MC.PA: LVMH

History

LVMH Moët Hennessy Louis Vuitton SE (LVMH) was formed in 1987 through the merger of Louis Vuitton, the fashion house, and Moët Hennessy, the champagne and cognac producer. Both companies had different motivations: Moët Hennessy’s motivation was protection from competing businesses, while Louis Vuitton wanted to expand into the luxury consumer business. At that time, Moët Hennessy was triple the size of Louis Vuitton, thus Alain Chevalier (president of Moët Hennessy), became the chairman of the new holding company. Henry Racamier, who had taken the top management position at Louis Vuitton a decade prior, became vice-president.

Disagreements began to arise shortly after the merger due to Henry Racamier believing that Moët Hennessy was attempting to absorb Louis Vuitton and become the prevailing controller of the merger. Legal battles commenced between the two top managers. Racamier then introduced Bernard Arnault into the situation with the intention of consolidating controlling power.

Bernard Arnault developed a growing interest in the company and was able to secure a 45% controlling interest of LVMH with the financial support of Lazard Frères, the French investment bank, and Guinness plc, the British beverage conglomerate.

Alain Chevalier eventually stepped down as the chairman of LVMH. This led to legal battles between Arnault and Racamier. Although Racamier had proven to successfully raise LV’s sales from $20m in 1977 to $1b in 1987, he was less favoured by the group.

Three years after the merger, Bernard Arnault had stood as the prevailing owner of LVMH, effectively controlling the largest luxury empire. Under Arnault, LVMH continued the prosperous journey of growth through acquisition and organic expansion. While LVMH did face several small crises throughout the decade of the 1990s, the journey of acquisitions continued.

As of 2024, LVMH is a conglomerate with over 75 brands. Aside from the corporate activity of LVMH and the luxury brand landscape, the importance of LVMH’s diversification in geographic and products is notable, due to its strong global presence across the entirety of the luxury goods market.

Below is a timeline of major acquisitions:

1987: Louis Vuitton – Founded in France in 1854, Louis Vuitton became part of LVMH in 1987 when the conglomerate was created. Moët et Chandon and Hennessy, leading manufacturers of champagne and cognac, merged respectively with Louis Vuitton to form the luxury goods conglomerate.

1988: Givenchy – Founded in 1952 by Heubert de Givenchy is a couture and ready-to-wear brand, initially focused on women’s wear before venturing into men’s wear, cosmetics and fragrances.

1993: Berluti – Founded in 1895 by Italian Alessandro Berluti, making men’s shoes, leather goods, and clothes.

1993: Kenzo – Founded in 1970 by Japanese designed Kenzo Takada, the brand was sold from SEBP and Financière Truffaut to LVMH for $80m.

1994: Guerlain – The French perfume, cosmetics, and skincare brand, which is among the oldest in the world, was owned and managed by members of Guerlain family from its inception in 1828 to 1994, at which point it was acquired.

1996: Céline – Founded in 1945, the Paris-based brand offers leather goods, shoes and accessories. In 1987, Arnault bought into Céline’s capital, but it was only in 1996 that the brand was integrated into LVMH for $540m.

1996: Loewe – The Spanish company created in 1846, manufacturer of leather goods, was acquired in 1996.

1997: Marc Jacobs – Founded in 1984, LVMH has held a majority stake in the New York-based brand since 1997. Marc Jacobs became the creative director of women’s wear for Louis Vuitton in 1997 until 2014.

1997: Sephora – The French cosmetics chain, which was founded in 1969, was brought under the LVMH umbrella in 1997, and has since been expanded globally.

1999: Thomas Pink – Founded in 1984, Thomas Pink is a recognized specialist in high-end shirts in the UK. LVMH is understood to have paid around £30m to Thomas Pink’s owner, the Irish Mullen family, for 66% of the company.

1999: TAG Heuer – The Swiss watch-maker, which was founded in 1860, accepted a $739m bid from LVMH in 1999 in exchange for 50.1% ownership.

1999: Gucci Group – [unsuccessful] On January 6, 1999, it publicly known that LVMH had acquired a 5% stake in Gucci. Bernard Arnault was adamant that it was a passive stake and he had every intention of letting Gucci remain independent. LVMH’s increased its stake to 34.4% by January 26, 1999. In September 1999, Pinault-Printemps-Redoute (now known as Kering) agreed to pay LVMH $806m for the majority of stake in the Gucci Group. At the same time, LVMH announced plans to sell its remaining shares in Gucci.

2000: Emilio Pucci – The Italian company, which was founded in Florence in 1947, was acquired in 2000. LVMH paid an undisclosed sum for 67% ownership stake. LVMH acquired the remaining 33% from the Pucci family for an undisclosed sum in June 2021.

2000: Rossimoda – The Italian fashion company was founded in 1977. LVMH took a minority stake in the company in 2000 and at a later date acquired sole ownership.

2001: La Samaritaine – Acquired a 55% stake in iconic French department store La Samaritaine and its real estate in 2001 for €256m. It took full ownership in 2010.

2001: Fendi – The Italian company, which was founded in Rome in 1925, has been part of the LVMH Group since 2000. In July 2000, LVMH and Prada both acquired ownership stakes in Fendi. In December 2001, LVMH bought Prada’s stake, increasing its share in Fendi to 51%. LVMH further increased its ownership stake to 84% in February 2003.

2001: DKNY – [sold] Founded in 1984, LVMH acquired an 89% stake in the New York-based brand. LVMH sold the company to G-III Apparel Group in December 2016 for $650m.

2001: Hermès – [unsuccessful] In 2001, LVMH acquired an initial 4.9% stake in Hermès, and continued to accumulate shares in its Paris-based rival by buying equity derivative, with each keeping holdings below 5%. In October 2010, LVMH announced that it had acquired a cumulative 14.2% stake and in December 2011, announced that raised its stake to 22.6%, and then to 23.1% as of 2013.

Following the investigation by the French courts, they found that LVMH had secretly bought shares in Hermès. An intervention by the courts, LVMH distributed its stake in Hermès to its shareholders and institutional investors and agreed not to buy more shares in Hermès for the next 5 years. LVMH’s shares in Hermès were fully distributed such that LVMH no longer held any Hermès shares as of year-end 2015.

2009: EDUN – [sold] Founded by Ali Hewson and Bono in 2005 to promote fair trade in Africa by sourcing production throughout the continent, the founders sold 49% to LVMH in May 2009. In June 2018, LVMH divested its minority stake in the brand back to its founders.

2010: Moynat – Founded by Octavie and François Coulembier, they joined with a woman, Pauline Moynat in 1849 making luxury trunks. The company closed in 1976, fast forward to 2010, LVMH bought the company to resurrect the brand. In December 2011, Moynat reopened with a store at 348 Rue Saint-Honoré.

2011: Bulgari – Founded in 1884, the Italian jewelry brand was acquired in an all-share deal for $6b, in which the Bulgari family sold their 50.4% stake in exchange for 3% of LVMH.

2013: Loro Piana – LVMH acquired an 80% stake in the Italian luxury textile company founded in 1924 for €2b.

2013: Nicholas Kirkwood – LVMH acquired a 52% stake in the British footwear company founded in 2004. In September 2020, Kirkwood announced that it will take back full ownership of its brand.

2013: J.W. Anderson – [sold] In addition to announcing that Jonathan Anderson would take the helm of Loewe, LVMH acquired a minority stake for an undisclosed sum.

2015: Repossi – LVMH acquired a 41.7% stake in the family-run Italian jewelry brand in November 2015. It upped its stake to 69% in 2019.

2016: Rimowa – LVMH acquired an 80% stake in the German luggage company founded in 1989 for €640m.

2017: Christian Dior – Founded in 1947, this is a multi-product brand, however the subsidiary inside LVMH works just with performs, make-up and cosmetics. LVMH acquired Dior in a $13.1b deal.

2017: De Beers – [sold] The diamond retailer was sold in 2017 to De Beers Group. They bought out LVMH’s 50% share, making De Beers the sole owner of the company.

2018: Belmond – LVMH paid $3.2b for Belmond, formerly known as Orient Express Hotels, this is a luxury hotel chain operating luxury train services and river cruises.

2019: Tiffany & Co. – Founded by Charles Lewis Tiffany and John B. Young in 1837. The initial deal was an all cash transaction of $16.2b, LVMH bid for the American luxury jewellery maker 5 times. In 2020, the offer was reduced by $425m due to COVID.

2022: Pedemonte Group – Founded in 2020 as a merger of several independent production workshops known for their use of technology and traditional craftsmanship, and currently has 350 artisans and employees. The company has its own jewellery brand, Vendorafa. LVMH bought Pedemonte Group from the Equinox III SLP SIF investment fund for an undisclosed sum.

2022: Joseph Phelps – In August 2022, the Group acquired the entire share capital of Joseph Phelps, a California estate offering a collection of Napa Valley and Sonoma Coast red wines. The price paid was $587m.

2023: Château Minuty – A high-tier wine producer, founded by Matton family in 1936, LVMH purchased a majority stake for estimated €350m to 450m.

2024: L’Épée – A swiss luxury clockmaker founded in 1839 initially specialized in watch components and music boxes, then expanded into carriage clocks. LVMH adds this to their horological holdings (Zenith, Hublot, TAG Heuer).

Corporate Structure

As of year-end 2022, LVMH did a corporate ownership restructuring. Arnault realized the necessity to create a succession plan as he grows older. Prior to this alteration, the conglomerate already contained a convoluted structure, which has recently become more elaborate. Arnault created Agache SA, which will transform the previous Agache SE into a limited joint-stock partnership.

This allows a shareholder with a relatively small ownership size to retain an outsized voting right. Bernard Arnault’s five children will have equal ownership rights which relate to Agache Commandite SAS, after certain contingencies are fulfilled.

Currently, Agache SA is solely owned by Bernard Arnault. Upon a determined set of anonymous conditions mentioned in Arnault’s succession plan, Agache SA will transfer ownership of Christian Dior to Agache Commandite SAS, owned by the 5 children.

Agache Commandite SAS’s purpose is to avoid inter-familial disagreements: containing a two-year chairmanship and mandatory unanimous board approval for large strategic changes.

The 5 children cannot sell their shares in Agache Commandite SAS for 30 years without unanimous approval and no partner in the company can come from outside the five bloodlines.

Overall, the Arnault family owns 48% of the existing shares and will retain 64% voting rights.

Institutions and public shareholders own about 25% each. Three largest institution owners are Capital Group, BlackRock, and La Piegne SA, holding 3%, 2.4%, and 1.9% respectively. Centralization of ownership amongst the Arnault family will make any takeover attempts highly unlikely.

To give a summary:

Arnault’s 5 children own 100% of Dior (20% each), which in turn owns 41% of LVMH.

Arnault owns 100% of Agache SA , which in turn owns 6.2% of LVMH. Total voting rights of Arnault family is 64%.

Institution investors own ~25%.

Individual investors own ~25%.

Business Segments

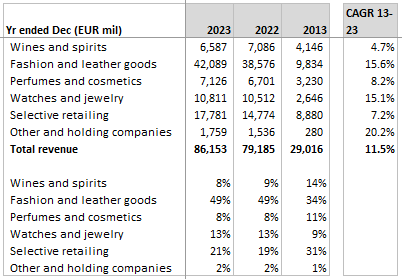

The fashion & leather goods (FLG) segment produces nearly half of total revenues and also reports the highest operating margins of 40%.

On total company level, margins are quite high and consistent with average gross margins 69% and operating margins 26% for the past 3 years.

LVMH attempts to obtain economies of scale through shared manufacturing, distribution, and marketing abilities.

Moat #1: Operating Synergies

For example, the acquisition of Sephora streamlined retail operations and distribution of the perfumes & cosmetics division. Sephora’s retail network and operational expertise reduced costs and provided an alternate distribution channel for perfumes & cosmetics owned by LVMH.

Moat #2: Marketing Synergies

Two examples:

Tiffany & Co. acquisition allowed LVMH to expand its presence in America, the second largest geographic market.

Acquisition of Dom Pérignon enabled the wines & spirits division to expand and absorb the strong prestigious branding of wines.

Arguably, majority of the acquisitions undertaken by LVMH are done for the purpose of realizing marketing synergies. LVMH growing brand of portfolios makes it easy for consumers to be aware of the conglomerate. The image and perception displayed by all LVMH brands are products of continued marketing efforts.

Moat #3: Financial Synergies

The luxury goods industry’s high operating margins and strong cash flow allow for financial synergies. The acquisition of Bvlgari in 2011 provided financial synergies as LVMH was able to increase the brands’ operating margin from 8% to 25% post-acquisition. Bvlgari was able to access capital which was necessary to expand its operations which were not previously financeable as a stand-alone firm.

LVMH’s deep financial resources represent a large expansion opportunity to many possible target firms. Brands no longer need to negotiate credit lines, instead they receive a budget allocated by the corporate leader. Consolidation within LVMH also provides access to more favourable financing rates. Hedging against currency fluctuations through the pooling of currency within the conglomerate is also possible.

Moat #4: Intellectual Property

LVMH, and other luxury fashion competitors, all operate within the higher-income section of the market. Brands which are excluded from this section of the market rely on mimicking the production, creative processes, and outputs of the industry’s leaders.

Due to the large influence LVMH plays in the creative positioning of the entire fashion market, it is crucial that the firm obtains trademarks, design patents, and copyrights to safeguard their brand’s image.

The majority of their patents relate to design. In the fashion industry, a patent implies the protection of a new manufacturing process, innovative production techniques, unique garment designs, or related design function.

LVMH recognizes that their products, especially durable luxury items such as handbags, clothing, and jewellery, are prime targets for the counterfeit markets. Competitors went as far as creating an alliance to fight counterfeits, LVMH, Cartier, and Prada are among several of the brands. The alliance formed a non-profit Aura Blockchain Consortium to utilize technology for the purpose of ensuring authenticity. Consumers can follow a product’s lifecycle, from conception to distribution, with trusted data throughout, to ensure authenticity of a product.

Moat #5: Unique Pricing Power

The luxury goods industry has undergone consolidation. More than half of the revenues generated within the industry are attributable to the top companies. These leaders have pursued acquisitions recently with Michael Kors acquiring Versace in 2018, LVMH acquiring Tiffany in 2021, and Kering buying Valentino in 2023.

Because of this consolidation trend, brands also become more uniform in their quality and image. This leads to independent pricing powers, limiting the risk of price wars.

Moat #6: Suppliers Switching Cost

We often hear about consumer switching costs as a competitive advantage relating to how sticky a product is to a consumer. On the other side, there’s supplier switching costs which are important for this industry.

All incumbent brands in the luxury sector operate with strong brand identities and factors of product differentiation. This poses a difficulty to suppliers in the process of production because their manufacturing processes must be sufficiently flexible.

Furthermore, strict codes of conduct are often imposed for the protection of the retail brand.

LVMH publicly released their “Supplier Code of Conduct” contract stipulation, which highlights various legal requirements in addition to top product quality delivery. LVMH requires suppliers to abide by sustainability, corruption, worker-rights, and audit clauses.

The luxury brands strictness with suppliers translates into a relationship where suppliers are content with maintaining their current supplier position.

Due to consolidation of leading luxury firms, a supplier will have difficulty landing a contract of comparable size. Different creative preferences of each conglomerate result in the suppliers retaining a small amount of power.

Suppliers need to fight to land prestigious contracts with luxury firms. With large financial capabilities, LVMH likely has the ability to acquire multiple touchpoints in the supply chain.

Hence, the switching costs from a supplier viewpoint are high, and their bargaining powers are low.

Risk #1: Managing Luxury Brands is Difficult

The success of LV and Dior has not been replicated everywhere across LVMH’s portfolio. Some brands like Celine and Marc Jacobs have been nowhere near as successful over the last decade, with their respective relaunch attempts experiencing mixed receptions. Ultimately, creativity and innovation are just as important as the commercial aspects of luxury brand management, and these are difficult to formulate as they depend on the genius of the creator.

Risk #2: High Expenses

Maintaining brand image is an expensive exercise, especially for luxury goods where methods of marketing often include art and exorbitant showrooms.

As a proportion of sales, marketing and selling expenses are ~35%, materials and workmanship costs are ~30%. We can think of these costs as mandatory in running luxury brands. During financially difficult times, they are unlikely to be cut. For example, during the GFC (2008), marketing expenses continued to eat up 35% of revenues.

Valuation

Similar to our Hermès article, we think that the value of LVMH lies in terminal value. This implies that we think these brands will last for a very long time.

To justify the current market cap of €313b, we run a reverse DCF with:

1. Starting free cashflows €8.1b

2. Net cash -€3.4b

3. Growth 10% for years 1 to 10, terminal growth 6%

These assumptions will return ~10% IRR.

Given that the luxury industry as a whole has growth rates in single digits, we cannot justify buying LVMH at current prices.

Furthermore, Q2 2024 results were not very pleasing with revenues declining slightly against last year.