MKL: Markel (6)

Update for FY2024

Insurance

Net earned premiums (NEP) of $7.4b grew only +2% YOY but underwriting profitability recorded significant improvements over last year. The loss ratio improved from 63% to 58.3%, while expense ratio worsened from 34.8% to 36%, overall combined ratio improved from 97.8% to 94.3%.

This improvement was due to MKL international insurance businesses, while the US professional liability lines experienced higher loss ratios.

There was also a favorable prior year development (PYD) release of $451m compared to release of $105m in 2023. This release was primarily attributable to favorable development on the US general liability products in 2024 compared to significant adverse development in 2023.

Expense ratio increased due to cost inflation outpacing premium growth, MKL also mentioned about technology investments across their global operations which are expected to deliver operational efficiencies in the future; we will have to track this progress.

Reinsurance (RI) continued to make underwriting losses of -$5.4m, the combined ratio was 100.5% in 2024. RI earned premiums were flat at $1b. Significant variability in premium volumes can be expected in RI due to significant contracts size spanning across multi-years.

MKL discontinued writing public entity product lines (insurance for the unique risks faced by governmental entities and public organizations) in Q4 2024 due to increased frequency of large claims from recent accident years. Although management have discontinued some of these businesses in 2020, there were still adverse trends emerging from the remaining policies. Due to the inability to meet their profitability targets, this product was discontinued.

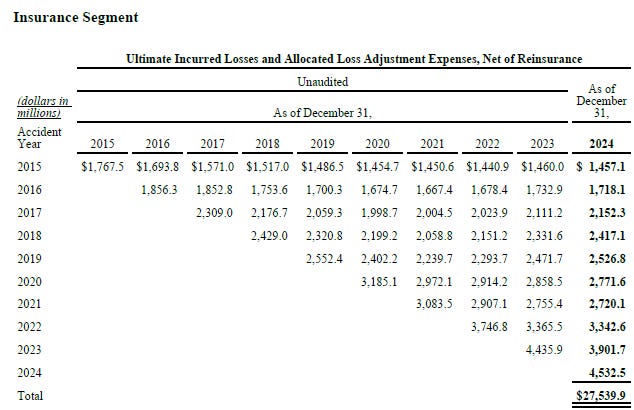

Reserving

Below is the loss development triangle, every Accident Year’s initial loss reserve developed to be adequate in 2024. This is consistent with MKL’s conservative aim to have reserves be more adequate than deficient. As at 2024, cumulative favorable PYD is $2,357m (8.5% of total insurance reserves):

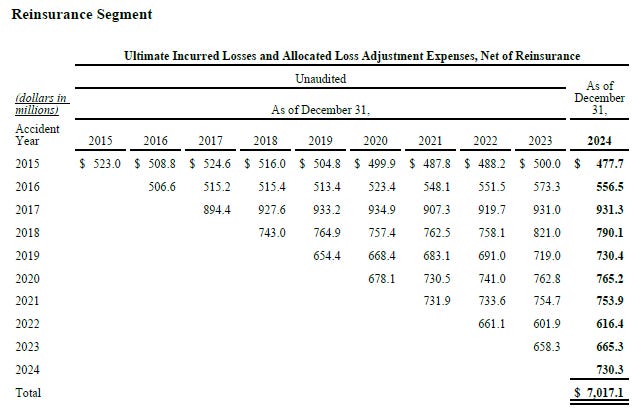

However, the RI segment doesn’t show adequate reserving, as at 2024, the cumulative deficiency is $236m (3.3% of total RI reserves):

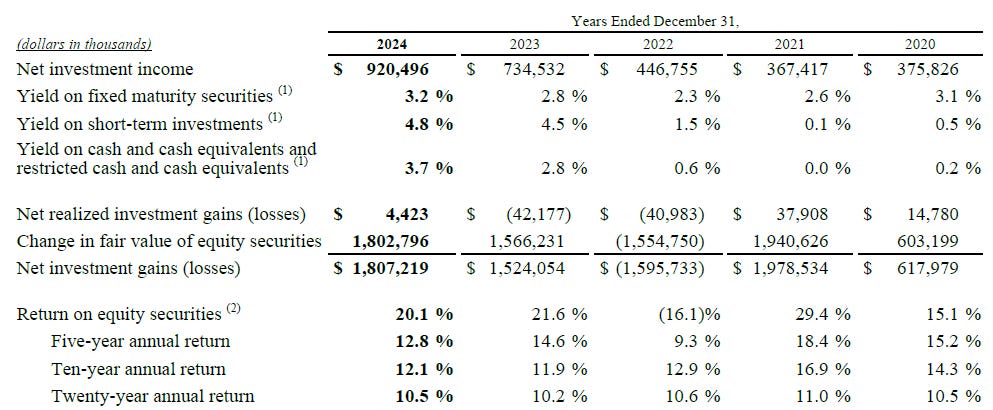

Investments

MKL provides a 5-year summary:

Improved yields across short term assets continue to provide higher investment income as MKL invests the insurance float mostly in 60% fixed income securities ($18.2b) and the remaining 40% in equities ($11.8b).

The equity portfolio has an impressive 20-year CAGR of 10.5%, remember that this is funded by negative cost of float. Effectively, policyholders’ premiums self-fund their liabilities because underwriting is profitable on average. There is also the benefit of deferred tax liabilities where MKL does not take profits just to report higher earnings; this long-term approach compounds over long periods of time.

For context, the cost basis of the public equities portfolio is $3.9b while the market value is $11.8b, that’s a huge margin of safety in the remote situation when MKL has to liquidate equities to meet insurance claims.

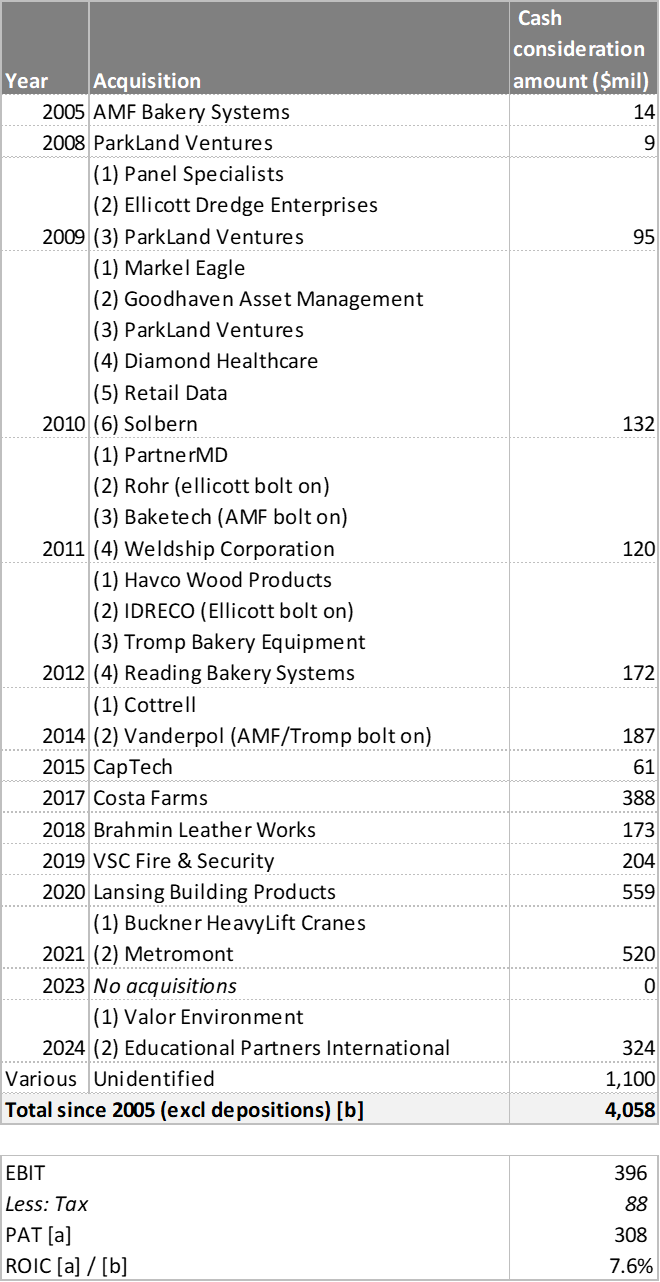

Ventures

There were 2 acquisitions in 2024:

Total cash paid $156m for 98% of Valor Environmental, an environmental services company providing erosion control and related services to commercial develoment sites and homebuilders in the US.

Total cash paid $168m for 68% of Educational Partners International (EPI), a company that sponsors international teachers for placements in US schools. This is accounted under equity method, only to be consolidated in Q1 2025 after receiving regulatory approval in Jan 2025.

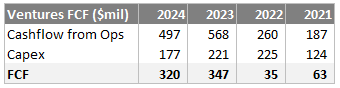

Revenues of $5.1b grew slightly by +3% YOY due to consumer building products, there was organic growth from higher prices and inorganic growth from an acquisition. However, operating income was flat at $520m due to lower margins of transport-related and construction services businesses. Below is the historical free cashflow (FCF) disclosed since 2021:

Ventures segment has been investing in CAPEX at a higher rate than depreciation:

These are the identifiable records of acquisitions since 2005:

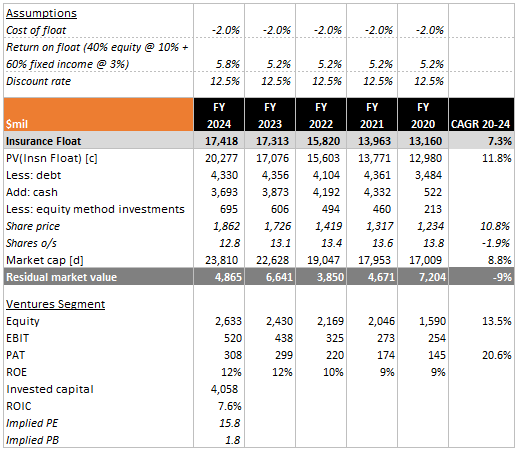

Valuation

There are some amendments we made to this model:

Terminal returns on float used to be 2.5%. We think this under-estimated the earning power of float because the long run track record is very consistent, so we assume current returns will persist.

Less out equity method investments to get implied Ventures market value since the entities accounted under equity method are not attributable to Ventures. The most significant entity is Hagerty, an automotive enthusiast brand offering membership products and specialty insurance. MKL owns 23% of Hagerty, as at 2024, the fair value was $754m and carrying value was $265m.

We estimate float and using those assumptions to get PV(float). Then we find the implied market value of Ventures and derive the implied FCF yield. Given that Ventures produced $320m FCF, the yield is 7%, implying that MKL is likely fairly valued currently at $23.8b market cap.

For context, Ventures reported $308m PAT which implies PE multiple of 16x.

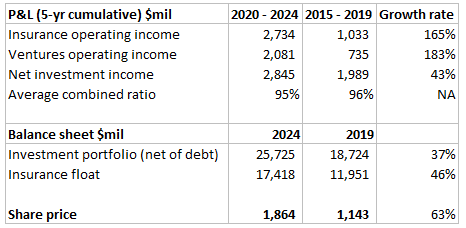

Below is the comparative stats between 5-year periods:

Since the stock is no longer cheap, we will continue to hold our position.

Activist Hedge Fund Jana Partners

In Dec 2024, Jana Partners bought 108,926 shares for a cost basis of $188m and call options on 69,000 shares at a cost of $119m. This is a 1.3% stake in MKL, and they are calling for management to unlock value for shareholders by breaking up MKL business units.

MKL reached out to shareholders and Jana Partners to get feedback on what can be improved, and hired a consultant to do this job.

We speculate that this was the reason Tom Gayner included a section on valuation in his annual letter, this hasn’t happened before in history. In any case, we feel these expenses are a waste of resources, but it also reflects that MKL management as a group does not have majority voting to thwart such requests.

Fortunately, MKL shareholders are an unique group which buy into long term thinking. In fact, MKL conducted a study and found that among its peers only Berkshire Hathaway has lower shareholder turnover rate. We think that the common shareholder as a group will vote against Jana Partners motion at the annual meeting.