OXY: Occidental Petroleum (2)

Anadarko Acquisition

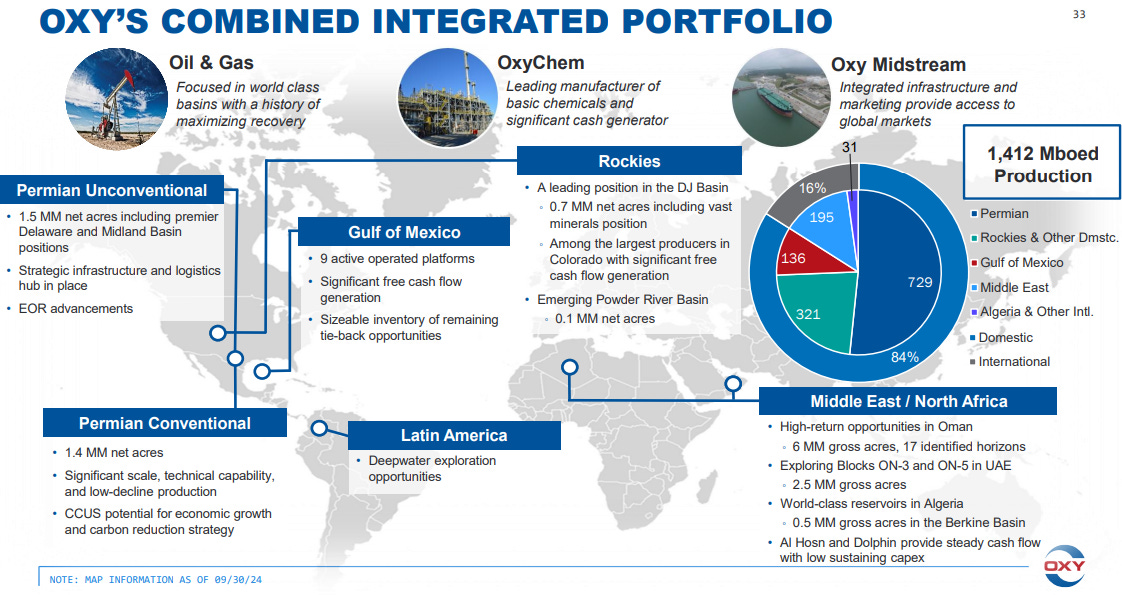

It helps to start from 2019 when OXY paid $55b for Anadarko, outbidding Chevron with the help of $10b preferred equity investment from Berkshire. Before this acquisition, OXY did not have a significant presence in the Permian. Post acquisition, 84% of assets operate in the Permian:

The acquisition was not of best timing, shortly after the COVID pandemic came and drove oil prices to all time lows. OXY took on a huge amount of debt to buy Anadarko and with oil prices depressed it was unclear whether or not the business could generate enough cash to service its debt. As a result, the share price collapsed from $45 to less than $10 during 2020.

Today, after the momentary oil price shock, the share price is back to $45 and debt has reduced significantly (2019: $38.5b, Q3 2024: $25.5b).

Is this due to managerial skill or luck?

We think it’s both. Obviously, we can’t deny the fact that the rebound in oil prices helped OXY. However, management has also been clever with capital allocation, selling off non-Permian assets to pay down debt and returning cash to shareholders instead of doing speculative oil discovery.

OXY competitive edge

If we take a broad view, there are 2 ways to evaluate the attractiveness of a business that is heavily influenced by commodity prices:

Are we able to predict commodity prices

What is the relative competitive advantages of the business versus its peers?

We have no idea what oil prices will be in any time frame, but we are quite certain that we can analyze the competitive advantages of OXY. Experience tells us that when the product has commodity-like features, the low cost producer usually has the strong competitive position.

For example, in banking where money is the commodity, the lowest cost bank usually is more defensible during market cycles compared to those with just high net income margins alone. Another example, in the auto insurance industry companies like GEICO and Progressive take market share by having low underwriting expenses.

In 2006, Buffett mentioned this cost factor:

If you have an oil-producing company, you want a management that, over a five- or 10-year period, discovers and develops oil at lower-than-average unit cost. There’s been a huge difference in performance in that among even the major companies, and I would pay the people that did that well. I would pay them very well, because they’re creating wealth for me.

Then in 2007, he makes this point again:

If oil goes from $30 to $60 a barrel, there’s no reason in the world why oil executives should get paid more for what’s going on. They didn’t get it to $60 a barrel. If they have low finding costs, which is under their control, I would pay like crazy for that. A person who finds oil and develops reserves at $6 a barrel is worth a lot more than somebody that finds and develops them at $10 a barrel, assuming they’re similar-quality reserves.

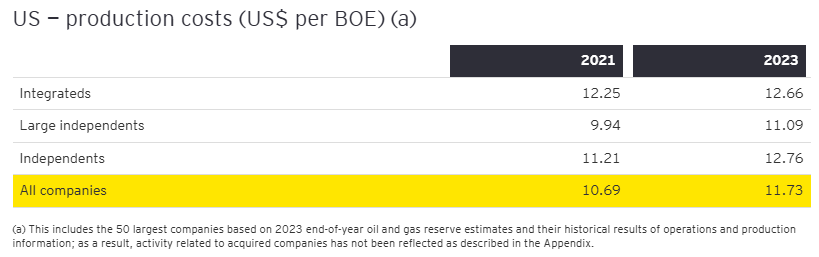

OXY’s domestic cost per BOE (barrels of equivalent) is $8.65 (Q3 2024), compared to industry wide averages:

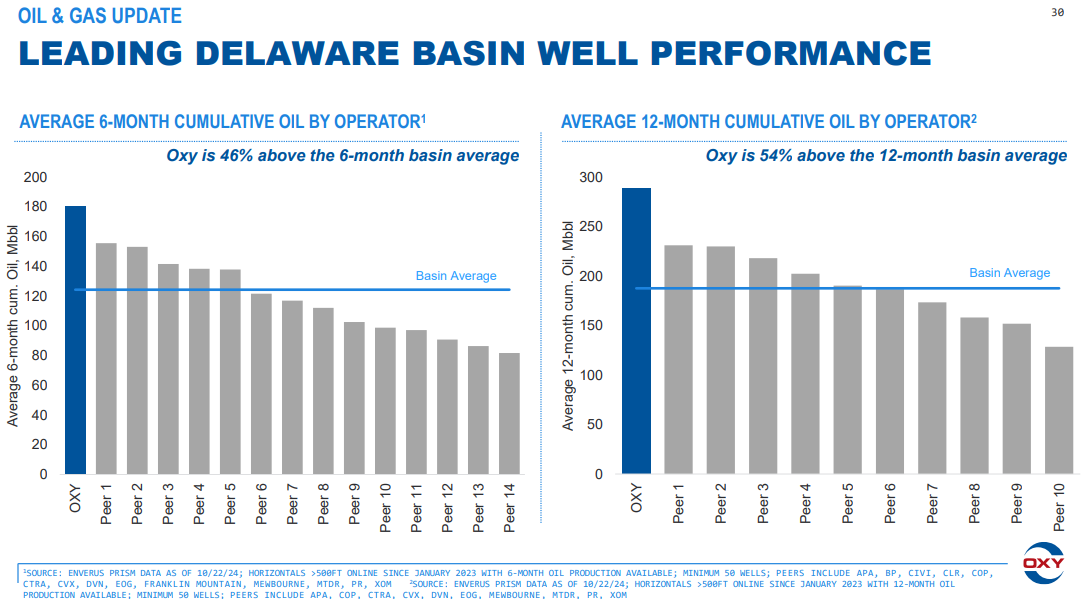

In terms of well performance, OXY is above average too:

Incentives

In the 2024 proxy, one of the main incentive driver is “spend per barrel” (pg. 44). This metric is defined by the sum of SG&A, OPEX and CAPEX, divided by MMBOE (millions of BOE). It has a weightage of 70% in the scorecard, in 2023 the target was $29.25 and they achieved $28.22.

Another incentive driver is “cash return on capital employed (CROCE)”. This was added as a financial metric in 2023 to provide incentives for management to use capital efficiently. It shares the same category weightage as “spend per barrel” and the target was 24% with 23.3% achieved.

Well efficiency and focus on cost control ultimately results in lower oil breakeven prices and greater resiliency during market cycles. OXY breakeven oil price is ~$40/barrel and it was selling oil at average $76/barrel. For context, Permian basin breakeven average price is $65/barrel.

Domestic Assets

The acquisition of Anadarko increased OXY’s domestic US assets and it is an advantage because overseas drilling comes with a geopolitical risk.

OXY has a mix of slow and fast decline wells. Part of the limited exposure they have abroad are operations in Oman where slow decline wells produce oil steadily. The Permian production can be increased or decreased in response to oil price.

OXY had 8 of the top 10 industry wells in the entire Delaware Basin from a six-month cumulative production standpoint. Today, it claims 8 of the top 10 DJ Basin (Colorado) wells drilled since 2019, several of which came online in 2024.

Capital Allocation

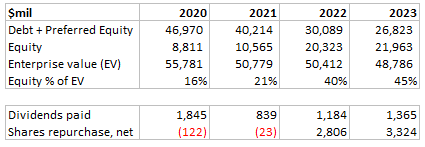

In determining the value of a company, debt holders come first followed by preferred equity, and common equity holders are last in line. Assuming that a company’s enterprise value (debt + equity) is relatively stable over time, then the more debt it has, the less value is left for equity holders. It also means that every $1 of debt reduced is effectively transferring $1 to common equity holders.

Vicki Hollub said in 2022 that as soon as OXY achieved its target leverage levels, they would start aggressively returning capital to shareholders via dividends and share repurchases.

This was how the situation played out:

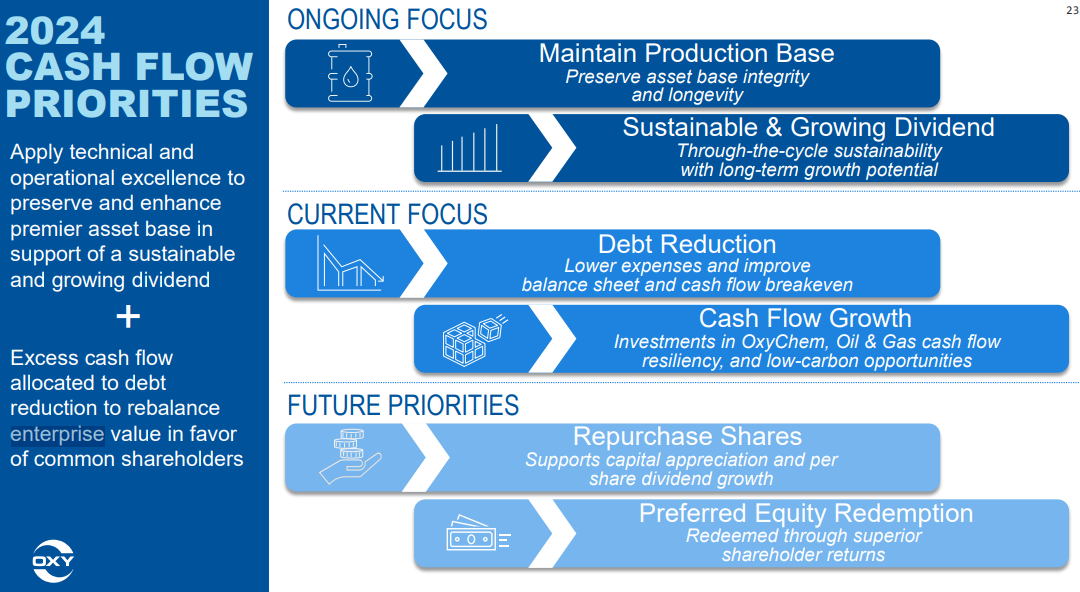

Observe that due to the paying down of debt, the equity % of enterprise value increased dramatically from 2020 to 2023. We should expect this trend to continue given that management has reiterated cashflow priorities:

In the Q1 2023 earnings call, Vicki Hollub said again:

I want everybody to understand that, looking forward, our capital program for our oil and gas development, chemicals, midstream, the corporation’s capital is going to be invested in a way that fits with the priorities we’ve established, one of which, and as important as any of the others, is investing in ourselves. That is the repurchase of shares. That’s a big part of our cash flow priorities. And I want to make sure that people don’t think that we’re going to, in the future, have capital spending so much that we can’t accomplish that.

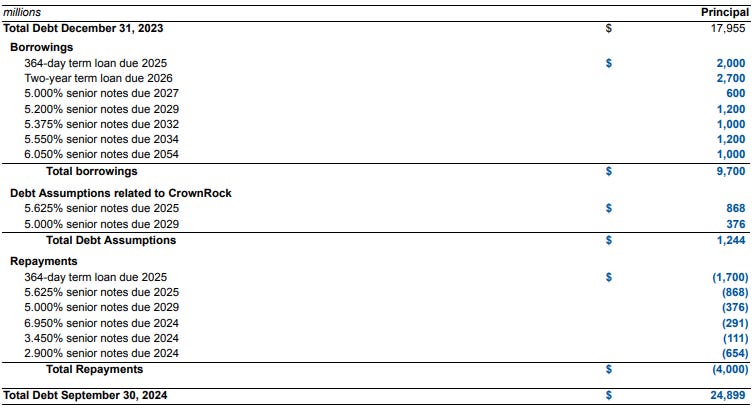

At the end of 2024 there was zero debt due. In 2025, there is $1.5b of debt maturity which their current unrestricted cash balance of $1.8b is sufficient to cover. OXY plans the medium term debt level to be $15b, which is a $10b reduction from $25b as at Q3 2024 (includes finance leases $785m).

CrownRock Debt Financing

In Aug 2024, the CrownRock deal was completed, resulting in the highest quarterly oil production in Midland Basin in over 5 years. This deal cost $12.4b (cash $9.4b and 29,560,619 common shares at $59.38/share) with $1.2b of existing debt.

OXY issued $9.7b new debt in July 2024 to finance CrownRock. As of Q3 2024, they repaid $4.0b, which included the satisfaction and discharge of the 5% senior notes due 2029 that were acquired with CrownRock.

Progress in the domestic divestiture program (closing of Barilla Draw, sale of a portion of WES holdings) has put OXY well ahead of repayment schedule.

Valuation

OXY realized oil worldwide averaged $94/barrel in 2022 and $76/barrel in 2023. Free cashflow was $12.9b and $6.5b for respective years. The sensitivity is ~$260m of FCF per $1/barrel change in oil prices (Q3 2024 conference slides 25).

Guidance was given for 1,430 to 1,470mil BOE/day in Q4. If we assume the lower end, then we can expect FCF for 2024 to be ~$5b (YTD Q3 2024 reported $3.5b with 1,412mil BOE/day in third quarter).

OXY current market cap is $44.1b, so FCF yield is 11% (TTM).

Our initial post had a valuation model using historical ROIC of 5%, no growth, and PE of 14x, the IRR is 7%. Add on dividend and buyback yields we should be getting more than 7% total return.

Conclusion

We will start a position at today’s market cap of $44.1b.

These are the key points for the investment to work:

1. Oil and natural gas reserves in the Permian will last for many decades (refer here for details).

2. OXY continues to be the low cost producer.

3. OXY continues to reduce debt and return cash to shareholders, keeping oil discovery minimal.

So far, management has worked towards these points and produced good results. The macro view is that demand for energy, in terms of natural gas and oil, will continue to increase, and OXY has assets and low cost production techniques to take advantage of this.

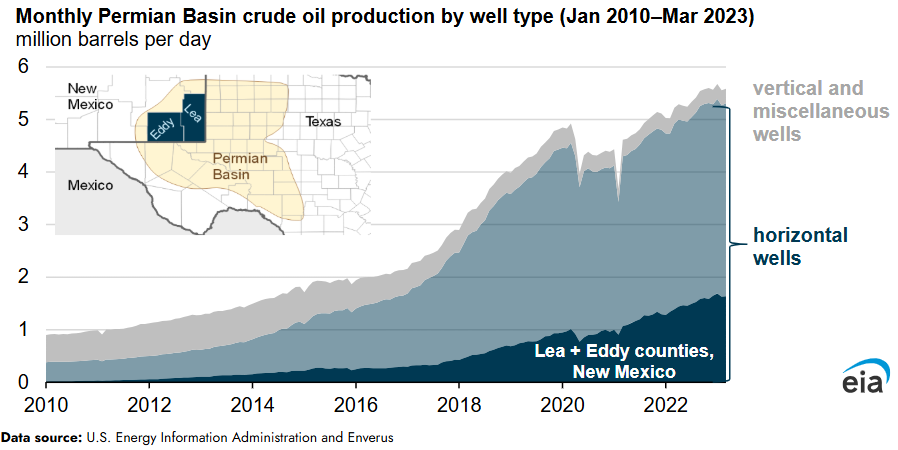

Historical chart of Permian Basin production: