MKL: Markel (2)

Update FY2023 Results

MKL share price fell -6% after Q4 2023 results were published. The bad news is mainly the disappointing 98% combined ratio. The good news against 2022 include:

Earned premiums +9%.

Operating income from Markel Ventures +35%.

Net investment income +64% due to higher yield across fixed maturity portfolio.

The 5 year CAGR in book value per share was 11% while share price grew only 6.5%. We want to remind again that book value does not include changes in fair value of acquired businesses or equity method investments, other than decreases arising from impairment. Specifically for Markel Ventures, these non-insurance operating businesses are not recorded on the balance sheet at market values.

MKL has long maintained a large fixed maturity portfolio that is designed to match the projected amount and timing of insurance liabilities. It allocates about 64% to fixed maturities and 36% equities. Compared to Berkshire which holds only about 7% fixed maturity securities.

To the extend that equities yield higher returns over the long run, MKL overall invested assets compound at less than 10% per year even though its equity portfolio generates above 10% over the long run.

However, there will come a point in time that MKL will not be constraint by this requirement when deciding the allocation between bonds and stocks. The key metric to track is whether equity capital is growing at a faster rate than insurance liabilities. This builds a margin of safety and provides flexibility in terms of how capital can be invested, either toward equities or wholly owned subsidiaries via Markel Ventures.

There is also an accounting mismatch which is interesting to know. Accounting rules require that the value of the bond portfolio be mark-to-market, hence rising interest rates causes unrealised losses. However, loss reserves are not discounted to present, except for a run-off book of United Kingdom motor business (refer to 2022 annual report: 10K pg 103, Reserving Methodology).

Economically speaking, the present value of liabilities should decrease when interest rates increase. In this sense, book value can be understated because assets decreased while the loss reserves remained unaffected.

To the extent that insurance liabilities are accurately matched by fixed maturities, MKL has a natural hedge in place when it comes to interest rate fluctuations. The declining value of fixed maturities is offset by declining value of loss reserves even though they are not marked down on the balance sheet.

Valuation

Our valuation method is as usual; find the present value of insurance float and assign the residual from market cap to Ventures segment.

We estimate insurance float as of FY2023 to be $14.8b. Define float = unpaid losses + unearned premiums – receivables – RI recoverables – deferred acquisition cost – prepaid RI premiums

Cost of float = -2% (normalized combined ratio 98%)

Returns on float = 5.3%, perpetual returns = 2.5%

Discount rate = 10%

The PV turns out to be $14.3b. Market cap is currently $18.3b, that leaves $4b for Ventures segment. Year-on-year, Ventures EBITDA grew by 24%, if we apply 24% growth to free cash flow, we get $322m. So FCF yield is 8% (or 12.5x multiple). We think this is a good price to pay when we reference it to returns on capital employed (ROCE) in 2022 (10K, pg. 50):

Capital Employed = Equity + non current liabilities – non controlling interest – redeemable non controlling interest = $2,872m

ROCE = EBITDA/Capital Employed = 506/2872 = 17.6%

Basis for returns on float 5.3%:

Equity portfolio (36% weightage): 20-year CAGR 10.6%

Bond portfolio (64% weightage): assume 2.5%

For conservatism, we did not consider the scenario that MKL will have increased flexibility deploying float into equities as time progresses.

As shareholders’ equity grow faster than insurance float, there will be incentives to reduce allocation to bonds, coupled with a strong record in equity investments, this should generate value for shareholders.

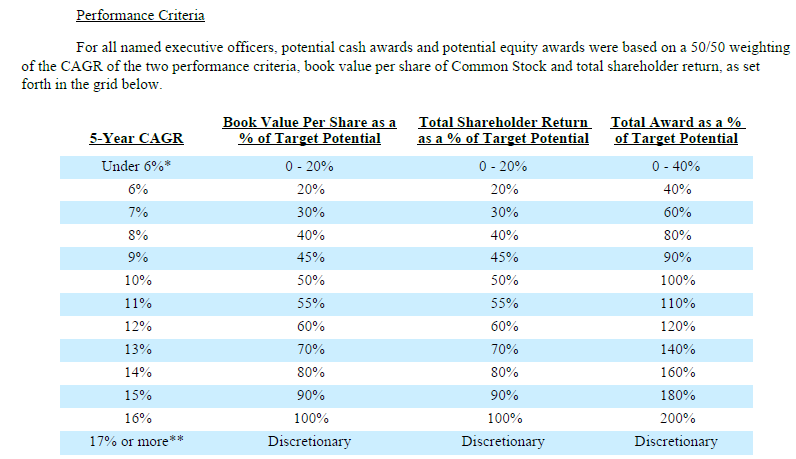

Executive Officers Compensation

Below is taken from the latest proxy for named executive officers compensation. It is made of 5-year CAGR on two simple factors:

Book value per share

Total shareholder return

Conclusion

In our valuation we remain conservative, assuming that the equity-bond proportion remains heavily skewed to bonds till perpetuity. By this calculation, the FCF yield on Ventures segment is 8%. We conclude that current share price of $1,395 is undervalued.