PGR: Progressive (5)

YTD Aug 2025 Update

We wrote in May 2025 that PGR stock was expensive at PE of 21x. Currently, the market cap is $143b and over the past 1 year the stock has fell -4%. However, business fundamentals have continued to improve. Consequently, PE has decreased to 13x.

Below are the highlights for YTD Aug 2025 YOY comparisons:

1. Growth in net earned premiums was +18% with its main Personal Lines business up +21%.

2. This growth comes with a very profitable combined ratio of 85%. This is much lower than their 96% target. YTD prior year developments were favorable at $912m and actuarial reserves released were $321m. If we exclude these releases, the combined ratio would be 88%.

3. Advertising expenses continue to be the main driver of a higher expense ratio. Direct channel reported expense ratio of 20%, while Agents ran at 18%.

4. PIF (policies in force) continued to grow at +14% for Personal Lines and +6% for Commercial Lines. PGR auto insurance market share went from 14% in 2022 to 19% currently.

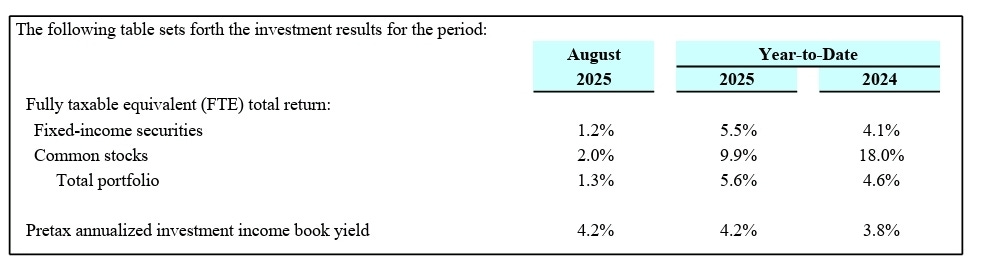

5. YTD investment income was $2.3b (annualized $3.5b). FY2024 was $2.8b. The growth is expected to decrease as Treasury yields have been falling. Yields remain elevated, we don’t expect it to collapse unless interest rates fall dramatically:

6. YTD underwriting profits were $7.5b compared to $5b last year (+50%). The reserve releases last year were much lesser at $118m versus this year’s $1,233m. If we remove this benefit of $1.1b, then underwriting this year would be $6.4b, a lower but still impressive +28% growth YOY.

The story of profitable growth and better investment book yields is still intact, although it is not accelerating at a pace seen last year.

YTD Aug net written premiums was $56.5b, while equity was $35.2b, meaning that PGR is only writing at 1.6x leverage. Historically, it has written premiums at 2.8x of equity. We think that over the long run, as PGR and GEICO take market share from State Farm, the market would become more saturated and high levels of premium/equity ratios cannot be maintained.

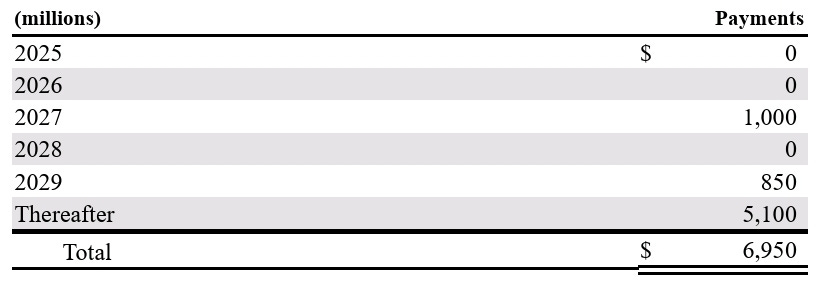

Debt levels remain unchanged at $6.9b. Repayments are due mostly after 2029, with no scheduled maturities in 2026:

Book value increased by $11b from YE2024 $26b to YTD Aug $35b mainly from investment assets $89b to $92b, driven by growth in the core insurance business.

Shares outstanding did not change, so book value per share increased by +37% from $43.7 to $60 entirely due to a larger asset base.

We will be adding more PGR shares at the current $143b market cap. The business performance has improved significantly over the past year, but the share prices haven’t moved.