NVR: NVR Inc (1)

Disclosure

We own shares at $3,600/share.

The Rise of NVR

Dwight Schar, the founder of NVR, grew up in rural northeast Ohio. He graduated high school in 1960 and left home at 18 to work on a relative’s farm. After marrying his high school sweetheart at the age of 20, he paid his college school fees by working the night shift at a pipe-fitting factory. After graduation he briefly taught science and business in junior high school and sold houses on the weekend.

He quit after one semester and joined Ryan Homes as a land buyer. Schar headed land acquisition and development efforts in Ohio, Kentucky, and Indiana. In 1973 Ryan Homes expanded into Washington D.C. and Schar followed it there.

Schar served as regional manager for Baltimore to Richmond for four years and watched the suburbs expand exponentially. His insight was that the region’s highly educated and well-paid population would demand more expensive housing than the starter homes offered.

With this insight, at age 35, Schar quit Ryan Homes to build his own company. In 1977, he founded NVLand with Stephen Cumbie. They bought and developed land for local builders, including Ryan Homes, while Schar waited out his three years non-compete clause. In 1980, William Moran joined the duo to form Northern Virginia Homes and started building. Later they shortened the name to NVHomes.

Besides NVLand and NVHomes, Schar and his partners also started many subsidaries like NVCommercial, NVProperties, NVRetail, NVIndustrial… to serve every niche in the real estate industry.

NVHomes grew rapidly by targeting buyers who wanted to upgrade but could not afford a custom home. It doubled its earnings every year, reaching $14m in 1986. That same year, Schar took the company public to get capital for even faster growth, while the other NV companies remained private.

Schar divested his stake in NVLand to avoid related party transactions with NVHomes. Then NVLand was renamed “Elm Street Development” to avoid confusion with a wholly owned land development subsidiary “NVDevelopment”, this subsidary would ultimately cause NVR to fail.

Remember Ryan Homes, the company Schar left? Months after the IPO, Schar made a $360m hostile bid for his former company. For comparison, in 1985, Ryan Homes earned $22m and built 7,534 homes while NVHomes only earned $6.1m and built 763 homes. Nevertheless, Schar sold $218m of junk bonds to close the deal in 1987. NVHomes changed its name to NVRyan and shortened it to NVR in 1989.

NVR continued to grow rapidly and vertically integrated into every phase of the homebuilding and financing process. It controlled nearly 100 subsidiaries that manufactured building products and provided services related to construction, land acquisition, home finance, investment advice, and other real estate development activities. In 1988, NVR even acquired a failed thrift from the government called McLean Federal Savings & Loan Association. The bank was renamed NVR Federal Savings Bank.

A nationwide housing boom made NVR’s rapid growth possible. Mortgage rates declined rapidly from their 1981 peak. The 30-year fixed rate peaked at 18% in November 1981 and bottomed at 5.9% in September 1986. Deregulation in 1980s allowed thrifts to offer Adjustable Rate Mortgages (ARMs), further increasing affordability.

President Reagan’s tax cuts further accelerated the booming market: depreciation charges were increased on real estate and long term capital gains tax were lowered. This set off a real estate investing spree. The Baby Boomer generation, born between 1946 and 1964, reached their prime home-buying years in the 1980s. All of these factors combined with a strong economy created a surge in demand for housing.

The Fall of NVR

Ten years after starting NVHomes, Schar had become one of the biggest homebuilders in the country.

NVR’s strategy was to borrow money to buy huge plots of land. Land prices were skyrocketing throughout the 1980s, times were easy and credit was flowing. Why not buy the land before it appreciates in value? NVR would eventually build a house and capture the gain for itself. Many homebuilders did the same.

This strategy worked beautifully during the bull market but faltered when interest rates rose. Inflation measured by the CPI rose to 4.4% in 1987 and stayed there until 1989. The Fed responded by tightening monetary policy and pushed borrowing costs into the double digits. Demand for housing fell fast.

Simultaneously, the Tax Reform Act of 1986 phased out the benefits of investing in real estate through limited partnerships.

Although NVR earned $30m in 1989, the company was in distress. It was carrying loans for land it no longer needed. Land development inventory increased from $400m in 1988 to $600m in 1990. Revenues fell from $1,115m to $900m. NVR wrote down the value of its land and reported a $260m loss in 1990.

In August 1990 Iraq invaded Kuwait. Oil prices per barrel went from $17 in July to $40 in October. The oil shock hurt consumers’ confidence and pushed the US into a recession. The housing market dried up.

NVR responded by restructuring. It’s here that the company’s modern form began to take shape.

NVR retreated to its core mid-Atlantic markets and simplified its homebuilding product offering. They ditched their speculative land business and pared back ancillary services. Besides the homebuilding operation, NVR kept only its mortgage origination business, title insurance brokerage, and bank.

The restructuring narrowed NVR’s losses, but it was too little too late. Volumes fell 27% in 1991 and prices another 5.5%. Net income remained negative.

Bankrupt by 1992

On April 6, 1992 NVR filed for Chapter 11 bankruptcy. To make matters worse, Anthony Satariano (CFO of NVR’s finance business) embezzled $763,000 and fled to Malta.

A reorganization swapped $205m of debt for 90.6% of NVR’s equity, then in September 1993, NVR emerged from bankruptcy.

NVR rebirth

Since the bankruptcy, NVR has been run as conservatively as possible. While NVR won’t be the best builder to own during an upcycle, it’s unquestionably the best to own in the inevitable downcycles.

NVR got out of the land ownership business completely. It buys options on its land from developers and waits to exercise those options until a home is sold.

This approach has trade offs, which is why none of the competitors fully adopt it. Lennar and D.R. Horton have moved in this direction, but still own 25% of their land.

NVR sacrifices margins for a higher return on equity. When builders buy and develop their own land, they also capture that margin. But that ties up a lot of capital. Land tends to appreciate slowly, so owning it unleveraged produces a poor return on equity. Leverage makes the returns more appealing, but carries significant risk.

Owning land is usually a good bet… until a downturn comes combined with leverage, and it’s catastrophic. NVR went bankrupt because it became illiquid, not insolvent. It was the classic “good business, bad balance sheet” scenario. Its homebuilding and finance operations actually made some money in 1991 but not enough to pay the interest on its loans. That’s why NVR has become fanatical about reducing risk by reducing capital employed, even at the expense of margins.

NVR may grow slower in a booming market, but the company is very likely to survive a downturn. NVR was the only publicly traded homebuilder that remained profitable through the GFC housing crash, which demonstrates how far it has come since its bankruptcy.

US Housing Demand and Supply

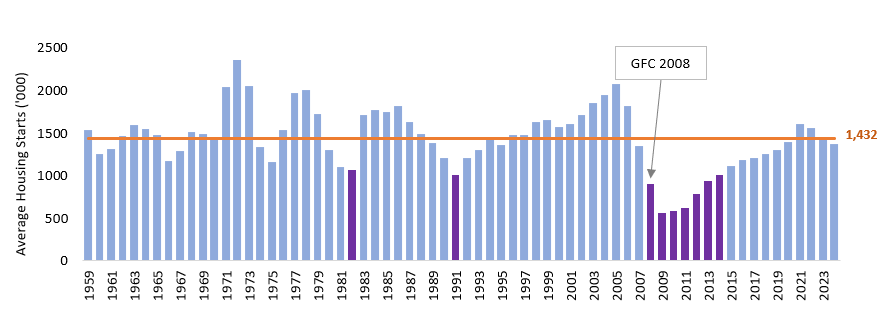

We must state the obvious: housing is cyclical. Today we are at the point where undersupply has led to higher prices, incentivizing home builders to soak up the demand.

Before the GFC, there were only two years of housing starts that averaged 1 million units. After the GFC there were six such years (see purple bars). We show the average of all years as the orange line at 1.4m units:

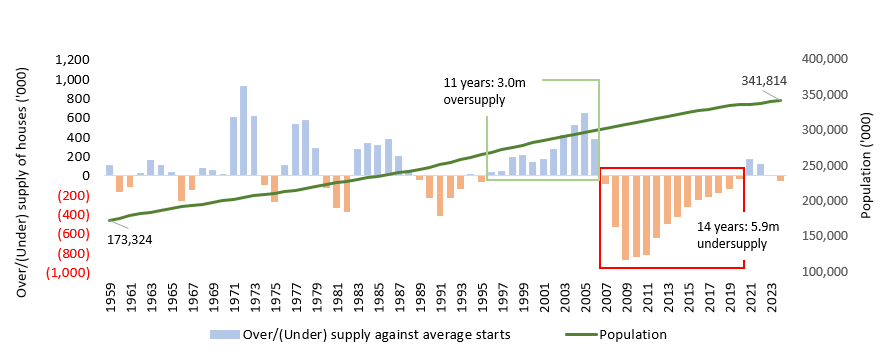

The housing cycle is even more apparent when we chart the population growth and over/undersupply of houses against the average of 1.4m units:

So the important question: Did the 14 years of undersupply more than offset prior 11 years of oversupply? Clearly not.

If we assume that 1.4m houses is the equilibrium number that matches supply with demand, the net effect from 1996 to 2020 is an undersupply of 2.9m houses. Furthermore, the equilibrium number is definitely not 1.4m houses because this is just the simple average since 1959. Obviously the population has nearly doubled and average household size decreased from 3.3 (1960) to 2.5 (2023). More people with fewer people per house both point to greater demand for housing.

This analysis is not precise, we cannot know the exact numbers for what the housing starts will look like in the future, but directionally the next decade is likely to be better for home builders.

If this is true, the average housing starts will be higher than 1.4m and in the last 3 years the average was 1.5m. This increment is not enough to cover up the 2.9m undersupply and to cater for a higher equilibrium.

Segment Breakdown

The business can be broken down into 3 parts:

Main segment is homebuilding. Ryan Homes targets first-time and upgrading buyers. NVHomes and Heartland Homes both target luxury buyers, but only operate in 4 metros (Washington, Baltimore, Philadelphia, and Pittsburgh).

Mortgage banking subsidiary called NVRM which sells title insurance and originates mortgages to be sold in the secondary market. NVRM only serves NVR customers and has contributed on average 2% of revenues and 9% of operating profits. As of 2023, 98% are fixed rate mortgages.

NVR occasionally enters into JV agreements to develop land/lots, but these investments and the subsequent income have always been very small.

They operate in 36 metros in 15 states, the largest presence in Washington, Baltimore and Richmond.

Market Share

NVR’s market share by revenue is 4th largest in the US but it’s only 9% compared to the 2 largest builders: DHI and LEN each with 32%.

The growth strategy over the last 20 years has been focused on achieving leading share in existing and adjacent markets. In 2001, they operated in 18 metros and 11 states. Today, they expanded into 36 metros and 15 states. They entered 3 states (Florida, Indiana, and Illinois) and 9 metros during the GFC, but have otherwise rarely expanded their geographic footprint outside of recessions.

Most of the new metros they entered were in states that they already had a presence, and in most cases these metros were near existing ones where they could likely leverage existing relationships and infrastructure.

This becomes important to understand when we describe NVR’s competitive advantage in terms of scale economies, since it is mostly relevant at a regional and not national level.

This approach of having a dominant presence in a few metros likely leads to better operating margins and higher ROIC. We think this is an important pillar to the strategy that’s unlikely to change and has implications for organic growth.

Competitive Advantage #1: Efficiencies in Building

NVR acquires contingent lots to maximize efficiencies building them. Sub-contractors can wire or plumb all of the houses on a block in a day, they accept lower margins for this, but make it up in volume. The savings accrue to NVR, which flows down to customers keeping its housing affordable. NVR has some of the lowest average selling prices among big builders despite focusing on the relatively expensive mid-Atlantic states.

NVR is also a leader in a construction technique known as panelization. NVR has 8 centralized production facilities which build large sections like floors, wall panels, roof, and stairs. A crane can assemble all of the panels into a house in about 6 hours. Panelization is safer, uses less labour and materials, and isn’t subject to weather delays. All the big builders do it to varying degrees and its efficiency gives them a huge advantage over smaller builders.

Panelization is only efficient at scale, which is why NVR prefers to concentrate on a few key geographies. The need for centralized manufacturing facilities operating at scale limits growth to adjacent areas.

Competitive Advantage #2: Economies of Scale

Builders FirstSource, a manufacturer of engineered wood products, counts all of the big builders except NVR among its biggest clients.

Why so?

Because NVR offers less customization than competitors to reap economies of scale. Customers can pick from a few packages of layouts and themes but cannot mix and match.

Most homebuilders love customization because upgrades carry large incremental margins, but this causes lower inventory turnover. NVR turns over inventory faster than competitors (NVR: 3.6x; DHI, LEN: 1.2x).

NVR’s manufacturing facilities also serve as distribution centers. They can buy building materials in bulk directly from a manufacturer and have them delivered to their centralized facility, then as homes are built, NVR sends materials out one at a time. Most builders, rely on their sub-contractors to procure materials, this means the cost of building goes up as sub-contractors will take a margin too.

Competitive Advantage #3: Conservatism + Asset Light

After emerging from bankruptcy in 1993, NVR has not carried material net debt. NVR also procures nearly 100% of their backlog via finished lot option contracts as opposed to owning land/lots on their balance sheet.

And, since 1993, they’ve deployed less than 1% of operating cashflows on M&A.

Because NVR takes the asset-light strategy to the extreme, they produce average ROIC of 30% compared to DHI 15%, while also having significantly less risk of permanent capital impairment.

The main contributor for lower working capital is the control land-lot backlog via option contracts versus outright ownership. For example: If a land-lot costs $100k and a builder owns 100% with 5 years of backlog, they will need to deploy $500k to secure that backlog for every home that they sell per year. However, if a builder controls their land-lot via option contracts costing 10% of the price, then that builder would only need to deploy $50k (ignoring some offsetting COGS impact).

A second point we can make is that NVR doesn’t build homes until a customer commits, which requires that a customer secures financing and places a non-refundable deposit equivalent to ~3% of the purchase price. NVR is rarely stuck with finished homes without a buyer.

Risk #1: Business Model Limits Organic Growth

This ties back to the reason why NVR chooses to expand slowly. The same efficient business model that produces high ROIC and inventory turnovers is also the same reason why NVR has limited organic growth.

If we assume that NVR is reaching full penetration in their major markets (New York & Washington), then the outlook for organic growth is much worse today than in 2005 if NVR isn’t willing to target new markets. Even then, most metros across the country are more concentrated today than ever before, and we suspect NVR will struggle to steal share from local incumbents.

Risk #2: Competitors Using Land-lot Options

A natural follow up question is whether this strategy is sustainable? Is there something that could force NVR to own more of their land-lot backlog, drive inventory turnover lower, or lead to inflation in option contract premiums?

We don’t think so. NVR often has 15%+ market share in a given metro, and they are frequently the largest customer to any one developer. In our view, this balance of power would make it difficult for developers to change the status quo. That’s especially true if other large competitors like DHI are also leaning more on the option strategy, leaving fewer alternatives for developers.

We think it’s reasonable to expect that the strategy would still be viable for the foreseeable future and NVR will continue to generate exceptional ROIC.

Another negative to the lot option strategy is that it probably leads to lower growth because developers don’t like the option approach, which makes it difficult to enter new markets.

We could argue that the next time there is a housing downturn NVR’s strategy could once again lead to share gains, but DHI and LEN balance sheets are in a much better shape today than before the GFC, and most metros are considerably more concentrated today.

Ultimately, we think NVR is making a trade-off between ROIC and reinvestment rates. That trade-off might make NVR’s business more resilient and profitable, but it might not be optimal.

Risk #3: Can Competitors Copy?

Yes, theoretically speaking competitors can adopt NVR’s model but nobody will want to do it.

Because a homebuilder does not automatically have NVR’s efficiency by copying parts of their strategy. They must copy the entire playbook for it to work: no outright land ownership, no speculative building, low choices for house customization, slow expansion, setting up distribution centers… the list goes on.

Existing competitors already have deep rooted structures that cannot be overturned, no management will risk to attempt such a change.

It is possible for new entrants to imitate NVR, but we don’t think it will disrupt the company in any major way. Because entry into the highly competitive metros is not easy, existing homebuilders already have deep relationships with developers, we don’t see any sudden innovation that can disrupt NVR’s strategy.

Incentives & Compensation

Management receives a relatively small (bottom 25% of industry) cash salary. An annual cash bonus is limited to 100% of base salary and 80% contingent on pre-tax profit and 20% new orders, net of cancellations.

The juicy compensation is in stock option grants made every 4 years. The next issuance will be 2026. The options strike price is at the stock’s closing price on the day of issuance and vest 25% in years 3, 4, 5, and 6.

50% of the options vest based on continued employment and 50% based on three-year average ROE. This ROE must be in the top three of its peer group for a 100% payout.

NVR uses options, as opposed to restricted stock, to tie compensation to total shareholder return. If management hits the ROE target and their options vest but the stock has not appreciated since the grant date, those options will be worthless. If the options vest and the stock has appreciated significantly then the options will be worth a lot. As a result, insiders own 11.7% of the company worth ~$2.7b.

One disagreement we have on the incentive structure is that it emphasizes ROIC over NPV (net present value). We know that NVR’s ROIC is the highest in their peer group, and often by a huge margin. The executive team is clearly incentivized to keep it that way. As such, we think they would reject opportunities to deploy incremental capital at returns lower than their current return on capital but still much higher than their cost of capital.

Capital Allocation

The benefits of a low reinvestment rate and being asset light with very low levels of CAPEX results in huge share repurchases.

NVR’s repurchase program began in 1996 when it had 12.89m shares outstanding, now in Q1 2024 it has 3.38m, retiring 74% of shares at a 4.6% annual rate!

Comparing the FCF yields to the 10-year, we agree that NVR made good use of share repurchases. The weighted average price over 20 years is ~$1,600 per share, obviously very accretive compared to current price of $7,200.

Conclusion

We will be happy holding on to our positions and we don’t think the current market cap of $23.5b is cheap enough. We will write a more detailed valuation if there is an opportunity.