PGR: Progressive (7)

FY2025 Update

PGR is a business we owned for a long time even before this fund started. The first buys were around $90/share and over time we added on. Currently, our average price is $162.5/share.

We have written 6 articles prior, readers can search the blog for them. Here’s a few important pieces:

Recently the stock has retreated quite a bit but the fundamentals have advanced substantially in FY2025.

Total revenues +15%.

Combined ratio 87.4% (2025), 90.3% (2024).

Investment income +26%.

Book value per share +18%.

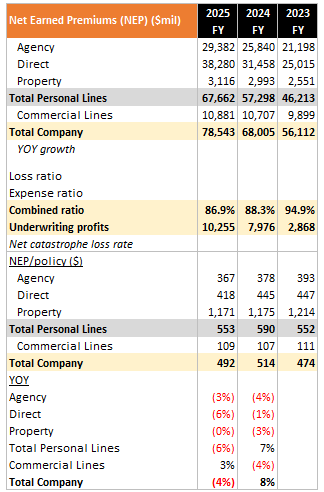

Now, if we look at the net earned premium (NEP) per policy for personal lines, it actually went down -6% YOY:

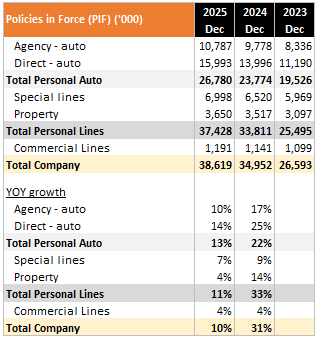

Policies in force (PIF) growth also slowed down in 2025:

What happened?

This has to do with the hard market turning as more competition is coming into the space. It doesn’t take much capital to underwrite admitted auto insurance since regulators allow $3 of premiums to be supported by just $1 of capital.

Furthermore, on 24 March 2023, Florida Governor Ron DeSantis signed House Bill 837 into law, passing extensive tort reform measures pertaining to civil litigation. The motivation is to curb rising insurance premiums because of the litigation cost that previously allowed policyholders to recover fees from insurers if they won court cases which encouraged heavy attorney fees.

In early March 2026, Florida’s 5 largest auto insurers are signalling average rate decreases of -8% for 2026. Because of this reform, Florida’s physical damage loss ratio improved from 112% in 2022 to 49.5% in 2025!

Florida is PGR’s largest market (as large as Texas), and we are guessing that market participants are expecting high customer churn rates as competitors start to slash premiums to gain market share.

There is evidence of this already. In 2025, JD Power Insurance Shopping Study recorded the highest shopping rate in 19 years: 57% of auto insurance customers actively sought a new policy, up from 49% the prior year. In fact, 29% of policyholders switched insurers in 2025 which is quite a deviation from historical 20—25% average.

The top 5 auto insurers in Florida (PGR, GEICO, State Farm, Allstate, USAA) control 78% of market share. All of them are planning to cut rates. GEICO is also spending more marketing dollars, shown by their expense ratio increasing from 9.7% to 12.4%.

LexisNexis data through Q4 2025 showed that 47% of in-force policies had been shopped at least once in the past 12 months — nearly half of the market have already started churning.

People are shopping because premiums are finally dropping, we should see the number of uninsured motorists decrease (by the way, a good sign for Copart).

Price War

Insurers have started to offer steep discounts:

State Farm filed for -10% rates deduction, they have cumulatively cut by at least 20% since October 2024.

GEICO announced lower rates for more than 700,000 Floridians.

PGR returned $1.2b of policyholder credits in 2025.

Sales distribution channel data from LexisNexis showed that direct-channel shopping grew +12.6% in Q4 2025. For insurers who depend on agency salesforce, this is a structural cost disadvantage versus direct channels in a price war.

Therefore, both PGR and GEICO are in an advantageous position. PGR has wisely increased the mix on direct channel from 57% to 60% in the past 3 years. Their agency salesforce is independent and doesn’t incur as much commissions as captive agents.

For GEICO, they sell mostly through direct and they are the lowest cost operator.

Underwriting Discipline

In the insurance business, it’s quite easy to gain market share — you just have to offer silly prices. Encouraged by the tort reforms and lower loss ratios, the danger of market share gains by price war is obviously mispricing of risk.

To add to the complexity, regulators have restricted the ways how insurers use telematics data:

Texas filed the first state attorney general lawsuit enforcing a comprehensive data privacy law. The January 2025 suit against Allstate and its subsidiary Arity alleged covert collection of driving data from 45 million customers through SDKs embedded in third-party apps including Life360 and GasBuddy.

California’s Privacy Protection Agency fined Honda $632,500 in March 2025 for data-sharing practices in connected vehicles, signaling that regulators will pursue the upstream data suppliers carriers depend on, not just carriers themselves.

New York introduced two bills in 2025/26 (Senate Bill 5486 and Assembly Bill A. 10364) that would force insurers to file telematics algorithms with the state superintendent and demonstrate non-discriminatory outcomes.

North Carolina’s House Bill 81, the most advanced of the state proposals, would require written consumer consent before any telematics data collection, with the right to revoke consent within 24 hours at any time.

In 2024, more than 21 million policyholders are enrolled in telematics programs. PGR runs Snapshot, Allstate has Drivewise, State Farm uses Drive Safe & Save. Even GEICO launched DriveEasy in 2019. These programs generate the granular behavioral data that enables precise risk segmentation in a falling-rate market.

So it’s a thorny issue:

Use telematics and risk regulatory actions.

Don’t use telematics and lose out in a price war where targeted rate cuts require behavioral data to avoid adverse selection.

Proper regulations is actually more of a boon to the insurance industry, because a stable regulatory environment allows insurers to better predict loss development, which results in lower premiums benefiting consumers.

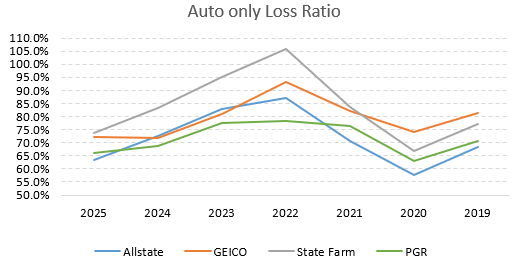

So among the fray, the company which can consistently match price to risk will be the winner, since auto insurance is a commoditized product. Among the top insurers in Florida, PGR has the lowest average auto loss ratio, followed by Allstate and GEICO. This proves the superior underwriting capabilities of PGR:

Winning a Soft Market

As rates fall, Florida will enter a soft market. Underwriting skill will separate insurers who gain durable market share from those who chase volume and build inadequate reserves.

Unfortunately, rate cuts don’t actually buy loyalty. When rebates were given post-COVID, it was not surprising that people demanded more. There’s no loyalty in a commoditized product.

But rate cuts do buy some time as customers adjust. It’s a mistake to treat this as a marketing event. To capitalize on this opportunity, insurers should invest in retention strategies — which PGR has done ahead of these reforms since 2022. They call these high lifetime-value customers “The Robinsons”. This demographic, aged 31 to 45, represents a key market for comprehensive bundled insurance products like home + auto insurance.

If executed well, we should see slower premiums growth but profitability will be maintained. This is the most important, we don’t care about high topline growth, but want to see profitable underwriting. By the way, PGR has been underwriting profitably every year since 2001.

Fun fact: In 2001, PGR began publishing monthly underwriting results — the first public insurer to do that. It’s still the only company doing it today.

For the last 20+ years, combined ratios were well below PGR’s target of 96%. The most recent loss development shows cumulative surplus, meaning that reserves are adequate:

Note: Personal lines cumulative surplus was $425m

Capital Allocation

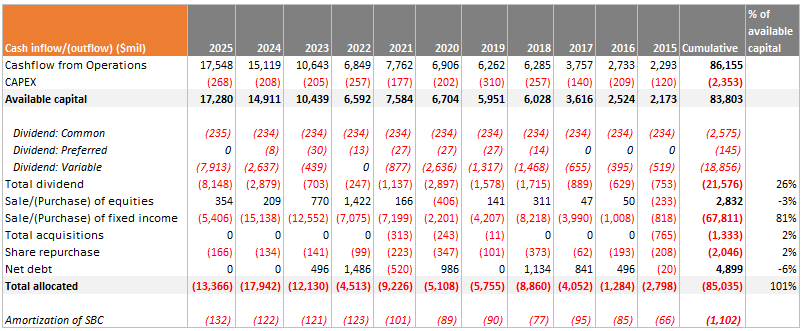

In 2025, PGR paid a $13.5/share special dividend on top of the regular quarterly dividends. There are 2 main uses of free cashflow:

Buying fixed income to support insurance liabilities.

Dividend payout.

Imagine that you bought PGR in 2015 for $26b, the cumulative dividends from 2016 to 2025 of $20.8b would have been 80% of your purchase price! Put another way, current dividends of $8.1b would be 31% yield of your cost basis — time is the friend of a wonderful business!

During 2024, PGR redeemed all of the previously issued 500,000 Series B preferred shares for an aggregate payout of $508m. These preferreds were issued in 2018 paying 5.375% annually with a 5 year call option.

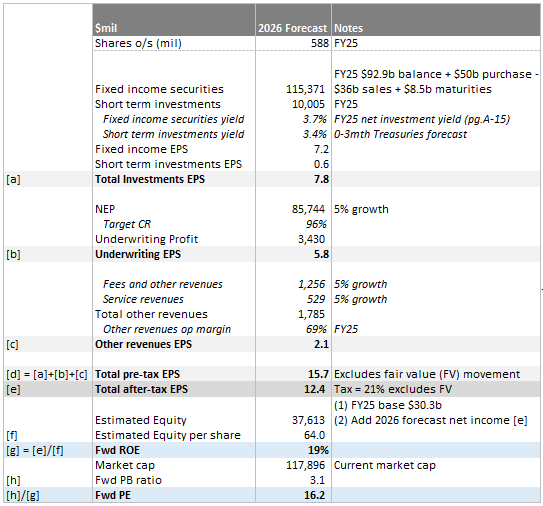

Valuation

An effective way to value PGR is to model the forward ROE and earnings multiple.

The main assumptions:

NEP, fees and service revenues conservatively grow +5%.

Fees and other revenues: Fees collected from policyholders relating to installment charges in accordance with bill plans, late payment and insufficient funds fees, and revenue from ceding commissions.Combined ratio 96%.

Fixed income yield 3.7%, short term yield 3.4%.

At today’s market cap of $117.9b ($202/share), we are paying 16x forward PE for a business that can generate 19% ROE — sounds good to us.

A few notes:

Equities portfolio unrealized pre-tax gains of $3.2b on cost basis $819m is excluded from valuation.

PGR doesn’t have any open derivatives.

Investment income covers interest expenses by 12.8x.

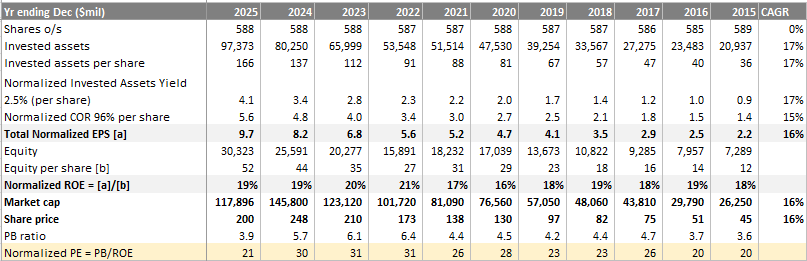

To sense check this ROE number, we can normalize the investment yield and combined ratio for historical numbers. So we can see under constant conditions what does the normalized PE ratio look like:

At 21x normalized PE basis, the stock is indeed cheap relative to history. We don’t see any issues that can impair the business in the foreseeable future.

We will add on to our existing position.

Excellent analysis! I recently posted a short write-up on inflation and the auto insurance industry. Would love your feedback if suits. Also, have you ever looked at Root (ROOT)?

Great analysis.. Considering the fact that the house bill 837 was implemented somewhere in 2023, I am not sure when this will be live across all the states.. perhaps that’s when we may start seeing an drop in insurance premiums and therefore more people getting a more comprehensive cover across the country. Being a copart shareholder may require waiting for some time for this tide to turn in their favour.