PGR: Progressive (4)

Update for FY2024

We wrote about PGR in Sept 2024 here. At that time PGR was trading at 21x TTM earnings and we deemed that it was too expensive with these assumptions:

If PGR earns its target 96% combined ratio and leverages 2.8x to equity, it should earn ~11.2% ROE from underwriting.

Investment portfolio yields ~2.5%.

Expected ROE = 11.2%+2.5% = 13.7%.

Since then, the share price went from $250 to $285, that’s +14% over just 5 months. At least in the short run, PGR has over-achieved our assumptions:

Combined ratio was very good at 88.8%, far lower than the target 96%.

Investment portfolio yield was 3.9%, increasing from 3.1% in 2023.

Net written premiums increased YOY by $12.9b (+21%) with excellent underwriting profits, resulting in higher invested assets. This coupled with higher yields grew investment income by +50% YOY! We underestimated the rapid growth of investment income: 2024 $2.8b, 2023 $1.9b, 2022 $1.2b.

Policy in force (PIF) increased +18% YOY.

Net written premiums $74.4b on equity $25.6b is a 2.9x leverage.

Personal Lines: Auto (81% of net written premiums)

Growth in premiums were mainly due to volumes generated from greater advertising spend.

In 2024, pricing increased +3% compared to +19% in 2023. The prior year price increase would have contributed to the low combined ratio, we do not expect pricing as a driver of profitability to persist. Because auto insurance is afterall a commoditized product.

Another factor to the improved loss ratio was lower accident frequency by -5% and severity trends were stable at +1% YOY.

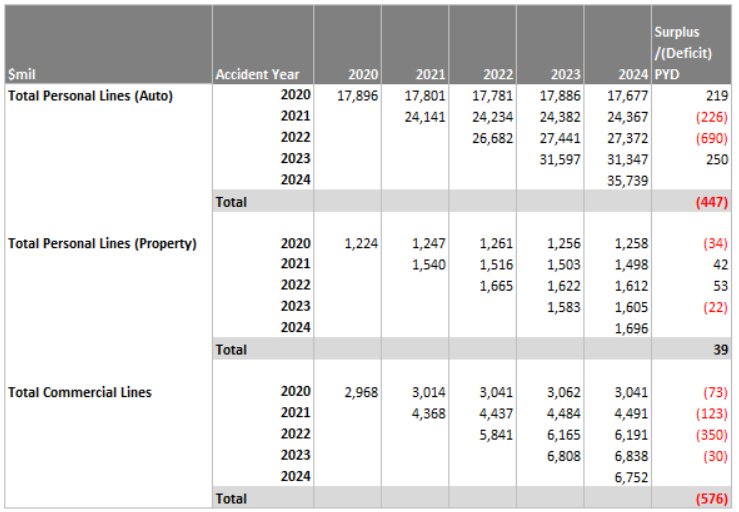

The combination of all these factors resulted in better prior year development (PYD):

From the loss development triangle, Personal Lines Auto had significant unfavorable PYD in Accident Year 2022 due to unexpected higher inflation. Following that, pricing was increased in 2023, and we started to see favorable PYD.

Fortunately, auto insurance is short tail in nature with renewal period within 6 to 12 months and almost all claims are paid out within 5 years. This gives PGR an advantage to adjust pricing quickly in response to variances with actuarial assumptions.

It is well known that PGR has a deep database of high quality drivers’ data which is very valuable in matching price to risk. PGR has been using Telematics for many years, this is essentially a primitive version of AI and predictive models. There’s likely room for cost efficiencies in their pricing model if AI proves to be useful.

PGR has an usage-based insurance offering called Snapshot which management believes to be more accurate in pricing risk. Adoption for Snapshot program decreased -9% in agency auto and increased +6% in direct auto.

In 2024, advertising spend was $4b (+150% YOY). PGR continues to maximize growth during hard market cycles while keeping combined ratio below 96%.

However, we know that onboarding a new policyholder is more expensive than retaining one. In an effort to improve retention ratio, PGR continues to bundle homeowner’s insurance with auto policies. The TTM total auto policy’s life expectancy decreased -4% YOY.

Personal Lines: Property (4% of net written premiums)

On the homeowners insurance segment, PGR achieved 98.3% combined ratio. Since 2023, underwriting has turned profitable after reporting 110.5% combined ratio in 2022. Management continues to reduce exposure in more volatile markets and was willing to slow growth in exchange for profitability. They also prioritized insuring lower risk properties (eg. new construction, existing homes with newer roofs), accepting new business for homeowners products only when bundled with auto insurance.

PGR began exiting the non-owner occupied home market and expanded cost sharing through mandatory wind and hail deductibles.

Commercial Lines (15% of net written premiums)

About 90% of PIF have 12-month terms and majority of business is written through independent agency channel, with about 10% through direct channel. New business increased +8% YOY, this was depressed from the for-hire transportation segment as freight market conditions continue to be weak. If we exclude for-hire transportation, the new business growth would have been +15% YOY.

Average premium per policy also grew by +5% reflecting the rate increases in 2023.

This business segment carries the same economics as the auto segment with combined ratio of 89.4% improved from prior year of 98.8%.

Incentives: Gainshare

The incentive plan is applicable to all employees except temporary staff. The performance measure has not changed for decades, it is simple yet effective:

Growth in PIF

GAAP combined ratio target 96%

If the combined ratio is above 100% then payout is zero.

These incentives drive profitable growth which is what a disciplined underwriter should be doing.

Investments

PGR invests most of their insurance float in fixed income. As at 2024, $76.7b was in fixed income and $3.5b in equities. Below is the performance breakdown:

Clearly, we don’t buy PGR for their ability to generate long term returns from float investing since more than 95% of invested assets are in fixed income. The attractiveness of PGR is its ability to underwrite profitably while maintaining a good growth rate.

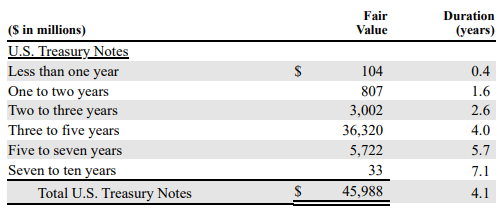

During 2025, we expect ~$7.6b (or 25%) of principal repayment from fixed income portfolio. As long as underwriting is profitable, the policyholder’s premiums self-fund their liabilities, so there is no risk of fair value losses from interest rate risk. Below is the duration details:

Shares Repurchased

In 2024, PGR repurchased 0.7 million common shares at total cost of $134m (average price $191/share).

The policy remains the same: buybacks happen to neutralize dilution from stock-based compensation, and when shares are trading at below fair value.

Conclusion

It was a very impressive year for PGR, however we believe that such outlier performance cannot persist. Effects from price hikes cannot be maintained for long as auto insurance is a commoditized product. GEICO being the lowest cost producer, has a huge competitive advantage.

We can’t think of any risk of capital loss with this investment, while our only concern is the price tag.

In this case, we continue to hold our position and wait.