LOGC: ContextLogic

Special Situation

LOGC is trading at $210m market cap ($7.86/share, 26.7 million shares). As of Oct 2025, it has $218m in cash & marketable securities with zero total liabilities.

If you checked the stock chart, you would see a -99% drop from it's all time high $902/share. The company today is different from what it used to be, there is a story behind this hidden gem.

The story starts with a company many of you probably remember: Wish.com.

At its IPO in 2020, during peak pandemic e-commerce enthusiasm, Wish was valued at more than $14b. But the business model just wasn’t sustainable. It spent heavily on advertisements but couldn't produce earnings. Over time, the underlying economics caught up with it.

Eventually, the legacy Board and management team made the tough but correct decision to sell the business to Qoo10 for $173m in 2024.

They successfully undertook efforts to preserve ~$2.9b of net operating losses (NOL) plus other tax attributes.

CEO Rishi Bajaj from hedge fund Altai Capital was brought on the Board of directors and took on CEO role specifically to monetize these NOL in November 2023.

In February 2024, the Board adopted a Tax Benefits Preservation Plan to preserve and monetize the NOL.

Essentially this means LOGC has to acquire a profitable, tax paying company. That acquired business will have tax savings and become more valuable as a result of that, which is how the NOL gets monetized.

But there are tax rules which prevent companies from being acquired for their tax losses, helping ensure the tax benefit goes to owners who actually incurred the losses.

Under IRC Section 382, a change in ownership will impair the ability to use the NOL. “Change in ownership” is defined as:

More than 50 percentage points of stock ownership shift among 5% shareholders within a rolling 3-year period.

So the key to preserving NOL is to limit ownership changes in the owners with more than 5%. To avoid ownership change, they sold the assets of Wish rather than the equity. After the asset sale, the company essentially became a “shell corporation” with $218m investable cash and $2.7b of NOL.

We end up with the situation today after Wish was renamed to ContextLogic.

Permanent restrictions embedded directly into the certificate of incorporation, prohibiting any person or group from acquiring 4.9% or more of LOGC. That implies the maximum any entity can hold is $10.3m worth of shares, large institutions wouldn't bother with such a small quantum. So we are left with small retail investors, who are unlikely to be digging for such opportunities.

NOL Details

With $2.9b of NOL, at tax rate of 21%, LOGC can theoretically offset ~$609m of future taxes.

However, we need to cater for the present value (PV) of the NOL because it will take a period of time to monetize them, and management may not be successful in monetizing the entire amount.

The longer they take, the lower the PV.

Rishi Bajaj joined LOGC specifically to prevent the Board from selling the entire company as it would invalidate all the NOL.

To illustrate the value of the NOL, assume that LOGC buys a business for $300m trading at 10x earnings. That buys $30m of net income ($38m pre-tax @ 21% tax), of which 80% * $38m = $30.4m get shielded (only 80% can be shielded).

So, 21% * $30.4m = $6.4m is the tax saved by the NOL.

Next, assume that this business reinvests back at 10% returns, growing 10% every year. Then the tax offset will also grow 10%.

We can then do a DCF on the tax offset cashflows on 10 years with 10% discount rate, PV comes up to be $128m of tax savings.

In practice, if management are able to do a few decent acquisitions that are profitable (either in number or size of acquisitions), they should be able to utilise a good portion of the theoretical $609m tax savings from NOL.

Acquisition Strategy

So how were they going to do acquisitions without a operating business generating cash?

Enter BC Partners in February 2025.

They injected $150m of convertible preferred to execute an acquisition strategy. The explicit goal is to “capitalize on the embedded value within ContextLogic”, especially the NOL.

The company then reorganized into a two-tier structure consisting of a publicly traded holding company (PubCo: LOGC) and an underlying LLC where operations and investments occur.

Very shortly afterward, they met Abrams Capital, led by renowned investor David Abrams, along with his partner Raja Bobbili.

Both BC Partners (Mark Ward, Ted Goldthorpe) and Abrams Capital (David Abrams, Raja Bobbili) came together to set the organisation structure.

According to them, they were inspired by Swedish serial acquirers (eg. Lifco) and Berkshire.

Management has two core principles:

Every operating business that ContextLogic acquires will be run in a decentralized manner. Decisions should and will be made as close to the business as possible, by people who actually run it. Corporate exists as a support function, not a command center. Its job is to help the operators, not to micromanage them.

Only work with top-tier management teams and ensure their incentives are truly aligned with shareholders.

To identify target businesses, they look for three clear criteria:

Niche markets: Big enough to grow in but small enough to avoid competitive spotlight. As a general principle, strong businesses in small markets tend to be pretty good businesses.

Competitive advantages: “Obvious” competitive advantages. Not theoretical or “potential” future advantages. Actual, durable competitive strengths and positioning you can point to and understand.

Long-duration assets: Businesses that we expect to have a clear reason to exist 20 or 30 years from now. We’re building a long-term business ownership platform, not something we hope to flip in a couple of years.

Management goes on to explain what they will not pursue:

We’re equally clear about what we will not pursue.

We’re not pursuing big “TAMs” just because the market size looks impressive on a slide.

We’re not paying for “multiple expansion” in the hope that the market rerates the stock.

We’re not trying to ride “earnings momentum” or “future profitability” narratives.

We’re also not interested in “good enough” management teams or high growth at any price, or loose synergy stories, or grabbing whatever happens to be the trend of the moment.

We’re focused on durable, understandable businesses with real advantages.

Operationally, the structure will be decentralized. Each operating business runs autonomously with its own management team, while governance is kept close to operators through small, owner-affiliated Business Oversight Committees.

Capital allocation decisions are centralized at the Board level via an Investment Committee composed primarily of major equity owners: BC Partners and Abrams run by Ted Goldthorpe, David Abrams, Raja Bobbili and Mark Ward.

The focus is on capital allocation and M&A rather than day-to-day operations.

There will be no CEO, but rather, a president and a Board of 7 people, including Ted, David, Raja, Mark all of which will receive no salary or director compensation.

Incentives Structure

To align leaders in the operating businesses with shareholders, there are 3 components of incentives that are linked to value creation:

1. Base salary: straightforward fixed pay.

2. Annual bonus: based on year-over-year profit growth. Zero bonus if organic profit growth is below 5%.

3. Long-term incentive: based on profit growth over a five-year period, not capped, and expected to be paid in equity.

If a team delivers strong, sustained profit growth, they do very well. For managers, this really is the best of both worlds: private equity type incentives without the forced exit that pushes so many good companies to sell before their time.

LOGC will attract operators who want true pay-for-performance and the freedom to build against the backdrop of a long-term horizon and the backing of public capital markets.

Financial Model

Management is judged against free cashflow (FCF) per share, which they define as operating cashflow less all capital expenditures.

This is how they think about the compounding profile:

Operating businesses that can grow FCF organically at 5–10% over a long time.

Acquisitions 5–10% without equity issuance.

Incentive plan creates dilution 1–2% tied to financial performance.

So when we net it all out, the target is to compound FCF per share growth at 9–18% annually.

First Acquisition: US Salt

In early December 2025, Mark Ward (BC Partners) was appointed President and an agreement was reached to acquire US Salt for an enterprise value of $907.5m.

The US Salt financing package totals ~$922m:

Cash: ~$292m provided by LOGC, including the $150m convertibles from BC Partners. These can eventually be converted into class common shares in the PubCo.

Debt: $215m senior secured and $25m revolver led by Blackstone.

Rights offering (equity): ~$115m expected proceeds. Existing shareholder are given pro-rata rights, meaning, they can buy more to maintain the same % ownership after the new shares are issued. BC Partners and Abrams Capital backstopping the offering at $8, implying that institutional investors are willing to commit at that price.

Abrams Capital equity rollover: ~$315m rolls all of its existing US Salt equity into LOGC rather than cashing out. This materially reduces cash needs and signals long-term ownership intent.

Below is the capital structure post-acquisition:

Business Breakdown US Salt

Salt is a deceptively simple product, but the industry structure really matters.

There are three main forms of salt:

Rock

Solar

Evaporated

US Salt operates in the highest value, highest purity segment: Evaporated salt.

This has over 99% purity, low seasonality, and premium pricing many multiples of where Rock and Solar salt can sell. Within evaporated salt, they focus on the highest value niches.

They sell a significant amount of 26-ounce private label round can salt, and high-purity pharmaceutical grade salt which carries some of the highest prices in the entire industry because the standards are so strict and the qualification process is long and demanding.

Salt may sound like a commodity, but evaporated salt is absolutely not a commodity market. The barriers to entry are meaningful:

Reserve scarcity: Only a few basins in the US have the right combination of depth, purity, and access to energy and water. As far as we know, no new evaporated salt facility has been built in over 2 decades.

Geography: Salt has a low value-to-weight ratio, so shipping long distances erodes margins quickly. Domestic producers close to major demand corridors have a structural cost advantage. US Salt is ideally positioned in upstate New York with access to population corridors.

CAPEX and permitting: Building a new evaporated salt facility would require massive capital and years of permitting and regulatory approvals, if it is even possible to do near major population centers.

Regulatory and customer qualification: Pharmaceutical and food customers require extensive testing, audits, and documentation. It can take years to qualify a new supplier.

Because evaporated salt is a niche market, the economics are attractive for incumbents, but the total market size is too small to justify new competition given the CAPEX, permitting, and qualification hurdles.

Put simply: if you’re not already in this market, it’s not attractive to enter it.

The industry exhibits steady growth in pricing over 25 years on the back of nearly flat domestic evaporated salt supply.

Because supply is concentrated and doesn’t change much, and because demand is stable, pricing has been rational for decades.

Across all evaporated salt categories (bulk, pellets, packaged) we see steady upward pricing. It’s effectively an inflation-protected business.

For US Salt, volumes have grown steadily at ~1% annually, and closer to 5% more recently as they introduced new products and increased penetration in certain channels.

But the bigger story is that prices have increased consistently through a combination of pricing, mix shift, and new product introductions.

US Salt believes that a long-term goal of 5–10% annual organic profit growth is achievable.

Bringing this all back to LOGC acquisition strategy, US Salt fulfills their 3 criteria:

Niche: Operates in the highest-value segment of the salt market, with stable demand and rational pricing.

Competitively advantaged: Experience and location are an asset, from geology to regulatory approvals to specialized equipment.

Long-duration asset: This is a 130 year old business with ~100+ years of reserves remaining.

Although, the transaction won’t close until 1H2026, on a full-year basis management expects FCF of $31m to $38m (after all CAPEX).

Management Team

As mentioned earlier, two committees are formed to manage the corporation:

Investment committee: Responsible for determining how the company's cash flow and capital are deployed. It will be chaired by Ted Goldthorpe, and includes Raja Bobbili, David Abrams, and Mark Ward.

Business Oversight committee: Functions as a focused Board for the subsidiary, working closely with US Salt CEO David Sugarman to approve budgets, review financial performance, oversee key hires, and make compensation decisions. Composed of Raja Bobbili and Mark Ward.

David, Mark, Ted, and Raja will be aligned through their interests in BC Partners and Abrams Capital, and the performance of those funds. Both firms own an aggregate 60%, and the 4 men are the largest owners.

It is worth underscoring, the four of us represent the largest owners of the business. To reiterate, the whole structure is designed to keep governance focused and ownership minded.

Mark Ward

Some background of these 4 men:

Mark Ward (President, Director): Previously an analyst at Houlihan Lokey doing corporate restructuring, he’s now a director of credit at BC Partners.

Ted Goldthorpe: Ted is finance veteran with a distressed credit allocation background. He is the architect of the “NOL monetization + acquisition platform” strategy. Prior to founding BC Partners Credit arm, he spent 13 years at Goldman Sachs in special situations, and 4 years leading Apollo’s credit US opportunities platform.

David Abrams (Director): David is a seasoned investor with a 30+ year career, including experience at Baupost and decades running Abrams Capital. He has a value-driven philosophy, similar to Seth Klarman, whom he worked for early in his career.

Raja Bobbili (Chairman): Raja is a Managing Director/Partner at Abrams Capital. His expertise covers financials, communications, retail, and special situations. Raja will oversee the integration and performance of US Salt. LOGC is his single biggest personal holding.

In August 2025, Rishi Bajaj stepped down as CEO of LOGC to return to Altai Capital (his independent investment firm). He was granted 600,000 Class P units that only vest if LOGC 20-day average closing price reaches $30 per share by December 31, 2030. He will remain a key shareholder going forward, but he will not be economically decisive.

Later in December, CFO Michael Scarola, resigned to rejoin Altai Capital with Rishi Bajaj.

Valuation

We need to remember the capital structure post-acquisition.

Equity ownership is held at two levels:

PubCo shares (LOGC is what we can buy and is traded in the market)

LLC units (BC + Abrams)

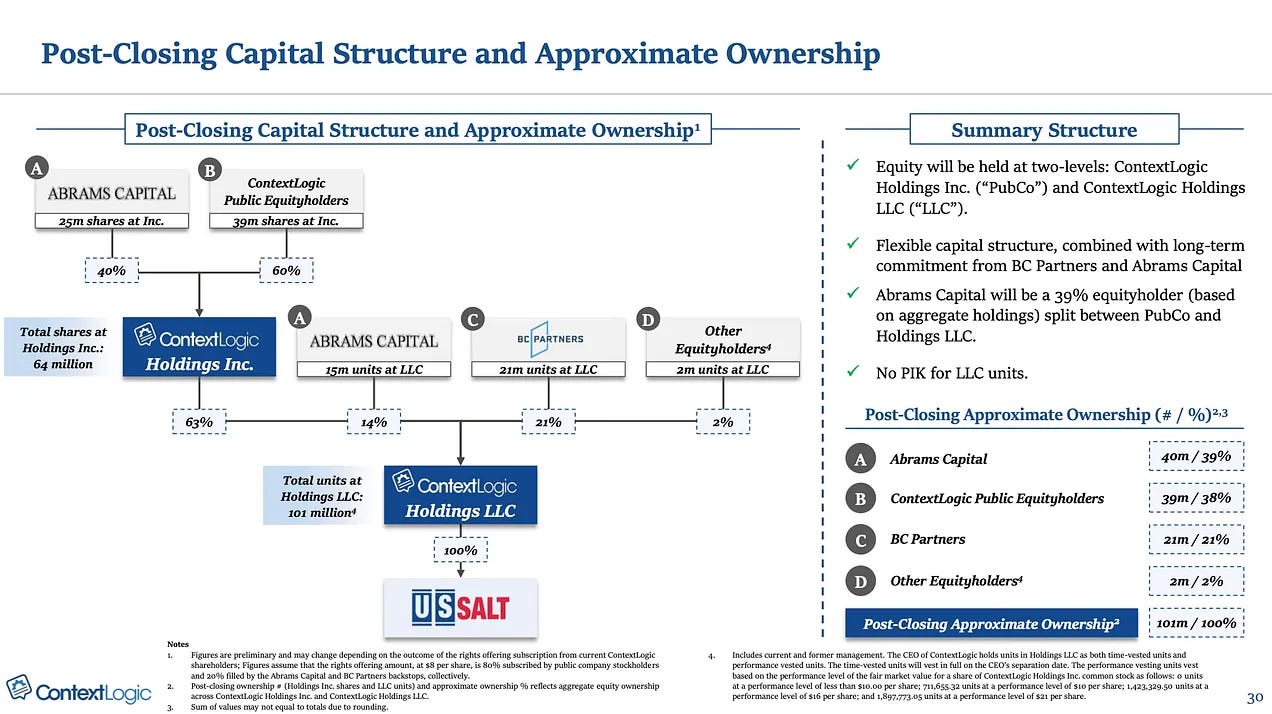

The LLC has a total of 101 million units, of which the PubCo owns 63% (64 million units).

PubCo will have a corresponding 64 million public shares outstanding after the deal closing. The remaining 37 million LLC units are held by BC Partners and Abrams Capital and may be exchanged into PubCo shares at their election, so long as it does not trigger “ownership change” as defined by IRC that invalidates the NOL.

Value of US Salt cashflows

US Salt sits entirely within the LLC and is expected to generate levered FCF of $31–38m. Because PubCo owns 63% of the LLC, its share of that FCF is $22–24m.

Divide by 64 million PubCo shares outstanding, we get FCF/share of $0.34–0.38.

If we apply a 15x multiple, FCF/share is worth $5.1–5.7.

Then we have the NOL treatment:

US Salt produces $37.5m pre-tax income.

Only 80% of income can be shielded in a given year. So $30m gets shielded.

At 21% tax rate, $30m * 21% = $6.3m tax saved.

Assume US Salt grows at 7% per year, terminal growth 2.5%. The PV of tax savings is ~$120m. PubCo share is ~$76m.

Divide by 64 million PubCo shares, we get NOL related to US Salt worth $1.2/share.

Adding #8 and #3 together, we get at least $6.3/share for US Salt.

That's a 25% premium to market price of LOGC shares of $7.86 (which is close to the $8 investors close to this situation believes it should be worth).

However, this analysis doesn't consider other value accretive acquisitions and utilisation of NOL.

Risk

The most obvious risk is bad acquisitions and/or taking too long to buy new businesses such that the PV of NOL goes down.

Conclusion

In short, we think at current price we are getting US Salt at a fair price and the rest of unutilised NOL for free.

Management's stated aim is to grow FCF/share at 9–18% annually. If LOGC demonstrates a few years of consistent FCF growth, the market will stop viewing it as a single asset holding company and start pricing in a well-run serial acquirer.

We think the risk-reward asymmetry is worth it. The opportunity could be time sensitive too!