MKL: Markel (5)

The Insurance Float

The idea of insurance float and using it to value insurance companies can be found explicitly in Warren Buffett’s letter to shareholders in 2009. He wrote a logical explanation of the power of insurance float:

Insurers receive premiums upfront and pay claims later. In extreme cases, such as those arising from certain workers’ compensation accidents, payments can stretch over decades. This collect-now, pay-later model leaves us holding large sums – money we call “float” – that will eventually go to others. Meanwhile, we get to invest this float for Berkshire’s benefit. Though individual policies and claims come and go, the amount of float we hold remains remarkably stable in relation to premium volume. Consequently, as our business grows, so does our float.

If premiums exceed the total of expenses and eventual losses, we register an underwriting profit that adds to the investment income produced from the float. This combination allows us to enjoy the use of free money – and, better yet, get paid for holding it.

The theory behind float valuation is that float is the net amount of capital that an insurance company has at its disposal to invest until those premiums are either earned, or until an insured loss occurs.

If float is stable and growing over time together with volume of premiums, then the insurer will have a stable level of capital to invest. In addition, if underwriting is consistently profitable, then float is in theory free, thus providing greater freedom in how this capital could be allocated.

While Buffett did not explicitly provide a method of calculating float, by working with the idea presented, we can find the needed elements on the balance sheet. In this exercise we use MKL as an example.

Cost of Float

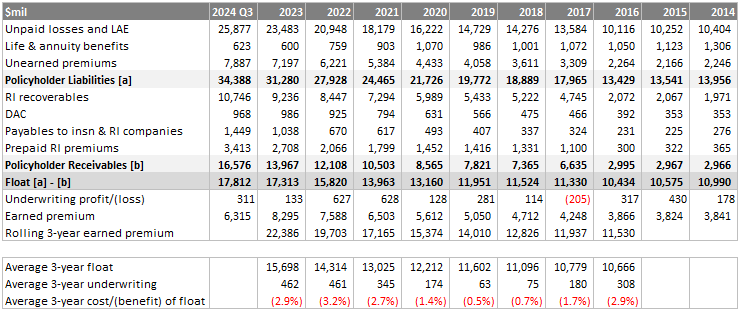

In order to better understand the nature of this float, we need to look at it’s evolution over time.

As we mentioned above, float is free if it doesn’t incur underwriting losses. In other words, if MKL can underwrite a cohort of insurance policies without making losses then the float has no cost and MKL can allocate it to the best of its abilities.

In fact, if the cost of float is lower than the cost of borrowing, then strictly speaking it is still a better source of capital than debt. That is also the reason why the insurance industry can afford to run underwriting losses on average. Of course, the ideal situation is that MKL makes underwriting profits.

To determine the true cost of float, we would need to go back to each cohort and track the underwriting results until the risk coverage for each cohort ends. This is impossible to do without inside information. However we can approximate the cost of float by looking at long term results using disclosed information.

Due to the volatile nature of underwriting insurance, we need to normalize underwriting results and float over some period of time. Our best estimate is that this period should be how long it takes for existing float to be replaced by earned premiums. From the cumulative “rolling 3-year earned premium” line, we can see that 3-years of earned premiums can more than replace the float balance. Note that we cannot estimate the amount of previously collected premiums that result in claims to get a more accurate measure of float replacement, but we think that this approximation of 3-years is sufficient.

So we average the float and underwriting results over 3 years, then find the cost of float by just dividing these numbers. The average cost of float turns out to be -2%, a negative number means that MKL is actually getting “paid” to hold onto float even if it makes nothing on investments; this is even better than free float.

Float Utilisation

After establishing that there is no cost of float to MKL, we should see how float is used. MKL holds a portfolio of fixed income (64%) and equities (36%).

Generally for typical insurance companies the float belongs to policyholders, thus they get prior economic claims on part of the investment portfolio. For common shareholders, they get claims on the excess of invested assets over float. But MKL is not an usual insurer because the market value of its equity portfolio is quite close to the amount of investments less float:

Furthermore, the cost basis of its equity portfolio is $3.5b, more than 3 times less than market value, implying that there is no risk of impairment in the event that equities need to be sold to meet insurance claims.

In reality, MKL doesn’t have to liquidate its equities to meet insurance claims because fixed income securities of $16.1b (as of Q3 2024) alone are enough to cover the float. Historically, these bonds are held to maturity in the majority of cases since underwriting results have been profitable.

So MKL doesn’t have to sell its fixed income before maturity to meet insurance claims either!

Combining these two strengths, it follows that investment income (coupons and dividends) are added to underwriting profits to result in free cashflow to the firm (FCFF). This FCFF is available for further investments. Recall that since MKL produces negative cost of float, these FCFF are effectively belonging to shareholders, treating it as free cashflow to equity (FCFE). Policyholders are entitled to their insurance coverage, for which is self-funding due to underwriting profitability.

This is where we see the power of insurance float and the economic fly-wheel that MKL operates.

The Markel Model

MKL doesn’t stop at utilising the power of a well-run insurance operation, it goes a step further by using the cashflows to acquire non-insurance companies. They group these companies under a segment called “Ventures”.

These non-insurance companies are wholly owned and operated by the same managers before MKL acquired them. It is a decentralized approach that requires no significant incremental cost.

Ventures segment generated positive free cashflow every year for the last decade. MKL funded all acquisitions with cash only, spending cumulatively $2.6b since 2005 when they bought their first subsidiary AMF Bakery Systems. In 2023, Ventures reported revenues of $5b, operating income $437m, and EBITDA $628m.

We can think of Ventures having little correlation to the insurance operations, thus diversifying MKL’s ability to generate earnings. This massively improves the flexibility on where MKL is able to invest float. Compared to typical insurance companies, they have to mostly invest in fixed income to satisfy capital adequacy requirements from regulators.

We expect that as Ventures grow in size, the weightage to equities can be increased. Given the long run performance of their equity portfolio (20-year CAGR 10.2%), it is reasonable to expect that future float will have more earning power.

In this way, there is a fly-wheel effect in the MKL model, as long as insurance premium volumes grow profitably, the float can be thought of as possessing equity-like characteristics even when it is accounted for as a liability.

Valuation

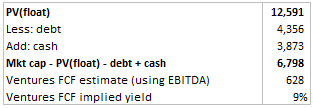

Since we have written so much, it doesn’t hurt to do a quick valuation using Q3 2024 results released this week. We calculate the present value of the insurance float and derive the implied market value of Ventures.

Assumptions:

Cost of float = -2%

Returns on float (36% equity @ 10% + 64% fixed income @ 2.5%) = 5.2%

Terminal returns on float = 2.5%

Discount rate = 12.5%

PV(float) = $12,591m.

To get implied value of Ventures: Current market cap $19,872m – debt + cash – PV(float). We get 9% implied FCF yield on Ventures segment. This is a cheap price to pay.

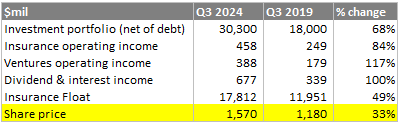

To supplement this, consider these statistics for the last 5-years:

All the important fundamental drivers of business value have grown at faster pace than share price. We think that MKL has been persistently undervalued and we actually prefer this situation because this allows management to repurchase shares at a discount, which is value accretive to shareholders.

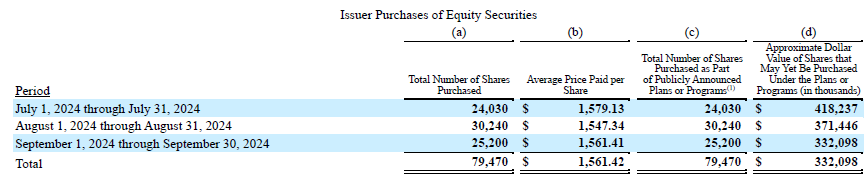

On share repurchases in Q3 2024:

MKL has heavily repurchased shares in an environment where public equities are expensive and continued to roll forward maturing bonds into higher yields. On the insurance side, the loss reserves continue to prove more redundant than deficient. We do not see risks that can cause the earning power of MKL to diminish and will be very comfortable adding to our already large position.

Why this model is difficult to replicate?

The idea of investing cost-free insurance float and buying operating businesses is not a new playbook. Berkshire Hathaway has been operating this way for decades, and the strategy is put out there for insurers to copy. However, few have succeeded due to the following factors:

It is difficult to run an insurance operation profitably. Competitors are willing to have underwriting losses as investment income helps to offset. This results in competition where prices set are not commensurate with risk. Due to this commodity-like nature, insurers that can keep expenses low have operational advantages.

Incentives must be designed for long term thinking and penalize short term gains. It is very easy to chase revenue targets and forget about profitability. Underwriting insurance requires discipline and the willingness to walk away from business when the price is not right.

Management needs to be talented at capital allocation and risk management. An inefficient use of capital destroys the compounding effect of the model, especially when underwriting margins are thin. Competition in the private equity space also creates challenges when buying operating businesses.

Trust has to be earned and maintained. Insurance is a business of promises; the discipline of prudent reserving decreases reported earnings but ensures longevity. The ability to look beyond the accounting numbers and communicate economic reality is a high order task.