Principles: Credit Cycles

The Credit Cycle

Superior investing doesn’t only come from buying high-quality assets, but from buying when the deal is good, the price is low, the potential return is substantial, and the risk is limited. These conditions are much more the case when the credit markets are in a less euphoric and more stringent part of their cycle.

Howard Marks

Changes in availability of credit/capital constitute one of the most fundamental influences on economies, companies and markets. The finance world calls “the credit window” as the “place you go to borrow money”. When the window is open, financing is plentiful and easy, and when it’s closed, financing is hard to get.

It is essential to bear in mind that the credit window can go from wide open to slammed shut in an instant.

Why Credit Cycles Matter

Credit is an important ingredient in the productive process. The ability of companies and economies to grow depends on the availability of incremental credit.

For example, companies and other economic agents such as governments and consumers generally don’t pay off their debts. Most of the time, debt is rolled over. But if a company is unable to issue new debt at the time the existing ones come due, it may default and lead to bankruptcy. Therefore, the state of the credit cycle is important: whether credit is easy or difficult to obtain is the greatest determinant of whether debt can be refinanced.

Many corporate assets are long-term in nature (properties, factories, goodwill…), however they acquire these assets by issuing short-term debt. They do this because the cost of borrowing is usually lowest at the short maturities.

“Borrowing short to invest long” works well most of time when credit windows are open and functioning, meaning that debt can be refinanced when due. But the mismatch between long-term assets (which cannot be easily liquidated) and short-term liabilities can easily turn into a crisis when maturing debt cannot be refinanced. This mismatch when combined with a dried up credit market is often the cause of spectacular meltdowns.

When the GFC of 2007 took place, credit markets froze up, and the Treasury took unprecedented steps to guarantee all commercial paper. They had to otherwise debts could not be rolled over and would have caused defaults even across the strongest companies. In fact, defaults will be concentrated among the biggest companies, since they issue debt in billions of dollars precisely for the reason that their creditworthiness gives them easy borrowing.

Financial institutions also represent a huge reliance on credit markets. Banks borrow short and lend long, deposits can be withdrawn at any moment while loans won’t be repaid in years. Bank failures occur when a bank run occurs and the bank has limited access to credit markets.

Moreover, credit markets give off signals that have great psychological impact. A closed credit market will spread out of proportion fears, even if businesses do not face such realities.

Why Credit Cycles Occur

Now that we know why credit cycles are important; what are the drivers behind their cycles?

The process is typical of economic cycles:

Economy moves into period of prosperity.

Providers of capital thrive, increasing their capital base.

Bad news is scarce leading to low risk aversion.

Financial institutions lend out more, competition reduces lending standards and lower yields.

There is a saying that goes: “The worst of loans are made during the best of times.”

An euphoric market leads to investment of capital in projects where the cost of capital exceeds the return on capital, and eventually to cases where there is no return of capital.

When this point is reached, the process continues to reinforce the economic contraction:

Losses causes lenders to be discouraged and stop lending.

Risk aversion and lending standards increase.

Less capital is made available.

Companies that borrowed cannot roll over their debts, leading to defaults.

At the bottom of this cycle, the process is ready to be reversed. Because after the weak companies are eliminated, high returns can be demanded with stricter lending covenants. Those who commit capital at this bottom will have increased chances of high returns. This draws in more capital and starts a recovery.

Market is an Auction House

In an auction house, the item being offered goes to the highest bidder. The financial markets are no different. The opportunity to make an investment goes to the participant who is willing to pay the most. This bidding takes price to higher valuation parameters.

In the credit market, high prices leads to low yields, and the provision of credit goes to the lender who is willing to accept the lowest yield and riskiest debt structure.

Just like how an overheated stock market produces high bidding “winners” who would eventually turn into losers; an overheated credit market results in lenders not getting paid enough for the risk they underwrite.

The degree of openness in this auction-like credit market depends entirely on whether lenders are eager or shy, and it has a profound impact on the entire economy, including prospective returns of investors.

Lessons

The excessive generosity in credit markets stem from shortage of prudence. This lack of risk aversion is one of clearest red flags. The wide-open credit window arises when news is good, asset prices are rising, optimism is high, and all things seem possible. But it invariably leads to issuance of unsound securities and debt levels that lead to failure.

An increased focus on making sure opportunities aren’t missed rather than avoiding losses makes investors willing to buy assets at lower quality.

The other end of the cycle puts the power in the hands of capital providers (we as investors). Because borrowing is difficult, those who possess capital and are willing to apply high standards of underwriting, will benefit from high prospective returns.

It’s things like these which provide margin of safety required for superior investment returns. When these conditions are met, investors should swing for the fat pitch.

Finally, we took a long route of explaining credit cycles to return to the quote at the start of the article: “Superior investing doesn’t only come from buying high-quality assets, but from buying when the deal is good, the price is low, the potential return is substantial, and the risk is limited”.

A small note about expectations of rate cuts

Market participants overwhelmingly are concerned by the short-term question of whether rates are going to be reduced in the next Fed meeting. But the real question that matters is: what the range of interest rates will be in the next 5 to 10 years?

Do you think it will be back to near 0%? Or is it more likely to be above the 2% inflation target? If it’s the latter, then equities will not see returns similar to the near zero interest rates period, leveraged strategies will be less advantaged, and returns from credit will be better than they were.

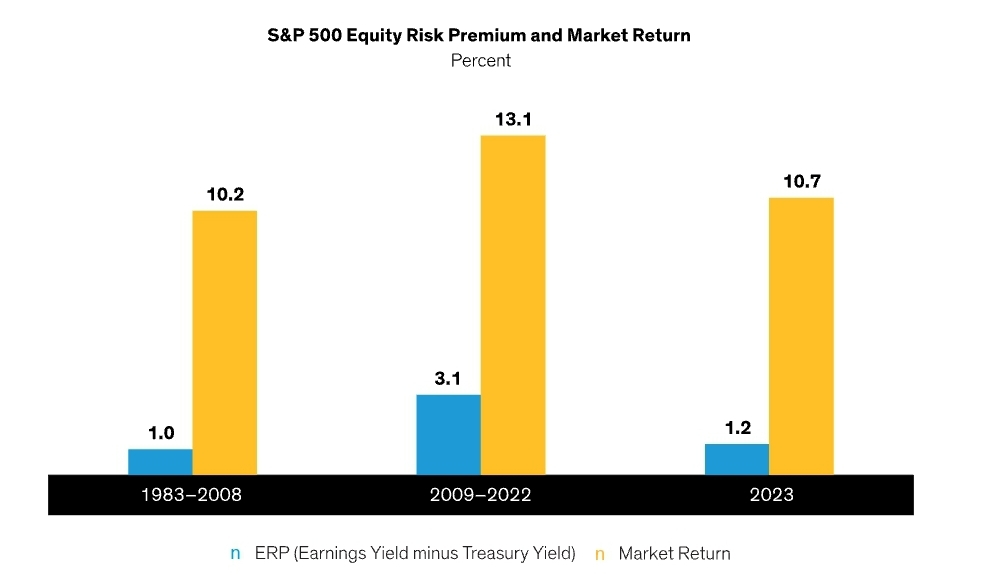

For context, the above chart shows the S&P500 returns and equity risk premium (ERP) against 10-year Treasuries, averaged over the 3 periods. If you believe that rates will be above 2%, then your ERP calculation must be lower than the 2009 to 2022 period. Implying that market returns must be lower too.

We don’t often go into board macroeconomics talk, but just to state our stance: we expect above 2% interest rates and hence also expect lower prospective market returns.

Also, we are positioned to benefit from this expectation of higher rates for longer by the profiles of businesses we own:

1. Low debt balance sheets.

2. Well run insurance companies who have the benefits of free leverage via premium float reinvested at higher rates than before.