth it deserves to be valued at a discount to book. Because $100 of equity generates $5 earnings, for you to get 10% RRR the business should trade at PB = 0.5x.

At PB = 0.5x, you will pay $50 and earn $5 profits. Again, back to the 10% earnings yield matching your RRR. The logic remains the same, lower ROE translates directly into discount to equity capital.

In this case, growth actually is value destructive because earnings are reinvested at 5% which is below the 10% RRR. In fact, the more this business grows, you should demand even more discount to book value and lower PE ratios.

The best solution is not to grow the business and return cash to shareholders!

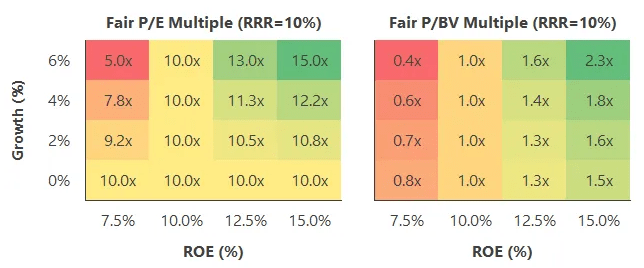

The Matrix

Below is the matrix between ROE, growth and fair multiples:

We hope this post gave you a quick mental shortcut to evaluate your favorite businesses.