MKL: Markel (7)

Q3 2025 Update

We have wrote many articles on MKL, readers can search the blog for prior analysis.

In Q3 2025, management has greatly improved on the details of reporting. This came as a promise from Simon Wilson as the new head of Markel Insurance, who previously was President of the International insurance segment.

Because of this restructuring we can now break the business down into more granular pieces and try to make sense of the valuation. We think MKL at $24.9b market cap is still trading below intrinsic value.

Insurance

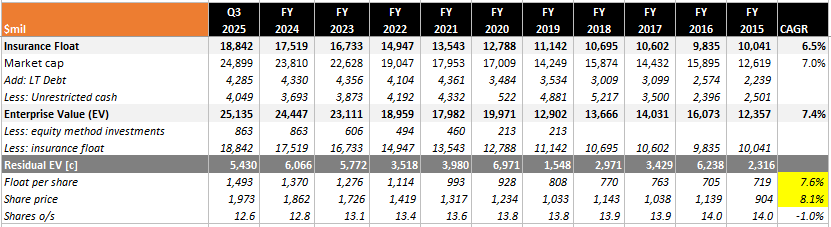

On the insurance segment, management now tells us what is the value of insurance float. We had previously calculated from the balance sheet and the historical numbers are very close to management’s disclosure.

Below we show the float, enterprise value and share price history:

What’s interesting is the long run CAGR of float per share and the share price (yellow cells). You can see that both track each other quite closely, with the share price growing slightly faster.

Does the market think that MKL growth is tethered to it’s float only?

This seems strange to us because MKL has a separate non-insurance segment called Ventures. It grew quite significantly since 2015 and operating margins have been improving in recent years, with return on capital of 12% in 2024. Unless the market thinks that growing Ventures is actually value destructive, we don’t think MKL share price should grow in line with insurance float only.

Furthermore, the underwriting track record is very good averaging 95% combined ratio since 2015, with 1 year of underwriting loss in 2017:

If the insurance operations don’t shrink in size and maintains profitable underwriting, it means that future policyholders’ premiums are paying for existing claims. The float can be thought of as permanent capital (instead of a liability) and must be worth more than face value.

Let’s be conservative and suppose that float is worth only its face value. Then we can calculate the residual enterprise value (EV) by subtracting equity method investments and float from total EV.

As at Q3 2025, we get residual EV of $5,430m. This is the amount that largely represents what we will pay for Ventures segment.

Let’s see if that’s a reasonable price to pay…

Ventures

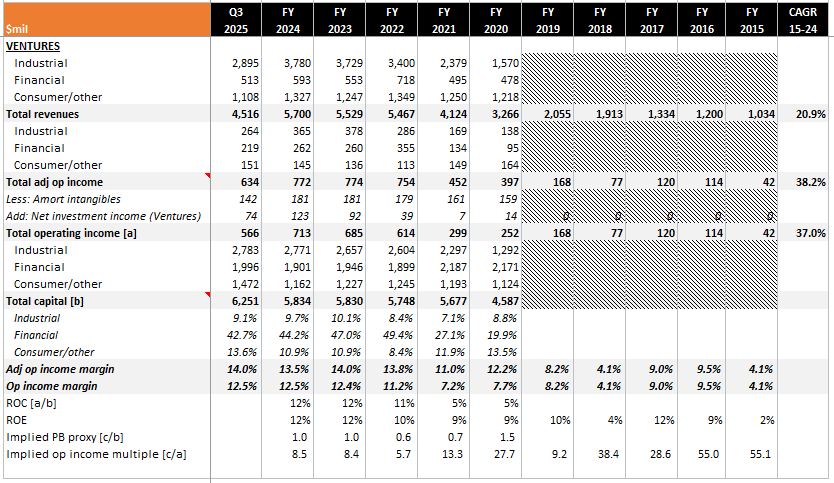

Management has done a great job at giving a lot more details moving forward. They split Ventures into Industrial, Financial and Consumer/other segments:

Overall, Ventures is producing at least 10% ROE. We get an implied PB of 0.8x with a capital employed of $6,251m against paying residual EV of $5,430m.

Suppose that our hurdle rate (or IRR) is 10%, then if Ventures can produce 10% ROE, the fair valuation should be 1x book value. Therefore, we’re getting Ventures for a good price.

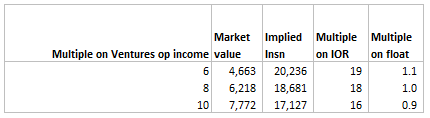

Another way to think about this is to see the sensitivity on the multiples we can pay on operating income:

For a collection of businesses that produce ~10% operating margins, we think it’s reasonable to pay 8x operating income. If we annualize operating income to $777m, at 8x multiple the market value is $6.2b, implying the remainder insurance segment is worth $18.7b, which comes back to the same value as their float!

Again, this contradicts with the idea that MKL insurance float cannot be just worth face value because they are growing the business profitably. Unless there are good reasons why their insurance will make losses, the conclusion has to be that the shares are below fair value.

Advantageous Sources of Funding

As at Q3 2025, MKL stock portfolio is valued at $12.8b, this is less than equity capital of $13.2b (insurance segment only, not total company). This tells us that the stock portfolio is not funded by liabilities, so where did the float go to?

The float ($18.8b) went into fixed income and Treasuries ($19.3b), which also implies management sees no good investments that they like in the stock market currently. This situation is not bad news, it repeats every now and then if you study disciplined capital allocators; Berkshire is currently in the same situation, and also back in the early 1970s and late 1990s, both of which were periods marked by high stock market valuations.

Interest rates are expected to fall, the current yield on MKL fixed maturities is 3.5% and short-term investments is 3.8%. Their stocks portfolio returned only 8.4% so far this year, underperforming the S&P500, however the 20-year return is 10.5% which is slightly better than the index.

MKL has access to two low-cost, non-perilous sources of leverage that allows it to safely own far more assets than their equity capital alone would permit: deferred taxes and insurance float.

As at Q3 2025, MKL had unrealized gains of $8.8b on their stocks portfolio, which means they have ~$2.2b of deferred tax liabilities. Although MKL eventually has to pay taxes on these gains, but as long-term owners of stocks this deferred taxes can be thought of as an interest-free loan from the government; effectively MKL is putting off tax payments today to compound wealth. This is similar to how float is cost-free policyholders’ money that can be invested and not repaid (unless the company winds down).

Of course, neither of them are true equity, they are real liabilities. But they are liabilities without covenants or due dates attached. In effect giving MKL the benefit of leverage to have more assets, but yet doesn’t saddle the company like how debt does.

We have no doubt that MKL will have optionality to capture value in the long run when the stock market presents better risk-adjusted returns.

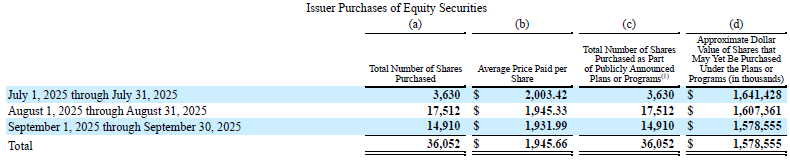

MKL continues to repurchase shares which we believe it’s a sensible way to allocate capital now:

We have an existing large allocation of 22% to MKL and will continue holding the position.

Other Notes

This is how MKL splits wholly owned subsidiaries in Ventures: