MA: Mastercard (3)

Preface

This post addresses some of the important head/tailwinds for MA business.

Click here for a deeper dive and links to prior posts.

Geographic Mix

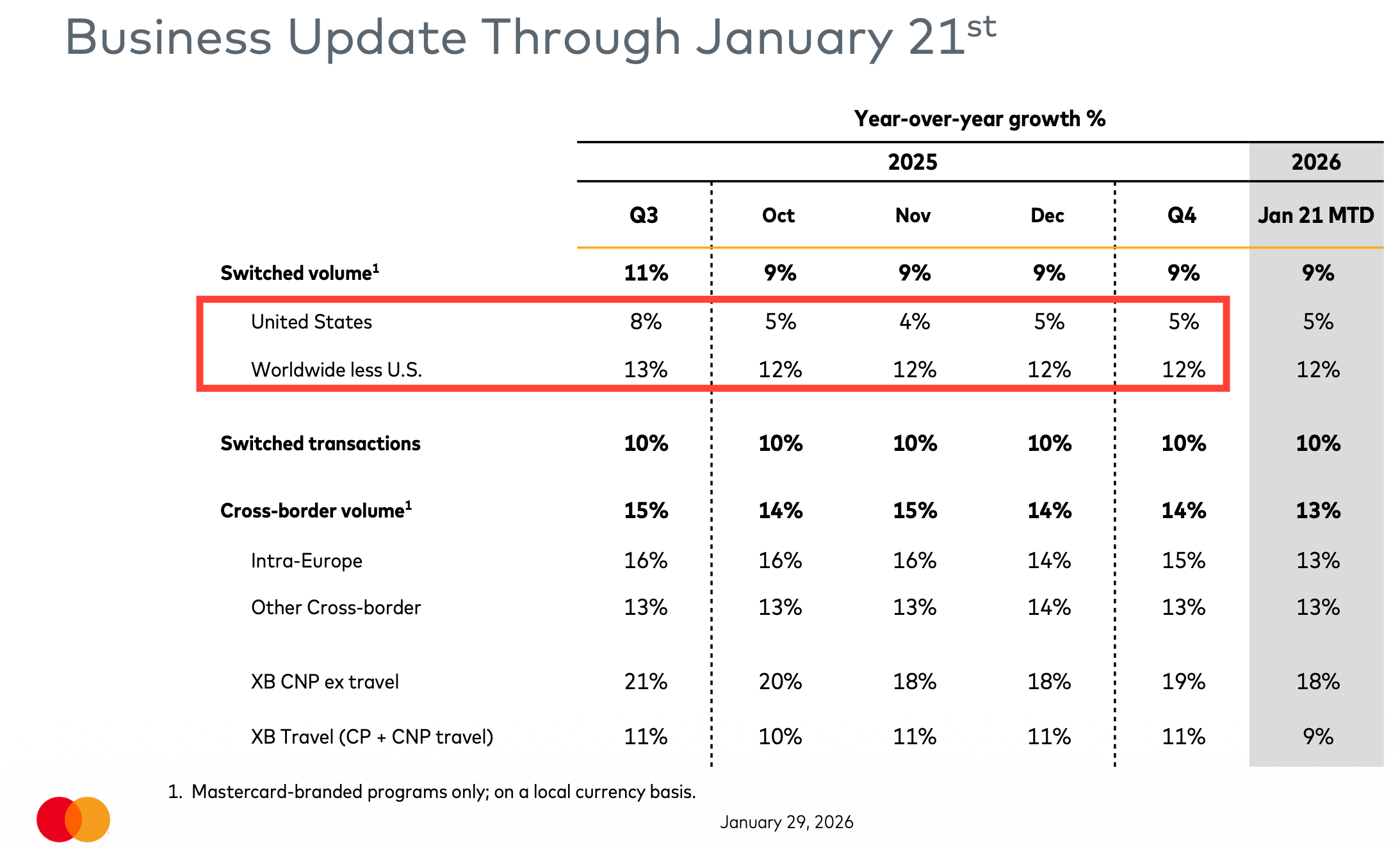

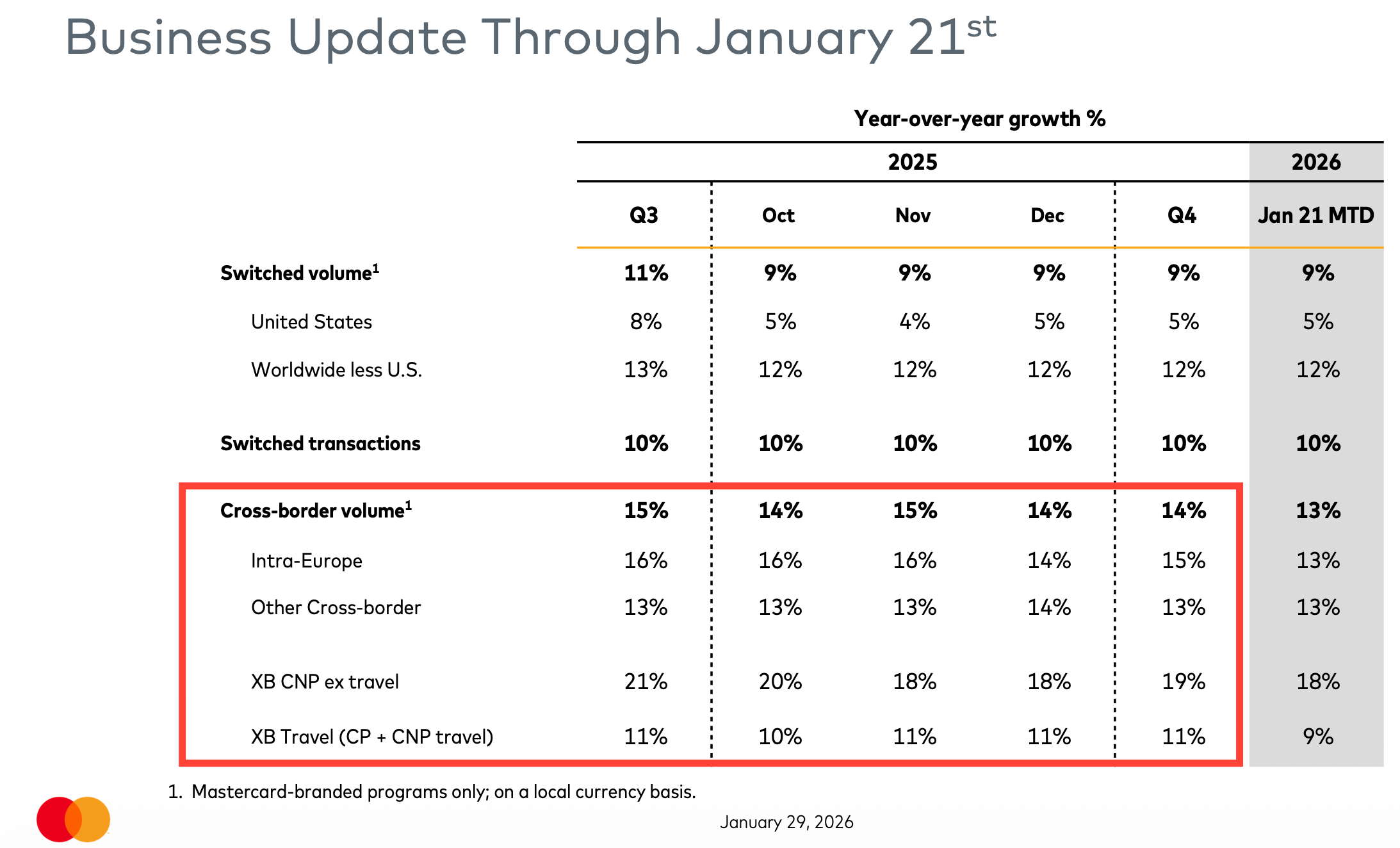

Let’s start with this report for 2025. Switched volumes represent the dollar amount of transactions that went through MA network.

Refer to the red box, there are 2 observations:

US switched volumes growth rates fell from +8% to +5%, while worldwide (ex US) held steady at +12%.

This trend was consistent in months leading up to Q4.

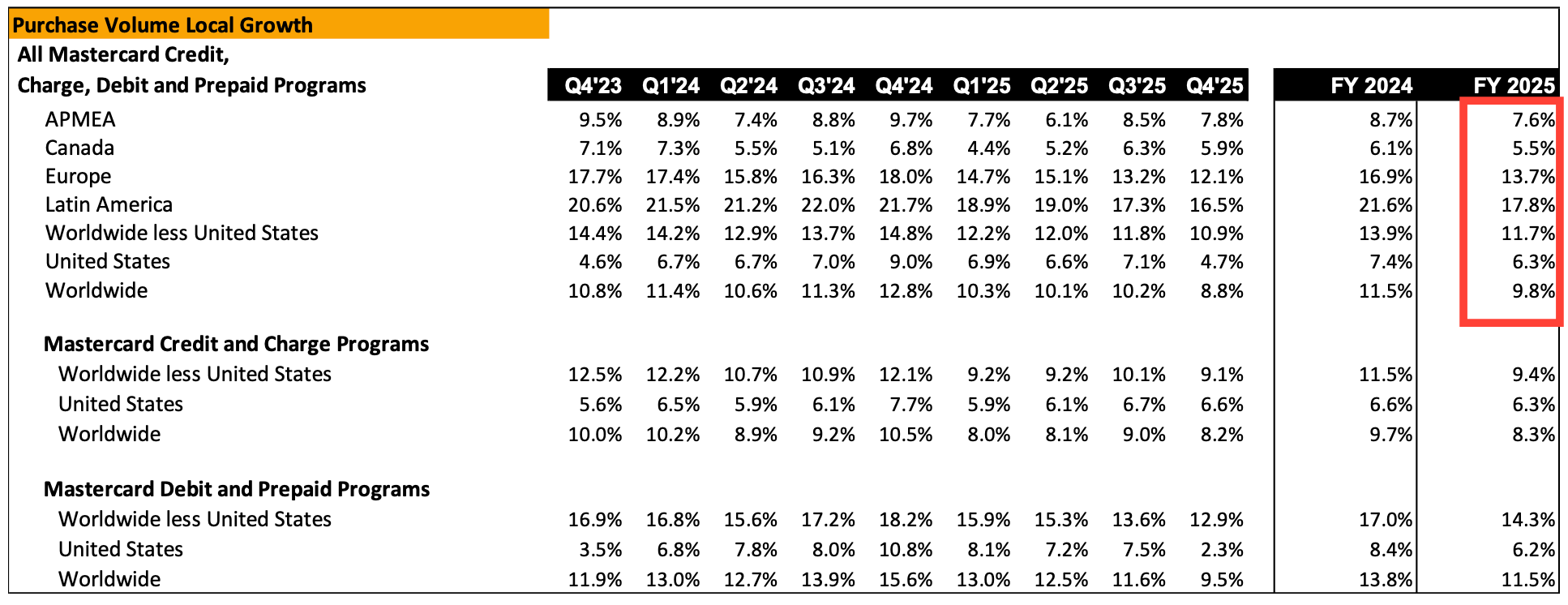

Below is that purchase volume growth by region. It tells the same trend:

International markets grew +11.7% but domestic US only +6.3%. Of which, Europe and LATAM grew +13.7% and +17.8% respectively. Both of these regions already have matured digital payments infrastructure, yet they were able to produce higher growth against the US.

Clearly, this is not a one-off thing, there are no abnormal events that could cause a temporary shift in growth profile. This is a structural change.

In Europe, the Payment Service Directive (PSD2) was created in 2018 to protect consumers and encourage competition. It introduced open banking to the EU and established strong consumer protection standards by requiring stricter security measures for online protocols. It was intended to be the core pillar to which other regulation would anchor. However, because payments evolved quickly (in part due to accelerated digitization driven by COVID), areas of opportunity for improvement and expansion of the directive have become apparent.

PSD3 builds upon these foundations by tightening anti-fraud measures, harmonizing consumer rights, and integrating electronic money services.

Europe is accelerating due to digital wallet penetration, open banking infrastructure, and cross-border e-commerce within the EU.

MA recognizes this potential and invested €250m in 3 new datacenters in France (Oct 2025).

LATAM's growth comes from real-time payment (RTP) infrastructure PIX, fintech innovation from Nubank and Mercado Pago, and the digitization of small businesses that never had formal banking relationships.

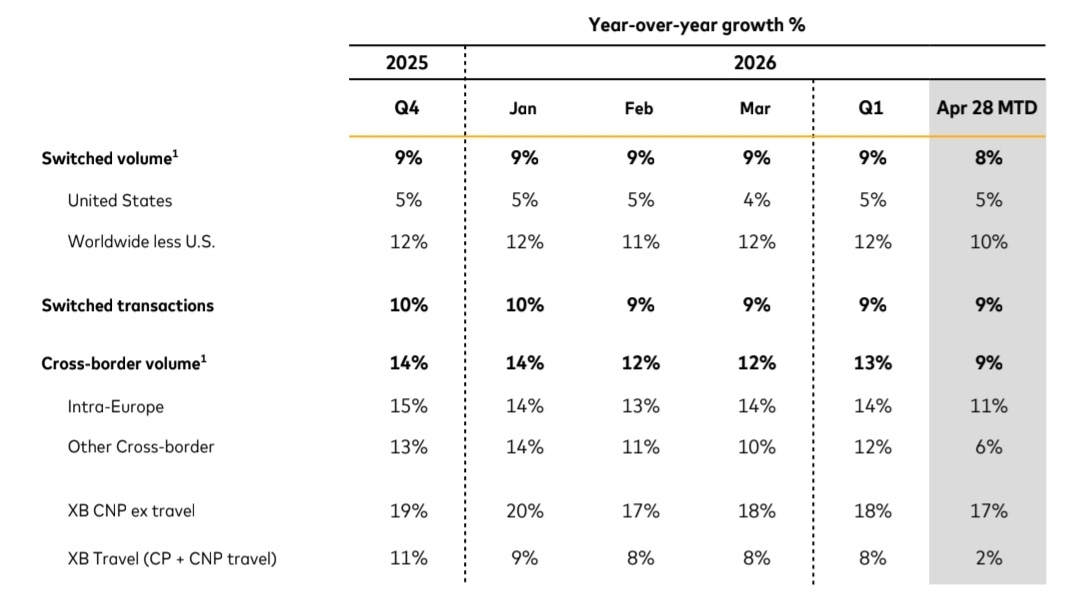

For context, here is the same Q1 2026 table showing same trends:

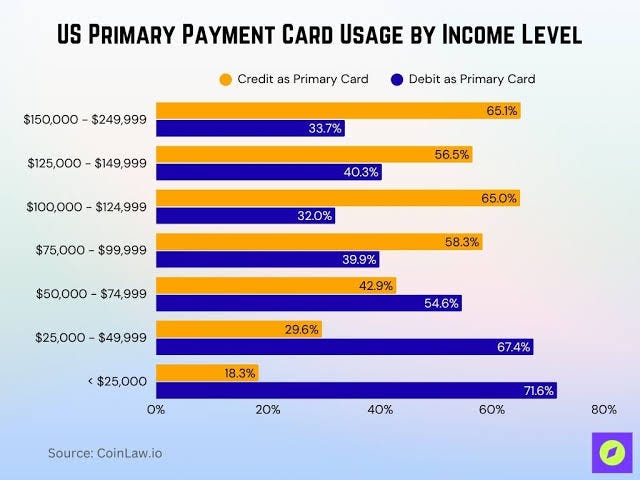

Debit/Credit Mix

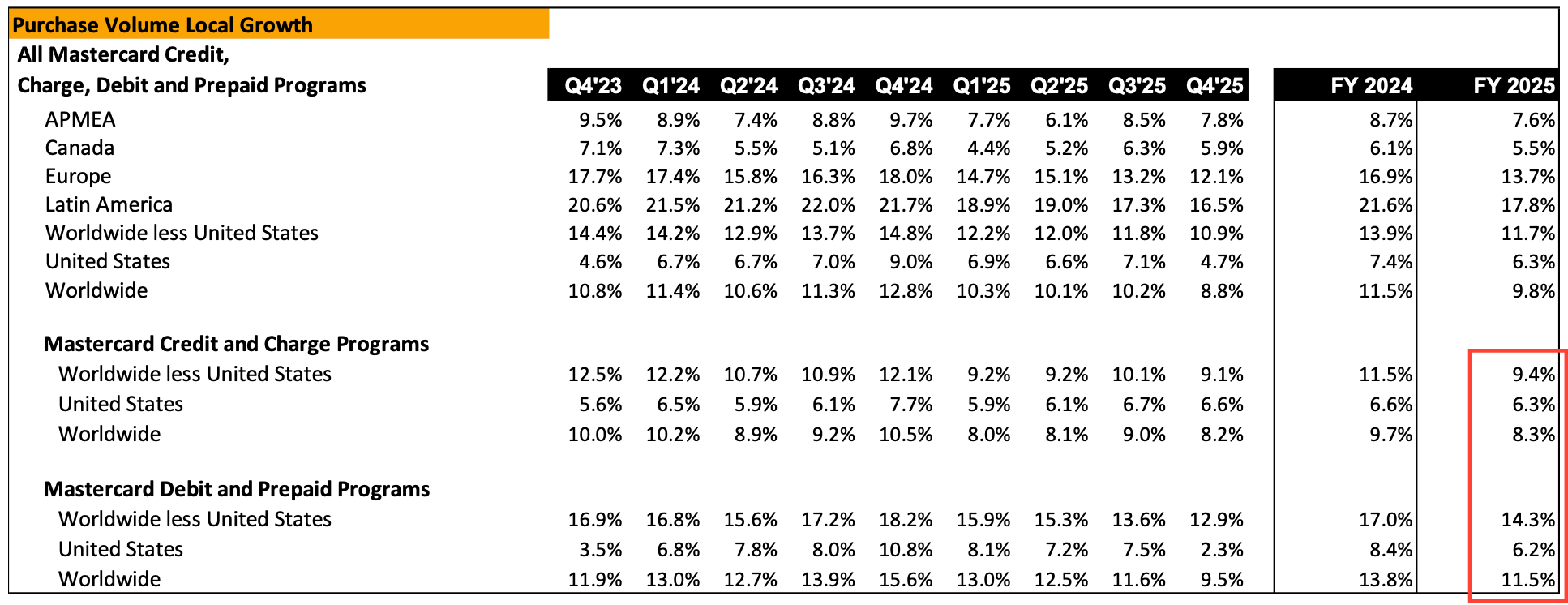

Debit growth of +11.5% was higher than credit +8.3%.

The gap is even greater for Worldwide (excl US) debit +14.3% versus credit +9.4%.

Debit is actually a big deal:

Contactless payments represent 45% of all debit card transactions, up from 38% the previous year.

Debit cards account for 53% in the US; 65% in Europe.

37% of US restaurant payments are by debit (33% credit; 16% cash).

Middle and lower income groups mainly use debit cards.

Recall that higher growth is in Europe & LATAM regions? Coincidentally, both are also debit-heavy.

This results in a reinforcing flywheel of debit card usage. The implications are important:

Debit has lower interchange economics than credit.

Debit has different fraud patterns.

Debit has different consumer value propositions, unlike credit card rewards optimization.

MA is facing some headwinds in debit. Capital One acquired Discover, and is migrating its debit card portfolio out of MA over to the Discover payment network — that’s why debit growth is only +2.3% in Q4 2025.

Some other headwinds include:

Market saturation with alternative payment methods taking share.

Digital wallet fragmentation creating routing optionality for merchants.

Consumers optimizing their spend across multiple rails.

Management acknowledged this in the earnings call but phrased it in a positive light:

We see a truly savvy and intentional consumer using their loyalty programs…

The harsh reality is that in a matured market, consumers have so many payment options that they’re choosing based on rewards, acceptance, and convenience. No single payment rail is automatically top choice. This is a departure from the early days of MA.

This is exactly why VAS fills in the gap printing rapid growth, outperforming the core payment network. As of Q1 2026, VAS net revenues grew +18% YOY (FX neutral) and now accounts for 40% of total net revenues.

Cross Border Payments

Back to this table… Cross-border volume overall grew at +14% in Q4. It’s a strong number, but the breakdown is interesting: XB CNP (cross-border card-not-present) excl travel grew +19%, while XB Travel grew only +11%.

This gap is not new.

The business model has changed structurally, cross-border transactions used to be dominated by travel but today it is no longer the case. The drivers of cross-border growth now are consumers buying from international e-commerce, businesses subscribing to foreign software platforms, gamers purchasing from international game publishers, and digital marketplaces connecting buyers and sellers across borders.

There are some important points:

They are all XB CNP transactions.

They are not seasonal unlike travel.

They require a completely different infrastructure than travel spending.

Travel spending was predictable in terms of seasonality, fraud patterns, and merchant categories.

On the other hand, digital cross-border is fragmented across all sorts of merchants. Fraud patterns also varies between different types of payments.

This is a tailwind for payment rails only if the infrastructure is present. For this, MA have built their disbursement and remittance platform in 2024: Mastercard Move.

This was a consolidation and rebranding of Mastercard Send and Mastercard Cross-Border Services. The equivalent for Visa is Visa Direct launched in 2015.

This is part of their fast growing Value Added Services (VAS) segment. It now reaches 17 billion endpoints with transaction growth of +35% in Q4 2025.

CEO Michael Miebach highlighted specific expansions during the Q4 earnings call, with the strategic partnerships:

Mastercard Move recipients had the option to receive funds across a variety of endpoints, including, but not limited to, bank accounts, debit cards, digital wallets, and cash if you want to. We continue to expand our network reach just recently by enabling bank account deposits in Bangladesh.

[…] expanding digital wallets and endpoints in Philippines (partnership with GCash), and in China (partnership with WeChat).

Strategic Positioning

From what we described above, it can be inferred that growth opportunities are outside of the US.

International payment flow developments include:

Real-time payment (RTP) infrastructure across LATAM, Asia, and Africa.

Open banking mandates pressure incumbents to modernize.

Digital identity frameworks enabling financial inclusion at scale.

Stablecoin regulation clarity in the US and Europe.

MA recognizes the change and have plans to embed themselves into the emerging infrastructure.

Examples:

MA operates an expansive, global network of over 100 stablecoin partners designed to bridge traditional fiat banking with blockchain technology.

MA facilitates RTP through the Mastercard Instant Payment Service (MIPS) and various global clearing networks.

MA partners with major global digital wallets (Apple Pay, Google Pay, Samsung Pay…) to enable tokenized, contactless transactions globally.

Digital payments are also increasingly cross-border, this trend is not going to reverse.

Consumers will continue to shop globally through e-commerce.

Digital goods like games and entertainment comes from all around the world.

Businesses are sourcing inventories overseas.

Software subscriptions are online and international.

Freedom of labour movement increases international remittances.

MA value proposition is seamless low cost payment flow. MA's advantage is their huge endpoint reach.

Instead of building separate, resource-intensive integrations for every single local bank switch or national scheme, merchants can integrate directly with the Mastercard Gateway API. The gateway intelligently routes the transaction to the corresponding domestic rail.

MA is connected to 90+ domestic schemes and 60+ card and wallet networks.

Below are some of the newer innovations:

MA processed $3.7b in stablecoin-linked card volume across 200+ countries in 2025. Monthly volume is at $2.5b annualized run rate, with the strongest growth in Colombia, Argentina, and Brazil.

Mastercard Agent Pay is an AI infrastructure that allows consumers to securely make purchases through autonomous AI agents. By verifying user consent and using tokenized credentials, it lets digital assistants handle everyday tasks (book rides, buy tickets…) directly within their chat interface.

Mastercard Transaction Stream, a new processing technology that speeds up the life cycle of payments. This benefits liquidity for small businesses.

We like MA's deliberate strategy calibrated to take advantage of these emerging international growth trends.