NVR: NVR Inc (2)

Update for FY2024

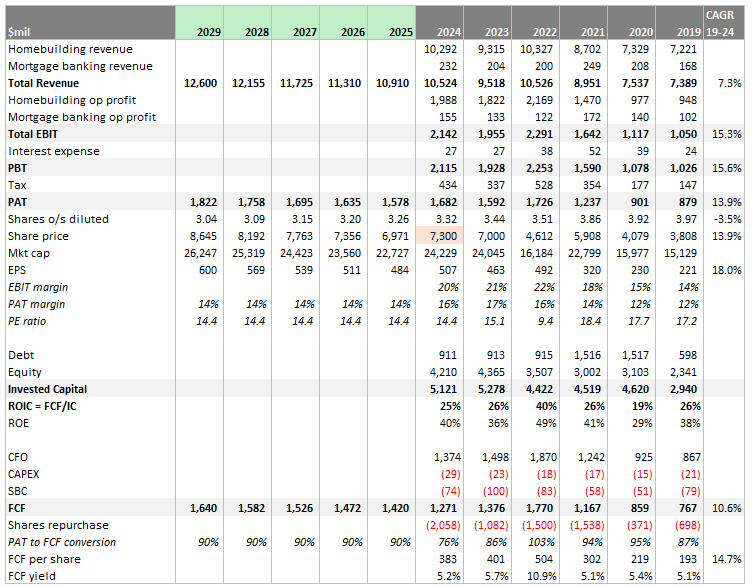

Year 2024 has closed, these are the key achievements YOY:

Homebuilding sales +10.5%

Mortgage banking sales +13.7%

EBIT +9.6%, PAT +5.7%, EPS +9.5%

256,871 shares repurchased at average price of $8,010 (FCF yield ~4.8%)

Free cashflow (FCF) -7.6%, FCF per share -4.5%

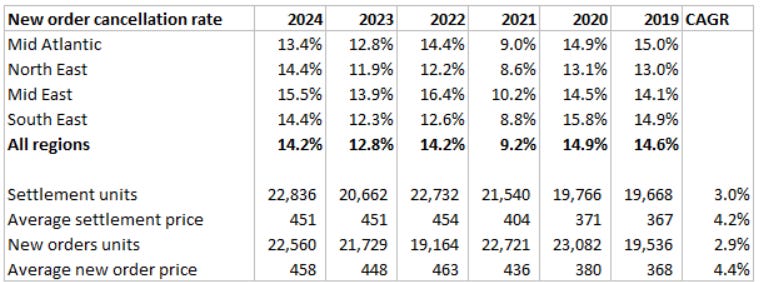

Cancellation rates went back up in 2024 likely due to affordability pressures caused by higher mortgage rates. Prices per unit are stable, new and settled units continued to grow.

Despite improving fundamentals, the share price today is $7,300. We will do a valuation exercise here.

Industry Dynamics

The homebuilding industry has little barriers to entry. In the US there are over 400,000 homebuilders, however most of them are small, if we consider that there are more than a dozen publicly traded homebuilders and DR Horton is the largest with only 5% market share. This shows that the industry is fragmented and the top 100 homebuilders are estimated to be responsible for completing only 50% of all homes.

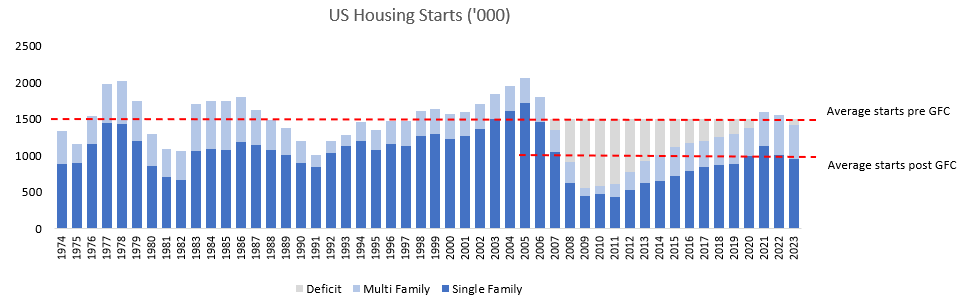

We have shown this chart above before, but it is worth reminding that there is a supply deficit of homes post-GFC (gray bars). The over-supply pre-GFC was followed by 15 years of under-supply, given that population grew over these years, it is obvious that the current housing dynamics is demand exceeding supply:

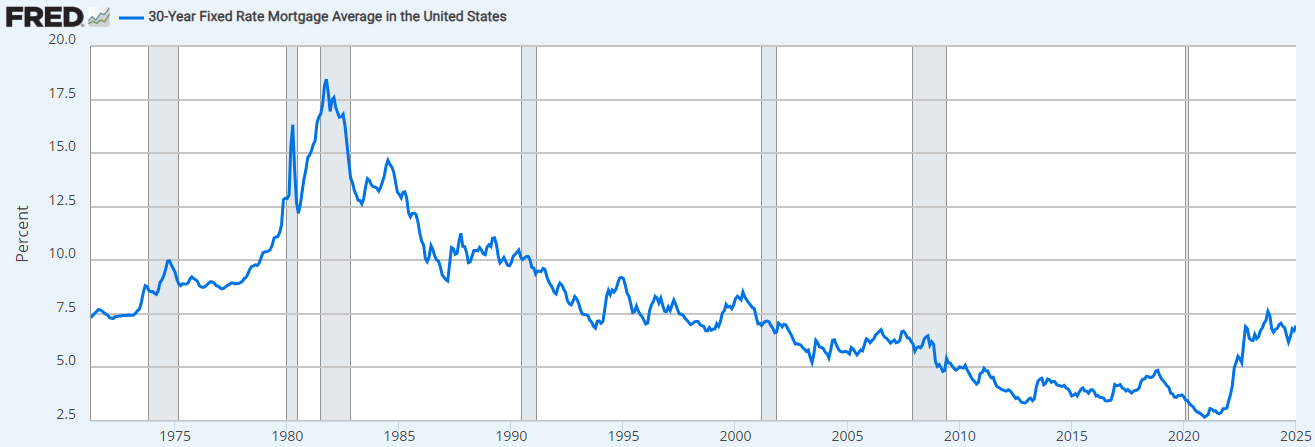

Although these statistics point to a need for more houses, we still have to consider whether or not people can afford it. Homebuilders can focus on building smaller and lower cost homes, which many of them do, but they cannot make potential homebuyers wealthier. The higher 30-year mortgages recently have caused problems with affordability:

Nevertheless, while we may have been used to low interest rates, from 1975 to 2000, 30-year mortgage rates seldom dipped below 7%. Furthermore, from 1979 to 1991, 30-year mortgage rates were in the double digits. While the real rate was lower back then (inflation was higher) it doesn’t really matter because many homebuyers didn’t have guaranteed inflation-adjusted salaries and loans aren’t originated on future income.

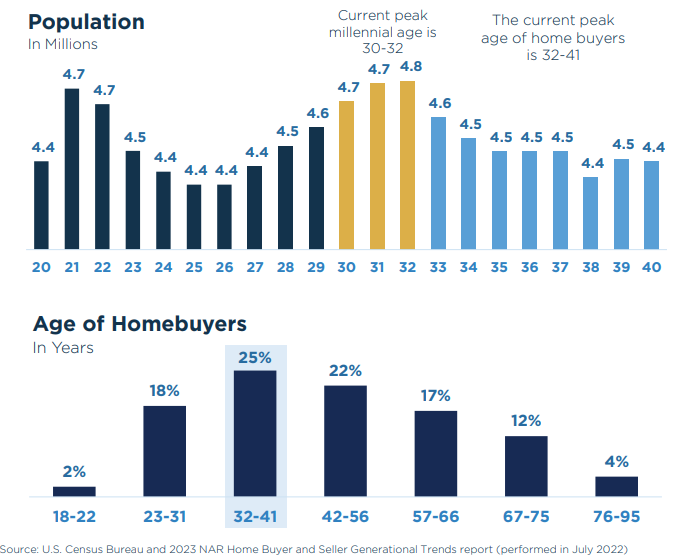

Another tailwind is the population distribution is concentrated at the age group of late twenties to early thirties. This happens to be the group that buys the most houses:

Insider Ownership and Incentives

NVR founder, Dwight Schar, retired from the Board in 2022 at the age of 80. He served as CEO from 1993 to 2005, and passed the baton to Paul Saville. He has been with NVR since 1981, took the role of CEO from 2005 to 2022 and became Executive Chairman of the Board. The new and current CEO is Eugene Bredow who has been with NVR since 2004, he was previously the President for NVR Mortgage Finance.

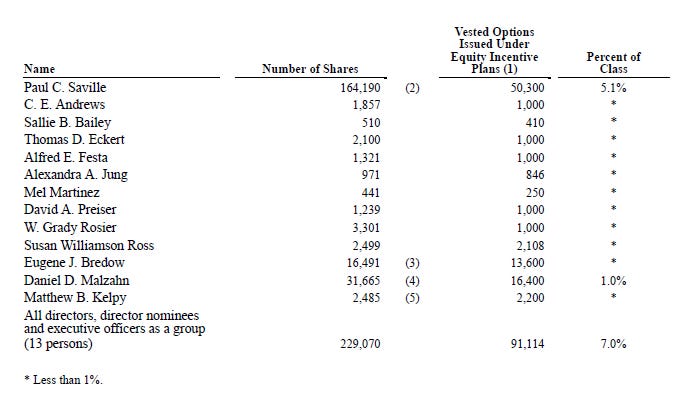

Paul Saville still holds a lot of shares with a 5.1% ownership of NVR valued at $1.2b (at $7,300/share).

CEO Bredow also owns a significant amount of 16,491 shares valued at $120m, many times his base salary of $900k.

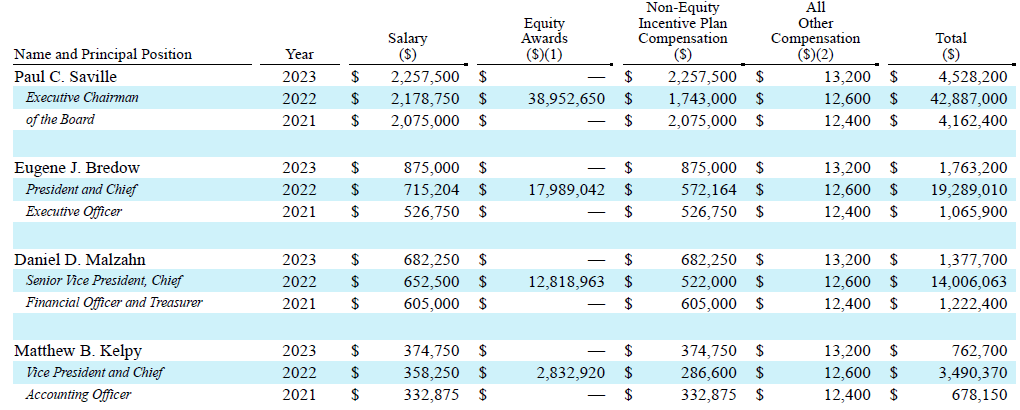

Of course the juicy part of compensation is in equity awards, otherwise known as share-based compensation (SBC).

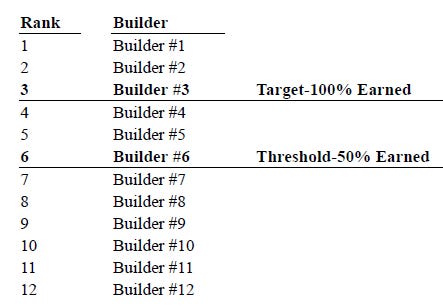

This SBC is achieved based on NVR relative ranking in return on capital:

These stock options have no value unless the stock price increases between the grant and vesting date. 50% of stock option grants are subject to attainment of a return on capital performance condition, and there is no opportunity to earn more than 100% of the target number of options granted, even if the return on capital significantly outperforms the peer group.

This is the peer group:

Return on capital is defined as:

NVR produced 10-year average return on capital of 27% and ROE of 38%, these achievements are the highest among major homebuilders in US. (Note: these returns remain stable over recent last 5 years too)

The reason for such high capital efficiency is due to high inventory turnover. NVR turns over their inventory 3.2x compared to LEN and DHI of 1.3x. It is worth noting that DFH (Dreams Finder Homes) is also an asset-light homebuilding, holding majority of land via options, it has inventory turnover of 1.9x.

NVR has several distinct elements that allow them to be much more efficient than DFH.

NVR only starts building a home once they get a non-refundable deposit from a buyer. They never speculatively build homes. They also will exercise the land option contract only after they have received a deposit. This means that the land is never on their balance sheet until they are ready to build on it (83% of balance sheet inventory is homes under construction that are in contract to be sold).

NVR has local build density meaning that they will build many homes next to each other.

This is important for two reasons. The first is that it allows them to have a building product manufacturer nearby and save on transportation of materials. Second, they can start work on multiple homes at the same time. This is only enabled by getting enough orders placed close by within each building community.

Similarly, having many of their homebuilding community projects nearby also rationalizes NVR setting up manufacturing facilities for building products, which in turn reduces the cost to build homes as manufactured products have much higher labour utilization rates and lower defection rates due to standardization. The close proximity between building product manufacturer and home site not only reduces cost, but saves on shipping time.

DFH allows more home customization and is willing to incorporate buyers’ desired fixtures for a premium fee, NVR standardizes their builds to a larger extent, with very limited premium features available and fewer styles to choose from. DFH has a design studio to mix and match different desired finishes, NVR has just a handful of styles to choose from and typically does not allow much customization.

NVR can spread their selling costs across a larger base of homes. NVR, like other homebuilders, has a direct-to-consumer advertising effort to attract buyers and does not just rely on third-party real estate agents to bring them business. The larger the building community, the more they can spend on advertising and rely less on realtors.

Homebuilders have their own commissioned sales force that typically cost less than a third-party realtor. For context, DFH 4% of revenues as commissions.

All of these elements from the capital-light approach and local build density to building product manufacturer and larger advertising push translate to NVR’s industry-leading turnover as well as high margins.

Valuation

DCF method

These are our assumptions for 2025 to 2029 projections:

Revenue growth of 3.7% per year

PAT margin 14%

PAT to FCF conversion 90%

Terminal FCF growth rate 2.5%

To solve for today’s market cap of $24.2b, the required rate of return = 11.5%

ROIC method

Another way is to work backwards for the required earnings growth rate. Given ROIC = 25%, PE = 14x, IRR = 12.5%, then expected earnings growth = 7.5%.

We don’t think these valuation assumptions are aggressive. However, we think that the stock not cheap, most likely fairly priced.

Conclusion

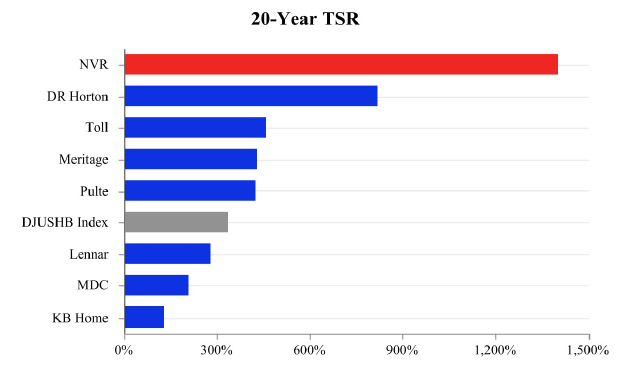

NVR has given outsized returns relative to their competitors. The strong long-term results are due to the business model which is designed to minimize risk and maximize returns on capital in a cyclical industry:

Incentives are aligned with TSR at all levels, not just executive officers. There is high retention within the management team; Chairman Saville (43 years), CEO Bredow (20 years), CFO Malzahn (30 years), we believe this is a sign for excellent corporate culture.

Weak points

Note that although the ROE numbers look high, it doesn’t mean that intrinsic value will grow at high rates. Because the amount of cash reinvested into the business is not significant, most of the FCF is used for shares buyback.

Also, an incentive structure that depends on ROIC may result in management rejecting higher NPV projects for the sake of boosting ROIC via buybacks.