History: First Ever Negative Coupon Note

Financial Meltdown

At the turn of the year 2000, financial markets saw some of the worst drawdowns in recent history. First came the bursting of the internet-bubble from 2000 to 2002, where the S&P500 index was cut in half and NASDAQ collapsed by 77%.

Then came the 9/11 terrorist attacks which halted trading for 6 days, this was the third time in history that the NYSE experienced prolonged closure, rivalling the longest closure for 4 months during World War 1, and the Great Depression which ended a period of speculative mania known as the “Roaring Twenties”.

To add insult to injury, Enron imploded in an accounting fraud which at that time was the largest bankruptcy in US history. Ironically Enron published a 64-page booklet called “Enron Code of Ethics”. The foreword was such a joke:

The Fed started aggressively cutting rates 11 times from 6.5% to 1.75% throughout 2001. Then in 2002, another 50bps cut brought rates down to 1.25%, as the economy struggled after the shocks of 9/11 and Enron.

Fears of deflation took hold and the Fed eventually took rates down to 1% in June 2003.

Safe Harbour: Berkshire Hathaway

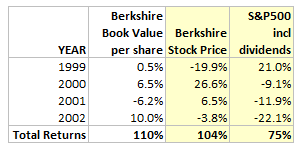

Amidst this crisis, Berkshire performed quite well against the market. If you look at the stock price movement, you will realize that it is totally detached from economic performance in the short-term.

For example in 1999, although Berkshire’s book value grew +0.5%, but tech stocks were the market’s darlings, and Berkshire’s stock price fell -19.9% reflecting this sentiment causing its largest underperformance relative to the S&P500:

However, as economic reality sets in, Berkshire’s stock price more accurately tracked it’s underlying growth in book value over time (see total returns).

Financial Engineering: SQUARZ

This was when Berkshire issued the SQUARZ notes on 15 November 2002, the first ever security in modern corporate history to carry a negative coupon. Despite the lack of precedent, the low interest rate environment and resilient Berkshire stock created a possible scenario to issue a negative coupon note, and so Buffett asked Goldman Sachs to create such an instrument and they responded promptly with this innovative security.

The total issuance was $400m carrying a negative interest rate in exchange for the right to purchase either 0.1116 Berkshire Class A or 3.348 Class B shares for $10,000 share prior to 15 May 2007.

It was broken up in $10,000 par value notes due in November 2007. Maturity was 5 years.

Holders pay Berkshire 3.75% annually for the right to receive 3% coupon and the option to buy shares within the 5 years. In other words, SQUARZ is a -0.75% interest rate note with warrants attached.

This note would only benefit you if Berkshire shares increased over the ensuing 5 years. If the share price decreased instead, you have the option to receive your cash back at maturity, after paying 0.75% annually for this privilege.

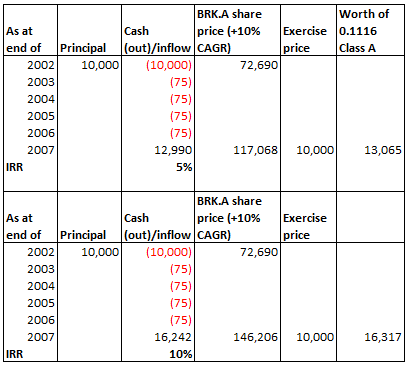

For a SQUARZ note holder, the IRR looked like this under 2 scenarios:

The advantages of SQUARZ notes were entirely in Berkshire’s favor, yet investors found them attractive (initial offer was $250m, increased to $400m) perhaps due to so many uncertain events that happened during that time.

For Berkshire, there were 4 benefits:

Upfront use of the cash.

Annual interest income from the negative interest rate.

Low effective cost if the notes were converted into shares.

3% payable to note holders reduces tax, while 3.75% collected from them is not taxable.

At the time (2002), Berkshire’s shares were trading at ~1.7x book value. After tech stocks got killed, it was Berkshire’s turn to became expensive.

The SQUARZ notes allowed Buffett monetize the situation by issuing shares at a lower cost. Investors also paid for this exposure to Berkshire’s shares with an option for cash in the event that shares fell in value.

Results

So what happened eventually?

Berkshire’s shares compounded at +14.3% until the eve of the 2008 Great Financial Crisis:

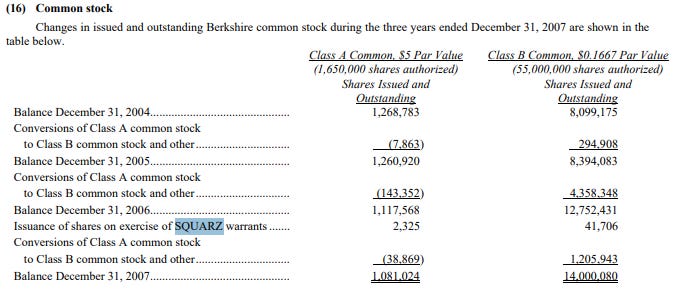

We can see the number of shares issued (3715 Class A equivalent) from investors exercising their warrants. In exchange, Berkshire received $333m.

If you subscribed to SQUARZ, converted and sold all shares at maturity, your IRR would be ~9%. Simply buying Berkshire’s shares would return you ~14% over the same period. Effectively, you paid ~1% per year for the optionality for getting your initial $10k back in the unlikely event that Berkshire shares fell.

For context, the S&P500 index total return was +12.8%.

that is quite a financial curiosity

For the optionality to convert into BRK shares at the end, does it mean BRK has to issue new stocks to discharge the obligation? How do the technicalities work?