OXY: Occidental Petroleum

History

OXY was founded in 1920s and was a largely unprofitable small driller until Armand Hammer bought a controlling stake in 1950s. In 1956 Hammer and his wife each invested $50,000 in two oil wells that OXY planned to drill in California. When both wells struck oil, Hammer took an active interest in further oil exploration. Under Hammer, OXY diversified into multiple sectors like chemicals, fertilisers and even owned a meat packer at one point (Iowa Beef Processors from 1981 to 1987, later acquired by Tyson Food in 2001). Hammer treated OXY as his personal investment vehicle for all practical purposes, despite owning only 1% by 1990s.

After Hammer’s death, he was replaced by Dr. Ray Irani, a chemical engineer who brought OXY’s focus back to oil. Irani immediately divested all non-core assets and expanded OXY deeper into the Middle East. His Lebanese heritage helped form key relationships in Middle East and OXY vastly expanded there. When Libya’s sanctions were lifted in early 2000, OXY was the first company there getting concessions for oil fields.

By 2008 to 2009, shareholders were increasingly worried that Irani was paying himself exorbitant amounts as CEO. He was the highest paid executive amongst oil companies and awarded himself close to $730m in stock options. By 2010, shareholders voted to fire Irani and he was replaced by the CFO, Steve Chazen, who was instrumental in bringing OXY’s focus back to domestic assets.

Chazen set the strategy that OXY would continue until the present date under Vicki Hollub who was appointed CEO in 2016. Vicki started her career in 1981 with Cities Service which was a fully integrated oil and gas company, it was then acquired by OXY in 1982. She subsequently held technical and management positions for OXY.

OXY’s strategy was to look for more oil where it is already known to exist and focus mainly on Permian. Currently OXY is the leader in Enhanced Oil Recovery (EOR) in the Permian Basin. It has 3 principal businesses: oil and gas, chemical and midstream. The oil and gas segment explores, develops and produces oil and natural gas. The chemical segment manufactures basic chemicals and vinyls. The midstream and marketing segment gathers, processes, transports and stores oil, natural gas, CO2 and power. It also optimises its transportation and storage capacity, and invests in entities that conduct similar activities. Given that ~80% of OXY’s current earnings come from oil, we will mainly focus on their oil business for the rest of the article.

Unlike other drillers, OXY has always preferred to hold long-lived legacy assets with enhanced secondary, tertiary recovery properties rather than brand new oil fields.

Secondary/Tertiary Recovery and EOR

Typically, in any oil well, crude gets pushed from sub-surface to top due to the inherent pressure build up in the well. This pressure in effect is released by the drilling and oil comes up. However this pressure does not push all the oil out and if rock is not porous enough, this oil gets trapped in the rocks.

As the pressure difference between the well and atmosphere reduces, the flow begins to also reduce. In this setting, Enhanced Oil Recovery (EOR) methods such as pumping water or CO2 into the well, which will in effect push the remaining oil up, thus extending the life of the well. CO2 reduces viscosity of oil which helps bring it out easily.

Although Permian Basin was recognised as a ready candidate for CO2-based EOR due to its favourable rock structure, it was not until late 1980s when CO2 pipelines were laid bringing down the costs of EOR.

OXY has historically purchased long-lived legacy assets in Permian Basin, applied EOR techniques to improve yield in these fields. Currently, OXY has over 2,500 miles of CO2 pipelines, in-house supply of CO2 via Bravo Dome (this is a 99% pure natural carbon source field in north-eastern New Mexico). For competitors to start their EOR process, they would have to invest in building these pipelines, or buy CO2 which we estimate would easily be $2b to $2.5b worth of CO2 for size of OXY’s operations (20 million tons per year @ $100/ton).

History of Permian Basin

The Permian Basin is the largest oil field in United States both in acreage and production. Spanning over 86,000 square miles across Texas & New Mexico, the Permian accounted for 46% of US oil production in 2022. Much of this increase came after 2009, due to technological improvements in hydraulic fracking, horizontal drilling and EOR methods. Even though shale-wells have much lesser lifetime (1-1.5 years), over 50% of current US oil production comes from shale, making it a critical strategic resource.

Oil in Permian was discovered only in 1922. Before that, the Permian was largely considered an oil graveyard; population was sparse, land was arid and there was no transportation facilities. Back in late 1800s, transportation and refining was a large portion of oil prices, which resulted in prospectors avoiding the West Texas areas.

As technology improved, so did the production in Permian. Despite being a 100 year old oil field, it is still the largest producer of oil in the US with several decades of reserves left and this has been closely linked with technological development in drilling.

Permian consists of 3 sub-basins. Entirely located within Texas, on the eastern edge is the Midland Basin. On western edge, located in New Mexico is the Delaware basin. Between Midland Basin and Delaware is Central Basin. Hydrocarbon deposits in Permian is usually a mix of oil and natural gas. There are few deposits with predominantly natural gas but those are a minority.

Recently, the United States Geological Society evaluated the potential of one formation in the Permian Basin, the Wolfcamp shale, and estimated a potential recovery of 20bbl (billion barrels) of oil and 1.6bbl of natural gas liquids. To put this in perspective, the massive East Texas Oilfield, the largest conventional field ever discovered in the lower 48 states, will produce roughly 5.5bbl to 6bbl of oil when it is ultimately depleted. In short, the Permian has a long way to go before depleting.

Permian Basin predominantly has shale formations, with the wells having longer horizontal components. These wells span long stretches horizontally and stack on top of each other. Because of this feature, some geologists describe the Permian Basin like a layered cake of stacked potential producing formations.

The benefit of stacked layers is that drillers can locate multiple wells at one surface location and drill from that site to different depth horizons. This procedure reduces surface damage and substantially increases drilling efficiency by reducing costs of pipelines, tanks, separators, and compressors.

Recently, drillers have developed technology to drill horizontally to tap into more oil wells from a single location. This allows drillers to reach more inaccessible location with vertical drilling and access more wells from a single location. Once drilled, they use hydraulic fracking to break these shale formations to extract oil.

As technology improved, we are now able to access previously inaccessible sources of oil in Permian. One crucial method is going longer distances laterally with modern equipment, they are cost efficient and reduce drilling time, resources to move rigs and crew. It is estimated in the Delaware Basin the breakeven WTI price of a well decreases from $38/b to $34.5/b when going from 5,000ft to 10,000ft laterals.

However, one big requirement for longer lateral drilling is large areas of contiguous acreage. OXY has ~2.8 million net acres in Permian. Second largest player, Pioneer Natural Resources has ~1.4 million acres after ExxonMobil acquired it in May 2024. This partly explains the latest land-grab acquisitions in Permian basin (Exxon + Pioneer; OXY + Anadarko, Crown Rock).

OXY Acquisition Playbook

Elk Hills (1998)

In 1998, OXY paid $3.5b to buy a mature oil field which previously owned by the US government. Elk Hills was a 100 year old oil field and OXY was widely criticised for over-paying to buy a field that was largely “depleted”. This was largely funded through proceeds from sales of non-core assets.

After the purchase OXY aggressively employed CO2 flooding to increase yield and reserves. By 2000s, Elk Hills was giving more oil than it ever had before and had higher reserves than what OXY bought. In 2006, it was estimated that Elk Hills had 109 million BOE (barrels of oil equivalent) of reserves. By 2009, OXY discovered additional 150 million BOE of reserves (1/3 oil, 2/3 natural gas).

By 1998, Elk Hills was producing close to 54,000 BOE/day. Then in 2006, it was sold to California Resources Corp, it was doing 91,000 BOE/day. A 68% increase in production from a 100 year old field.

The Elk Hill acquisition returned average 15% free cashflow return on capital employed when it was operated by OXY. By 2003, it had cumulatively generated $3.5b in FCF, paying back its acquisition price in 6 years.

This was one of the first notable examples of OXY’s playbook that we will see repeat in other acquisitions:

Buy legacy assets with optionality;

Drill with CO2-based EOR methods to enhance asset quality;

Increase both production and reserves.

While we simplified this playbook, in practice this is complex to run. OXY has to focus exclusively on geology favourable for EOR, so they focused mainly on Permian Basin. Next, this requires infrastructure to transport CO2 which is the biggest cost for EOR. By 2015, OXY was the second largest CO2 pipeline owner in the US. The flywheel effect comes from 2 areas:

Depth of EOR knowledge where Oxy has decades of experience.

Extensive sub-surface data of Permian basin.

These two factors help reduce operating costs, even if it appears that OXY is overpaying. Additionally, this is a low-risk playbook with very minimal speculative drilling.

Altura Energy (2000)

OXY acquired Altura for $3.5b in April 2000. This acquisition drastically increased OXY’s exposure in Permian basin. Along with this, they swapped Alaskan oil assets for low-cost CO2 unit called Bravo Dome with British Petroleum (BP). This put in place 2 key elements OXY needed for driving the EOR playbook: Large legacy assets and cheap CO2 supply. To fund the Altura acquisition, OXY took $2.4b of non-recourse loan, making it a leveraged buy-out.

Even in this acquisition, OXY has had very satisfactory free cashflow return on capital employed of 15% to 20% from 2000 to 2003. OXY stopped publishing Altura’s stats beyond 2004 making it hard to extract it’s returns.

Anadarko (2019)

This was arguably one of the most divisive deals by OXY. A $38b acquisition, bidding war with Chevron followed by COVID oil crash followed by a rapid rise in oil prices. This alone made OXY one of the largest oil operator in Permian. Immediately after the deal, Vicki Hollub was widely criticised for buying a company much bigger than OXY and by leveraging up the balance sheet (Berkshire loaned $10b in form of perferred stock paying 8% dividend). It was clear OXY wanted Anadarko only for their Permian and midstream assets. Even prior to closing the deal, OXY had a deal to divest Anadarko’s assets in Africa to French oil major Total for $8.8b.

Anadarko holds close to 1.3bbl of oil in the Permian. However, looking at their net additions to Proved Resources (refers to proven oil extracted), they have done little in terms of EOR. Below is the breakdown of our estimate of the Permian assets value:

At 1.3bbl of oil equivalent reserves, OXY paid $27/barrel. But if they are able to enhance those reserves by 20% to 25% (historical averages), they ideally paid closer to $22/barrel. This appears in line if we look at recent transactions: Exxon acquired Pioneer at $27/barrel and Chevron acquired Hess at $48/barrel.

Crown Rock (2024)

OXY bought Crown Rock at $12.4b expanding OXY’s area in the Permian by 94,000 acres, expected to add an average daily volume of 170k barrels of oil equivalent. It was financed by $9.4b cash and 29.6 million shares with assumption of $1.2b existing debt at Crown Rock.

OXY will divest $4.5 to $6b of non-core assets from Crown Rock to repay debt.

Summary of Economic Moat

A few themes from studying OXY’s acquisitions:

Focusing on Permian: After 2010, OXY decided to increase Permian activity and reduce Middle East exposure.

Buy legacy assets with optionality: OXY prefers existing oil in known fields with possible undiscovered large reserves.

Enhance asset quality and reduce cost: Once acquiring a legacy asset, OXY uses EOR methods to boost production and increase reserves which helps increase returns on capital.

Ability to leverage: Since they can exploit assets with EOR better than others, OXY has ability to pay up for oil fields even with leverage. OXY’s in-house CO2 supply, sub-surface knowledge in Permian gives an edge that competitors lack. For example, Exxon has CO2 supply but lacks sufficient Permian exposure in EOR; Conoco Philips has Permian exposure but only recently even started CO2-based EOR.

OXY’s acquisition playbook has largely become the growth strategy. Over the last decade, OXY ran with a focus on becoming the best EOR operated producer in Permian. There is this quote from the ex-CEO Chazen: “We are in oil-recovery business, not oil-discovery”.

This is OXY’s competitive advantage that we believe is an unique case in Oil & Gas.

Competitive Advantage #1: Large Acreage in Permian

Large contiguous acreage in Permian gives OXY the ability to further drill long lateral distances, thus reducing their capital and operational cost. As easy-oil depletes, it is likely the smaller land owners will be more willing sellers to OXY which will in turn help them drill longer lateral distances for oil.

Competitive Advantage #2: In-house Supply of CO2

As the largest owners of CO2 pipeline and supply, OXY will be able to further improve asset quality at a cheaper rate. CO2 supply is biggest cost in EOR methods that competition would have to bear which OXY has already established.

Competitive Advantage #3: EOR Knowledge

EOR was likely ignored as Permian was initially gushing easy oil. With limited CO2 supply and expensive pipelines, other players were not encouraged to invest in EOR. However, as easy oil depletes, we believe EOR is going to be extra critical to stretch the Permian assets further.

Competitive Advantage #4: Low Cost of Debt

OXY used up the low-interest rate environment to leverage their balance sheet in 2019 with Anadarko acquisition. The debt maturity schedule for next 3 years are respectively: $1b, $1.2b, $1.4b. As at 2023, long term debt was $18.5b with interest expense of $945m (cost of debt ~5%).

Competitive Advantage #5: Large and Growing Sub-surface Data

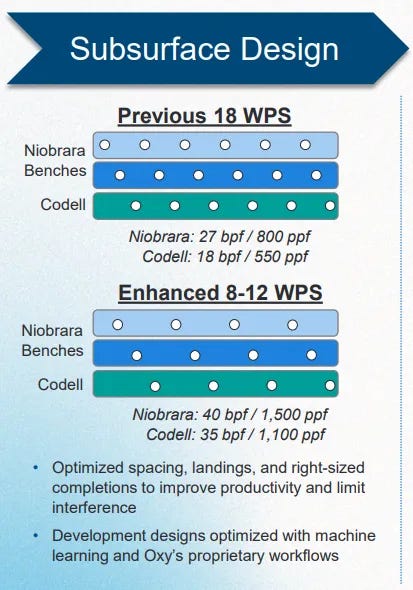

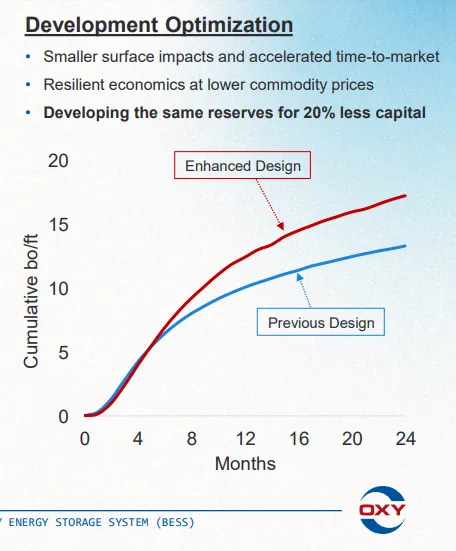

A large sub-surface data would help characterise underground geology better which in turn would help optimise the number of oil wells that are drilled. If OXY can drill lesser wells to produce same oil, it would reduce the production and capital cost per barrel. In the investor presentation, deep in Appendix, we found this:

For the Niobrara, Benches and Codell fields, OXY has reduced Wells Per Section (WPS) from 18 to 8-12, increased barrels produced for every foot drilled (bpf) from 27bpf to 40bpf in Niobrara. The sub-surface data provides additional leverage for OXY to enhance asset quality with relatively low capital, which they mention here:

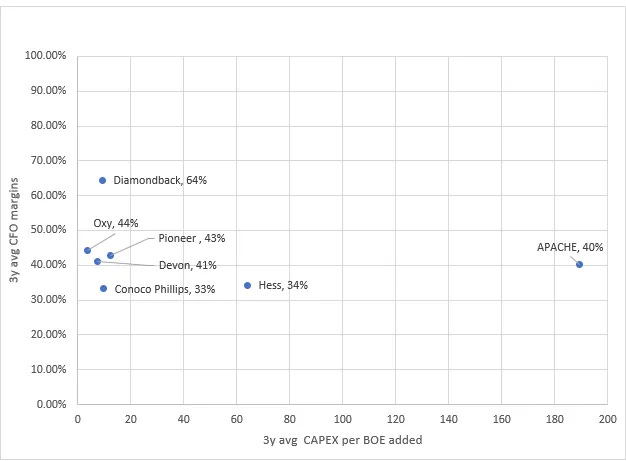

Comparison Metrics with Competitors

CAPEX dollar per BOE (barrels of oil equivalent) added

Simplified definition of “reserves” is an estimate of oil that exists under the ground in the land owned/leased by the company that can be profitably extracted. If a company increases its reserves by 100 million BOE and employs $1b in doing so, we could say it spent roughly $10/BOE.

This is a very crude metric because CAPEX also goes towards maintenance. Secondly, estimate of reserves is also determined by price and this can range very widely. We caution that this metric is simply used for comparing 2 companies during the same period. That way, we are able to keep much of external factors constant.

Cashflow Margins

This is cashflow from operations divided by revenue. We do not like operational margins or net margins as there can be significant asset impairment/gains that find its way into income statement. Secondly, cashflows give a better sense of debt serviceability, shareholder return and ability to acquire more assets.

When we compare CAPEX/BOE of reserve added versus cashflow margins across all US based E&P players, we see that OXY has been adding reserves at $3.62/bbl versus average of $9.62/bbl. Their cashflow margins are in line with industry which means they are really good at finding & development, and quite good in production.

Industry-wide Capital Allocation

Cash deployed for CAPEX has come down from over 80% (2011 – 2014) to 45% in 2022. Remaining cash goes to either debt repayment or dividends and share repurchases. Industry wide capital allocation has become rational and shareholder friendly.

Currently OXY’s preferred equity from Berkshire is the most expensive quasi-debt they have at 8%. So paying that down would considerably boost free cashflows which can go towards dividends and share buybacks.

In 2019, Berkshire invested $10b in 8% perpetual preferred shares and with warrants to purchase up to 83.86 million common shares at $59.62, exercisable in whole or part until a year after the preferred stock is fully redeemed. When Berkshire made the investment, energy companies were reeling from years of over-investment through 2015. COVID caused oil prices to be negative for a moment, OXY had the option to pay the 8% in shares instead of cash, which they did for several quarters.

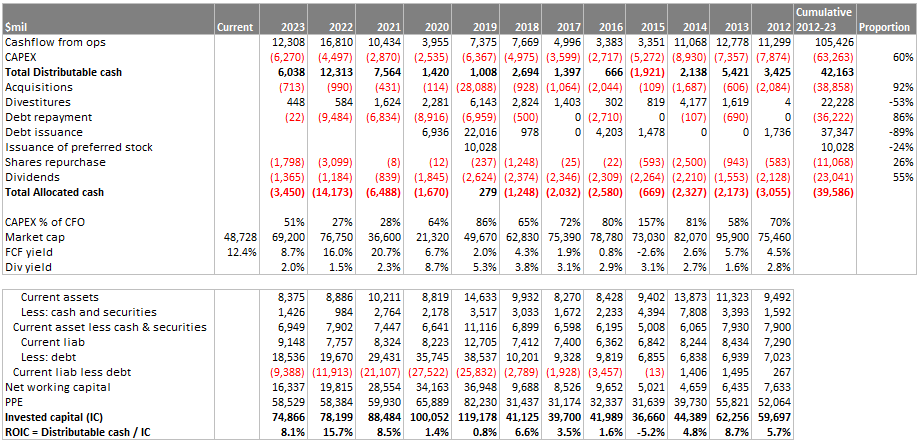

Below is the cumulative allocation of FCF and ROIC:

There are a few notable observations:

CAPEX % of CFO did trend down, this is a good trend as the ROIC is not very attractive for reinvestment.

Share repurchases and dividends cumulatively were 81% of distributable cash. This shows that OXY is returning cash to shareholders which is a good sign.

Cumulative debt issuance and repayment largely offset each other.

Acquisitions net of divestitures is 39% of distributable cash.

Note: We use distributable cash (or FCF) as the numerator of ROIC because the P&L has noise in impairment/gains on assets.

Risk #1: Asset Concentration

More than 80% of OXY production is in the Permian, so any problem there is a big problem for OXY.

Risk #2: Strong Competition

OXY still fights the big companies like Exxon and Chevron in land grab. It is clear that the Permian is becoming a focal point for all players which means the acreage has quickly gotten very expensive. This means poorer returns to shareholders.

From recent headlines, it is clear that the Permian is becoming a focal point for all players which means the acreage has quickly gotten very expensive.

Valuation

The average ROIC from 2012 to 2023 is 5%. It’s not a high ROIC, but fortunately OXY management shows intelligent capital allocation by returning much of the cash back to shareholders via dividends and buybacks. Currently, at $48.7b market cap, OXY is trading at PE of 14x. If we assume zero growth in FCF, we can solve for our IRR = 7% (given ROIC = 5% and PE = 14x).

Similarly if we run a reverse DCF on dividends and share buybacks, assuming zero growth, we get IRR = 6.5%.

Add on dividend yield and share count reductions, the zero growth scenario could yield a prospective return of ~10%.